FD 36514 2021.04.30 CP4 Objection to KCS Waiver V3.0

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Reporting Marks

Lettres d'appellation / Reporting Marks AA Ann Arbor Railroad AALX Advanced Aromatics LP AAMX ACFA Arrendadora de Carros de Ferrocarril S.A. AAPV American Association of Private RR Car Owners Inc. AAR Association of American Railroads AATX Ampacet Corporation AB Akron and Barberton Cluster Railway Company ABB Akron and Barberton Belt Railroad Company ABBX Abbott Labs ABIX Anheuser-Busch Incorporated ABL Alameda Belt Line ABOX TTX Company ABRX AB Rail Investments Incorporated ABWX Asea Brown Boveri Incorporated AC Algoma Central Railway Incorporated ACAX Honeywell International Incorporated ACBL American Commercial Barge Lines ACCX Consolidation Coal Company ACDX Honeywell International Incorporated ACEX Ace Cogeneration Company ACFX General Electric Rail Services Corporation ACGX Suburban Propane LP ACHX American Cyanamid Company ACIS Algoma Central Railway Incorporated ACIX Great Lakes Chemical Corporation ACJR Ashtabula Carson Jefferson Railroad Company ACJU American Coastal Lines Joint Venture Incorporated ACL CSX Transportation Incorporated ACLU Atlantic Container Line Limited ACLX American Car Line Company ACMX Voith Hydro Incorporated ACNU AKZO Chemie B V ACOU Associated Octel Company Limited ACPX Amoco Oil Company ACPZ American Concrete Products Company ACRX American Chrome and Chemicals Incorporated ACSU Atlantic Cargo Services AB ACSX Honeywell International Incorporated ACSZ American Carrier Equipment ACTU Associated Container Transport (Australia) Limited ACTX Honeywell International Incorporated ACUU Acugreen Limited ACWR -

March 2007 News.Pub

WCRA NEWS MARCH 2007 AGM FEB. 27, 2007 WESTERN RAILS SHOW MARCH 18, 2007 WCRA News, Page 2 ANNUAL GENERAL MEETING NOTICE Notice is given that the Annual General Meeting of the West Coast Railway Association will be held on Tuesday, February 27 at 1930 hours at Rainbow Creek Station. The February General Meeting of the WCRA will be held at Rainbow Creek Station in Confederation Park in Burnaby following the AGM. ON THE COVER Drake Street Roundhouse, Vancouver—taken November 1981 by Micah Gampe, and donated to the 374 Pavilion by Roundhouse Dental. Visible from left to right are British Columbia power car Prince George, Steam locomotive #1077 Herb Hawkins, Royal Hudson #2860’s tender, and CP Rail S-2 #7042 coming onto the turntable. In 1981, the roundhouse will soon be vacated by the railway, and the Provincial collection will move to BC Rail at North Vancouver. The Roundhouse will become a feature pavilion at Expo 86, and then be developed into today’s Roundhouse Community Centre and 374 Pavilion. Thanks to Len Brown for facilitating the donation of the picture to the Pavilion. MARCH CALENDAR • West Coast Railway Heritage Park Open daily 1000 through 1700k • Wednesday, March 7—deadline for items for the April 2007 WCRA News • Saturday, March 17 through Sunday, March 25—Spring Break Week celebrations at the Heritage Park, 1000—1700 daily • Tuesday, March 20—Tours Committee Meeting • Tuesday, March 27, 2007—WCRA General Meeting, Rainbow Creek Station in Confederation Park, Burnaby, 1930 hours. The West Coast Railway Association is an historical group dedicated to the preservation of British Columbia railway history. -

Transportation on the Minneapolis Riverfront

RAPIDS, REINS, RAILS: TRANSPORTATION ON THE MINNEAPOLIS RIVERFRONT Mississippi River near Stone Arch Bridge, July 1, 1925 Minnesota Historical Society Collections Prepared by Prepared for The Saint Anthony Falls Marjorie Pearson, Ph.D. Heritage Board Principal Investigator Minnesota Historical Society Penny A. Petersen 704 South Second Street Researcher Minneapolis, Minnesota 55401 Hess, Roise and Company 100 North First Street Minneapolis, Minnesota 55401 May 2009 612-338-1987 Table of Contents PROJECT BACKGROUND AND METHODOLOGY ................................................................................. 1 RAPID, REINS, RAILS: A SUMMARY OF RIVERFRONT TRANSPORTATION ......................................... 3 THE RAPIDS: WATER TRANSPORTATION BY SAINT ANTHONY FALLS .............................................. 8 THE REINS: ANIMAL-POWERED TRANSPORTATION BY SAINT ANTHONY FALLS ............................ 25 THE RAILS: RAILROADS BY SAINT ANTHONY FALLS ..................................................................... 42 The Early Period of Railroads—1850 to 1880 ......................................................................... 42 The First Railroad: the Saint Paul and Pacific ...................................................................... 44 Minnesota Central, later the Chicago, Milwaukee and Saint Paul Railroad (CM and StP), also called The Milwaukee Road .......................................................................................... 55 Minneapolis and Saint Louis Railway ................................................................................. -

Transcontinental Railways and Canadian Nationalism Introduction Historiography

©2001 Chinook Multimedia Inc. Page 1 of 22 Transcontinental Railways and Canadian Nationalism A.A. den Otter ©2001 Chinook Multimedia Inc. All rights reserved. Unauthorized duplication or distribution is strictly prohibited. Introduction The Canadian Pacific Railway (CPR) has always been a symbol of Canada's nation-building experience. Poets, musicians, politicians, historians, and writers have lauded the railway as one of the country's greatest achievements. Indeed, the transcontinental railway was a remarkable accomplishment: its managers, engineers, and workers overcame incredible obstacles to throw the iron track across seemingly impenetrable bogs and forests, expansive prairies, and nearly impassable mountains. The cost in money, human energy, and lives was enormous. Completed in 1885, the CPR was one of the most important instruments by which fledgling Canada realized a vision implicit in the Confederation agreement of 1867-the building of a nation from sea to sea. In the fulfilment of this dream, the CPR, and subsequently the Canadian Northern and Grand Trunk systems, allowed the easy interchange of people, ideas, and goods across a vast continent; they permitted the settlement of the Western interior and the Pacific coast; and they facilitated the integration of Atlantic Canada with the nation's heartland. In sum, by expediting commercial, political, and cultural intercourse among Canada's diverse regions, the transcontinentals in general, and the CPR in particular, strengthened the nation. Historiography The first scholarly historical analysis of the Canadian Pacific Railway was Harold Innis's A History of the Canadian Pacific Railway. In his daunting account of contracts, passenger traffic, freight rates, and profits, he drew some sweeping conclusions. -

CP's North American Rail

2020_CP_NetworkMap_Large_Front_1.6_Final_LowRes.pdf 1 6/5/2020 8:24:47 AM 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 Lake CP Railway Mileage Between Cities Rail Industry Index Legend Athabasca AGR Alabama & Gulf Coast Railway ETR Essex Terminal Railway MNRR Minnesota Commercial Railway TCWR Twin Cities & Western Railroad CP Average scale y y y a AMTK Amtrak EXO EXO MRL Montana Rail Link Inc TPLC Toronto Port Lands Company t t y i i er e C on C r v APD Albany Port Railroad FEC Florida East Coast Railway NBR Northern & Bergen Railroad TPW Toledo, Peoria & Western Railway t oon y o ork éal t y t r 0 100 200 300 km r er Y a n t APM Montreal Port Authority FLR Fife Lake Railway NBSR New Brunswick Southern Railway TRR Torch River Rail CP trackage, haulage and commercial rights oit ago r k tland c ding on xico w r r r uébec innipeg Fort Nelson é APNC Appanoose County Community Railroad FMR Forty Mile Railroad NCR Nipissing Central Railway UP Union Pacic e ansas hi alga ancou egina as o dmon hunder B o o Q Det E F K M Minneapolis Mon Mont N Alba Buffalo C C P R Saint John S T T V W APR Alberta Prairie Railway Excursions GEXR Goderich-Exeter Railway NECR New England Central Railroad VAEX Vale Railway CP principal shortline connections Albany 689 2622 1092 792 2636 2702 1574 3518 1517 2965 234 147 3528 412 2150 691 2272 1373 552 3253 1792 BCR The British Columbia Railway Company GFR Grand Forks Railway NJT New Jersey Transit Rail Operations VIA Via Rail A BCRY Barrie-Collingwood Railway GJR Guelph Junction Railway NLR Northern Light Rail VTR -

Federal Railroad Administration Fiscal Year 2017 Enforcement Report

Federal Railroad Administration Fiscal Year 2017 Enforcement Report Table of Contents I. Introduction II. Summary of Inspections and Audits Performed, and of Enforcement Actions Recommended in FY 2017 A. Railroad Safety and Hazmat Compliance Inspections and Audits 1. All Railroads and Other Entities (e.g., Hazmat Shippers) Except Individuals 2. Railroads Only B. Summary of Railroad Safety Violations Cited by Inspectors, by Regulatory Oversight Discipline or Subdiscipline 1. Accident/Incident Reporting 2. Grade Crossing Signal System Safety 3. Hazardous Materials 4. Industrial Hygiene 5. Motive Power and Equipment 6. Railroad Operating Practices 7. Signal and train Control 8. Track C. FRA and State Inspections of Railroads, Sorted by Railroad Type 1. Class I Railroads 2. Probable Class II Railroads 3. Probable Class III Railroads D. Inspections and Recommended Enforcement Actions, Sorted by Class I Railroad 1. BNSF Railway Company 2. Canadian National Railway/Grand Trunk Corporation 3. Canadian Pacific Railway/Soo Line Railroad Company 4. CSX Transportation, Inc. 5. The Kansas City Southern Railway Company 6. National Railroad Passenger Corporation 7. Norfolk Southern Railway Company 8. Union Pacific Railroad Company III. Summaries of Civil Penalty Initial Assessments, Settlements, and Final Assessments in FY 2017 A. In General B. Summary 1—Brief Summary, with Focus on Initial Assessments Transmitted C. Breakdown of Initial Assessments in Summary 1 1. For Each Class I Railroad Individually in FY 2017 2. For Probable Class II Railroads in the Aggregate in FY 2017 3. For Probable Class III Railroads in the Aggregate in FY 2017 4. For Hazmat Shippers in the Aggregate in FY 2017 5. -

Baker & Miller Pllc

301783 ENTERED BAKER & MILLER PLLC Office of Proceedings March 19 2021 Part of 2401 PENNSYLVANIA AVENUE, NW S U I T E 3 0 0 Public Record WASHINGTON, DC 20037 ( 2 0 2 ) 6 6 3 - 7 8 2 0 ( 2 0 2 ) 6 6 3 - 7 8 4 9 William A. Mullins Direct Dial: (202) 663 - 7 8 2 3 E - M a i l : [email protected] March 19, 2021 VIA E-FILING Ms. Cynthia T. Brown Chief, Section of Administration Office of Proceedings Surface Transportation Board 395 E Street, S.W., Room 1034 Washington, DC 20423-0001 Re: FD 36472 CSX Corporation and CSX Transportation, Inc. – Control and Merger – Pan Am Systems, Inc., Pan Am Railways, Inc., Boston & Maine Corporation, Maine Central Railroad Company, Northern Railroad, Pan Am Southern LLC, Portland Terminal Company, Springfield Terminal Railway Company, Stony Brook Railroad Company, and Vermont & Massachusetts Railroad Company FD 36472 (Sub-No. 5) Pittsburg & Shawmut Railroad, LLC d/b/a Berkshire & Eastern Railroad – Operation of Property of Rail Carrier Pan Am Southern LLC – Pan Am Southern LLC and Springfield Terminal Railway Company Reply Comments of Norfolk Southern Railway Company Dear Ms. Brown: Norfolk Southern Railway Company (“NSR”) hereby submits the following comments in reply to the Application (the “Application”) filed by CSX Corporation (“CSX”) and CSX Transportation, Inc. (“CSXT”) (collectively, the “Applicants”). NSR supports the proposed transaction as submitted. Baker & Miller PLLC Ms. Cynthia T. Brown March 19, 2021 Page 2 of 4 NSR initially had some concerns about possible adverse anticompetitive effects that would arise from an unconditioned transaction,1 but CSXT and NSR have discussed and worked through those concerns. -

MDOT Michigan State Rail Plan Tech Memo 2 Existing Conditions

Technical Memorandum #2 March 2011 Prepared for: Prepared by: HNTB Corporation Table of Contents 1. Introduction ..............................................................................................................1 2. Freight Rail System Profile ......................................................................................2 2.1. Overview ...........................................................................................................2 2.2. Class I Railroads ...............................................................................................2 2.3. Regional Railroads ............................................................................................6 2.4. Class III Shortline Railroads .............................................................................7 2.5. Switching & Terminal Railroads ....................................................................12 2.7. State Owned Railroads ...................................................................................16 2.8. Abandonments ................................................................................................18 2.10. International Border Crossings .....................................................................22 2.11. Ongoing Border Crossing Activities .............................................................24 2.12. Port Access Facilities ....................................................................................24 3. Freight Rail Traffic ................................................................................................25 -

Rail-Hwy Crossing Inventory Bulletin No.17,1994

HIGHWAY-RAIL CROSSING ACCIDENT/INCIDENT AND INVENTORY BULLETIN NO. 17 CALENDAR YEAR 1994 W4444444444444444444 U.S. Department of Transportation Federal Railroad Administration Office of Safety NOTICE This document is disseminated under the sponsorship of the Department of Transportation in the interest of the information exchange. The United States Government assumes no liability for its contents or use. This document only reflects data information. Information is viewed in summaries and tables. No graphics are depicted in this document. This document is prepared in WordPerfect 6.1 and saved as a WordPerfect 5.1 document with fonts defined in courier new, 10pt., and the top, bottom, left, and right margins are the smallest possible. Remember that you may have to adjust your font to enable proper printing or viewing of this document. Federal Railroad Administration Office of Safety, RRS-22 400 Seventh Street, S.W. Washington, D.C. 20590 TABLE OF CONTENTS SECTIONS INTRODUCTION ......................................... RESOURCE ALLOCATION PROCEDURE CONSTANTS .............. TABLE-S. Summary of Highway-Rail Crossing Accident Statistics for the Nation ............................ HISTORICAL ACCIDENT TRENDS - DATA TABLE 1. Summary of Accidents/Incidents and Casualties at Highway-Rail Crossings ........................ TABLE 2. Summary of Accidents/Incidents and Accident Rates at Highway-Rail Crossings Involving Motor Vehicles .......................... CURRENT YEAR ACCIDENT DATA AT PUBLIC CROSSINGS ONLY - DATA TABLE 3. Accidents/Incidents at Highway-Rail Crossings by State ............... TABLE 4. MV Accidents/Incidents at Highway-Rail Crossings by State ............... TABLE 5. Accidents/Incidents at Highway-Rail by Type of Motor Vehicle ......... TABLE 6. MV Accidents/Incidents at Highway-Rail Crossings by Type of Consist ..... TABLE 7. MV Accidents/Incidents at Highway-Rail Crossings by Warning Device by Railroad ......................... -

Rocky Mountain Express

ROCKY MOUNTAIN EXPRESS TEACHER’S GUIDE TABLE OF CONTENTS 3 A POSTCARD TO THE EDUCATOR 4 CHAPTER 1 ALL ABOARD! THE FILM 5 CHAPTER 2 THE NORTH AMERICAN DREAM REFLECTIONS ON THE RIBBON OF STEEL (CANADA AND U.S.A.) X CHAPTER 3 A RAILWAY JOURNEY EVOLUTION OF RAIL TRANSPORT X CHAPTER 4 THE LITTLE ENGINE THAT COULD THE MECHANICS OF THE RAILWAY AND TRAIN X CHAPTER 5 TALES, TRAGEDIES, AND TRIUMPHS THE RAILWAY AND ITS ENVIRONMENTAL CHALLENGES X CHAPTER 6 DO THE CHOO-CHOO A TRAIL OF INFLUENCE AND INSPIRATION X CHAPTER 7 ALONG THE RAILROAD TRACKS ACTIVITIES FOR THE TRAIN-MINDED 2 A POSTCARD TO THE EDUCATOR 1. Dear Educator, Welcome to our Teacher’s Guide, which has been prepared to help educators integrate the IMAX® motion picture ROCKY MOUNTAIN EXPRESS into school curriculums. We designed the guide in a manner that is accessible and flexible to any school educator. Feel free to work through the material in a linear fashion or in any order you find appropriate. Or concentrate on a particular chapter or activity based on your needs as a teacher. At the end of the guide, we have included activities that embrace a wide range of topics that can be developed and adapted to different class settings. The material, which is targeted at upper elementary grades, provides students the opportunity to explore, to think, to express, to interact, to appreciate, and to create. Happy discovery and bon voyage! Yours faithfully, Pietro L. Serapiglia Producer, Rocky Mountain Express 2. Moraine Lake and the Valley of the Ten Peaks, Banff National Park, Alberta 3 The Film The giant screen motion picture Rocky Mountain Express, shot with authentic 15/70 negative which guarantees astounding image fidelity, is produced and distributed by the Stephen Low Company for exhibition in IMAX® theaters and other giant screen theaters. -

Madison County January 8, 2016 Mitchell Lenox Tower Reconfiguration (UPPR MP 270) High-Speed Rail – Chicago to St

2300 South Dirksen Parkway / Springfield, Illinois / 62764 Madison County January 8, 2016 Mitchell Lenox Tower Reconfiguration (UPPR MP 270) High-Speed Rail – Chicago to St. Louis IDOT Sequence #18436 Federal - Section 106 Project ADVERSE EFFECT – PROPOSED MITIGATION Dr. Rachel Leibowitz Deputy State Historic Preservation Officer Illinois Historic Preservation Agency Springfield, Illinois 62701 Dear Dr. Leibowitz: In coordination with the Federal Railroad Administration (FRA), the Illinois Department of Transportation (IDOT) proposes to replace the Lenox Tower located at the junction of Union Pacific (UPRR) rail lines in Mitchell, Illinois. The existing tower and its associated switching equipment are obsolete. For the High- Speed Rail (HSR) program, the tower must be replaced with modern equipment. This action will cause an Adverse Effect to the Lenox Tower, a resource determined eligible for the National Register of Historic Places. This Adverse Effect finding is documented in the attached concurrence letter dated August 12, 2014. The attached draft document outlines proposed mitigation measures, which include Historic American Building Survey recordation and marketing of tower components prior to the removal of the tower. On behalf of the FRA and in accordance with the HSR Programmatic Agreement, ratified January 24, 2014, we request your review of the proposed mitigation measures. Please provide comments within 30 days. If you have no comments, then we request the concurrence of the State Historic Preservation Officer regarding the proposed mitigation measures. Sincerely, Brad H. Koldehoff, RPA Cultural Resources Unit Bureau of Design & Environment Cc: Andrea Martin (FRA), Chris Wilson (ACHP), and concurring parties DRAFT Section 106/Section 4(f) Documentation of Adverse Effect for Lenox Tower Chicago to St. -

Canadian Pacific Railway Investigation of Safety-Related Occurrences Protocol Considered Helpful by Both Labor and Management

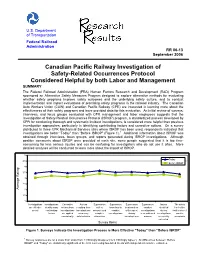

U.S. Department of Transportation Federal Railroad Administration RR 06-13 September 2006 Canadian Pacific Railway Investigation of Safety-Related Occurrences Protocol Considered Helpful by both Labor and Management SUMMARY The Federal Railroad Administration (FRA) Human Factors Research and Development (R&D) Program sponsored an Alternative Safety Measures Program designed to explore alternative methods for evaluating whether safety programs improve safety outcomes and the underlying safety culture, and to conduct implementation and impact evaluations of promising safety programs in the railroad industry. The Canadian Auto Workers Union (CAW) and Canadian Pacific Railway (CPR) are interested in learning more about the effectiveness of their safety programs and have provided data for this evaluation. An initial review of surveys, interviews, and focus groups conducted with CPR management and labor employees suggests that the Investigation of Safety-Related Occurrences Protocol (ISROP) program, a standardized process developed by CPR for conducting thorough and systematic incident investigations, is considered more helpful than previous investigation approaches, particularly in identifying contributing factors and corrective actions. On a survey distributed to three CPR Mechanical Services sites where ISROP has been used, respondents indicated that investigations are better “Today” than “Before ISROP” (Figure 1).1 Additional information about ISROP was obtained through interviews, focus groups, and reports generated during ISROP investigations. Although positive comments about ISROP were provided at each site, some people suggested that it is too time- consuming for less serious injuries and can be confusing for investigators who do not use it often. More detailed analyses will be conducted to learn more about the impact of ISROP.