Advertising Restrictions and Competition in the Children's

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

USDA CHILD and ADULT CARE FOOD PROGRAM Umatilla Morrow

USDA CHILD AND ADULT CARE FOOD PROGRAM sponsored by: Umatilla Morrow Head Start, Inc. serving Umatilla, Morrow, Grant, Gilliam and Wheeler Counties GENERAL INFORMATION PACKET Background. Umatilla Morrow Head Start, Inc. (UMCHS) is the local sponsor of the U.S. Department of Agriculture (USDA) Child and Adult Care Food Program (CACFP). At the state level, Oregon Department of Education (ODE) is the administrative agency in charge of monitoring and dispersing funds to Child and Adult Care Food Program sponsors. The primary goal of the Child and Adult Care Food Program is to improve the health and diet of children in a child care setting by (a) assuring that well-balanced nutritious meals are served to children (b) helping children learn to eat a wide variety of food as part of a balanced diet, and (c) helping children develop good eating habits that will last throughout their lives. This federally funded program reimburses child care providers for part of the cost of foods they serve to children in registered family child care homes, certified family homes or DHS Listed homes. CACFP ELIGIBILITY REQUIREMENT CHILD CARE PROVIDER C First, a child care provider must have a current registration/license from Child Care Division (CCD), State Employment Office, or be Listed with Department of Human Services Self Sufficiency Program to be eligible to participate in the USDA/CACFP. As registration/license is renewed a copy must be sent to the USDA C Second, a provider must sign up with the local sponsor of the USDA Child and Adult Care Food Program. A representative from the sponsoring organization will visit your home. -

Kellogg's Annual Report 2008

KELLOGG COMPANY TWO THOUSAND AND EIGHT ANNUAL REPORT WHAT MAKES ® ™ At Kellogg Company, we have: • For more than a century, Kellogg Company has been dedicated to producing great-tasting, high-quality, nutritious foods that consumers around the world know and love. With 2008 sales of nearly $13 billion, Kellogg Company is the world’s leading producer of cereal, as well as a leading producer of convenience foods, including cookies, crackers, toaster pastries, cereal bars, frozen waffles and vegetarian foods. We market more than 1,500 products in over 180 countries, and our brands include such trusted names as Kellogg’s, Keebler, Pop-Tarts, Eggo, Cheez-It, Nutri-Grain, Rice Krispies, Morningstar Farms, Famous Amos, Special K, All-Bran, Frosted Mini-Wheats, Club, Kashi, Bear Naked, Just Right, Vector, Guardian, Optivita, Choco Trésor, Frosties, Sucrilhos, Vive, Muslix and Zucaritas. Kellogg products are manufactured in 19 countries around the world. We enter 2009 with a rich heritage of success and a steadfast commit- ment to continuing to deliver sustainable and dependable growth in the future. TWO 2008 ANNUAL REPORT A commitment ™ to sustainable and dependable GROWTH ™ 2008 FINANciaL HigHLigHTS / DELIVERING STRONG RESULTS (dollars in millions, except per share data) 2008 Change 2007 Change 2006 Change Net sales $ 12,822 9% $ 11,776 8% $ 10,907 7% Gross profit as a % of net sales 41.9 % (2.1 pts) 44.0 % (0.2 pts) 44.2 % (0.7 pts) Operating profit 1,953 5% 1,868 6% 1,766 1% Net earnings 1,148 4% 1,103 10% 1,004 2% Net earnings per share Basic 3.01 8% 2.79 10% 2.53 6% Diluted 2.99 8% 2.76 10% 2.51 6%(b) Cash flow (net cash provided by operating activities, reduced by capital expenditure)(a) 806 (22%) 1,031 8% 957 24% Dividends per share $ 1.30 8% $ 1.20 5% $ 1.14 8% (a) Cash flow is defined as net cash provided by operating activities, reduced by capital expenditures. -

Cereal List Arranged Numerically Generic Default=***** Note: ### Following Codenumber Signifies That Cereal Was Not Updated in 2001, Please Choose Another Code

