Investor Newsletter November 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

HINO RANGER Year: 1983 -1996 HINO RANGER LOHAN Year: 2004

HINO RANGER Year: 1983 -1996 No. OEM Part No. Part Name Model Name Remarks L/T MB SB CER DEF 1 794114580L Front Windshield 3FF17S-6FWZTT0 FZ T - - N - 2 - Front Windshield 2HR17S-6RWSTT0 FR T - - N - 3 794611-070L Front Vent. Left/Right 3FF17S-4FVBTT0 - T - - N - 4 79451-1160L Front Door Left/Right 3FF17S-4FDBTT0 - T - - N - 5 79441-1060L Side Window Left/Right 3FF17S-4SWBTT0 - T - - N - 6 794311-060L Backlite 3FF17S-4RWSTT0 - T - - N N HINO RANGER LOHAN Year: 2004 -Now No. OEM Part No. Part Name Model Name Remarks L/T MB SB CER DEF 1 - Front Windshield 3Y078M-CFHNTT0 - L N N N - 2 - Front Windshield 2HR78S-6RWSTT0 FR T - - N - 3 - Front Door Left 3Y078M-AFDLTT1 - T - - N - 4 - Front Door Right 3Y078M-AFDRTT1 - T - - N - TOYOTA NEW DYNA / HINO DUTRO Year: 2004 -Now No. OEM Part No. Part Name Model Name Remarks L/T MB SB CER DEF 1 56111-0W570 Front Windshield 3TR041-5FHNTT1 Non Logo L N N N - 2 - Front Windshield 2TR04S-6RWSTT0 FR T - - N - 3 68102-0W020 Front Door Left 3TR04M-AFDLTA1 Non Logo T - - N - 4 68101-0W020 Front Door Right 3TR04M-AFDRTA1 Non Logo T - - N - 5 64811-0W300 Backlite 3TR04M-ARWSTT0 Non Logo T - - N N SUZUKI CARRY Year: 1984 - Now No. OEM Part No. Part Name Model Name Remarks L/T MB SB CER DEF 1 79611-77310-L000 Front Windshield 3SCR3M-5FWZTT0 FZ T - - N - 2 - Front Windshield 2SL41S-5RWSTT0 FR T - - N - 3 79636 -79111-L000 Front Door Left 3SCR3M-AFDLTT0 - T - - N - 4 79631 -79111-L000 Front Door Right 3SCR3M-AFDRTT0 - T - - N - 5 79671-79112-L000 Backlite 3SCR3M-ARWSTT0 - T - - N N SUZUKI KATANA Year: 1984 - Now No. -

Katalog Service Manual

KATALOG SERVICE MANUAL www.manualbookmobil.com Pemesanan: Telp/SMS: 0856 2509 556 email: [email protected] Service Manual Mobil Audi Audi A4 (1997-2000) Audi A4 (2002-2008) Wiring Diagram Audi A6 1995 Wiring Diagram Audi A6 2000 Wiring Diagram Audi S8 2001 BMW BMW Technical Information System BMW Elektrical Troubleshooting Manual BMW Diagnostic Trouble Codes BMW OBD-II Trouble Code BMW E30 M3 BMW 3 Series (E36) BMW 3 & 5 Series (83-91) BMW 3 Series (E46) BMW 5 Series E34 (1989-1995) BMW 5 Series E39 (1997-2002) BMW 7 Series (E32) BMW E32 BMW 8 Series (E31) 1994 BMW E30 Chevrolet Chevrolet Aveo (2002-2006) Chevrolet Blazer 4.3L (1997) Chevrolet Captiva (2008-2010) Daihatsu Daihatsu Charade & Classy (1987-1994) Daihatsu Espass 1600cc Daihatsu Feroza Daihatsu Grand Max-Diagnostik Daihatsu Sirion Daihatsu Taft F50 Daihatsu Taft, Hiline & Rocky F70, F75, F77 Daihatsu Taruna EFI-Pemeriksaan Sistem EFI Daihatsu Terios-Mesin Daihatsu Zebra EFI-Mesin Wiring Diagram Daihatsu Xenia VVTi Daewoo Daewoo Matiz (2003) Daewoo Musso (1991-2000) Daewoo Espero Dogde Dodge Neon Ferrari Ferrari 308 QV & 328 GTB/GTS Ferrari 365 GT4 (1973) Fiat Fiat Uno 45,55,60,70 Fiat Bravo/Brava Ford Ford Service Database 2007-2008 Ford Escape 2000-2007 Ford Laser - Engine (1989-1992) Parts Catalog Ford Ranger Pickup XLT 2007 Ford Ranger 1999 Ford Ranger 2001-2005 Ford Ranger 2006-2009 Ford Ranger 2010-2013 Honda Honda Accord 1986-1988 Honda Accord 1991-1993 (Maestro) Honda Accord 1994-1997 Honda Accord 1998-2002 Honda Accord 2003-2006 Honda Accord 2008-2010 Honda Civic -

