Contactless Payments Rising

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

VX690 User Manual

Sivu 1(36) 28.9.2016 VX690 User Manual English Author: Verifone Finland Oy Date: 28.9.2016 Pages: 20 Sivu 2(36) 28.9.2016 INDEX: 1. BEFORE USE ............................................................................................................................... 5 1.1 Important ......................................................................................................................................... 5 1.2 Terminal Structure ......................................................................................................................... 6 1.3 Terminal start-up and shutdown .................................................................................................. 6 1.4 Technical data ................................................................................................................................ 7 1.5 Connecting cables ......................................................................................................................... 7 1.6 SIM-card.......................................................................................................................................... 8 1.7 Touchscreen ................................................................................................................................... 8 1.8 Using the menus ............................................................................................................................ 9 1.9 Letters and special characters.................................................................................................... -

First Washington Associates Washington, D.C. December,,: 198

5 1- BANK JAMAICA/U.S. FULL SERVICE MERCHANT DEVELOPMENT CONCEPT-PAPER' Prepared by First Washington Associates Washington, D.C. December,,: 198 .2.1 TABLE!OF CONTENTS Page 1. Concept. * 1* II. Economic Climate and Private Investment . .4 III. Existing Financial Infrastructure ..... 7 IV. Activities of the New Bank . ... 13 V. Formation, Ownership, and Capitalization ,19 VI. Direction and Management,. .. " .22 VII. Implementation . ' .• ****25 0-H- I. CONCEPT 1. This discussion paper has been prepared at the,, request of the Bureau for Private Enterprise (PRE) and the Jamaican Mission of the U.S. Agency for International Development (AID) and is intended to describe the role which a new Jamaica/U.S. Full-Service Merchant Development Bank can play in helping achieve economic development and growth through expansion and stimulation of the private sector in Jamaica. 2. Under the Government of Prime Minister Seaga, Jamaica has embarked upon a serious, across-the-board program of measures to encourage expansion of private sector productivity and output and lead to substantial new investments in agri culture, manufacturing, and related service industries. The private sector is looked upon as the major driving force for economic rehabilitation, and investments from the United States and local entrepreneurs are being counted upon to bring new vitality and diversification to the Jamaican economy, reverse the outward flow of private capital, transfer new technologies, and help solve the country's balance of payments and unemployment problems. 3. Seriously limiting the achievement of these goals is the lack of an adequate institutional infrastructure to provide equity funding and aggressive medium- and long-term credit facilities to stimulate capital investment. -

BR-69915-210X297mm-Update the UBS Securities China Brochure

UBS Securities First foreign-invested fully-licensed securities firm in China, 51% owned by UBS AG He Di Eugene Qian UBS Securities Co., Limited (UBS Securities) was incorporated on 11 December 2006 following the restructuring of Beijing Securities Co., Limited. In December 2018, UBS AG increased its shareholding in UBS Securities to 51%; the first time that a foreign financial institution had raised its stake to take majority control of a securities joint venture in China. With the support of the UBS Group and the dedication of our employees, UBS Securities remains at the forefront of the industry as the first foreign-invested fully-licensed securities firm in China. Client-centric and committed to the pursuit of excellence and sustainable performance, UBS Securities relies on international experience complemented by local expertise to maintain its market- leading position. Our success would not have been possible without our employees. We would also like to thank our clients, shareholders, business partners, as well as government and regulatory bodies for their support which has been a driving force for the business. Our market position today is a strong foundation for the decades to come. We are determined to build on our core strengths to capture the opportunities arising from ongoing wealth creation, market reforms and globalization in China. We will continue to offer world-class products, services and advice to our clients, and work with all stakeholders towards the further development of China’s financial markets. Very best wishes. He Di Eugene Qian Chairman President UBS Securities UBS Securities 2 Milestones Moving forward December 2018 UBS AG increased its shareholding in UBS Securities to 51%, first international bank to increase stake to take majority control in a China securities joint venture. -

Acquiring – Terms and Conditions 2020

Acquiring – Terms and Conditions 2020 nets.eu/payments Contents DEFINITIONS ........................................................................................................................................................................................................................................................................3 1. SCOPE OF THE AGREEMENT ....................................................................................................................................................................................................................5 2. GENERAL REQUIREMENTS APPLICABLE TO THE MERCHANT ...........................................................................................................................................5 3. ACCEPTANCE OF PAYMENT CARDS .....................................................................................................................................................................................................8 4. THE RELATIONSHIP BETWEEN THE MERCHANT AND THE CARDHOLDER ..............................................................................................................10 5. PRICES, PAYMENTS AND SETTLEMENTS ......................................................................................................................................................................................10 6. DISPUTED CARD PAYMENTS ..................................................................................................................................................................................................................11 -

Tap on Phone Implementation Guide February 2021

Tap on Phone Implementation Guide February 2021 © 2020 Mastercard. Proprietary and Confidential. | 1 Contents 1: Overview .................................................................................................................................................................... 3 1.1 What is Tap on Phone? ......................................................................................................................................................................... 3 1.2 Who is this guide for? ........................................................................................................................................................................... 3 1.3 What is this guide intended for? ......................................................................................................................................................... 3 2: Process ....................................................................................................................................................................... 4 2.1 PCI timeline ............................................................................................................................................................................................ 4 2.2 Suggested market criteria .................................................................................................................................................................. 4 2.3 Solution options ................................................................................................................................................................................... -

National Payment System Development Strategy for 2021 – 2023

NATIONAL PAYMENT SYSTEM DEVELOPMENT STRATEGY FOR 2021 – 2023 Moscow 2021 CONTENTS Introduction .......................................................................................................................... 2 1. Current status of the NPS ............................................................................................... 4 1.1. Regulation ..................................................................................................................................................................................4 1.2. NPS infrastructure .................................................................................................................................................................5 1.3. Payment service providers ................................................................................................................................................9 1.4. Payment service consumers ..........................................................................................................................................10 2. Global and domestic trends and challenges of the payment market ......................13 2.1. Transformation of client experience and consumption models .....................................................................13 2.2. New payment technologies ...........................................................................................................................................13 2.3. New payment market participants .............................................................................................................................14 -

Know Your Customer Form

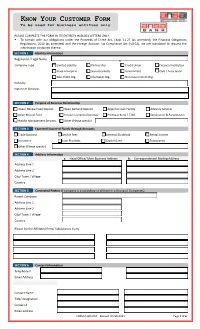

KNOW Y OUR C USTOMER F ORM To be used for business entities only PLEASE COMPLETE THE FORM IN ITS ENTIRETY IN BLOCK LETTERS ONLY . To comply with our obligations under the Proceeds of Crime Act, Chap. 11.27 (as amended), the Financial Obligations Regulations, 2010 (as amended) and the Foreign Account Tax Compliance Act (FATCA), we are mandated to request the information contained therein. SECTION 1 Identity Information Registered / Legal Name Company Type Limited Liability Partnership Credit Union Financial Institution State Enterprise Statutory Body Government Club / Association Non-Profit Org. Charitable Org. Non-Government Org. Industry Nature of Business SECTION 2 Purpose of Business Relationship Open/ Renew Fixed Deposit Open Demand Deposit Apply for Loan Facility Advisory Services Open Mutual Fund Foreign Currency Exchange Purchase Bond / T-Bill Syndication & Participation Wealth Management Services Other (Please specify) SECTION 3 Expected Source of Funds through Accounts Trade Business Service Fees Interest/ Dividends Rental Income Donations Loan Proceeds Capital Gains Subsidiaries Other (Please specify) SECTION 4 Address Information a. Head Office/ Main Business Address b. Correspondence/ Mailing Address Address Line 1 Address Line 2 City/ Town / Village Country SECTION 5 Connected Parties (if company is a subsidiary or affiliate in a Group of Companies) Parent Company Address Line 1 Address Line 2 City/ Town / Village Country Please list the Affiliated firms/ Subsidiaries if any SECTION 6 Contact -