Cereal List arranged numerically generic default=***** Note: ### following codenumber signifies that cereal was not updated in 2001, please choose another code COMPLETE CEREAL LIST 000 ***None 000 ***Rarely 000 ***Seldom 001 All Bran (Kellogg's) 001 Kellogg's All Bran 002 ### Alpen 003 ### Alpha-Bits (Post) 003 ### Post Alpha-Bits 004 ### Apple Jacks (Kellogg's) 004 ### Kellogg's Apple Jacks 005 All Bran Bran Buds (Kellogg's) 005 Bran Buds 005 Kellogg's All Bran Bran Buds 006 Bran 006 Bran Cereal 007 100% Bran Cereal (Nabisco/Post) 007 Post 100% Bran Cereal 009 Bran Flakes 009 Complete Wheat Bran Flakes (Kellogg's)*** 009 Fiber, High 009 High Fiber 009 Kellogg's Complete Wheat Bran Flakes 011 Cap'n Crunch (Quaker) 011 Quaker Cap'n Crunch 012 ### Cap'n Crunch Crunchberries (Quaker) 012 ### Crunch Berries 012 ### Quaker Cap'n Crunch Crunchberries 013 ### Cap'n Crunch Peanut Butter (Quaker) 013 ### Quaker Cap'n Crunch Peanut Butter 014 Cheerios (General Mills) 014 General Mills Cheerios 014 Toasted Oats 015 Cocoa Krispies (Kellogg's) 015 Kellogg's Cocoa Krispies 015 Krispies, Cocoa 016 ### Cocoa Pebbles (Post) 016 ### Pebbles, Cocoa 016 ### Post Cocoa Pebbles 017 Cocoa Puffs (General Mills) 017 General Mills Cocoa Puffs 017 Puffs, Cocoa 019 Chex, Corn (General Mills) 019 Corn Chex (Ralston Purina/General Mills) 019 General Mills Corn Chex 020 Corn Flakes (Kellogg's)*** 020 Kellogg's Corn Flakes 022 Corn Total (General Mills) 022 General Mills Total Corn Flakes 022 Total Corn Flakes (General Mills) 023 ### Corn Flakes, Country (General Mills) -

Kellogg Company (Exact Name of Registrant As Specified in Its Charter)

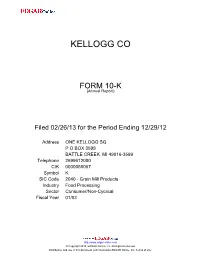

KELLOGG CO FORM 10-K (Annual Report) Filed 02/26/13 for the Period Ending 12/29/12 Address ONE KELLOGG SQ P O BOX 3599 BATTLE CREEK, MI 49016-3599 Telephone 2699612000 CIK 0000055067 Symbol K SIC Code 2040 - Grain Mill Products Industry Food Processing Sector Consumer/Non-Cyclical Fiscal Year 01/03 http://www.edgar-online.com © Copyright 2013, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended December 29, 2012 TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For The Transition Period From To Commission file number 1-4171 Kellogg Company (Exact name of registrant as specified in its charter) Delaware 38 -0710690 (State or other jurisdiction of Incorporation (I.R.S. Employer Identification No.) or organization) One Kellogg Square Battle Creek, Michigan 49016-3599 (Address of Principal Executive Offices) Registrant’s telephone number: (269) 961-2000 Securities registered pursuant to Section 12(b) of the Securities Act: Title of each class: Name of each exchange on which registered: Common Stock, $.25 par value per share New York Stock Exchange Securities registered pursuant to Section 12(g) of the Securities Act: None Indicate by a check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Low Fibre Food Choices May Be Helpful for Loose, Frequent Bowel Movements Low Fibre Food Choices

Low Fibre Food Choices May be helpful for loose, frequent bowel movements Low Fibre Food Choices Eating less fibre may help reduce symptoms such as abdominal cramping, bloat- ing, frequent, loose bowel movements or diarrhea Low Fibre Guidelines • Eat small, frequent meals and snacks. Try to eat every 2-3 hours. • Include at least at least 1½ –2 litres (6-8 cups) of a variety of fluids per day (eg: water, juice, sports drinks, soup, and herbal tea). Limit caffeine or alcohol containing drinks. • Chicken, fish, beef, pork, eggs, and dairy products do not have fibre so you can eat these foods as desired. • Avoid deep fried, spicy, greasy, and very rich foods. • Plant foods have fibre and need to be restricted. Remove skin and seeds from foods to reduce the fibre content. • Cooking, chopping, canning, and blenderizing foods will not reduce their fibre content. • A multivitamin with minerals may be needed if you are unable to eat a variety of foods. Any “one a day” brand sold in drugstores is appropriate. • Use the charts on the following pages to help choose meals and snacks. - Eat foods from the Low Fiber column as you wish. - Discuss the use of Medium Fiber foods with your dietitian. - LIMIT foods from the High Fibre column. Low Fibre Food Choices 1 Dietary Fibre Content of Common Foods LIMIT YOU MAY EAT High Fibre Medium Fibre Low Fibre Hot Cereals Red River® Cream of Wheat® Sunny Boy® Oatmeal: 1/2 cup, cooked or 1 pouch, instant Cold Cereals All Bran® Life® Any cereal with less Bran Buds® Mini Wheats® than 2 grams of fibre Bran Flakes® -

2 These Trademarks Include Kellogg's for Cereals, Convenience Foods And

These trademarks include Kellogg’s for cereals, convenience foods and our other products, and the brand names of certain ready-to-eat cereals, including All-Bran, Apple Jacks, Bran Buds, Choco Zucaritas, Cocoa Krispies, Complete, Kellogg’s Corn Flakes, Corn Pops, Cracklin’ Oat Bran, Crispix, Crunchmania, Crunchy Nut, Eggo, Kellogg’s FiberPlus, Froot Loops, Kellogg’s Frosted Flakes, Krave, Frosted Krispies, Frosted Mini- Wheats, Just Right, Kellogg’s Low Fat Granola, Mueslix, Pops, Product 19, Kellogg’s Origins, Kellogg's Raisin Bran, Raisin Bran Crunch, Rice Krispies, Rice Krispies Treats, Smacks/Honey Smacks, Smart Start, Special K, Special K Nourish, Special K Red Berries and Zucaritas in the United States and elsewhere; Sucrilhos, Krunchy Granola, Kellogg's Extra, Kellness, Musli, and Choco Krispis for cereals in Latin America; Vector in Canada; Coco Pops, Chocos, Frosties, Fruit‘N Fibre, Kellogg’s Crunchy Nut Corn Flakes, Krave, Honey Loops, Kellogg’s Extra, Country Store, Ricicles, Smacks, Start, Pops, Honey Bsss, Croco Copters and Tresor for cereals in Europe; and Guardian, Sultana Bran, Frosties, Rice Bubbles, Nutri-Grain, Kellogg’s Iron Man Food, and Sustain for cereals in Asia and Australia. Additional trademarks are the names of certain combinations of ready-to-eat Kellogg’s cereals, including Fun Pak and Variety. Other brand names include Kellogg’s Corn Flake Crumbs; All-Bran, Choco Krispis, Froot Loops, Special K, Zucaritas and Sucrilhos for cereal bars, Pop-Tarts for toaster pastries; Eggo and Nutri-Grain for frozen waffles -

Fortification Examined

Fortification examined How added nutrients can undermine good nutrition A survey of 260 food products with added vitamins and minerals by Gillie Bonner, SRD, Hugh Warwick, Martin Barnardo and Tim Lobstein © The Food Commission (UK) Ltd 94 White Lion Street London N1 9PF October 1999 £125 Contents 1 EXECUTIVE SUMMARY........................................................................................................................3 2 BACKGROUND ..........................................................................................................................................5 2.1 TERMINOLOGY ...........................................................................................................................................5 2.2 PRINCIPLES.................................................................................................................................................5 2.3 TECHNICAL NOTES.....................................................................................................................................7 2.4 HISTORY OF FORTIFICATION....................................................................................................................8 2.5 UK SITUATION...........................................................................................................................................9 2.6 LEGISLATION IN OTHER COUNTRIES......................................................................................................11 2.6.1 The Australian Experience....................................................................................................... -

How Much Sugar Is in Your Cereal ?

