Lake County, Florida

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NEW MEMBERS of the SENATE 1968-Present (By District, with Prior Service: *House, **Senate)

NEW MEMBERS OF THE SENATE 1968-Present (By District, With Prior Service: *House, **Senate) According to Article III, Section 15(a) of the Constitution of the State of Florida, Senators shall be elected for terms of 4 years. This followed the 1968 Special Session held for the revision of the Constitution. Organization Session, 1968 Total Membership=48, New Members=11 6th * W. E. Bishop (D) 15th * C. Welborn Daniel (D) 7th Bob Saunders (D) 17th * John L. Ducker (R) 10th * Dan Scarborough (D) 27th Alan Trask (D) 11th C. W. “Bill” Beaufort (D) 45th * Kenneth M. Myers (D) 13th J. H. Williams (D) 14th * Frederick B. Karl (D) Regular Session, 1969 Total Membership=48, New Members=0 Regular Session, 1970 Total Membership=48, New Members=1 24th David H. McClain (R) Organization Session, 1970 Total Membership=48, New Members=9 2nd W. D. Childers (D) 33rd Philip D. “Phil” Lewis (D) 8th * Lew Brantley (D) 34th Tom Johnson (R) 9th * Lynwood Arnold (D) 43rd * Gerald A. Lewis (D) 19th * John T. Ware (R) 48th * Robert Graham (D) 28th * Bob Brannen (D) Regular Session, 1972 Total Membership=48, New Members=1 28th Curtis Peterson (D) The 1972 election followed legislative reapportionment, where the membership changed from 48 members to 40 members; even numbered districts elected to 2-year terms, odd-numbered districts elected to 4-year terms. Organization Session, 1972 Redistricting Total Membership=40, New Members=16 2nd James A. Johnston (D) 26th * Russell E. Sykes (R) 9th Bruce A. Smathers (D) 32nd * William G. Zinkil, Sr., (D) 10th * William M. -

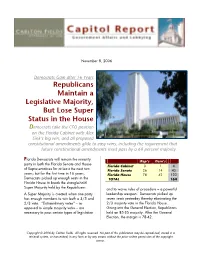

Capitol Report November 8, 2006

N ovem ber 8, 2006 Dem ocrats Gain after 16 Years Republicans M aintain a Legislative M ajority, But Lose Super Status in the House Dem ocrats take the CFO position on the Florida Cabinet with Alex Sink’s bi win! and all proposed constit"tional am endm ents lide to eas# wins! incl"din the re$"irem ent that f"t"re constit"tional am endm ents m "st pass b# a 6% percent m a&orit#' lorida D em ocrats w ill rem ain the m inority F Rep’s D em ’s party in both the Florida Senate and H ouse Florida Cabinet + # 4 of epresentatives for at least the ne!t tw o Florida Senate 26 #4 40 years" but for the first tim e in #6 years, Florida H ouse 38 42 #20 D em ocrats pic$ed up enou%h seats in the TO TA L 1 6 4 Florida H ouse to brea$ the stran%le&hold Super ' a(ority held by the epublicans) and to w aive rules of procedure 1 a pow erful * Super ' a(ority is created w hen one party leadership w eapon) D em ocrats pic$ed up has enou%h m em bers to w in both a +,- and seven seats yesterday thereby elim inatin% the 2,+ vote) ./!traordinary votes0 1 as 2,+ m a(ority vote in the Florida H ouse) opposed to sim ple m a(ority votes && are 2 oin% into the 2 eneral /lection, epublicans necessary to pass certain types of le%islation held an 8-&+- m a(ority) * fter the 2 eneral /lection, the m ar%in is 38&42) Copyright © 2006 by Carlton Fields. -