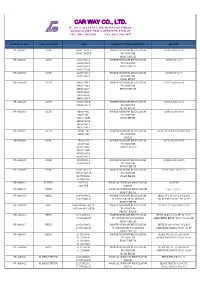

Carway Product List for Window Regulator

CAR WAY CO., LTD. 1F., NO. 8, ALLEY 10, LANE 20, WAN AN STREET, BANQIAO DIST., NEW TAIPEI CITY, TAIWAN TEL: 886-2-2963-6702 FAX: 886-2-2963-1897 CAR WAY NO. APPLICATION OE# PRODUCT DESCRIPTION MODEL CW-AB0001 AUDI 8D0837461B L POWER WINDOW REGULATOR AUDI A4/S4 96-02 8D0837462B R W/O MOTOR FRONT RH/LH CW-AB0002 AUDI 4A0837461A POWER WINDOW REGULATOR AUDI 100 92-97 4A0837462A W/O MOTOR 4A0837461B FRONT RH/LH 4A0837462B CW-AB0003 AUDI 4A0839461A POWER WINDOW REGULATOR AUDI 100 92-97 4A0839462A W/O MOTOR REAR RH/LH CW-AB0004 AUDI 4B0837461A POWER WINDOW REGULATOR AUDI A6/S6 98-05 4B0837462A W/O MOTOR 4B0837461C FRONT RH/LH 4B0837462C 4B0959802E 4B0959801E CW-AB0005 AUDI 8D0839462 R POWER WINDOW REGULATOR AUDI A4/S4 96-02 8D0839461 L W/O MOTOR REAR RH/LH CW-AB0006 AUDI 4B0839462 POWER WINDOW REGULATOR AUDI A6/S6 98-05 4B0839461 W/O MOTOR 4B0839462B REAR RH/LH 4B0839461B 4B0839462A 4B0839461A CW-AB0007 AUDI 4N0837462 POWER WINDOW REGULATOR AUDI TT COUPE/ROADSTER 4N0837461 W/O MOTOR RH/LH CW-AB0008 AUDI 4F0837461 POWER WINDOW REGULATOR AUDI A6/S6 '05-07 4F0837462 W/O MOTOR 4F0837461D FRONT RH/LH 4F0837462D 4F0837461A 4F0837462A CW-AB0009 AUDI 4F0839461 L POWER WINDOW REGULATOR AUDI A6/S6 2005/6 4F0839462 R W/O MOTOR FRONT RH/LH CW-AB0010 AUDI 8E0837461C L POWER WINDOW REGULATOR AUDI A4 05-ON 01-05 8E0837462C R W/O MOTOR 8E1959802G REAR RH/LH 8E1959801G CW-AB0011 AUSTIN 907179 L MANUAL WINDOW REGULATOR AUSTIN 907180 R RH/LH CW-AB0013 FORD MANUAL WINDOW REGULATOR FORD 卡多98'- FRONT RH/LH CW-AB0014 BENZ 1247200346 L POWER WINDOW REGULATOR BENZ W-124 -

