Analysys Mason Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Integrating Technology with Student-Centered Learning

integrating technology with student-centered learning A REPORT TO THE NELLIE MAE EDUCATION FOUNDATION Prepared by Babette Moeller & Tim Reitzes | July 2011 www.nmefdn.org 1 acknowledgements We thank the Nellie Mae Education Foundation (NMEF) for the grant that supported the preparation of this report. Special thanks to Eve Goldberg for her guidance and support, and to Beth Miller for comments on an earlier draft of this report. We thank Ilene Kantrov for her contributions to shaping and editing this report, and Loulou Bangura for her help with building and managing a wiki site, which contains many of the papers and other resources that we reviewed (the site can be accessed at: http://nmef.wikispaces.com). We are very grateful for the comments and suggestions from Daniel Light, Shelley Pasnik, and Bill Tally on earlier drafts of this report. And we thank our colleagues from EDC’s Learning and Teaching Division who shared their work, experiences, and insights at a meeting on technology and student-centered learning: Harouna Ba, Carissa Baquarian, Kristen Bjork, Amy Brodesky, June Foster, Vivian Gilfroy, Ilene Kantrov, Daniel Light, Brian Lord, Joyce Malyn-Smith, Sarita Pillai, Suzanne Reynolds-Alpert, Deirdra Searcy, Bob Spielvogel, Tony Streit, Bill Tally, and Barbara Treacy. Babette Moeller & Tim Reitzes (2011) Education Development Center, Inc. (EDC). Integrating Technology with Student-Centered Learning. Quincy, MA: Nellie Mae Education Foundation. ©2011 by The Nellie Mae Education Foundation. All rights reserved. The Nellie Mae Education Foundation 1250 Hancock Street, Suite 205N, Quincy, MA 02169 www.nmefdn.org 3 Not surprising, 43 percent of students feel unprepared to use technology as they look ahead to higher education or their work life. -

Beginners and Basics

Beginners & Basics S O C I A L M E D I A 1 0 1 Beginners W E L C O M E T O & Basics T W I T T E R 1 0 1 What is Twitter? Twitter is technically a “micro-blogging service,” allowing users to post and share comments, photos, videos and more. So what does that actually mean? Because it has a 240 character limit (recently bumped up from 140), it’s a place to share brief posts — not paragraphs. Twitter has some unique terminology when referring to specific features. It may be confusing to newbies, so we broke down the basics for you: Twitter Lingo Who Uses It? Tweet: to post With over 330 million monthly active users Retweet: to repost another user’s and 145 million daily active users, Twitter post has a huge influence. Many users are Reply: using the @ to respond to younger, but Twitter’s reach is not just someone’s post millennials and Gen-Z. Direct Message: private chat Hashtag: a symbol (the # sign) that 63% of Twitter users are between the ages categorizes tweets of 35 and 65. While other social media platforms like Snapchat and TikTok are Brands that are killing the Twitter game famous for catering to younger generations, it’s clear that Twitter appeals to a more mature audience as well. 17.7M 13.2M 11.2M 12M Why is it helpful? With such an impressive number of active users, Twitter is one of the best digital marketing tools for businesses. Twitter allows for brands and businesses to engage personally with their consumers. -