December 08.Indd

December 2008 www.FloridaPoolPro.com December 19 deadline Election Night Brings fast approaching Some Surprises By Jennifer Hatfi eld, Director of Government & Public Affairs By Kari Hebrank, FSPA Lobbyist, and Jennifer Hatfi eld, Director of Government & Public Affairs There are many questions websites. surrounding the implementation of The approximately 7,000 public The election results for the Florida vacated by Sen. Webster and kept the federal Virginia Graeme Baker pools/spas in Florida that have single House of Representatives and Florida SD 24, previously fi lled by Sen. Posey, Pool & Spa Safety Act (VGB Act) drain direct suction will be required by Senate races provided a few surprises. with former Rep. Altman beating within Florida and across the nation. the DOH to be retro-fi tted to gravity In the House races, the Democrats Democrat Moore. Additionally, Sen. The Consumer Product Safety drainage within the next four years. gained HD 10, formerly held by Carlton’s seat remained in Republican Commission (CPSC), charged with These pools/spas can either retro- Republican Will Kendrick, with Bembry hands with Republican candidate implementing and enforcing the VGB fi t to gravity drainage now to meet beating out the Republican candidate Detert capturing SD 23 over Democrat Act, and the Florida Department of the VGB Act and the pending DOH Curtis. The Democrats also picked Bentley. The Democrats managed to Health (DOH), continue to provide requirement, or use one of the other up HD 81 with Fetterman beating hold onto previously held democratic information on what they will require options found in the VGB Act as a Republican contender DiTerlizzi, a slots with Sen. -

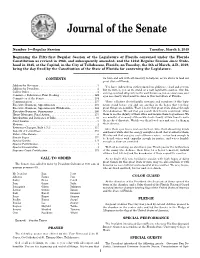

Journal of the Senate

Journal of the Senate Number 1—Regular Session Tuesday, March 5, 2019 Beginning the Fifty-first Regular Session of the Legislature of Florida convened under the Florida Constitution as revised in 1968, and subsequently amended, and the 121st Regular Session since State- hood in 1845, at the Capitol, in the City of Tallahassee, Florida, on Tuesday, the 5th of March, A.D., 2019, being the day fixed by the Constitution of the State of Florida for convening the Legislature. CONTENTS we turn and ask with all sincerity to help us, as we strive to lead our great State of Florida. Address by Governor . 3 You have endowed us with tremendous abilities to lead and govern, Address by President . 2 but we turn to you as we stand at a new legislative session. Our dis- Call to Order . .1 cerning eyes look diligently to the work before us, but we also know your Committee Substitutes, First Reading . 149 eyes see clearly what must be done in this vast State of Florida. Committees of the Senate . 174 Communication . 175 These collective elected public servants and members of this legis- Executive Business, Appointments . 172 lature stand before you and one another in the hopes that together, Executive Business, Appointments Withdrawn . 168 great things are possible. Their love for this great state shines through Executive Business, Suspensions . 160 their dedication. We ask that you search their hearts and minds. Allow House Messages, Final Action . 175 them to see the dignity of their office and inspire them to greatness. We Introduction and Reference of Bills . -

6:00 Pm 11 Expo Center 12 Orlando, Florida 13 14 15 16 1

Page 1 1 2 3 4 5 6 7 REAPPORTIONMENT PUBLIC HEARING 8 9 10 AUGUST 20, 2001 - 6:00 P.M. 11 EXPO CENTER 12 ORLANDO, FLORIDA 13 14 15 16 17 18 REPORTED BY: 19 KRISTEN L. BENTLEY, COURT REPORTER 20 Division of Administrative Hearings 21 DeSoto Building 22 1230 Apalachee Parkway 23 Tallahassee, Florida 24 25 Page 2 Page 4 1 MEMBERS IN ATTENDANCE 1 REPRESENTATIVE ALLEN TROVILLION 2 SENATOR GINNY BROWN-WAITE 2 REPRESENTATIVE MARK WEISSMAN 3 SENATOR LEE CONSTANTINE 3 REPRESENTATIVE FREDERICA S. WILSON 4 SENATOR ANNA P. COWIN 4 REPRESENTATIVE ROGER B. WISHNER 5 SENATOR MANDY DAWSON 5 6 SENATOR BUDDY DYER 6 7 SENATOR BETTY S. HOLZENDORF 7 8 SENATOR JAMES E. KING, JR. 8 9 SENATOR RON KLEIN 9 10 SENATOR JACK LATVALA 10 11 SENATOR JOHN F. LAURENT 11 12 SENATOR DURELL PEADEN, JR. 12 13 SENATOR BILL POSEY 13 14 SENATOR RONALD A. SILVER 14 15 SENATOR J. ALEX VILLALOBOS 15 16 SENATOR DEBBIE WASSERMAN-SCHULTZ 16 17 SENATOR DANIEL WEBSTER 17 18 REPRESENTATIVE BOB ALLEN 18 19 REPRESENTATIVE CAREY BAKER 19 20 REPRESENTATIVE GUS MICHAEL BILIRAKIS 20 21 REPRESENTATIVE RANDY BALL 21 22 REPRESENTATIVE MARSHA L. BOWEN 22 23 REPRESENTATIVE FREDERICK C. BRUMMER 23 24 REPRESENTATIVE JOHNNIE B. BYRD, JR. 24 25 REPRESENTATIVE FRANK ATTKISSON 25 Page 3 Page 5 1 REPRESENTATIVE LARRY CROW 1 PROCEEDINGS 2 REPRESENTATIVE JOYCE CUSACK 2 CHAIRMAN BYRD: The Joint Legislative Committee 3 REPRESENTATIVE DON DAVIS 3 meeting will now come to order. Thank you, ladies and 4 REPRESENTATIVE MARIO DIAZ-BALART 4 gentlemen, for coming to this meeting. -