CHAPTER 1 INTRODUCTION 1.1 Object Overview the Car Industry In

CHAPTER 1 INTRODUCTION 1.1 Object Overview The car industry in Indonesia has been expanding very fast. Every car manufacturer in Indonesia are launching their newest model or some additional updates on their current model annually, this situation is a linear condition due to the high demand of new car, the competition of every car manufacturer has been very tight making every competitor must give their best effort on competing on each segment. The numbers of sales on private vehicle especially cars are increasing massively linear to the demand on Indonesian market on purchasing new car. The increasing economic background and the change of social economy supports this factor. There is an increasing amount of car in Indonesia significantly from 2013-2016; it will be shown in the table 1.1 below, Table 1.1 Total amount of car in Indonesia from 2013-2016 Year Total Amount 2013 11.484.514 2014 12.599.038 2015 13.480.973 2016 14.580.666 Source: Badan Pusat Statisik (2016) Private car is one of the very developing transportation choices in Indonesia, many car manufacturers cause the increase of car amounts on the roads every year. Some manufacturers that exist here came from Japan, Korea, China, German, France, Italy, Sweden, Great Britain, America, India, and Malaysia. The increasing amount of new cars is also caused by the existence of LCGC (low cost green car). In 2013 the government made a new order on state regulation number 41/2013 (PP No.41/2013) about the items that is tax chargeable as luxury goods, the state’s regulation states that car with low energy consumption and reasonable price, the sales tax of luxury goods charged as 0 percent of the selling price. -

Pengaruh Kebijakan Low Cost Green Car Terhadap Strategi Nissan

Pengaruh Kebijakan Low Cost Green Car Terhadap Strategi Nissan Motor Corporation Menguasai Pasar Otomotif di Indonesia Oleh: SAMUEL BERLIANDO HASIHOLAN PURBA ([email protected]) Pembimbing: Yurnarida Eka Nizmi, S.IP. M.Si Bibliografi: 4 Jurnal, 6 Buku, 1Skripsi, 30 Situs Internet Jurusan Ilmu Hubungan Internasional ± Prodi Hubungan Internasional Fakultas Ilmu Sosial dan Ilmu politik Universitas Riau Kampus Bina Widya Jl. H.R. Soebrantas Km. 12,5 Simp. Baru Pekanbaru 28294 Telp/Fax. 0761-63277 Abstract This research discusses the influence of Low Cost Green Car policy to strategy Nissan Motors Corporation dominate the automotive market in Indonesia. In 2013 Indonesia by Minister of Industry issued Low Cost Green Car policy. To face the enthusiasts of Low Cost Green Car that much, Nissan issued old products are very popular in Indonesia called Datsun. Perspective that used in this research is Neoliberalism perspective. The theory used in this research is the competitive theory by Michael Porter's. According to this theory, competitive advantage is the advantage by delivering greater value to customers, the price is cheaper and give more advantages from its competitors. The influence of Low Cost Green Car policy to the strategy of Nissan Motor Corporation in dominate the automotive market in Indonesia is Nissan follow low cost green car policy with its subsidiary company registered Datsun successfully. This is proven from the beginning of the presence of the first model of Datsun like Datsun Go+ Panca which began in May. Datsun sales continue to increase each month until November. The success of the Nissan strategy was proven with the launch of a second product that LCGC manifold Datsun Go Panca Hatchback. -

Di Indonesia, Mobil Murah Ramah Lingkungan Alias Low Cost

BAB I PENDAHULUAN 1.1 LATAR BELAKANG MASALAH Di Indonesia, mobil murah ramah lingkungan alias Low Cost Green Car (LCGC) semakin banyak peminatnya di Tanah Air. Perbedaan pada mobil laiinya yaitu harganya murah, irtit bahan bakar, serta ada sejumlah model yang menawarkan kapasitas tujuh penumpang. Sejak diluncurkan pada pertengahan 2013, Low Cost Green Car (LCGC) makin diminati. Meski penjualannya sempat turun pada 2015 menjadi 165.434 unit, namun secara persentase pangsa pasar mobil murah ini meningkat. Pangsa pasar mobil LCGC pada 2015 meningkat menjadi 16,3 persen dibanding posisi 2014 sebesar 14,2 persen dari total penjualan mobil domestik. Kehadiran mobil murah mulai menggerus pangsa pasar kendaraan multi purpose vehicle (MPV) kelas bawah. Selain itu LCGC juga menjadi alternatif bagi pengguna motor yang ingin beralih menggunakan kendaraan roda empat. Imbasnya, penjualan motor turun sejak hadirnya mobil murah ini. Harga yang terjangkau, irit bahan bakar serta ramah lingkungan menjadi alasan masyarakat memilih mobil LCGC. Selain itu, naiknya jumlah penduduk kelas menengah Indonesia yang berimbas meningkatnya daya beli masyarakat turut mendorong pesatnya penjualan mobil murah.1 Gambar I.1 Penjualan Mobil Murah (LCGC) 2013-Juni 2016 Sumber: databoks.katadata.co.id Eksistensi mobil LCGC yang kian diminati oleh masyarakat Indonesia berdampak besar terhadap arah penjualan mobil di dalam negeri. Trend terbaru menunjukkan sebagian besar masyarakat lebih memilih mobil LCGC yang tentunya lebih terjangkau dan hemat bahan bakar. Munculnya berbagai macam mobil LCGC membuat masyarakat harus dapat memilih mobil LCGC yang terbaik di kelasnya. 1 (http://databoks.katadata.co.id/datapublish/2016/08/10/mobil-murah-makin-diminati) Berdasarkan data yang didapat Gabungan Industri Kendaraan Bermotor Indonesia (Gaikindo), Calya kini menjadi mobil terlaris pertama di Indonesia. -