Virtual Card Management Service (VCM) Built to Support Payment from Any Device

Virtual Card Management Service (VCM) Built to support payment from any device EASY DEPLOYMENT Nets’ VCM is designed to easily integrate with your existing payment Fast time to market for platform, ensuring compatibility with your current processes for card mobile payment solutions. management. Payment technologies, schemes, wallet types and Virtual card management in place for easy integration functionalities are included in a single API – making it fast and easy to with your core services. implement, integrate and deploy a strong solution. REACH THIS SERVICE IS BASED ON: 50+ banks already • A personal user experience for your • Full card management on individual virtual on board. Independent of customers through smart customisa- card level in accordance with industry stand- payment technology with ble self-service features. ards. full control and transparen- • A one-stop solution including all • Secure processes for critical card manage- cy from a card is virtualised necessary features for virtual card life ment functions such as card virtualisation, until it expires. cycle management. passcode reset, etc. through integration to customer provided cardholder identification EASY AND SECURE • A highly secure and constantly availa- and authentication security processes. The virtual card ble mobile payment solution ensuring • A fully fledged API to enhance user experi- management service is a reliable solution for your customers. ence based on customer preferences. based on industry stand- ards in addition to PCI DSS • A fast and smooth deployment solu- and PCI CPP compliance tion that integrates with your existing The ability to manage and control virtual cards regarding card management life cycle management process. is crucial for you as a card issuer as it enables and control. -

Financial Crimes Enforcement Network

Federal Register / Vol. 69, No. 163 / Tuesday, August 24, 2004 / Proposed Rules 51979 (3) Covered financial institution has to document its compliance with the include the agency name and the the same meaning as provided in notice requirement set forth in Regulatory Information Number (RIN) § 103.175(f)(2) and also includes: paragraph (b)(2)(i)(A) of this section. for this proposed rulemaking. All (i) A futures commission merchant or (ii) Nothing in this section shall comments received will be posted an introducing broker registered, or require a covered financial institution to without change to http:// required to register, with the report any information not otherwise www.fincen.gov, including any personal Commodity Futures Trading required to be reported by law or information provided. Comments may Commission under the Commodity regulation. be inspected at FinCEN between 10 a.m. Exchange Act (7 U.S.C. 1 et seq.); and Dated: August 18, 2004. and 4 p.m., in the FinCEN reading room (ii) An investment company (as in Washington, DC. Persons wishing to William J. Fox, defined in section 3 of the Investment inspect the comments submitted must Company Act of 1940 (15 U.S.C. 80a–5)) Director, Financial Crimes Enforcement request an appointment by telephoning Network. that is an open-end company (as defined (202) 354–6400 (not a toll-free number). [FR Doc. 04–19266 Filed 8–23–04; 8:45 am] in section 5 of the Investment Company FOR FURTHER INFORMATION CONTACT: Act (15 U.S.C. 80a–5)) and that is BILLING CODE 4810–02–P Office of Regulatory Programs, FinCEN, registered, or required to register, with at (202) 354–6400 or Office of Chief the Securities and Exchange DEPARTMENT OF THE TREASURY Counsel, FinCEN, at (703) 905–3590 Commission under section 8 of the (not toll-free numbers). -

NETS and Comfortdelgro Launch Convenient In-App Payment for NETS Users

Media Release NETS and ComfortDelGro launch convenient in-app payment for NETS users NETS Click, the new in-app payment method enables consumers to use NETS bank cards on apps such as the ComfortDelGro Taxi Booking App for seamless and hassle-free payments Singapore, October 31, 2019 – NETS and ComfortDelGro Taxi today announced the launch of NETS’ new in-app payment method for taxi bookings and street hail trips made through the ComfortDelGro Taxi Booking App. Named NETS Click, the initiative enables consumers to use their NETS bank cards from DBS, OCBC and UOB to conveniently pay for both mobile booking and street hail trips with ComfortDelGro taxis via the ComfortDelGro Taxi Booking App. The partnership with ComfortDelGro Taxi marks the first time consumers can store NETS payment details on file to use their NETS bank card as an in-app payment mode. NETS will soon partner with online merchants to integrate NETS Click into their in-app payment process, providing consumers another option when they make payments for their purchases on their mobile devices. To use NETS Click for ComfortDelGro taxi rides, passengers can add their NETS bank card to the ComfortDelGro Taxi Booking App and authenticate their identity with a one- time password sent to their registered mobile number. Subsequently, NETS can be selected as the in-app payment option for ride bookings made via the app or street hail. For street hail trips, passengers would need to select the ‘Pay for Street Hail’ option on the ComfortDelGro Taxi Booking App. When they have boarded the hailed taxi, they may select NETS Click as the payment method on the app. -

Contactless Card Facts

CONTACTLESS CARDS FAQs What’s the benefit of a contactless card and tapping to pay? Tapping to pay with a contactless card helps you avoid touching surfaces at checkout. It’s safe, easy and secure — perfect for places like fast-food restaurants, grocery stores, coffee shops, vending machines, taxis and more. Tapping to pay is also secure because just like a chip card, each transaction is accompanied by a one-time code that protects your payment information. Unlike cash, tapping to pay provides an electronic record of your purchases and gives you all the great functionality and convenience of a Visa card. How do I know if my card is contactless? Contactless cards will contain the Contactless Indicator on the back (Classic and Business) or the front (Platinum) of the card. How will I know if a payment terminal accepts contactless cards? Contactless payment-enabled devices will display the Contactless Symbol . How do I pay with a contactless card? Follow these 3 steps: 1. Look – Make sure your card has the Contactless Indicator on it, then find the Contactless Symbol at checkout. 2. Tap - When prompted, simply tap your Visa contactless card over the Contactless Symbol to make a payment. 3. Go - Your payment is processed in seconds. Once your payment is confirmed, you’re good to go. What is the technology behind tap to pay? Tap to pay uses short-range wireless technology to make secure payments between a contactless card or payment-enabled device and a contactless-enabled checkout terminal. When you tap near the Contactless Symbol , your payment is sent for authorization. -

ATM & NETS Link Frequently Asked Questions

ATM & NETS Link Frequently Asked Questions 1. What do you mean by linking of my DBS/POSB current/savings account to my DBS/POSB Credit Card? When you link your DBS/POSB current/savings account to your DBS/POSB Credit Card, ATM and NETS functions are made available on your DBS/POSB Credit Card. 2. What are the benefits of doing the linkage? • Save wallet space with one Card, reduce the need to carry many Cards around. • Perform ATM card functions such as cash withdrawal from your DBS/POSB current/savings account with your DBS/POSB Credit Card. • Enjoy the convenience of NETS with your DBS/POSB Credit Card at more than 70,000 NETS acceptance points. 3. How do I apply for this linkage? You can log into your digibank via internet or mobile banking to apply. You can visit https://www.dbs.com.sg/personal/support/card-application-link-card-to-deposit-account.html for more details. Please allow up to 5 working days for processing. 4. How will I know if the linkage is successful? An SMS or letter will be sent to notify you upon the successful linkage of DBS/POSB current/savings account to your DBS/POSB Credit Card. 5. When I sign for my transactions via American Express®/MasterCard®/Visa on this linked Credit Card, will it be considered as a Credit Card transaction? Yes. When you sign for your transactions with your linked Credit Card, it will be considered a Credit Card transaction. Only when you make NETS transactions, the purchase would be debited from your DBS/POSB current/savings account linked to your DBS/POSB Credit Card.