Konkan Railway Corporation Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Indian Railways Facts & Figures 2016-17

INDIAN RAILWAYS FACTS & FIGURES 2016-17 BHARAT SARKAR GOVERNMENT OF INDIA RAIL MANTRALAYA MINISTRY OF RAILWAYS (RAILWAY BOARD) KEY STATISTICS 2016-17 1. Route Length (Kms.) - Broad Gauge (1.676 M.) 61,680 - Metre Gauge (1.000 M.) 3,479 - Narrow Gauge 2,209 (0.762 M. and 0.610 M.) Total 67,368 2. Double and Multiple Track - Broad Gauge 22,021 (Route Kms.) - Metre Gauge - Total 22,021 3. Electrified Track (Route Kms.) - Broad Gauge 25,367 - Metre Gauge - Total 25,367 4. Number of Railway Stations 7,349 5. Number of Railway Bridges 1,44,698 6. Traffic Volume Passengers Originating (Millions) 8,116 Passenger Kms. 1,149,835 Tonnes Originating (Rev. Traffic) (Millions Tonnes) 1,106.15 Tonne Kms. (Millions) 620,175 7. Number of Employees (Thousands) 1308 8. Revenue (` in Millions) 1,65,292.20 9. Expenses (` in Millions) 1,59,029.61 10. Rolling Stock - Locomotives: - Steam 39 - Diesel 6,023 - Electric 5,399 Total 11,461 - Passenger Carriages 64,223 - Freight Cars/Wagons 2,77,987 Note : All the figures, unless otherwise stated, are as at the end of the fiscal year i.e. March 31, 2017. CONTENTS Review of the year 5 Originating Passengers & Average Lead 6 Passenger Kilometres 7 Passenger Services 8 Passenger Revenue 9 Freight Operations — Originating Tonnage 10 — Net Tonne Kms. 11 — Freight Train & Wagon Kms. 12 — Commodity wise Loading 13 — Commodity wise NTKms. 14 — Average Lead 15 — Revenue 16 — Commodity wise Earnings 17 Rolling Stock — Locomotives 18 — Passenger Coaches 19 — Freight Cars/Wagons 20 Track/Route Kilometres 21 Gross Tonne Kilometres 22 Electrification 23 Signalling 24 Telecommunication 25 Personnel 26 Revenue 27 Expenses 28 Net Revenue & Excess/Shortfall 29 Assets 30 Asset Utilisation 31 Engine Kms. -

Railway Budget 1996-97 — General Discussion And

393 Railway Budget, 1996-97 and SRAVANA 3. 1918 (Saka) Demands for Grants on Account (Rly) 394 (vi) Industrial Disputes (Amendment) Bill. that this new railway track would be laid Bastar 1996. (As passed by Rajya Sabha) has large forest wealth and the mineral wealth but no railway line has been provided there. The (4) General Discussion on the Budget (General) tor construction of new railway line will open up new 1996-97. dimensions of development and it can benefit the SC- Tuesday, 30th July 1996 ST people (1) Reply ot Minister of Railways Madam seven successive Railway Ministers had (2) Submission to the vote of the House Demands promised in their Railway Budgets laying of Dina - for Grants for Railways for 1996-97 and Purvai - Mahava- Chowpata - Siroj - Beavara railway consideration and passing of the relevant line for which survey was ordered Half the survey has Appropriation Bill been completed But what is the use of half survey Similarly, there is Guna - Shiopuri - Bhind - Etawah (3) General Discussion on the Budget (General) for railway line and the Railway Minister have been 1996-97 repeatedly assuring its completion But this Budget does I am calling the next speaker In the meantime if . not include any provision for this rail track The Lalitpur there is any correction to be made. I will let the hon - Khajuraho - Singrauli track was sanctioned in 1981- Members know 82 I would like to know from the hon ble Railway Minister when this line will be taken up for construction Now I call upon Shri Shivraj Singh to speak The Korba-Ranchi line is pending for the last 12 years and a sum of Rs 80 crore has been spent on the survey of it but no action has been taken to start work 00.12 hrs. -

The Crisis of Public Transport in India

The Crisis of Public Transport in India The Crisis of Public Transport in India: Overwhelming Needs but Limited Resources John Pucher and Nisha Korattyswaroopam, Rutgers University Neenu Ittyerah, Indian Railways, Chennai, India Abstract The rapid growth of India’s urban population has put enormous strains on all trans- port systems. Burgeoning travel demand far exceeds the limited supply of transport infrastructure and services. Public transport, in particular, has been completely over- whelmed. Most bus and train services are overcrowded, undependable, slow, incon- venient, uncoordinated, and dangerous. Moreover, the public ownership and opera- tion of most public transport services has greatly reduced productivity and inflated costs. India’s cities desperately need improved and expanded public transport ser- vice. Unfortunately, meager government financial assistance and the complete lack of any supportive policies, such as traffic priority for buses, place public transport in an almost impossible situation. Introduction Public transport faces severe problems in almost all countries of the developing world, although the situation varies from one country to another, and even from one city to another (Vasconcellos 2001). Perhaps most important, the lack of fi- nancial resources prevents necessary investments in maintaining and upgrading 95 Journal of Public Transportation, Vol. 7, No. 3, 2004 existing bus and rail systems and building new ones. Likewise, many advanced tech- nologies long available in Western Europe are simply not affordable in most devel- oping countries. Public transport systems in the Third World are plagued by chronic corruption and inefficiency, overcrowded and undependable service, congested roadways that slow down buses, and an operating environment that is often cha- otic and completely uncoordinated. -

Speech of Mamata Banerjee Introducing the Railway Budget 2011-12 25Th February 2011

Speech of Mamata Banerjee introducing the Railway Budget 2011-12 25th February 2011 1. Madam Speaker, I rise to present before this august House the Revised Estimates for 2010-11 and the estimated receipts and expenditure for 2011-12. I deem it an honour to present the third Railway Budget under the kind guidance of the hon'ble Prime Minister. I profusely thank the Finance Minster for his continued support and encouragement to the railways. 2. As the hon’ble members are aware, the wheels of the railways continue to move 24 hours, all 365 days. Railway’s services are comparable to emergency services, required all the time. I am proud of the 14 lakh members of my railway family, who toil day and night with unparalleled dedication. I am also grateful to all passengers without whose cooperation and consideration, we could not have run this vast system. I have also received unstinted support from our two recognised federations and staff and officers’ associations. 3. Madam, rail transportation is vitally interlinked with the economic development of the country. With the economy slated to grow at a rate of 8-9%, it is imperative that the railways grow at an even faster pace. I see the railways as an artery of this pulsating nation. Our lines touch the lives of humble people in tiny villages, as they touch the lives of those in the bustling metropolises. 4. We are taking a two-pronged approach, scripted on the one hand, by a sustainable, efficient and rapidly growing Indian Railways, and on the other, by an acute sense of social responsibility towards the common people of this nation. -

Konkan Railway Corporation Limited Telephone Directory

KONKAN RAILWAY CORPORATION LIMITED TELEPHONE DIRECTORY CORPORATE OFFICE: 022 - 27572015 - 18 / 022 – 27587180 & FAX NO: 022-27572420 COMMERCIAL CONTROL - 022-27587394 GENERAL DEPARTMENT - 022-27587441 MTNL Phone DESIGNATION NAME (CODE-022) CHAIRMAN & 27570415 MANAGING DIRECTOR 27587300 SANJAY GUPTA DIRECTOR (OPERATIONS & 27579953 COMMERCIAL) 27587301 27579950 DIRECTOR (WAY & WORKS) RAJENDRA KUMAR 27587302 27570353 DIRECTOR (FINANCE) AMITABH BANERJEE 27587303 27579948 COMPANY SECRETARY R. C. PARAB 27587305 SECRETARY TO CHAIRMAN & 27570415 U. S. SHENDYE MANAGING DIRECTOR 27587306 CHIEF MANAGER SIDDHESHWAR C. 27572679 (ADMINISTRATION) TELUGU 27587441 CHIEF PUBLIC RELATIONS 27561085 L. K. VERMA OFFICER 27587395 DEPUTY GENERAL MANAGER SMT. VAISHALI 27587442 (TRAINING) PATANGE LAW OFFICER ANIL PATIL 27587307 ACCOUNTS FINANCIAL ADVISOR & CHIEF 27572354 MATHEW PHILIP ACCOUNT OFFICER 27587310 DEPUTY FINANCIAL ADVISOR & CHIEF ACCOUNTS OFFICER A. D. PATANKAR 27587312 (ESTABLISHMENTS & PROJECT) 27570421 DEPUTY GENERAL MANAGER VINAYAK SALVI 27587318 (FINANCE) 27570421 (F) Continued… MTNL Phone DESIGNATION NAME (CODE-022) DEPUTY GENERAL MANAGER P. B. NANIVADEKAR 27587313 (ACCOUNTS) COMMERCIAL 27572126 CHIEF COMMERCIAL MANAGER D. S. LINGARAJU 27587490 ELECTRICAL 27579932 CHIEF ELECTRICAL ENGINEER A. K. BHARADWAJ 27587340 CHIEF ELECTRICAL ENGINEER/ 27561902 CONSTRUCTION/RAILWAY D. N. MAHAJAN ELECTRIFICATION 27587341 DEPUTY CHIEF ELECTRICAL ENGINEER/ RAILWAY M. P. KHOBRAGADE 27587347 ELECTRIFICATION ENGINEERING 27579951 CHIEF ENGINEER L. PRAKASH 27587322 -

Preparatory Survey on the Urban Railway Project in Pune City

PUNE MUNICIPAL CORPORATION PUNE, MAHARASHTRA, INDIA PREPARATORY SURVEY ON THE URBAN RAILWAY PROJECT IN PUNE CITY FINAL REPORT JUNE 2013 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. OS TOSHIBA CORPORATION JR(先) INTERNATIONAL DEVELOPMENT CENTER OF JAPAN INC. 13-067 PUNE MUNICIPAL CORPORATION PUNE, MAHARASHTRA, INDIA PREPARATORY SURVEY ON THE URBAN RAILWAY PROJECT IN PUNE CITY FINAL REPORT JUNE 2013 JAPAN INTERNATIONAL COOPERATION AGENCY ORIENTAL CONSULTANTS CO., LTD. TOSHIBA CORPORATION INTERNATIONAL DEVELOPMENT CENTER OF JAPAN INC. Preparatory Survey on the Urban Railway Project in Pune City Final Report TABLE OF CONTENTS List of Abbreviations Page Chapter 1 Implementation Policy 1.1 Basic Policy of the Study ...................................................................................................... 1-1 1.1.1 Background of the Study............................................................................................... 1-1 1.1.2 Purpose of this Study..................................................................................................... 1-2 1.1.3 Approach to Conducting the Study ............................................................................... 1-2 1.1.4 Study Methodology ....................................................................................................... 1-7 1.1.5 Selection of Study Team Members and Schedule ......................................................... 1-9 1.2 Target Area of this Study ................................................................................................... -

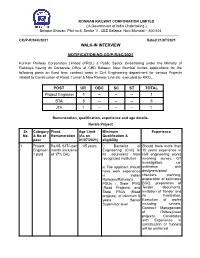

Walk-In-Interview for the Post of Project Engineer

KONKAN RAILWAY CORPORATION LIMITED ( A Government of India Undertaking ) Belapur Bhavan, Plot no.6, Sector 11, CBD Belapur, Navi Mumbai – 400 614 ----------------------------------------------------------------------------------------------------------------------------------- CO/P-R/04C/2021 Dated:21/07/2021 WALK-IN INTERVIEW NOTIFICATION NO.CO/P-R/4C/2021 Konkan Railway Corporation Limited (KRCL) a Public Sector Undertaking under the Ministry of Railways having its Corporate Office at CBD Belapur, Navi Mumbai invites applications for the following posts on fixed term contract basis in Civil Engineering department for various Projects related to Construction of Road, Tunnel & New Railway Line etc. executed by KRCL. POST UR OBC SC ST TOTAL Project Engineer 1 -- -- -- 1 STA 5 -- -- -- 5 JTA 1 -- -- -- 1 Remuneration, qualification, experience and age details. Kerala Project Sr. Category Fixed Age Limit Minimum Experience No. & No of Remuneration (As on Qualification & post 01/07/2021) eligibility 1 Project Rs.65, 637/- per 45 years i) Bachelor of Should have more than Engineer- month (inclusive Engineering (Civil) or 10 years experience in 1 post of 17% DA). its equivalent from civil engineering works recognized institution. involving survey, GT investigation, co- ii) The applicant should ordination with have work experience designers/proof in Indian checkers, planning, Railways/Railway’s preparation of estimates PSUs / State PWD BOQ, preparation of (Road Projects) and Tender documents, State PSUs (Road Invitation of Tender and projects), -

Indian Railways Budget Speech 1998 -1999 (Final) 636 Speech of Shri Nitish Kumar Introducing the Railway Budget for 1998

Indian Railways Budget Speech 1998 -1999 (Final) Speech of Shri Nitish Kumar Introducing the Railway Budget for 1998- 99, on 29 th May 1998 Mr. Speaker, Sir, I rise to present the Budget Estimates for 1998-99 for the Indian Railways. These Estimates reflect certain decisions taken by the Government after I presented an interim Budget to this august House on the 25th of March 1998. Introduction 2. In the last few months, Sir, I have had the opportunity of looking at the Indian Railways from close quarters. I have formed certain perceptions about their role, the present state of their health, the problems they face and the possible solutions. I would like to share these perceptions briefly with the Hon'ble Members. 3. Besides being a symbol of national integration, the Indian Railways are both a barometer and a principal determinant of the economic and social health of the nation. At this juncture, when the country is poised for significantly higher economic growth, Indian Railways cannot fail to match that growth. People must therefore know certain facts about the Railways - especially what the Railways can do, what they are unable to do and why. The Status Paper laid by me in the House two days back is an attempt to bring out these facts. 4. On this occasion, I would like to highlight a few of the basic issues that confront the Indian Railways. Sir, it is well known that Railways have a number of intrinsic advantages - they are six times more energy efficient, four times more efficient in land use and significantly superior from the standpoints of environmental impact and safety as compared to road transport. -

KONKAN RAILWAY CORPORATION LIMITED (~ Wcf)R Q)F~) (A GOVERNMENT of INDIA UNDERTAKING)

~~~~ KONKAN RAILWAY CORPORATION LIMITED (~ WCf)R q)f~) (A GOVERNMENT OF INDIA UNDERTAKING) ~ ~~ (Corporate Identity Number): U35201MH1990G0I223738 No.CO-13014{11 )/18/2015-PERS[3325] Date:- 27-05-2019 Director (Deputation) Ministry of Railways Railway Board Rail Bhavan New Delhi -110 001. Sub:- Notification for the post of Chief Electrical Engineer/RE (CEE/RE) on Deputation basis at Belapur/Margao/Udupi/Manglore. Ref:- Railway Board's circular dated 07.03.2018. Reference above, KRCL is in need of one officer from Indian Railways / Railway PSU as Chief Electrical Engineer/RE (CEE/RE) on Deputation basis at Belapur/Margao /Udupi/ Manglore. Requirement has been notified on KRCL website at link www.konkanrailway.com --> Recruitment --> Current notifications. As advised by Railway Board vide its letter referred above, PDF of the said notification is enclosed herewith for uploading the same on Indian Railways website for wide publicity. Requested to upload on Indian Railways website as early as possible. This issues with approval of the Competent Authority (CM D). Encl :- Notification. ~~: ~ 'I'j"q.'f, ~ - 11, m.<ft."it.~, -::rcft~ - 400614. Regd. Office: Belapur Bhavan, Sector- 11, CBD Belapur, Navi Mumbai 400 614. Tel: 91-22-27572015-18; Fax 27572420 {-it'0 (E-mail):[email protected] • ~ (Website) : www.konkanrailway.com LE! No. 335800CK2UZ7PG7WLL79 VACANCY NOTICE NO. DE-19-2019 et; a)i ISSUED ON:27-05-2019 ~~ LAST DATE:26-06-2019 Cfi1CfiOl ~ ~rcrr ~ (3ffiCi ~ CfiT ~) KONKAN RAILWAY CORPORATION LIMITED (Govt. of India undertaking) GENERAL MANAGERS ALL RAILWAYS/PRODUCTION UNITS. DIRECTOR GENERAL'S/DIRECTORS ALL RAILWAY TRAINING INSTITUTES. CMD/MD/CHAIRMAN ALL PSUs. -

Unclassified ENV/EPOC/GF/SD/RD(2004)5/FINAL

Unclassified ENV/EPOC/GF/SD/RD(2004)5/FINAL Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development 07-Feb-2005 ___________________________________________________________________________________________ _____________ English - Or. English ENVIRONMENT DIRECTORATE Environment Policy Committee Unclassified ENV/EPOC/GF/SD/RD(2004)5/FINAL Global Forum on Sustainable Development DEVELOPMENT AND CLIMATE: IMPACTS AND ADAPTATION FOR INFRASTRUCTURE ASSETS IN INDIA by P.R. Shukla, Manmohan Kapshe and Amit Garg Paris, 11-12 November 2004 English - Or. English JT00178103 Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format ENV/EPOC/GF/SD/RD(2004)5/FINAL Copyright OECD, 2004 Application for permission to reproduce or translate all or part of this material should be addressed to the Head of Publications Service, OECD, 2 rue André Pascal, 75775 Paris, Cédex 16, France. 2 ENV/EPOC/GF/SD/RD(2004)5/FINAL TABLE OF CONTENTS DEVELOPMENT AND CLIMATE: IMPACTS AND ADAPTATION FOR INFRASTRUCTURE ASSETS IN INDIA ........................................................................................................................................ 5 1. Introduction ...................................................................................................................................... 6 2. Infrastructure development in India ................................................................................................. 7 -

100 Days Initiatives & Achievements

Ministry of Railways, Government of India September 2019 Government Of India 100 DAYS INITIATIVES & ACHIEVEMENTS “Indian Railways is the growth engine of nation’s vikas yatra” - Narendra Modi, Prime Minister BEST EVER SAFETY RECORD Zero passenger fatalities during Apr-Aug 2019 SECURITY FIRST Commandos for Railway Security Launch of the first Railway Commando Battalion ‘CORAS’ to tackle the menace of terrorism and naxalism in Railways HIGHER INVESTMENT Highest ever CAPEX: Rs. 1,60,176 crore in 2019-20 20% higher over 2018-19 Budget 2019 proposed investment of Rs 50 lakh crore until 2030 INFRASTRUCTURE THRUST APPROVAL FOR CONNECTING INDIA RAISING OF SPEED -LINES APPROVED TO 160 KMPH BY 2022 3rd line between Allahabad- -23 ON DELHI-MUMBAI Pt. Deen Dayal Upadhyay Junction (UP) AND DELHI-HOWRAH ROUTES New Line between Sahjanwa-Dohrighat (UP) 60% increase in average speed of passenger trains Doubling of Line from New Bongaigaon-Agthori (Assam) Journeys by Rajdhani train to become fully overnight New Line between Vaibhavwadi-Kolhapur (Maharashtra) FASTER TOWARDS A GREEN CONSTRUCTION ELECTRIFIED RAILWAYS New line, Doubling and Gauge 1,106 RKM electrified during Apr-Aug 2019 conversion increased by 36% 1500 1000 704 km 518 km 500 0 Apr-Aug 2018 Apr-Aug 2019 Elimination of manned level crossings increased by 220% 4 3.49 3 2 1 1.09 0 Apr-Aug 2018 Apr-Aug 2019 ENHANCING PASSENGER SERVICES NEW COACHES AND TRAINS 2nd Vande Bharat Express to start service shortly 95 trains have been upgraded to Utkrisht standard 29% increase in the production of coaches -

A Case Study of Konkan Railways

PROMOTING LOW CARBON TRANSPORT IN INDIA Impact Assessment and Management Framework for Infrastructure Assets: A Case Study of Konkan Railways Authors Amit Garg Indian Institute of Management Ahmedabad Prakriti Naswa Indian Institute of Management Ahmedabad P.R. Shukla Indian Institute of Management Ahmedabad August 2013 UNEP Risø Centre on Energy, Climate and Sustainable Development Technical University of Denmark This publication is part of the ‘Promoting Low Carbon Transport in India’ project ISBN: 978-87-92706-25-6 Design and production: Magnum Custom Publishing New Delhi, India [email protected] Photo acknowledgement: Front cover: Vinayaraj, 2012; Wikimedia commons Back cover: Prakriti Naswa Disclaimer: The findings, suggestions and conclusions presented in the case study are entirely those of the authors and should not be attributed in any manner to UNEP Risø Centre or the United Nations Environment Programme, nor to the institutions of individual authors. Preface Huge investments are being committed in new infrastructure projects in developing countries. Infrastructuresare long-life assets and are designed to withstand normal variability in climate regime. The Konkan Railway Corporation Limited (KRCL), a railway line operating for the past decade on the western coast of India, has met with two major accidents since its inception due to bad weather conditions. This case study presents the uncertainties and risks that such infrastructure assets face due to the changing climate, and suggests possible adaptation strategies. A framework for assessing the likely climate change impacts on long-life assets, using a methodology of reverse matrix for climate change impact analysis, is also suggested. The framework links climate change variables – temperature, rainfall, sea level rise, extreme events, and other secondary variables – and sustainable development variables – technology, institutions, economic, and other policies.