Effectiveness of Dismantling Strategies on Moderated Vs. Unmoderated

www.nature.com/scientificreports OPEN Efectiveness of dismantling strategies on moderated vs. unmoderated online social platforms Oriol Artime1*, Valeria d’Andrea1, Riccardo Gallotti1, Pier Luigi Sacco2,3,4 & Manlio De Domenico 1 Online social networks are the perfect test bed to better understand large-scale human behavior in interacting contexts. Although they are broadly used and studied, little is known about how their terms of service and posting rules afect the way users interact and information spreads. Acknowledging the relation between network connectivity and functionality, we compare the robustness of two diferent online social platforms, Twitter and Gab, with respect to banning, or dismantling, strategies based on the recursive censor of users characterized by social prominence (degree) or intensity of infammatory content (sentiment). We fnd that the moderated (Twitter) vs. unmoderated (Gab) character of the network is not a discriminating factor for intervention efectiveness. We fnd, however, that more complex strategies based upon the combination of topological and content features may be efective for network dismantling. Our results provide useful indications to design better strategies for countervailing the production and dissemination of anti- social content in online social platforms. Online social networks provide a rich laboratory for the analysis of large-scale social interaction and of their social efects1–4. Tey facilitate the inclusive engagement of new actors by removing most barriers to participate in content-sharing platforms characteristic of the pre-digital era5. For this reason, they can be regarded as a social arena for public debate and opinion formation, with potentially positive efects on individual and collective empowerment6. -

International Guide to Social Media China

International Guide to Social Media China Overview “China’s famous one-child policy More than one in five internet users are Chinese. The nation’s has resulted in youngsters looking for the companionship of others 500 million internet users are just behind Japan on time their own age online” spent online per day at an average of 2.7 hours. Internet connectivity is not expected to reach the majority of the one billion strong population until 2015. In this report: Although China blocks western social networks, domestic • China’s most popular Social Media sites • Video sites & Location-based apps social networking sites are immensely popular. Half of • Influencers in Chinese Social Media internet users are on more than one domestic social network • Chinese Language & Culture • Online Censorship and 30 per cent log on to at least one network every day. China blocks foreign social networking sites, and censors In this series: posts on domestic social networks, yet social networking remains hugely popular amongst young urbanites. • United States • Mexico • India China’s famous one child policy has resulted in youngsters • Brazil • Latin America looking for the companionship of others their own age online. • Scandinavia This combined with the general mistrust of government- • France • Germany controlled media has resulted in social networking becoming the quickest, cheapest and most trusted way to communicate Further reports due Q3 2012 over long distances. International Guide to Social Media China Social Networks China has a thriving social networking scene with dozens of popular networks. QZone is currently the most popular social networking site used in China. -

Mobile Wallet Guide

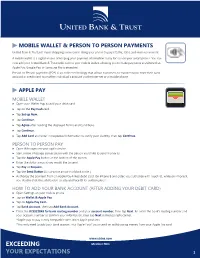

MOBILE WALLET & PERSON TO PERSON PAYMENTS United Bank & Trust just made shopping even easier! Using your phone to pay is faster, safer, and more convenient. A mobile wallet is a digital means of keeping your payment information ready for use on your smart-phone. You can now add your United Bank & Trust debit card to your mobile wallet, allowing you to make payments anywhere that Apple Pay, Google Pay, or Samsung Pay is accepted. Person-to-Person payments (P2P) is an online technology that allows customers to transfer funds from their bank account or credit card to another individual’s account via the Internet or a mobile phone. APPLE PAY MOBILE WALLET ▶ Open your Wallet App to add your debit card. ▶ Tap on the Pay Cash card. ▶ Tap Set up Now. ▶ Tap Continue. ▶ Tap Agree after reading the displayed Terms and Conditions. ▶ Tap Continue. ▶ Tap Add Card and enter in requested information to verify your identity, then tapContinue. PERSON TO PERSON PAY ▶ Open iMessages on your apple device. ▶ Start a new iMessage conversation with the person you’d like to send money to. ▶ Tap the Apple Pay button at the bottom of the screen. ▶ Enter the dollar amount you would like to send. ▶ Tap Pay or Request. ▶ Tap the Send Button (it is a white arrow in a black circle.) ▶ Authorize the payment from an Apple Pay-linked debit card. On iPhone 8 and older, you authorize with Touch ID, while on iPhone X, you double-click the side button to activate Face ID for authorization. HOW TO ADD YOUR BANK ACCOUNT (AFTER ADDING YOUR DEBIT CARD) ▶ Open Settings on your mobile phone. -

To the Pittsburgh Synagogue Shooting: the Evolution of Gab

Proceedings of the Thirteenth International AAAI Conference on Web and Social Media (ICWSM 2019) From “Welcome New Gabbers” to the Pittsburgh Synagogue Shooting: The Evolution of Gab Reid McIlroy-Young, Ashton Anderson Department of Computer Science, University of Toronto, Canada [email protected], [email protected] Abstract Finally, we conduct an analysis of the shooter’s pro- file and content. After many mass shootings and terror- Gab, an online social media platform with very little content ist attacks, analysts and commentators have often pointed moderation, has recently come to prominence as an alt-right community and a haven for hate speech. We document the out “warning signs”, and speculate that perhaps the attacks evolution of Gab since its inception until a Gab user car- could have been foreseen. The shooter’s anti-Semitic com- ried out the most deadly attack on the Jewish community in ments and references to the synagogue he later attacked are US history. We investigate Gab language use, study how top- an example of this. We compare the shooters’ Gab presence ics evolved over time, and find that the shooters’ posts were with the rest of the Gab user base, and find that while he was among the most consistently anti-Semitic on Gab, but that among the most consistently anti-Semitic users, there were hundreds of other users were even more extreme. still hundreds of active users who were even more extreme. Introduction Related Work The ecosystem of online social media platforms supports a broad diversity of opinions and forms of communication. In the past few years, this has included a steep rise of alt- Our work draws upon three main lines of research: inves- right rhetoric, incendiary content, and trolling behavior. -

Social Media Platforms

Social Media Platforms Tracking Your Traffic Nonprofit Institute At the College of Southern Maryland Professional Personal • Advocate o American Marketing • Motivated & Mission Oriented Association, Marketing Chair - Meet Sheebah Marketing Professional Charles County Chamber of • Over 10 Years of Experience Commerce, Sigma Gamma o Brand management, Rho Sorority, Inc., Zonta Club promotion, creative design, of Charles County (promoting forging digital strategies, justice and universal respect content creation, developing for human rights and strategic alliances, and public fundamental freedoms of relations. women.) • Nonprofit & For-Profit Organization • Education o National Urban League, o MBA, Masters Marketing NAACP, Human Society, Spring Management - UMUC/UMGC Dell Center o Bachelor’s Degree in o The Gott Company Communications & Electronic, (Convenience Stores, Gas Media Film - Towson Stations, Car Washes), eTrepid University. (Information Technology, Cloud o Hubspot Social Media Certified Computing and Cyber Security) o Just to name a few • The Fuzzy Stuff Bekozmarketing.com o One Cat o Loves to Travel and Eat Empowering Your Business to Compute with Clarity ✓ Cybersecurity ✓ Cloud Computing ✓ Artificial Intelligence and Machine Learning ✓ Unified Communications eTrepid.com We All Know A Little Teamwork Makes About A Lot! The Dream Work! 4 ▪ Sprout Social Resources - sproutsocial.com ▪ Social Media Examiner - socialmediaexaminer.com ▪ Hubspot - hubspot.com ▪ Buffer - buffer.com 5 Bekoz It Bekoz It Makes A Bekoz It Join Matters Difference -

Social Networking: a Guide to Strengthening Civil Society Through Social Media

Social Networking: A Guide to Strengthening Civil Society Through Social Media DISCLAIMER: The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government. Counterpart International would like to acknowledge and thank all who were involved in the creation of Social Networking: A Guide to Strengthening Civil Society through Social Media. This guide is a result of collaboration and input from a great team and group of advisors. Our deepest appreciation to Tina Yesayan, primary author of the guide; and Kulsoom Rizvi, who created a dynamic visual layout. Alex Sardar and Ray Short provided guidance and sound technical expertise, for which we’re grateful. The Civil Society and Media Team at the U.S. Agency for International Development (USAID) was the ideal partner in the process of co-creating this guide, which benefited immensely from that team’s insights and thoughtful contributions. The case studies in the annexes of this guide speak to the capacity and vision of the featured civil society organizations and their leaders, whose work and commitment is inspiring. This guide was produced with funding under the Global Civil Society Leader with Associates Award, a Cooperative Agreement funded by USAID for the implementation of civil society, media development and program design and learning activities around the world. Counterpart International’s mission is to partner with local organizations - formal and informal - to build inclusive, sustainable communities in which their people thrive. We hope this manual will be an essential tool for civil society organizations to more effectively and purposefully pursue their missions in service of their communities. -

How Access Your Debit Card Using Apple, Google Or Samsung Pay

How Access your Debit Card using Apple, Google or Samsung Pay Apple Pay Open “Wallet” which is pre-installed on your phone. Tap the + button at the top-right of the screen to add one. If you don't have Touch ID setup yet, you'll be walked through registering your fingerprints. Next, use the camera viewfinder to scan in your card. Just center it in the frame and Apple Pay will grab all of the details, or you can enter them manually. Like with the other payment options, you'll need to verify your card using a text message or email code sent to you from your bank. Enter that and you're all set. To use Apple Pay while your phone is locked, just double tap the home button. It'll bring up your favorite debit or credit card, or you can select others at the bottom of the screen. Hold your finger to Touch ID as you tap the phone on an Apple Pay-approved reader. Google Pay Download Google Pay from the Google Play App Store. Open the app and tap "Add Credit or Debit card." You can choose cards already associated with your Google Account or add a new one. Agree to the terms and conditions that pop up. Then verify your card via email (you'll receive a number to enter into the app) That's it! Now, the next time you see a card reader with the Google Pay logo, just open the app, choose your card, and tap to pay. Samsung Pay Open up Samsung Pay, which should be pre-installed on your Samsung smartphone. -

Samsung Galaxy Note 5 N920R6 User Manual

SMART PHONE User Manual Please read this manual before operating your device and keep it for future reference. Legal Notices Warning: This product contains chemicals known to Disclaimer of Warranties; the State of California to cause cancer, birth defects, or other reproductive harm. For more information, Exclusion of Liability please call 1-800-SAMSUNG (726-7864). EXCEPT AS SET FORTH IN THE EXPRESS WARRANTY CONTAINED ON THE WARRANTY PAGE ENCLOSED WITH THE PRODUCT, THE Intellectual Property PURCHASER TAKES THE PRODUCT “AS IS”, AND All Intellectual Property, as defined below, owned SAMSUNG MAKES NO EXPRESS OR IMPLIED by or which is otherwise the property of Samsung WARRANTY OF ANY KIND WHATSOEVER WITH or its respective suppliers relating to the SAMSUNG RESPECT TO THE PRODUCT, INCLUDING BUT Phone, including but not limited to, accessories, NOT LIMITED TO THE MERCHANTABILITY OF THE parts, or software relating there to (the “Phone PRODUCT OR ITS FITNESS FOR ANY PARTICULAR System”), is proprietary to Samsung and protected PURPOSE OR USE; THE DESIGN, CONDITION OR under federal laws, state laws, and international QUALITY OF THE PRODUCT; THE PERFORMANCE treaty provisions. Intellectual Property includes, OF THE PRODUCT; THE WORKMANSHIP OF THE but is not limited to, inventions (patentable or PRODUCT OR THE COMPONENTS CONTAINED unpatentable), patents, trade secrets, copyrights, THEREIN; OR COMPLIANCE OF THE PRODUCT software, computer programs, and related WITH THE REQUIREMENTS OF ANY LAW, RULE, documentation and other works of authorship. You SPECIFICATION OR CONTRACT PERTAINING may not infringe or otherwise violate the rights THERETO. NOTHING CONTAINED IN THE secured by the Intellectual Property. Moreover, INSTRUCTION MANUAL SHALL BE CONSTRUED you agree that you will not (and will not attempt TO CREATE AN EXPRESS OR IMPLIED WARRANTY to) modify, prepare derivative works of, reverse OF ANY KIND WHATSOEVER WITH RESPECT TO engineer, decompile, disassemble, or otherwise THE PRODUCT. -

Transcosmos Authorized As a Social Advertising Agency of “Tencent”, a Giant Internet Corporation in China

April 20, 2018 transcosmos inc. transcosmos authorized as a social advertising agency of “Tencent”, a giant internet corporation in China Offers clients ad delivery services on Tencent platforms such as “WeChat” and “QQ” Shanghai transcosmos Marketing Services Co., Ltd. (Headquarters: Shanghai, China; CEO: Eijiro Yamashita; transcosmos China), a wholly-owned subsidiary of transcosmos inc. (Headquarters: Tokyo, Japan; President and COO: Masataka Okuda) became an authorized social advertising agency of Tencent Holdings Ltd. (Tencent), a giant internet corporation in China in September, 2017. As an authorized Tencent advertising agency, transcosmos can offer ad delivery services to Chinese clients on all Tencent platforms, such as the instant messenger “QQ”, the mobile messaging app “WeChat”, Tencent portal website “QQ.com”, “Tencent Game”, and “Tencent Video”. The Chinese Internet business market is almost dominated by 3 companies, namely, Baido, Alibaba, and Tencent, which are collectively known as “BAT”. According to Tencent’s financial reports, the number of active users of “WeChat” and “QQ” has reached 1 billion and 783 million respectively, at the end of December, 2017. “Tencent Game” is also attracting numerous fans in China. In addition to offering speedy and low-cost Tencent ad delivery services, transcosmos will provide highly effective marketing services via Tencent tools based on the latest information on Tencent’s services and their ad strategy as an authorized Tencent agency. What’s more, transcosmos will offer sophisticated services to clients in order to help them boost sales and their brand value by strengthening the link with services that are offered in the Tencent ecosystem, whilst offering transcosmos’s existing services such as e-commerce support, digital marketing, real time sales promotion, customer services, and analytics services. -

Mastercard with Samsung

MASTERCARD® WITH SAMSUNG PAY ISSUER FAQ 1. What has been announced? 6. How do consumers set up their MasterCard to make Samsung announced the official launch of its mobile payment payments with Samsung Pay? service, Samsung Pay, initially on the Samsung Galaxy S6 and Consumers will create a Samsung account and add a fi ngerprint and Samsung S6 edge, S6 edge+ and Galaxy Note5. Samsung Pay will backup PIN to the device Settings. They can use the phone’s camera broaden the reach for mobile payments at the POS and enable to scan the card information and then the account is secured with MasterCard® cardholders to use compatible Samsung devices for a fingerprint and backup PIN. Cardholders can load eligible Credit, everyday purchases, at both contactless (NFC) and magnetic stripe Debit, Prepaid, and Small Business cards that have been enabled on POS terminals in the U.S. MDES by participating Issuers for Samsung Pay. 2. When will Samsung Pay be available for consumers? 7. How does Samsung Pay address safety? The service is slated to be available in the U.S. on September 28, Safety features include tokenization and cryptogram validation via 2015, with a limited invitation-only Beta program prior. Samsung Pay MDES and cardholder validation via fingerprint authentication or is compatible with select cards and Samsung devices; see backup PIN. Samsung does not store or share any payment information www.samsung.com/pay for details. 8. Where can consumers use Samsung Pay? 3. What is MasterCard’s relationship with Samsung? Consumers can use Samsung Pay at merchants accepting contactless MasterCard is working with Samsung to deliver a seamless and payments as well as mag-stripe only terminals commonly deployed secure mobile payment experience at both contactless-enabled POS in-stores where a plastic card can be swiped.