Danske Bank Hearing Aid Seminar June 22, 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sustainability • ESG Report GN Store Nord A/S –2019

Sustainability • ESG Report GN Store Nord A/S –2019 2 Sustainability - ESG Report ⋅ Contents Contents Contents GN Sustainability – ESG Report 2019 Content – GN Sustainability - ESG Report 2019 2 Management’s commitment 3 ESG overview 4 Our sustainability framework 5 Where GN has lasting impact 6 Business model 7 Sustainability governance 8 Making Life Sound Better 9 Safe, sustainable and responsible products 12 Reducing business flights 15 Sustainable operations 16 People excellence 19 Giving back 20 About this report 23 Membership of UN Global Compact Member since January 14, 2010 Number of employees: 6,275 Sector: Health care equipment and electronics Reporting date: February 5, 2020 The report covers the period: January 1, 2019 to December 31, 2019 This report forms part of the management’s report in the Annual Report 2019 for GN Store Nord A/S and constitutes GN’s corporate responsibility report according to Section 99a in the Danish Financial Statements Act. The report is not covered by the audit. Visit www.gn.com/About/Corporate-responsibility to read our responsibility guidelines and policies. GN Store Nord A/S –2019 Management’s3 Sustainability – ESG Report ⋅ Doing the right thing with impactcommitment Contents Doing the right thing with impact GN’s sustainability strategy is first and foremost driven by a desire to make real and lasting impact. Therefore, sustainability is integrated into how we run our company, as a consideration in every decision we make At GN, we transform people’s lives through the power of (ESG) more proactively, taking inspiration from the United sound. Our intelligent hearing, audio and collaboration so- Nation’s 17 Sustainable Development Goals. -

Communications Under the Seas: the Evolving Cable Network and Its

Communications under the Seas The Evolving Cable Network and Its Implications edited by Bernard Finn and Daqing Yang The MIT Press Cambridge, Massachusetts London, England © 2009 Massachusetts Institute of Technology All rights reserved. No part of this book may be reproduced in any form by any electronic or mechanical means (including photocopying, recording, or information storage and retrieval) without permission in writing from the publisher. For information about special quantity discounts, please email special_sales@mitpress .mit.edu This book was set in Bembo by The MIT Press. Printed and bound in the United States of America. Library of Congress Cataloging-in-Publication Data Communications under the seas : the evolving cable network and its implications / edited by Bernard Finn and Daqing Yang. p. cm. — (Dibner Institute studies in the history of science and technology) Includes bibliographical references and index. ISBN 978-0-262-01286-7 (hardcover : alk. paper) 1. Cables, Submarine—History. 2. Telecommunication—Social aspects—History. 3. Communication, International. I. Finn, Bernard S., 1932– II. Yang, Daqing, 1964– TK5103.15.C66 2009 621.387’8409162—dc22 2008042011 10 9 8 7 6 5 4 3 2 1 Index Admiralty (U.K.), 187 for voice communications, 37–38, 46, “Memorandum on the Protection of 51 British Submarine Cables,” 194 vacuum tube amplifiers, 30, 37, 46, 247 Ahvenainen, Jorma, 119 Anglo-American Telegraph Company, 29t, Alcatel, 175, 280 66, 71, 82–83, 162–163, 166 Alexander, grand duke of Russia, 124, 126 anti-trust legislation, 199 Algeria, 185 Associated Press, 169, 266 All America Cables, 33, 35, 84, 280 Atlantic Telegraph Company, 18, 66, 167 All-American Telegraph Companies, 89 AT&T. -

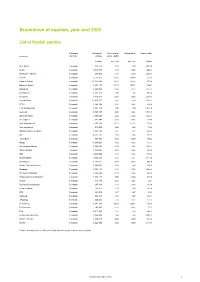

Breakdown of Equities, Year-End 2020

Breakdown of equities, year-end 2020 Listed Danish equities Company Number of Ownership of Voting rights Market value Company domicile equities share capital number per cent per cent DKKm ALK-Abello Denmark 830,794 7.46 4.10 2,077.0 Ambu Denmark 4,818,951 1.91 0.86 1,268.3 AP Moller - Maersk Denmark 253,690 1.27 0.90 3,358.9 Asetek Denmark 2,722,415 10.30 10.30 210.3 Bang & Olufsen Denmark 17,092,036 13.92 13.92 573.6 Bavarian Nordic Denmark 5,904,171 10.11 10.11 1,104.1 Carlsberg Denmark 1,227,664 0.84 0.27 1,197.2 Chr Hansen Denmark 1,381,570 1.06 1.06 865.4 Coloplast Denmark 1,310,347 0.61 0.35 1,218.1 Danske Bank Denmark 13,693,257 1.60 1.60 1,378.2 DFDS Denmark 1,949,162 3.32 3.32 536.4 DSV PANALPINA Denmark 2,281,956 1.00 1.00 2,327.6 Genmab Denmark 1,166,965 0.09 0.09 1,544.8 GN Store Nord Denmark 3,166,046 2.24 2.24 1,542.5 H Lundbeck Denmark 931,964 0.47 0.47 194.6 H+H International Denmark 2,107,893 11.72 11.72 278.2 Huscompagniet Denmark 615,000 3.08 3.08 76.9 INVISIO Communications Denmark 3,183,701 7.22 7.22 589.2 ISS Denmark 4,551,135 2.46 2.46 479.7 Jyske Bank 1 Denmark 455,709 0.63 0.00 106.2 Matas Denmark 1,846,027 4.82 4.82 159.5 Netcompany Group Denmark 1,660,500 3.33 3.33 1,033.7 Nilfisk Holding Denmark 1,436,062 5.29 5.29 189.0 NKT Denmark 2,637,690 6.14 6.14 715.3 Novo Nordisk Denmark 7,546,288 0.32 0.11 3,219.6 Novozymes Denmark 1,724,215 0.61 0.23 602.6 Nordic Transport Group Denmark 1,086,064 4.80 4.80 278.0 Pandora Denmark 2,153,187 2.16 2.16 1,466.3 Per Aarsleff Holding Denmark 2,064,304 10.13 6.34 636.8 Ringkjoebing -

Annual Report 2014

GN Store Nord A/S Annual Report 2014 INNOVATORS IN SOUND Co. reg. no. 24257843 M CONTENTS 2 / MANAGEMent’s rePORT / CONTENTS Contents Our investment case 2 MANAGEMENT'S REPORT Through relentless execution GROUP DEVELOPMENT 2014 2014 in figures 3 of our Strategy: INNOVATION Foreword by the chairman 4 & GROWTH, we create State of GN Store Nord 6 Consolidated financial highlights 9 shareholder value based on Group performance 2014 10 our core competency within Financial outlook 12 sound processing 18 BUSINESS DEVELOPMENT GN RESOUND GN ReSound 18 GN Netcom 26 • Leader in customer-driven innovations based on dif- Corporate social responsibility 35 ferentiated wireless 2.4 GHz technology Risk management 36 • Focused business model – dedicated wholesale 38 manufacturer refraining from vertical integration • Attractive market growth driven by sustainable SHAREHOLDER INFORMATION & GOVERNANCE megatrends in a consolidated industry with attrac- Shareholder information 38 tive profit margins Corporate governance 40 Board of directors 44 • Profitability in line with the best manufacturers in Executive management 46 the industry 47 GN NETCOM ADDITIONAL FINANCIAL INFORMATION • The world’s largest supplier of Unified Communica- Quarterly financial highlights 48 tions headsets driven by customer-focused com- Quarterly reporting by segment 49 mercialization of a state-of-the-art product portfolio Q4 segment disclosures 50 Foreign exchange impact 51 • Double digit mid- to long-term market growth GN ReSound income statement excl. SMART costs 52 driven by sustainable -

Fiscal Quarter-End Holdings (Pdf)

Quarterly Schedules of Portfolio Holdings International & Global Funds July 31, 2020 Retirement Institutional Administrative Investor Class Class Class Class Harbor Diversified International All Cap Fund HNIDX HAIDX HRIDX HIIDX Harbor Emerging Markets Equity Fund HNEMX HAEMX HREMX HIEEX Harbor Focused International Fund HNFRX HNFSX HNFDX HNFIX Harbor Global Leaders Fund HNGIX HGGAX HRGAX HGGIX Harbor International Fund HNINX HAINX HRINX HIINX Harbor International Growth Fund HNGFX HAIGX HRIGX HIIGX Harbor International Small Cap Fund HNISX HAISX HRISX HIISX Harbor Overseas Fund HAORX HAOSX HAOAX HAONX Table of Contents Portfolios of Investments HARBOR DIVERSIFIED INTERNATIONAL ALL CAP FUND. ..... 1 HARBOR EMERGING MARKETS EQUITY FUND . .......... 8 HARBOR FOCUSED INTERNATIONAL FUND. ................................. 11 HARBOR GLOBAL LEADERS FUND. ................. 13 HARBOR INTERNATIONAL FUND . 15 HARBOR INTERNATIONAL GROWTH FUND . ........................ 21 HARBOR INTERNATIONAL SMALL CAP FUND. ................. 24 HARBOR OVERSEAS FUND . ............................................ 26 Notes to Portfolios of Investments ..................................... 31 Harbor Diversified International All Cap Fund PORTFOLIO OF INVESTMENTS—July 31, 2020 (Unaudited) Value, Cost, and Principal Amounts in Thousands COMMON STOCKS—96.4% COMMON STOCKS—Continued Shares Value Shares Value AEROSPACE & DEFENSE—0.7% BANKS—Continued 28,553 Airbus SE (France)* .............................. $ 2,090 236,142 Svenska Handelsbanken AB (Sweden) ............... $ -

Annual General Meeting of GN Store Nord A/S

Annual General Meeting of GN Store Nord A/S Wednesday, March 17, 2021, at 10:00 a.m. (CET) Co.reg. no. 24257843 TO THE SHAREHOLDERS OF GN STORE NORD A/S The Annual General Meeting will be held on Wednesday, March 17, 2021, at 10:00 a.m. (CET) as a fully electronic general meeting without physical attendance. Attendance, request for admission card(s) and voting The Board of Directors has decided that the Annual General Meeting will be held as a fully electronic general meeting with a view to protect participating shareholders’ health and safety in light of COVID-19. Any shareholder who wishes to attend may attend electronically only. Registration Shareholders must register for GN Store Nord A/S’ Annual General Meeting by requesting an admission card. Admission cards can be obtained through the Shareholder Portal hosted by Computershare A/S at www.computershare.dk (also accessible through the company’s website at www.gn.com/agm) or by phone +45 45 46 09 97. Shareholders may attend the Annual General Meeting together with one accompanying person (advisor or guest). Shareholders wishing to attend the Annual General Meeting with an accompanying person have to request an extra admission card. The deadline for ordering admission card(s) is Friday, March 12, 2021, at 11:59 p.m. (CET). Admission cards are issued electronically. The admission card(s) will be sent to the email address provided by the shareholder on the Shareholder Portal at www.computershare.dk. Participation at the Annual General Meeting Participation takes place through LUMI AGM which is accessible through a web browser. -

Vanguard Total World Stock Index Fund Annual Report October 31, 2020

Annual Report | October 31, 2020 Vanguard Total World Stock Index Fund See the inside front cover for important information about access to your fund’s annual and semiannual shareholder reports. Important information about access to shareholder reports Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your fund’s annual and semiannual shareholder reports will no longer be sent to you by mail, unless you specifically request them. Instead, you will be notified by mail each time a report is posted on the website and will be provided with a link to access the report. If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. You may elect to receive shareholder reports and other communications from the fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with the fund, by calling Vanguard at one of the phone numbers on the back cover of this report or by logging on to vanguard.com. You may elect to receive paper copies of all future shareholder reports free of charge. If you invest through a financial intermediary, you can contact the intermediary to request that you continue to receive paper copies. If you invest directly with the fund, you can call Vanguard at one of the phone numbers on the back cover of this report or log on to vanguard.com. Your election to receive paper copies will apply to all the funds you hold through an intermediary or directly with Vanguard. -

Hear More, Do More, Be More GN Group – Annual Report 2017

GN Store Nord A/S Hear More, Do More, Be More GN Group – Annual Report 2017 2 Management's report ⋅ Contents Contents Contents Our investment case Management’s report Through relentless execution of 2017 at a glance 3 our 2017 – 2019 strategy “Hear Global reach, local presence 4 More, Do More, Be More”, we Business model and strategy 5 Business areas and brands 6 create shareholder value by Chairman's foreword 7 commercializing our core Consolidated financial highlights 9 Group performance 2017 10 competencies within sound Financial outlook 12 processing in attractive markets. GN Hearing 15 GN Audio 22 GN accolades and awards 29 GN Hearing Corporate responsibility 30 Risk management 32 Leader in customer-driven innovation in hearing aids Shareholder information 37 based on unique sound processing systems and Corporate governance 39 leading-edge wireless 2.4 GHz technology Board of Directors 43 Executive Management 45 • Focused business model – dedicated wholesale manufacturer, refraining from vertical integration Additional financial information 46 • Attractive market growth driven by sustainable Q4 financial highlights 47 megatrends in a consolidated industry with Quarterly financial highlights 48 attractive profit margins Quarterly reporting by segment 49 Q4 segment disclosures 50 • Profitability in line with the best manufacturers in the industry GN Audio Financial statements Consolidated - Financial statements 2017 51 The world’s leading supplier of Unified Parent company - Financial statements 2017 101 Communications headsets driven -

Reduction of GN Store Nord's Share Capital

Announcement no. 11 April 15, 2021 Reduction of GN Store Nord’s share capital At GN Store Nord’s annual general meeting on March 17, 2021, it was decided to authorize the board of directors to reduce the company’s share capital by nominally DKK 16,368,472 from nominally DKK 569,072,400 to nominally DKK 552,703,928 through the cancellation of treasury shares. In accordance with the authorization, today the board of directors has approved the capital reduction, and the capital reduction has been registered with the Danish Business Authority. Following the capital reduction, the company’s share capital amounts to nominally DKK 552,703,928 divided into 138,175,982 shares of DKK 4 each. As a consequence of the capital reduction, the company holds 8,299,342 treasury shares which correspond to 6.0% of the total share capital and voting rights. For further information, please contact: Investors and analysts Henriette Wennicke Vice President – Investor Relations & Treasury Tel: +45 45 75 03 33 Or Rune Sandager Director – Investor Relations & Treasury Tel: +45 45 75 92 57 Press and the media Lars Otto Andersen-Lange Head of Media Relations & Corporate Public Affairs Tel: +45 45 75 02 55 About GN Group The GN Group enables people to Hear More, Do More and Be More through its intelligent hearing, audio and video collaboration solutions. Inspired by people and driven by our innovation leadership, we leverage technological synergies between our hearing and audio divisions to deliver unique and increasingly individualized user experiences in our products and solutions. 150 years ago, GN was founded with a truly innovative and global mindset. -

Proxy Vote Record

Company Name Ticker Country Meeting Date Proposal Text Vote Instruction A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Receive Report of Board A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Accept Financial Statements and Statutory Reports For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Approve Discharge of Management and Board For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Approve Allocation of Income and Dividends of DKK 150 Per Share For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Reelect Jim Hagemann Snabe as Director For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Reelect Ane Maersk Mc-Kinney Uggla as Director For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Reelect Robert Maersk Uggla as Director For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Reelect Jacob Andersen Sterling as Director For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Reelect Thomas Lindegaard Madsen as Director For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Ratify PricewaterhouseCoopers as Auditors For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Authorize Board to Declare Extraordinary Dividend For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Approve DKK 784.9 Million Reduction in Share Capital via Share Cancellation For A.P. Moller-Maersk A/S MAERSK.B Denmark 23-Mar-20 Approve Guidelines for Incentive-Based Compensation for Executive Management and Board Against A.P. -

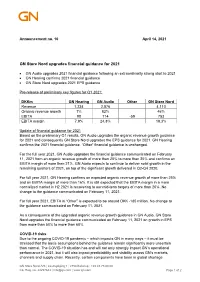

GN Store Nord Upgrades Financial Guidance for 2021

Announcement no. 10 April 14, 2021 GN Store Nord upgrades financial guidance for 2021 • GN Audio upgrades 2021 financial guidance following an extraordinarily strong start to 2021 • GN Hearing confirms 2021 financial guidance • GN Store Nord upgrades 2021 EPS guidance Pre-release of preliminary key figures for Q1 2021: DKKm GN Hearing GN Audio Other GN Store Nord Revenue 1,234 2,876 4,110 Organic revenue growth 1% 82% 46% EBITA 98 714 -59 753 EBITA margin 7.9% 24.8% 18.3% Update of financial guidance for 2021 Based on the preliminary Q1 results, GN Audio upgrades the organic revenue growth guidance for 2021 and consequently GN Store Nord upgrades the EPS guidance for 2021. GN Hearing confirms the 2021 financial guidance. “Other” financial guidance is unchanged. For the full year 2021, GN Audio upgrades the financial guidance communicated on February 11, 2021 from an organic revenue growth of more than 20% to more than 25% and confirms an EBITA margin of more than 21%. GN Audio expects to continue to deliver solid growth in the remaining quarters of 2021, on top of the significant growth delivered in Q2-Q4 2020. For full year 2021, GN Hearing confirms an expected organic revenue growth of more than 25% and an EBITA margin of more than 16%. It is still expected that the EBITA margin in a more normalized market in H2 2021 is recovering to our mid-term targets of more than 20%. No change to the guidance communicated on February 11, 2021. For full year 2021, EBITA in “Other” is expected to be around DKK -185 million. -

STATEMENT of INVESTMENTS Dreyfus Premier Total Return Advantage Fund July 31, 2007 (Unaudited)

STATEMENT OF INVESTMENTS Dreyfus Premier Total Return Advantage Fund July 31, 2007 (Unaudited) Coupon Maturity Principal Bonds and Notes--103.6% Rate (%) Date Amount ($) Value ($) Asset-Backed Ctfs./Auto Receivables--4.6% Capital One Auto Finance Trust, Ser. 2005-C, Cl. A3 4.61 7/15/10 57,941 57,806 Chase Manhattan Auto Owner Trust, Ser. 2003-C, Cl. A4 2.94 6/15/10 47,229 47,018 Daimler Chrysler Auto Trust, Ser. 2004-A, Cl. A4 2.58 4/8/09 40,568 40,391 Harley-Davidson Motorcycle Trust, Ser. 2004-1, Cl. A2 2.53 11/15/11 58,861 57,503 Honda Auto Receivables Owner Trust, Ser. 2005-5, Cl. A4 4.69 2/15/11 140,000 139,153 Household Automotive Trust, Ser. 2003-2, Cl. A4 3.02 12/17/10 49,853 49,489 USAA Auto Owner Trust, Ser. 2004-3, Cl. A4 3.53 6/15/11 100,000 98,865 WFS Financial Owner Trust, Ser. 2004-2, Cl. A4 3.54 11/21/11 62,435 61,869 552,094 Asset-Backed Ctfs./Credit Cards--3.3% Capital One Multi-Asset Execution Trust, Ser. 2005-A2, Cl. A2 4.05 2/15/11 100,000 99,216 Chase Issuance Trust, Ser. 2005-A10, Cl. A10 4.65 12/17/12 100,000 98,732 Citibank Credit Card Issuance Trust, Ser. 2003-A8, Cl. A8 3.50 8/16/10 100,000 98,317 MBNA Master Credit Card Trust, Ser. 2000-L, Cl. A 6.50 4/15/10 100,000 100,382 396,647 Asset-Backed Ctfs./Home Equity Loans--2.5% MASTR Asset-Backed Securities Trust, Ser.