Pengaruh Brand Association Terhadap Consumer Response Pada Mobil Merek Toyota Agya Dan Toyota Calya Di Bandung

Universitas Katolik Parahyangan Fakultas Ilmu Sosial dan Ilmu Politik Program Studi Ilmu Administrasi Bisnis Terakreditasi A SK BAN –PT NO: 468/SK/BAN-PT/Akred/S/XII/2014 Pengaruh Brand Association terhadap Consumer Response pada Mobil Merek Toyota Agya dan Toyota Calya di Bandung Skripsi Oleh Felicia 2013320092 Bandung 2017 Universitas Katolik Parahyangan Fakultas Ilmu Sosial dan Ilmu Politik Program Studi Ilmu Administrasi Bisnis Terakreditasi A SK BAN –PT NO: 468/SK/BAN-PT/Akred/S/XII/2014 Pengaruh Brand Association terhadap Consumer Response pada Mobil Merek Toyota Agya dan Toyota Calya di Bandung Skripsi Oleh Felicia 2013320092 Pembimbing Fransiska Anita Subari , S.S, M.M. Bandung 2017 Fakultas Ilmu Sosial dan Ilmu Politik Program Studi Ilmu Administrasi Bisnis Tanda Pengesahan Skripsi Nama : Felicia Nomor Pokok : 2013320092 Judul : Pengaruh Brand Association terhadap Consumer Response pada Mobil Merek Toyota Agya dan Toyota Calya di Bandung Telah diuji dalam Ujian Sidang jenjang Sarjana Pada Kamis, 6 Juli 2017 Dan dinyatakan LULUS Tim Penguji Ketua sidang merangkap anggota Dr. Rulyusa Pratikto, S.AB., M.SE : ________________________ Sekretaris Fransiska Anita Subari , S.S, M.M. : ________________________ Anggota Sanerya Hendrawan, Ph.D : ________________________ Mengesahkan, Dekan Fakultas Ilmu Sosial dan Ilmu Politik Dr. Pius Sugeng Prasetyo, M.Si Pernyataan Saya yang bertanda tangan dibawah ini: Nama : Felicia NPM : 2013320092 Jurusan/ Program Studi : Ilmu Administrasi Bisnis / Fakultas Ilmu Sosial dan Ilmu Politik Judul : Pengaruh Brand Association terhadap Consumer Response pada Mobil Merek Toyota Agya dan Toyota Calya di Bandung Dengan ini menyatakan bahwa skripsi ini merupakan hasil karya tulis ilmiah sendiri dan bukanlah merupakan karya yang pernah diajukan untuk memperoleh gelar akademik oleh pihak lain. -

BAB I PENDAHULUAN 1.1 Gambaran Umum Objek Penelitian 1.1.1 Profil

BAB I PENDAHULUAN 1.1 Gambaran Umum Objek Penelitian 1.1.1 Profil Perusahaan Suzuki adalah salah satu perusahaan asal Jepang yang mengembankan sayap di Indonesia. PT Suzuki Indomobil Motor merupakan kelompok usaha yang bergerak dibidang industri otomotif yang memproduksi, memasarkan, memperniagakan motor, mobil dan motor tempel (outboard-motor). Hal tersebut juga diidukung dengan pelayanan purna jual suku cadang serta perbaikan/pemeliharaan di seluruh Indonesia yang solid dan terintegrasi dalam melayani para pelanggan Suzuki. Suzuki Indonesia telah memberikan kontribusi untuk bangsa dan masyarakat dengan memberikan produk-produk bermanfaat bagi perkembangan bangsa. Pelayanan profesional dibidang pemasaran produk dan jasa pelayanan juga menjadi komitmen utama kami untuk memberikan yang terbaik bagi para pelanggan setia Suzuki. