Optus 28.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

State of Mobile Networks: Australia (November 2018)

State of Mobile Networks: Australia (November 2018) Australia's level of 4G access and its mobile broadband speeds continue to climb steadily upwards. In our fourth examination of the country's mobile market, we found a new leader in both our 4G speed and availability metrics. Analyzing more than 425 million measurements, OpenSignal parsed the 3G and 4G metrics of Australia's three biggest operators Optus, Telstra and Vodafone. Report Facts 425,811,023 31,735 Jul 1 - Sep Australia Measurements Test Devices 28, 2018 Report Sample Period Location Highlights Telstra swings into the lead in our download Optus's 4G availability tops 90% speed metrics Optus's 4G availability score increased by 2 percentage points in the A sizable bump in Telstra's 4G download speed results propelled last six months, which allowed it to reach two milestones. It became the the operator to the top of our 4G download speed and overall first Australian operator in our measurements to pass the 90% threshold download speed rankings. Telstra also became the first in LTE availability, and it pulled ahead of Vodafone to become the sole Australian operator to cross the 40 Mbps barrier in our 4G winner of our 4G availability award. download analysis. Vodafone wins our 4G latency award, but Telstra maintains its commanding lead in 4G Optus is hot on its heels upload Vodafone maintained its impressive 4G latency score at 30 While the 4G download speed race is close among the three operators milliseconds for the second report in row, holding onto its award in Australia, there's not much of a contest in 4G upload speed. -

Exesim Ultra 3G Mobile Voice Plan (4G17-ULTRA)

CRITICAL INFORMATION SUMMARY ExeSim Ultra 3G Mobile Voice Plan (4G17-ULTRA) This summary gives you the important information you need to know about your Exetel mobile Voice plan. It covers things like the length of your contract, billing, what’s covered and what’s not. Information About The Service This plan offers a $79.99 3G mobile voice service on a month to The monthly allowances are not interchangeable and unused value month term which includes one included value allowance and two from one allowance cannot be transferred to another or into the unlimited allowances: current of following month if unused. 1. UNLIMITED National talk to Landlines and Mobiles Subject to the Exetel Mobile Acceptable use Policy and the Exetel Terms and Conditions go to: 2. UNLIMITED National SMS and MMS http://www.exetel.com.au/terms 3. 90GB of 3G National Data* Information about pricing Recurring charges are payable monthly in advance. The allowances expire at the end of each month. The included National Data Minimum monthly cost allowance includes all usage for both uploads and downloads. This is a stand-alone service and is not bundled with any other product. $79.99 is the minimum financial commitment for this offer. If your * Prorata allowance applies in the first month. usage exceeds the included National 3G Data Allowance, additional usage charges will apply. BYO device The most common charges used to calculate your usage A compatible mobile (with the Optus 3G Network) device is (allowance and any excess) are as follows; required to gain access to the service, and is required to be operated inside the coverage area. -

Optus Internet Everyday

Critical information summary This summary does not reflect any special discounts, bonus data or promotions which may apply from time to time. Optus Internet Everyday Plan ID: 35287684 Information about the Service Description of the Service This plan is for a stand-alone Fixed Broadband service that is supplied using the Optus nbn™ network. The Optus Internet Everyday plan also has the option of bundling a Fixed Telephone service. See “Optional Phone Plans” (page 3) section for more information. Plan Minimum monthly charge $79/mth Minimum term Month-to-month Monthly data allowance Unlimited Start-up fee $0 However, fees may apply for a first time nbn connection to dwellings in new developments, for additional lines or for non-standard installations Modem charges $252 Optus will cover the cost of the modem if you remain connected for 36 months (i.e. $7/mth over 36 months) Cancellation fee There is no cancellation fee for this plan. If applicable, you’ll need to pay out any remaining device payments in full (any credits or discounts will be forfeited), plus, all charges incurred up to the end of the billing cycle in which your service is cancelled (unless otherwise specified) Minimum total cost $331 (includes $252 modem cost and one month of plan fee) (when you pay by direct debit) Service and plan availability Device Payment Plans Optus Broadband services are not available in all areas or to You can buy an eligible device (such as a Booster) on a Device all premises. The broadband service offered will be determined Payment Plan (DPP) and pay for it over a selected term by by what is available at your location. -

1. Optus - Background, Networks and Services

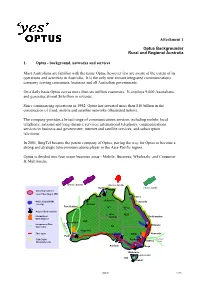

Attachment 1 Optus Backgrounder Rural and Regional Australia 1. Optus - background, networks and services Most Australians are familiar with the name Optus, however few are aware of the extent of its operations and activities in Australia. It is the only new entrant integrated communications company serving consumers, business and all Australian governments. On a daily basis Optus serves more than six million customers. It employs 9,000 Australians, and generates almost $6 billion in revenue. Since commencing operations in 1992, Optus has invested more than $10 billion in the construction of fixed, mobile and satellite networks (illustrated below). The company provides a broad range of communications services including mobile; local telephony; national and long distance services; international telephony; communications services to business and government; internet and satellite services; and subscription television. In 2001, SingTel became the parent company of Optus, paving the way for Optus to become a strong and strategic telecommunications player in the Asia-Pacific region. Optus is divided into four major business areas - Mobile; Business; Wholesale; and Consumer & Multimedia. B-Series Satellite A-Series Satellite Darwin C-Series Satellite Switching Systems/ Local Fibre Ring in CBD Cairns Mobile Digital(GSM) Katherine Townsville coverage Broome Port Hedland NT Mt Isa National Earth Stations Alice QLD International Springs Rockhampton Earth Station s WA S Geraldton International Fibre e M Brisbane e SA Optic Cable W e 3 Kalgoorlie Fibre Optic Port Augusta NSW Newcastle Perth SDH Digital Canberra Southern Sydney Microwave Link Cross VIC Adelaide Bega Melbourne Launceston TAS Hobart Optus 1 of 5 The company’s Mobile business unit has captured around one-third of the total Australian GSM mobile market and leads the market in mobile data take up. -

Optus Recognises That Such an Approach, Whilst It Has Strong Policy Merit, Might Be Challenging Politically

Public Version | Page 1 Executive Summary 3 Developments in the sector have removed the need for a USO 5 Historical rationale of the USO 5 Current USO is a failed policy 7 There is no need for a USO 8 No justification for multiple sets of infrastructure to deliver USO 13 Retail competition over competitive infrastructure ensures supply 13 Current USO imposes high and untested costs 16 Extent of the current USO 16 Costs of the current USO 18 The USO distorts competition 22 Impact of USO on competitors 23 USO tax diverts competitive rural investment 25 Interaction with other government policies 25 Alternate USO policy options 27 A reformed USO should leverage off the NBN infrastructure 28 Promoting retail competition for provision of services 29 Keeping Telstra’s USO contractual position whole 31 Appendix A. Historic rationale of the USO 32 Appendix B. Issues Paper Questions 39 Public Version | Page 2 1.1 The Universal Service Obligation (USO) remains rooted in principles more applicable to the analogue era of telecommunications. It is predominantly focused on the delivery of fixed voice handsets and voice calls over fixed line copper connections. The widespread deployment and use of mobile, data and broadband services now render it increasingly inappropriate. 1.2 Three decades after the genesis of the USO the industry is vastly different from that which existed in the late 1980s: (a) Whilst Telstra retains a dominant position in the market, especially in regional Australia, competitive forces and regulation ensure that customers have access to genuine choice in a way that was not possible in the 1980s. -

PRIMUS TELECOMMUNICATIONS GROUP, INCORPORATED (Exact Name of Registrant As Specified in Its Charter)

Table of Contents SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2007 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission File No. 0-29092 PRIMUS TELECOMMUNICATIONS GROUP, INCORPORATED (Exact name of registrant as specified in its charter) Delaware 54-1708481 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 7901 Jones Branch Drive, Suite 900, McLean, VA 22102 (Address of principal executive offices) (Zip Code) (703) 902-2800 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered None N/A Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $.01 per share Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Media Release

Media Release Netspace business update NETSPACE REPORTS SUCCESS WITH NEW VOICE OFFERING (THIS WAS NEVER ISSUED) Melbourne, March x, 2007 - National Broadband ISP, Netspace, today announced a record start to 2007 with above average growth in broadband sales driven in part by a strong take up by consumers for the company’s full service voice offerings, particularly its bundled VoiP and broadband plans. In December 2006, Netspace officially launched Netspace Phone – a range of telephony services for consumers and small businesses. These included 10¢ flat rate VoIP calls to anywhere in Australia and 4.9¢ per minute VoIP calls to many International destinations as well attractive home phone and broadband bundles, and standard long distance and pre-paid calling card options. Ben Dunscombe, Regulatory Affairs Manager for Netspace said the launch of Netspace Phone has sparked a new phase of growth for the company by bringing to market an offering that’s attractive to customers who might otherwise just use a large carrier such as Telstra or Optus for all their communications needs. “The start of 2007 has been a strong period of growth for Netspace which we believe has been driven by our competitive and successful Voice campaign. Since December, more than x% of our home and small business broadband customers have signed up to our VoIP services and we have also seen a surge in new broadband customers signing on to our Home Phone/Broadband bundled deals,” said Dunscombe. Netspace Plots SMB Push Netspace plans to boost its position in the SMB communications market with the relaunch of Netspace Business Solutions set for quarter three this year. -

Part 1 – Introduction

Netspace Customer Terms Edition 12 July 2007 Part 1 – Introduction 1. Welcome Welcome to Netspace Customer Terms. These are Our standard terms of business. (We may also refer to them as ‘Our Standard Form of Agreement’ or ‘SFoA’.) There’s an index at the end to help You find things. 2. It’s not so complicated Netspace Customer Terms cover a wide range of services and goods, so it’s quite a long document. But many parts of it are only relevant to You if You obtain a particular service or goods from Us. You can ignore the rest. We have done Our best to make it easy to understand which parts are relevant to which Services. 3. A general outline Netspace Customer Terms is made up of numbered ‘Parts’ – like this. Part 3 contains Our ‘Core Terms’. These apply to all Our Services and Contracts. Several of the other Parts are ‘Service Terms’. They only apply to certain Services and Contracts. For instance, Our ‘Local Call Service Terms’ apply if You obtain a local telephone call Service from us. Part 13 includes very important information about consumer rights. Each Part begins with an explanation of what it applies to. 4. Some legal information Netspace Customer Terms are a ‘Standard Form of Agreement’ under section 479 of the Telecommunications Act 1997. That means that they automatically operate as the terms between Us and You, whenever We supply You with services or goods. 1/112 Netspace Customer Terms Edition 12 July 2007 (Exception: see clause 9 if You are a Carrier or Carriage Service Provider.) If We agree in writing to vary any terms by Special Conditions, that is part of Your Contract. -

PRIMUS TELECOMMUNICATIONS GROUP, INCORPORATED (Exact Name of Registrant As Specified in Its Charter)

Table of Contents SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2010 OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission File No. 0-29092 PRIMUS TELECOMMUNICATIONS GROUP, INCORPORATED (Exact name of registrant as specified in its charter) Delaware 54-1708481 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 7901 Jones Branch Drive, Suite 900, McLean, VA 22102 (Address of principal executive offices) (Zip Code) (703) 902-2800 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered None N/A Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.001 per share Contingent Value Rights Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Optus Wholesale Story Book Layout 1009.Indd

OPTUS WHOLESALE. OUR STORY. Grow your business through partnership with Optus Wholesale CONTENts 0 1 The Optus Wholesale Difference Sustainable Relationships Superior Customer Service Innovative Solutions Partnering for growth 02 Our Network Extend your reach through partnership with Optus Wholesale The Optus Network 03 Our Services Mobile Wireline Satellite 04 Why talk to us? We offer the strength of a world-class telco Join us and stand out from the competition Our success is based on five clear and single-minded principles OPTUS WHOLESALE: OUR STORY 01 THE optus WHOLESALE DIFFERENCE Optus is the only Tier One provider with a consistent pedigree in wholesale services. Our mission is to deliver industry best value by investing in sustainable relationships, superior customer experience and innovative solutions. ConnEctIVITY FOR THE PROGREssIVE woRKPLACE We strive to be easy to deal with our approach to business embraces: • Strategic partnership with an agreed roadmap for mutual success • Products tailored specifically to the wholesale market • A flexible approach to negotiations and commercial arrangements • Innovative product and service solutions • Being trustworthy, reliable and respecting our relationship. SUPERIOR CUstoMER SERVICE Our vision is to be the first-choice telco partner for wholesale service providers in Asia-Pacific. We can only achieve this by delivering service and value to our wholesale partners. Optus continually improves our network, investing on average $1 billion each year in fixed, mobile, IP and satellite infrastructure to ensure our advanced technology platforms are capable of delivering integrated communications well into future. Our challenger spirit drives us to achieve ever-higher levels of customer support. For example, our handset replacement process for the rapid exchange of Dead on Arrival and Early Life Failure mobile handsets and devices leads the industry. -

NBN Faces Double Cost Hit on Ageing Optus Network

NBN faces double cost hit on ageing Optus network by David Ramli NBN Co spent $800 million to buy and reuse Optus' cable network. Now it may be forced to invest another $375 million to rebuild parts of the fading network because it isn't capable of delivering high-speed broadband to enough people. NBN struck the deal with Optus in 2012 to buy and convert the hybrid fibre-coaxial (HFC) network used for internet and pay TV. Where the last Labor government wanted to replace it with fibre-to-the-home technology, the Coalition pledged to save money and time by upgrading it instead and signed an updated contract last year. The draft of an internal NBN presentation this month says the Optus network is not "fit for purpose", lacks the capacity to support NBN services and must be upgraded or replaced at a cost of up to $375 million. This would be the latest cost increase at NBN since the Coalition took over in 2013. It revealed a potential cost blowout of $15 billion in August, citing higher than expected expenses. "Some Optus equipment [is] arriving at end of life and needs to be replaced," the presentation to senior executives said. "Optus nodes are oversubscribed compared with Telstra and will require node splits … 470,000 premises [in areas covered by Optus' network] would have to be overbuilt." The presentation warned that any of the planned works would "come at a significant cost" in terms of time and money. "NBN will miss its financial year 2017-18 ready-for-service targets by respectively 300,000 and 333,000 [premises]," it said. -

Comparing Broadband ISP Performance Using Big Data from M-Lab

1 Comparing Broadband ISP Performance using Big Data from M-Lab Xiaohong Deng, Yun Feng, Thanchanok Sutjarittham, Hassan Habibi Gharakheili, Blanca Gallego, and Vijay Sivaraman Abstract—Comparing ISPs on broadband speed is challeng- remote areas served by low-capacity (wired or wireless) infras- ing, since measurements can vary due to subscriber attributes tructure will compare poorly to an ISP-B whose subscribers such as operation system and test conditions such as access are predominantly city dwellers connected by fiber; yet, it capacity, server distance, TCP window size, time-of-day, and network segment size. In this paper, we draw inspiration from could well be that ISP-A can provide higher speeds than ISP- observational studies in medicine, which face a similar challenge B to every subscriber covered by ISP-B! The comparison bias in comparing the effect of treatments on patients with diverse illustrated above arising from disparity in access capacity is characteristics, and have successfully tackled this using “causal but one example of many potential confounding factors, such inference” techniques for post facto analysis of medical records. as latency to content servers, host and server TCP window size Our first contribution is to develop a tool to pre-process and visualize the millions of data points in M-Lab at various time- settings, maximum segment size in the network, and time-of- and space-granularities to get preliminary insights on factors day, that directly bias measurement test results. Observational affecting broadband performance. Next, we analyze 24 months studies therefore need to understand and correct for such biases of data pertaining to twelve ISPs across three countries, and to ensure that the comparisons are fair.