How much sugar is in your cereal ? If Your Total Limit Your Daily Daily Diet Has : Added Sugar To: Added sugars are put into foods during processing or preparation. Added sugars 1600 calories 24 grams provide calories but no vitamins and minerals, very little nutritional value. Avoid 2200 calories 48 grams getting too many calories, and reduce the chances for tooth decay, by limiting the 2800 calories 72 grams amount of added sugar in your diet. Note: 4 grams of sugar = 1 teaspoon Foods containing sugars and starches can cause tooth decay. Daily dental care including brushing with fluoride toothpaste and flossing will help prevent tooth decay. Cereal Brand Name Grams of Sugar Cereal Brand Name Grams of Sugar General Mills Apple Cinnamon Cheerios 13 * Kellogg’s Mini Wheats Frosted Bite Size 11 General Mills Basic 4 14 Kellogg’s Mini Wheats Frosted Original 10 General Mills Brown Sugar & Oat Total 9 Kellogg’s Mueslix with Raisins, Dates & Almonds 17 * General Mills Cheerios 1 Kellogg’s Pokemon 14 General Mills Cheerios - Frosted 13 Kellogg’s Product 19 4 General Mills Cheerios - Honey Nut 11 Kellogg’s Raisin Bran 18 * General Mills Cheerios - Multi Grain 6 Kellogg’s Raisin Bran Crunch 20 General Mills Cinnamon Toast Crunch 10 Kellogg’s Rice Krispies 3 General Mills Cocoa Puffs 14 Kellogg’s Rice Krispies Treats 9 General Mills Cookie Crisp 13 Kellogg’s Smacks 15 General Mills Corn Chex 3 Kellogg’s Smart Start 15 General Mills Corn Flakes Total 4 Kellogg’s Special K 4 General Mills Fiber One Bran Cereal 0 Kellogg’s Special K with Berries -

Glycemic Index of Popular Foods

ENDOCRINOLOGY & DIABETES UNIT Diabetes Clinic: 604-875-2868 Toll-free Phone: 1-888-300-3088, x2868 Fax: 604-875-3231 http://endodiab.bcchildrens.ca THE GLYCEMIC INDEX OF POPULAR FOODS Expressed as a percentage of the value for glucose, GI = 100 LOW GLYCEMIC INDEX MEDIUM GLYCEMIC INDEX HIGH GLYCEMIC INDEX (55 or less) (56 to 69) (70 or above) Choose most often Choose more often Choose least often BAKERY PRODUCTS Apple muffin Angel food cake Donut, cake type Banana cake Blueberry muffin Waffles Pound cake Bran muffin Sponge cake, plain Carrot muffin Croissant Crumpet Flan cake Pastry BEVERAGES Apple juice, unsweetened Coca cola Gatorade Carrot juice Cranberry juice cocktail Nestlé Quik chocolate powder, Nestlé Quik strawberry dissolved in 1% milk powder, dissolved in water Orange juice Grapefruit juice, unsweetened Pineapple juice, unsweetened BREADS 50% oat bran bread 100% barley flour bread Bagel, white 100% whole-grain bread Hamburger bun Baguette, white, plain Fruit and spice loaf Pita bread, white Kaiser roll Whole-grain pumpernickel Sourdough rye bread Melba toast Bulgur, or cracked wheat Baguette, with butter and Wonder bread, white, kernel bread strawberry jam enriched Wheat-flour flatbread Gluten-free multi-grain bread White bread Gluten-free white bread Whole-meal rye bread White flatbread Adapted from: Atkinson FS, Foster-Powell K, Brand-Miller JC. International tables of glycemic index and glycemic load values: 2008. Diabetes Care 2008;31(12):2281–2283. Available online at http://care.diabetesjournals.org/content/suppl/2008/09/18/dc08-1239.DC1/TableA1_1.pdf -

Sustainable Dependable Performance 200720072007 ANNUALANNUALANNUAL REPORTREPORTREPORT TMTMTM

® KELLOGG COMPANY 2007 ANNUAL REPORT Sustainable ® Dependable Performance TM KELLOGG COMPANY • ONE KELLOGG SQUARE • BATTLE CREEK, MICHIGAN 49016 • TEL (269) 961-2000 • www.kelloggcompany.com 2007 ANNUAL REPORT TM Kellogg Company 2007 Annual Report Net Sales (million $) Total Shareowner Return Sustainable 11,776 20% 19% Dependable 18% 10,907 15% 16% 10,177 Performance 9,614 7% 5% 8,811 3% Vision To be the food company of choice. -1% Kellogg Mission To drive sustainable growth through the power of our people and brands S&P Packaged Foods Index -8% 03 04 05 06 07 03 04 05 06 07 by better serving the needs of our consumers, customers and communities. Net sales increased again For the seventh consecutive year, in 2007, the seventh Kellogg Company’s total return to With 2007 sales of nearly $12 billion, Kellogg Company is the world’s leading producer of cereal consecutive year of growth. shareowners exceeded that of the and a leading producer of convenience foods, including cookies, crackers, toaster pastries, cereal S&P Packaged Food Index. bars, fruit-flavored snacks, frozen waffles, and veggie foods. The Company’s brands include Kellogg’s®, Keebler ®, Pop-Tarts®, Eggo®, Cheez-It ®, Nutri-Grain®, Rice Krispies ®, Morningstar Farms ®, Famous Amos ®, Special K ®, Stretch Island ®, All-Bran ®, Frosted Mini-Wheats®, Club ® and Kashi ®. Kellogg products Cash Flow (a) (million $) Dividends ($ per share) Net Earnings Per Share ($) (diluted) Operating Profit (million $) are manufactured in 18 countries and marketed in more than 180 countries around the world. 1,868 1,031 1.20 2.76 1,750 1,766 Table of Contents 1.14 1,681 950 957 2.51 924 1.06 Letter to Shareowners 2 2.36 1.01 1.01 1,544 Global Operations 8 2.14 769 1.92 Sustainable Dependable Global Brands 14 Our Nutrition Heritage 15 03 04 05 06 07 03 04 05 06 07 03 04 05 06 07 03 04 05 06 07 Our People 16 Dividends per share have Earnings per share of $2.76 Operating profit increased Including over $60 million of Environmental Sustainability 18 increased 19% over the past were 10% higher than 2006. -

The Whole Truth on Whole Grains

The whole truth on whole grains If you’ve jumped on the “low carb” band wagon, you’re likely avoiding whole grains, a food that is power-packed with vitamins, minerals, antioxidants and phytochemicals— plant compounds that help alter risk factors for chronic diseases such as heart disease, diabetes and cancer. Hopefully after learning more, you’ll reconsider eliminating that bowl of bran flakes! What makes a whole grain whole? Grains are made up of three parts: bran, germ and endosperm. The bran is the outer shell that provides a rich source of fiber, trace minerals, phytochemicals and B vitamins. The germ nourishes the grain and is packed with antioxidants, the B vitamins and vitamin E. It is also a source of heart healthy unsaturated fats. Finally, the endosperm is the largest portion of the grain and contains complex carbohydrates and protein to provide energy. While each part contributes important nutrients, the “whole” grain offers the most nutritional benefits. Refined grains When grains are refined to make white flour, the germ and bran portions are removed, leaving only the endosperm. As you’ve probably guessed, this process also removes the most nutrient-dense portions of the grain. Refined products are often “enriched,” meaning that key nutrients, such as the B vitamins, are added back. However, whole grain products, such as whole grain breads and pastas and brown rice, contain the germ, bran and endosperm, and all of the nutrients that go along with them. Fiber-rich whole grains Although refined grains are enriched, they are often lacking in fiber. Whole grains, on the other hand, offer two types: soluble and insoluble. -

Kellogg Company Annual Report 2009

Kellogg Company 2009 annual report The strength of ® Kellogg Company one Kellogg Square Battle Creek, Michigan 49017 phone: 269.961.2000 For more information on our business, please visit www.kelloggcompany.com. Sandy Alexander Inc., an ISO 14001:2004 certified printer with Forest Stewardship Council (FSC) Chain of Custody, printed this report with the use of renewable wind power resulting in nearly zero volatile organic compound (VOC) emissions and on recycled paper that contains 10% post-consumer (PCW) fiber for the text and cover and 30% post-consumer (PCW) for the financials. Table of ConTenTs ™ the 4 Financial Highlights 6 Letter to Shareowners strength of 11 Leadership Financials/Form 10-K Brands and Trademarks 1 Selected Financial Data 12 Management’s Discussion & Analysis 13 ™ Financial Statements 27 Notes to Financial Statements 31 Shareowner Information Sustainableand DePendable ™ PerfoRmAnCe™ FoR moRe thAn A CentuRy, Kellogg Company has been dedicated to producing great-tasting, high-quality, nutritious foods that consumers around the world know and love. With 2009 sales of nearly $13 billion, Kellogg Company is the world’s leading producer of cereal, as well as a leading producer of convenience foods, including cookies, crackers, toaster pastries, cereal bars, frozen waffles and vegetarian foods. We market more than 1,500 products in over 180 countries, and our brands include such trusted names as Kellogg’s, Keebler, Special K, Pop-Tarts, Eggo, Cheez-It, Nutri-Grain, Rice Krispies, Mother’s, Morningstar Farms, Murray Sugar Free, Townhouse, All-Bran, Frosted Mini-Wheats, Club, Kashi, Bear Naked, Just Right, Guardian, Optivita, Chocos, Trésor, Frosties, Sucrilhos, Vector, Muslix and Zucaritas.