Broward County

From the desk of . Gary Perkins, Executive Director Annual Guide to Government 2010 Florida Sheriffs Association CONTENTS FSA Officers and Board of Directors .......... 2 FSA Legislative Preview ............................. 4 Sheriffs of Florida/County Overview ........... 8 Directory of Law-Enforcement Agencies .. 36 Judicial Branch ......................................... 43 State Government Chart .......................... 50 Executive Branch ..................................... 52 Directory of State Agencies ...................... 54 Legislative Branch .................................... 60 Florida’s U.S. Senators and Representatives ............................. 66 Gary E. Perkins Sheriffs' addresses and phone numbers .............................. 72 October 1, 1949 – January 21, 2010 We will miss you... THE SHERIFF’S STAR January/February 2010, Volume 54, Number 1 Published since 1929 by the Florida Sheriffs Association (founded in 1893) Publisher Steve Casey, Executive Director Florida Sheriffs Association, Editor Julie S. Bettinger Editorial Coordinator Mary Jo Phillips Graphic Design Frank J. Jones In memory of Carl Stauffer Cover photo by Ray Stanyard, Tallahassee The Sheriff’s Star is published six times per year (January/ February, March/April, May/June, July/August, September/October and November/December) by the Florida Sheriffs Association, a non- profit corporation, P. O. Box 12519, Tallahassee, Florida 32317-2519 (street address, 2617 Mahan Drive). The subscription rate is $5 per year and the publication number is USPS 493-980. Periodicals post- age paid at Tallahassee, Florida and at additional mailing offices. POSTMASTER Please send address corrections to The Sheriff’s Star, P. O. Box 12519, Tallahassee, Florida 32317-2519. Copyright © 2010 by Florida Sheriffs Association. ISSN 0488-6186 E-mail: [email protected] • Web site: http://www.flsheriffs.org Phone (800) 877-2168 • Local (850) 877-2165 Fax (850) 878-8665 The Florida Sheriffs Association does not raise funds by telephone. -

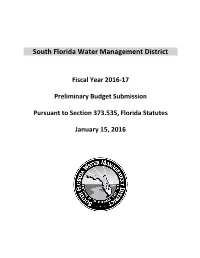

SFWMD FY2017 Preliminary Budget Submission

South Florida Water Management District Fiscal Year 2016-17 Preliminary Budget Submission Pursuant to Section 373.535, Florida Statutes January 15, 2016 South Florida Water Management District Governing Board Members Daniel O'Keefe, Chair Kevin Powers, Vice Chair Sam Accursio Rick Barber Sandy Batchelor Clarke Harlow Mitch Hutchcraft James J. Moran Melanie Peterson Pursuant to Section 373.535 F.S., the South Florida Water Management District’s Fiscal Year 2016-17 preliminary budget has been emailed to the following individuals. Florida Senate Office of Senate President President, Andy Gardiner – [email protected] Chief of Staff, Reynold Meyer - [email protected] Sr. Policy Advisor on Health, Carol Gormley – [email protected] Sr. Policy Advisor on Governmental Operations and the Environment, Lisa Vickers - [email protected]. Senate Committee on Appropriations Senator Tom Lee (R) Chair – [email protected] Senator Lizbeth Benacquisto (R) Vice Chair - [email protected] Staff Director, Cindy Kynoch - [email protected] Senate Appropriations Subcommittee on General Government Senator Alan Hays (R) Chair - [email protected] Senator Oscar Braynon (D) Vice Chair – [email protected] Staff Director, Jamie DeLoach - [email protected] Senate Committee on Environmental Preservation and Conservation Senator Charles S. "Charlie" Dean, Sr. (R) Chair - [email protected] Senator Wilton Simpson (R) Vice Chair – [email protected] Ellen Rogers, Staff -

March 2014 for Producing ESI – Part 1 Elliott Wilcox, Esq

A Publication of the Orange County Bar Association LaShawnda K. Jackson, Esq. The Hon. Faye L. Allen Rafael E. Martinez, Esq. Lawrence G. Mathews, Jr. Young Lawyer James G. Glazebrook Memorial William Trickel, Jr. Professionalism Award Professionalism Award Bar Service Award Inside this Issue: President’s Message Mediate ESI Issues Early and Technology Age: “The Best of Times Get Back to the Merits of Your Case and the Worst of Times” Lawrence H. Kolin, Esq. Paul J. Scheck, Esq. Presentation Skills Making Sense of E-Discovery: 10 Steps Destroy Your Relationship... With Technology! March 2014 for Producing ESI – Part 1 Elliott Wilcox, Esq. Vol. 82 No. 3 David P. Hathaway, Esq. The Orange County Bar Association April 5, 2014 7 O’Clock in the Evening The Alfond Inn in Winter Park, Florida TICKETS: $150 per person Sponsorships also Available To purchase tickets, please go to: ocba2014gala.brownpapertickets.com or contact the OCBA at 407-422-4551. For sponsorship information, contact Gala Chair Kimberly Webb at [email protected] All Proceeds to Benefit the Legal Aid Society and The Orange County Bar Foundation PRSRT STD U.S. POSTAGE 880 North Orange Avenue PAID MID-FL FL Orlando, Florida 32801 PERMIT NO. 581 Jonathan R. Simon Kerstin L. Morgan Michael J. Vaghaiwalla Refer Your Family Law Matters With Confidence Complimentary Consultations for All Referrals LITIGATION | MEDIATION | QDRO TheOrlandoFamilyFirm.com 121 S. Orange Avenue, Suite 1500 | Orlando, FL 32801 | 407.377.6399 For OCBA members, the training is free. For non-OCBA members participating in the LAS pro bono program, the training is free. -

2013 Regular Session of Issues the Florida Legislature

Voting Records Key Business 2013 Regular Session of Issues the Florida Legislature Champions2013 for BPageusiness 28 ASSOCIATED INDUSTRIES OF FLORIDA The Voice of Florida Business Since 1920 www.aif.com ASSOCIATED INDUSTRIES OF FLORIDA The Voice of Florida Business Since 1920 Dear Employer: It is my pleasure to provide you with this tabulation of the voting conduct of each member of the Florida Legislature during the 2013 Regular Session. Voting Records reports on the votes made by every legislator on bills that were lobbied, advocated, promoted or opposed by Associated Industries of Florida. By reporting on 10,451 votes cast by legislators on 89 bills, this publication embodies the most exhaustive Tom C. Feeney President & and complete record of the Legislature’s approach to the concerns of Florida’s employers. Chief Executive Officer We go to great lengths to ensure that legislators are aware of AIF’s positions on issues of great importance to the business community. Every year before the session begins, we produce AIF’s Session Priorities, which explains why we support or oppose key issues. In addition, during the session we provide each legislator with a Daily Brief on the activities of that day, highlighting bills of interest to business and our positions on those issues. Our greatest asset, however, is our experienced and accomplished legislative team, which has compiled a record of success second to none. For 38 years, AIF has published Voting Records, an analysis of every vote cast by every legislator on major business issues. Yet voting records only tell part of the story. -

