Download the Full GTC ONE Minute Brief

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1332 Nippon Suisan Kaisha, Ltd. 50 1333 Maruha Nichiro Corp. 500 1605 Inpex Corp

Nikkei Stock Average - Par Value (Update:August/1, 2017) Code Company Name Par Value(Yen) 1332 Nippon Suisan Kaisha, Ltd. 50 1333 Maruha Nichiro Corp. 500 1605 Inpex Corp. 125 1721 Comsys Holdings Corp. 50 1801 Taisei Corp. 50 1802 Obayashi Corp. 50 1803 Shimizu Corp. 50 1808 Haseko Corp. 250 1812 Kajima Corp. 50 1925 Daiwa House Industry Co., Ltd. 50 1928 Sekisui House, Ltd. 50 1963 JGC Corp. 50 2002 Nisshin Seifun Group Inc. 50 2269 Meiji Holdings Co., Ltd. 250 2282 Nh Foods Ltd. 50 2432 DeNA Co., Ltd. 500/3 2501 Sapporo Holdings Ltd. 250 2502 Asahi Group Holdings, Ltd. 50 2503 Kirin Holdings Co., Ltd. 50 2531 Takara Holdings Inc. 50 2768 Sojitz Corp. 500 2801 Kikkoman Corp. 50 2802 Ajinomoto Co., Inc. 50 2871 Nichirei Corp. 100 2914 Japan Tobacco Inc. 50 3086 J.Front Retailing Co., Ltd. 100 3099 Isetan Mitsukoshi Holdings Ltd. 50 3101 Toyobo Co., Ltd. 50 3103 Unitika Ltd. 50 3105 Nisshinbo Holdings Inc. 50 3289 Tokyu Fudosan Holdings Corp. 50 3382 Seven & i Holdings Co., Ltd. 50 3401 Teijin Ltd. 250 3402 Toray Industries, Inc. 50 3405 Kuraray Co., Ltd. 50 3407 Asahi Kasei Corp. 50 3436 SUMCO Corp. 500 3861 Oji Holdings Corp. 50 3863 Nippon Paper Industries Co., Ltd. 500 3865 Hokuetsu Kishu Paper Co., Ltd. 50 4004 Showa Denko K.K. 500 4005 Sumitomo Chemical Co., Ltd. 50 4021 Nissan Chemical Industries, Ltd. 50 4042 Tosoh Corp. 50 4043 Tokuyama Corp. 50 WF-101-E-20170803 Copyright © Nikkei Inc. All rights reserved. 1/5 Nikkei Stock Average - Par Value (Update:August/1, 2017) Code Company Name Par Value(Yen) 4061 Denka Co., Ltd. -

1332:Xtks Nippon Suisan Kaisha Ltd 3 4 1 1334:Xtks Maruha Nichiro Holdings Inc. 3 4 1 1377:Xtks Sakata Seed Corp. 3 5 2 1414:Xtks SHO-BOND Holdings Co

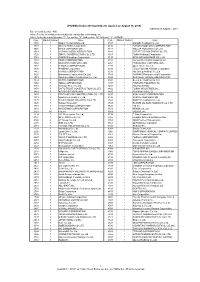

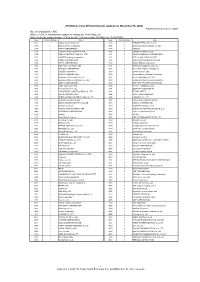

Symbol Code Description Current Rating New rating Diff 1332:xtks Nippon Suisan Kaisha Ltd 3 4 1 1334:xtks Maruha Nichiro Holdings Inc. 3 4 1 1377:xtks Sakata Seed Corp. 3 5 2 1414:xtks SHO-BOND Holdings Co. Ltd 3 6 3 1766:xtks TOKEN Corp. 3 6 3 1801:xtks Taisei Corp. 3 5 2 1803:xtks Shimizu Corp. 3 4 1 1808:xtks Haseko Corp. 3 4 1 1812:xtks Kajima Corp. 3 5 2 1820:xtks Nishimatsu Construction Co. Ltd 3 6 3 1824:xtks Maeda Corp. 3 6 3 1833:xtks Okumura Corp. 3 6 3 1860:xtks Toda Corp. 3 5 2 1861:xtks Kumagai Gumi Co. Ltd 3 8 5 1865:xtks Asunaro Aoki Construction Co. Ltd 3 6 3 1870:xtks Yahagi Construction Co. Ltd 3 4 1 1881:xtks NIPPO Corp. 3 6 3 1883:xtks Maeda Road Construction Co. Ltd 3 6 3 1911:xtks Sumitomo Forestry Co Ltd 3 4 1 1924:xtks PanaHome Corp. 3 4 1 1925:xtks Daiwa House Industry Co. Ltd 3 4 1 1928:xtks Sekisui House Ltd 3 4 1 1934:xtks YURTEC Corp. 3 6 3 1945:xtks Tokyo Energy & Systems Inc. 3 4 1 1961:xtks Sanki Engineering Co. Ltd 3 4 1 1963:xtks JGC Corporation 3 4 1 1968:xtks Taihei Dengyo Kaisha Ltd 3 4 1 1969:xtks Takasago Thermal Engineering Co. Ltd 3 4 1 1973:xtks NEC Networks & System Integration Corp. 3 5 2 1979:xtks Taikisha Ltd 3 4 1 1983:xtks TOSHIBA PLANT SYSTEMS & SERVICES Corp. -

"JPX-Nikkei Index 400"

JPX-Nikkei Index 400 Constituents (applied on August 30, 2019) Published on August 7, 2019 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3107 1 Daiwabo Holdings Co.,Ltd. 1333 1 Maruha Nichiro Corporation 3116 1 TOYOTA BOSHOKU CORPORATION 1605 1 INPEX CORPORATION 3141 1 WELCIA HOLDINGS CO.,LTD. 1719 1 HAZAMA ANDO CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3167 1 TOKAI Holdings Corporation 1721 1 COMSYS Holdings Corporation 3197 1 SKYLARK HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1802 1 OBAYASHI CORPORATION 3254 1 PRESSANCE CORPORATION 1803 1 SHIMIZU CORPORATION 3288 1 Open House Co.,Ltd. 1808 1 HASEKO Corporation 3289 1 Tokyu Fudosan Holdings Corporation 1812 1 KAJIMA CORPORATION 3291 1 Iida Group Holdings Co.,Ltd. 1820 1 Nishimatsu Construction Co.,Ltd. 3349 1 COSMOS Pharmaceutical Corporation 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1824 1 MAEDA CORPORATION 3382 1 Seven & I Holdings Co.,Ltd. 1860 1 TODA CORPORATION 3391 1 TSURUHA HOLDINGS INC. 1861 1 Kumagai Gumi Co.,Ltd. 3401 1 TEIJIN LIMITED 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3402 1 TORAY INDUSTRIES,INC. 1881 1 NIPPO CORPORATION 3405 1 KURARAY CO.,LTD. 1893 1 PENTA-OCEAN CONSTRUCTION CO.,LTD. 3407 1 ASAHI KASEI CORPORATION 1911 1 Sumitomo Forestry Co.,Ltd. -

Perfect Storm Profits at Risk in the Japanese Seafood Industry

PERFECT STORM PROFITS AT RISK IN THE JAPANESE SEAFOOD INDUSTRY SEPTEMBER 2019 FUNDERS Planet Tracker [email protected] DISCLAIMER Investor Watch’s reports are impersonal and do not provide individualized advice or recommendations for any specific reader or portfolio. Investor Watch is not an investment adviser and makes no recommendations regarding the advisability of investing in any particular company, investment fund or other vehicle. The information contained in this research report does not constitute an offer to sell securities or the solicitation of an offer to buy, or recommendation for investment in, any securities within any jurisdiction. The information is not intended as financial advice. The information used to compile this report has been collected from a number of sources in the public domain and from Investor Watch licensors. While Investor Watch and its partners have obtained information believed to be reliable, none of them shall be liable for any claims or losses of any nature in connection with information contained in this document, including but not limited to, lost profits or punitive or consequential damages. This research report provides general information only. The information and opinions constitute a judgment as at the date indicated and are subject to change without notice. The information may therefore not be accurate or current. The information and opinions contained in this report have been compiled or arrived at from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made by Investor Watch as to their accuracy, completeness or correctness and Investor Watch does also not warrant that the information is up-to-date. -

PAYS SECTION Japon Manufactures De Produits Intermédiaires

En vigueur depuis le: PAYS Japon 12/07/2021 00031 SECTION Manufactures de produits intermédiaires Date de publication 04/03/2011 Liste en vigueur Numéro Nom Ville Régions Activités Remarque Date de la demande d'agrément 01EZ200001 Daiichi Kishimoto Clinical Laboratory, Inc. Tomakomai Hokkaido CAT3 30/05/2017 01EZ280096 SEROTEC CHITOSE FACTORY Chitose Hokkaido CAT3 08/12/2014 02EZ285024 GODO SHUSEI CO., LTD. Enzyme and Pharmaceuticals Factory Hachinohe Aomori CAT3 13/04/2018 03AZ200001 Astellas Pharma Tech Co., Ltd. Nishine Plant Hachimantai Iwate CAT 2 28/04/2011 03EZ200001 A & T CORPORATION ESASHI WORKS Oshu Iwate CAT3 13/04/2018 07EZ280018 NITTOBO MEDICAL CO.,LTD. MEDICAL DEVELOPMENT Koriyama Fukushima CAT3 08/12/2014 CENTER 08AZ000046 Seikagaku Corporation Takahagi Plant Takahagi Ibaraki CAT3 28/04/2011 08EZ280001 Thermo Fisher Diagnostics K.K. Logistics Center Ishioka Ibaraki CAT3 30/03/2015 08EZ280050 NISSUI PHARMACEUTICAL CO.,.LTD. YUKI PLANT Yuki Ibaraki CAT3 08/12/2014 08EZ280097 SEKISUI MEDICAL CO.,LTD. TSUKUBA PLANT Ryugasaki Ibaraki CAT 1, CAT 2, CAT3 08/12/2014 08EZ280110 KAINOS Laboratories, Inc. Kasama Factory Kasama Ibaraki CAT3 11/04/2019 09AZ200008 Chugai Pharma Manufacturing Co.,LTD. Utsunomiya Plant Utsunomiya Tochigi CAT 2 28/04/2011 09AZ200012 Maruha Nichiro Foods, Inc. Foods & Fine Chemicals Department Utsunomiya Tochigi CAT 2 28/04/2011 09EZ280056 INSTITUTE OF IMMUNOLOGY CO.,LTD. TOCHIGI PLANT Shimotsuke Tochigi CAT 2, CAT3 08/12/2014 09EZ286008 SB Bioscience Co., Ltd. Fujikura Kasei Co., Ltd. Sano Medical Sano Tochigi CAT 2, CAT3 08/12/2014 Satellite 1 / 4 Liste en vigueur Numéro Nom Ville Régions Activités Remarque Date de la demande d'agrément 11EZ200009 NICHIREI BIOSCIENCES INC. -

"JPX-Nikkei Index 400"

JPX-Nikkei Index 400 Constituents (applied on November 30, 2020) Published on November 9, 2020 No. of constituents : 400 (Note) The No. of constituents is subject to change due to de-listing. etc. (Note) As for the market division, "1"=1st section, "2"=2nd section, "M"=Mothers, "J"=JASDAQ. Code Market Divison Issue Code Market Divison Issue 1332 1 Nippon Suisan Kaisha,Ltd. 3086 1 J.FRONT RETAILING Co.,Ltd. 1333 1 Maruha Nichiro Corporation 3088 1 Matsumotokiyoshi Holdings Co.,Ltd. 1605 1 INPEX CORPORATION 3092 1 ZOZO,Inc. 1719 1 HAZAMA ANDO CORPORATION 3107 1 Daiwabo Holdings Co.,Ltd. 1720 1 TOKYU CONSTRUCTION CO., LTD. 3116 1 TOYOTA BOSHOKU CORPORATION 1721 1 COMSYS Holdings Corporation 3141 1 WELCIA HOLDINGS CO.,LTD. 1766 1 TOKEN CORPORATION 3148 1 CREATE SD HOLDINGS CO.,LTD. 1801 1 TAISEI CORPORATION 3167 1 TOKAI Holdings Corporation 1802 1 OBAYASHI CORPORATION 3197 1 SKYLARK HOLDINGS CO.,LTD. 1803 1 SHIMIZU CORPORATION 3231 1 Nomura Real Estate Holdings,Inc. 1808 1 HASEKO Corporation 3288 1 Open House Co.,Ltd. 1812 1 KAJIMA CORPORATION 3289 1 Tokyu Fudosan Holdings Corporation 1820 1 Nishimatsu Construction Co.,Ltd. 3291 1 Iida Group Holdings Co.,Ltd. 1821 1 Sumitomo Mitsui Construction Co., Ltd. 3349 1 COSMOS Pharmaceutical Corporation 1824 1 MAEDA CORPORATION 3360 1 SHIP HEALTHCARE HOLDINGS,INC. 1860 1 TODA CORPORATION 3382 1 Seven & I Holdings Co.,Ltd. 1861 1 Kumagai Gumi Co.,Ltd. 3391 1 TSURUHA HOLDINGS INC. 1878 1 DAITO TRUST CONSTRUCTION CO.,LTD. 3401 1 TEIJIN LIMITED 1881 1 NIPPO CORPORATION 3402 1 TORAY INDUSTRIES,INC. -

Notice Concerning Acquisition of Sai Gon Food Joint Stock Company

January 8, 2021 Company name: Maruha Nichiro Corporation Stock exchange listing: Tokyo Stock Exchange, First Section Stock code: 1333 URL: https://www.maruha-nichiro.com/ Representative: Title: President and CEO Name: Masaru Ikemi Inquiries: Hiroyuki Metoki Acting General Manager of Corporate Planning Department Phone: +81 (0)3 6833 1195 Email: [email protected] Notice Concerning Acquisition of Sai Gon Food Joint Stock Company Maruha Nichiro Corporation (hereinafter “the Company”) hereby announces that the Board of Directors of the Company resolved the acquisition of Sai Gon Food Joint Stock Company (Head Office: Ho Chi Minh City, Vietnam, hereinafter “Sai Gon Food”) as follows. As this matter does not fall under the timely disclosure standards of the Tokyo Stock Exchange, some disclosure items and contents have been omitted. 1. Reason for the Acquisition Sai Gon Food was established in Ho Chi Minh City, Vietnam in 2003 and has developed strongly through the production and export of processed marine products to Japan. Focusing on the fast-growing domestic market in Vietnam, Sai Gon Food has been producing frozen and retort-packed foods which can be easily prepared, under the “SG FOOD” brand and has established itself as one of the leading brands of porridge and hot pot sets in Vietnam. Furthermore, in recent years, Sai Gon Food has also started selling baby food and has been recognized as a company that has enriched the food scene in Vietnam. Sai Gon Food has started business with the Company in 2017 as a consignment manufacturer of processed marine products for the Japanese market and the Company has helped improve Sai Gon Food’s manufacturing technology and business development through technical assistance. -

CORPORATE PROFILE Printed on Recycled Paper September 2019 Message from the President

Corporate Data Trade name Business operations Location Maruha Nichiro Corporation • Fishing 2-20, 3-chome, Toyosu, • Aquaculture Koto-ku, Tokyo, Japan Established • Import, export, processing, and March 31, 1943 Phone sales of marine products +81-3-6833-0826 Corporate representative • Production, processing, and Representative Director, sales of frozen foods, retort Fax President pouch foods, canned foods, fish +81-3-6833-0506 Shigeru Ito hams and sausages, food and chemicals, and beverages URL Capital • Import of meat and feedstuff https://www.maruha-nichiro.com 20 billion yen raw materials • Production, processing, and End of fiscal year sales of meat March 31 CORPORATE PROFILE Printed on recycled paper September 2019 Message from the President CORPORATE PROFILE Focusing Strengths and Capacity on Future Company Credo People: Growth Strategies Loyal to our people, the most important asset of our company As an amalgam of two companies, Maruha and Opportunity: Seek out creativity, originality and advancement Nichiro, both of which were established more in all aspects of life and business than a century ago, we at the Maruha Nichiro Group have overcome numerous challenges throughout Productivity: Plan everything we do with care, and follow the years with the wisdom and experience built up through with confidence until conclusion and handed down by our forebears. Harmony: Today, the Group is operating in an environment Always a responsible corporate citizen, with the marked by constant change. Trends with attendant courage to make a difference in communities and risks that could affect the Group have become sustainable business practices conspicuous globally. Whether we like it or not, Profit: this is an era where there is no choice but to keep Focus on long-term return on all investments to fully abreast of the ongoing changes in global society. -

Resona Maruha Building and Ryoshin Harajuku Building)

Translation Purpose Only December 24, 2009 For Immediate Release Real Estate Investment Trust Unit Issuer: TOKYU REIT, Inc. 1-12-1, Dogenzaka, Shibuya-ku, Tokyo, 150-0043, Japan Masahiro Horie Executive Director (Securities Code: 8957) Investment Management Company: Tokyu Real Estate Investment Management Inc. Representative: Masahiro Horie Representative Director & President, Chief Executive Officer Inquiries: Yosuke Koi Senior Executive Officer, Chief Financial Officer and General Manager, Investor Relations TEL: +81-3-5428-5828 Notice Concerning Disposition of Domestic Properties (Resona Maruha Building and Ryoshin Harajuku Building) TOKYU REIT, Inc. (“TOKYU REIT”) today announced details of its decision to execute a beneficiary interest disposition agreement in connection with the sale of domestic properties. Brief details are as follows. 1. Disposition Details (1) Resona Maruha Building (A) Type of Disposition : Trust beneficiary interest in real estate (B) Property Name : Resona Maruha Building (C) Disposition Price : ¥42,000,000,000 (Excluding fixed property tax, city planning tax, consumption tax and other imposts) (D) Book Value : ¥23,722,782,484 (expected) (E) Amount of Difference : ¥18,277,217,516 from Disposition Price (F) Agreement Date : December 24, 2009 (Thursday) (G) Settlement Date : January 15, 2010 (Friday) (H) Purchaser : Otemachi Development Tokutei Mokuteki Kaisha (Please refer to 4. Purchaser’s Profile for details) (I) Disposition Method : Disposition of real estate in the form of a trust beneficiary interest to -

Notice of the 77Th Ordinary General Meeting of Shareholders

Note: This document has been translated from a part of the Japanese original for reference purposes only. In the event of any discrepancy between this translated document and the Japanese original, the original shall prevail. (Securities Code: 1333) June 2, 2021 To our shareholders: Masaru Ikemi, President & CEO Maruha Nichiro Corporation 2-20, Toyosu 3-chome, Koto-ku, Tokyo Notice of the 77th Ordinary General Meeting of Shareholders We are pleased to inform you of the 77th Ordinary General Meeting of Shareholders of Maruha Nichiro Corporation (the “Company”), which will be held as indicated below. However, to avoid risk of infections of the novel coronavirus disease (COVID-19) at this general meeting of shareholders, you are strongly recommended to refrain from attending the meeting in person, and to exercise your voting rights in writing (Voting Rights Exercise Form) or via the internet instead. Please examine the attached Reference Documents for General Meeting of Shareholders and exercise your voting rights by 5:00 p.m. on Wednesday, June 23, 2021 (JST). 1. Date and Time: Thursday, June 24, 2021, at 10:00 a.m. (JST) (Reception desk opens at 9:00 a.m.) 2. Venue: Mielparque Hall 5-20, Shibakoen 2-chome, Minato-ku, Tokyo 3. Purpose Matters to be reported 1. The Business Report and the Consolidated Financial Statements for the 77th fiscal year (from April 1, 2020 to March 31, 2021), and the results of audits of the Consolidated Financial Statements by the financial auditor and the Audit & Supervisory Board 2. The Non-consolidated Financial Statements for the 77th fiscal year (from April 1, 2020 to March 31, 2021) Matters to be resolved Proposal No. -

Tokyo Sustainable Seafood Symposium 2020 Announces Its Program and Speakers, Featuring 6 Days Virtual Seminars with 100 Expert Speakers

Tokyo Sustainable Seafood Symposium 2020 announces its program and speakers, featuring 6 days virtual seminars with 100 expert speakers Tokyo, Japan (October, 7, 2020) Seafood Legacy Co., Ltd. and Nikkei ESG will hold the Tokyo Sustainable Seafood Symposium 2020 (TSSS2020) as a virtual event from 4 to 6 and 9 to 11, November, 2020. This year marks the 6th iteration of the Tokyo Sustainable Seafood Symposium, an international flagship event specializing in sustainable seafood. This year’s theme is: “Sustainable Seafood and the Blue Economy in the New Normal.” The English channel will broadcast the seminar content on Pacific Standard Time (UTC-8), allowing the global audience to view the content and send questions and networking requests to the speakers. The sustainable seafood movement has continued in spite of the severe adverse circumstances unlike anything seen before. Industry leaders, government representatives, academics, and global NGOs are invited to speak to share their knowledge and experiences, and the perspective of the blue economy, achieving both economic performance and sustainable for ocean resources, will be featured to discuss pressing topics which are of critical importance for the present such as ensuring food security, fishery resource management, technology, responsible procurement, and ESG investment. [Speakers] United Nations Global Compact, European Commission, Ministry of the Environment Japan, Fisheries Agency Japan, Maruha Nichiro corporation., NIPPON SUISAN KAISHA, Ltd., Walmart Inc., AEON Co., Ltd., Seiyu GK, Japanese Consumers' Co-operative Union, IBM Japan Ltd., Rakuten, Inc., NTT DOCOMO, INC., Panasonic Corporation., Hilton Worldwide Holdings Inc., Relais & Châteaux, and more. To learn more about the program and to register, please visit the TSSS2020 official website. -

Respondents(Eng)

JCGR JCGIndex Survey 2006 List of 312 responding firms Fishery, Agriculture & Forestry (2) The Nisshin OilliO Group, Ltd. (05) Nippon Suisan Kaisha J-OIL MILLS, Inc. Maruha Nichiro Corporation (04)(05) Kewpie Corporation (03)(04) House Foods Corporation (03)(05) Construction (13) Nichirei Corporation (02)(03)(04)(05) Hazama Corporation Taisei Corporation (05) Textiles & Apparel (6) OBAYASHI CORPORATION (04)(05) Gunze Limited (02)(03)(04)(05) Ando Corporation (04)(05) Japan Wool Textile Co., Ltd. (04)(05) DAIHO CORPORATION (05) Teijin Limited (03)(04)(05) Maeda Corporation (02)(03)(04)(05) Toray Industries, Inc. (03)(05) Maeda Corporation (04)(05) KURARAY CO., LTD (04)(05) Kumagai Gumi Co., Ltd. (05) Wacoal Holdings Corp. (02)(04)(05) TOHOKU MISAWA HOMES CO., LTD. Pulp and Paper (3) Daiwa House Industry Co., Ltd. (05) Tomoegawa Co., Ltd. (04)(05) Sekisui House, Ltd. (05) Nippon Paper Group, Inc. (05) Takasago Thermal Engineering Co., Ltd. Rengo Co., Ltd. (02)(04)(05) DAI-DAN Co., Ltd. (04)(05) Chemicals (32) Foods (19) Asahi Kasei Corporation (05) Nosan Corporation (05) Showa Denko K.K (04)(05) Meiji Seika Kaisha、Limited(02)(03) KUREHA CORPORATION (04) (04)(05) Nippon Soda Co., Ltd. (03)(04)(05) Yakult Honsha Co., Ltd. (03)(04)(05) Tokuyama Corporation (02)(04)(05) NH Foods Ltd. (04)(05) Toagosei Co., Ltd. (05) Itoham Foods Inc. (02)(03)(04)(05) Kanto Denka Kogyo Co., Ltd. (04)(05) Yonekyu Corporation (05) Shin-Etsu Chemical Co., Ltd. (05) Asahi Breweries, Ltd (02)(03)(04)(05) Mitsubishi Chemical Holdings TAKARA HOLDINGS INC. Corporation (04)(05) Oenon Holdings, Inc.