Florida Parole Commission

FLORIDA PAROLE COMMISSION lll A Governor and Cabinet Agency Created in 1941 ~Seventy Years of Service to the Citizens of Florida~ ANNUAL REPORT 2010-2011 Tena M. Pate, Chair - 0 - Table of Contents MISSION STATEMENT ………………………………………………………………………………………….. 3 FLORIDA BOARD OF EXECUTIVE CLEMENCY ……………………….……………………………….. 3 CENTRAL OFFICE HEADQUARTERS …………………….…….…………………………………………… 4 CHAIR’S MESSAGE …………………………………………………..…………………………………………… 5 SELECTED ACTIVITIES …………………………………………………………………………………………… 6 COMMISSIONERS’ VITAE ………………………………………………...…………………………………… 9 AGENCY AND EMPLOYEES RECOGNIZED FOR EXCELLENCE ………………………………….. 14 HISTORY OF THE COMMISSION ………………………………………..…………………………………. 17 FACTS ABOUT THE COMMISSION …………………………………….………………………………….. 22 HEARING DAY ACTIVITIES ……………………….….……………………………………………………….. 24 YEAR IN SUMMARY: Performance Measures ……….................................................. 25 YEAR IN SUMMARY: Statistics …………………………………………………………………………….. 27 PROGRAM COMPONENTS ………………………..…………………….…..………………………………. 29 DIVISIONS AND OFFICES Division of Operations ……………………………………………………................................... 34 Release Services ………………………………………..……........................................... 36 Revocations …………..………………………………………………….……….……………………. 37 Special Projects …………….……………………………………………............................... 40 Victims' Services ………..……………………………………….……….............................. 41 Field Services ………………………………………………….………................................... 44 Division of Administrative Services ………………………………….…...…………………………. 48 Human -

Remarks in New Port Richey, Florida October 19, 2004

Administration of George W. Bush, 2004 / Oct. 19 families had been turned upside down be- On September the 14th, 2001, I stood in cause of death in World War II. But there the ruins of the Twin Towers. It’s a day was this belief in the country that if we I will never forget. There were workers helped Japan become a democracy, the in hardhats yelling at me at the top of world would be better off for it. Today, their lungs, ‘‘Whatever it takes.’’ I remem- because people held that belief, I sit at ber the fellow who grabbed me by the arm. the table with the Prime Minister of a He looked me straight in the eye, and he former enemy, talking about how to keep said, ‘‘Do not let me down.’’ Ever since the peace we all want. that day, I wake up every morning thinking Someday, someday, an American Presi- about how to better protect America. I will dent will be sitting down with the duly never relent in defending our country, elected leader from Iraq, talking about the whatever it takes. peace, and our children and our grand- Four years ago, when I traveled your children will be better off for it. great State, I made a pledge that if you I believe that millions in the Middle East gave me the chance to serve, I would up- plead in silence for their freedom. I believe hold the honor and the dignity of the office women in the Middle East want to live to which I had been elected. -

Rulebook 11 18 04 REVISED2 (2).Qxd

Rules and Manual of the SENATE of the STATE OF FLORIDA Senator Tom Lee President 2004-2006 As adopted November 16, 2004 and subsequently amended March 10, 2005 and March 7, 2006 Updates to the Florida Senate Rules and Manual 2004-2006 June 26, 2006 Page UPDATES number(s) cover and subsequently amended March 10, 2005 and March 7, 2006 11-83 Senate Rules As amended March 10, 2005 and March 7, 2006 95-109 Joint Rules As adopted March 7, 2006 111 Committees of the Senate Current composition 115 Committee Assignments Current composition CONTENTS Senate Officers and Committee on Rules and Calendar . 1 Members of the Senate . 3 Senate Rules — Table of Contents . 5 Rules of the Senate . 11 Germanity Standards and Common Motions . 85 Joint Rules — Table of Contents . 92 Joint Rules of the Florida Legislature . 95 Committees of the Senate . 111 Joint Legislative Committees . 113 Committee Assignments . 115 Index to Senate Rules and Joint Rules of the Florida Legislature . 123 Constitution of the State of Florida . C-1 Index to the Constitution of Florida . C-53 Vote Required – Senate Rules and Constitution of Florida SENATE OFFICERS 2004-2006 (As of May 1, 2006) President: Senator Tom Lee President Pro Tempore: Senator Charlie Clary Majority (Republican) Leader: Senator Daniel Webster Minority (Democratic) Leader: Senator Lesley “Les” Miller, Jr. Minority (Democratic) Leader Pro Tempore: Senator Walter G. “Skip” Campbell, Jr. Secretary: Faye W. Blanton COMMITTEE ON RULES AND CALENDAR Senator Ken Pruitt, Chair Senator Nancy Argenziano, Vice Chair Senator Walter G. “Skip” Campbell, Jr. Senator Lisa Carlton Senator Charlie Clary Senator Lee Constantine Senator Alex Diaz de la Portilla Senator Paula Dockery Senator Rudy Garcia Senator Steven A.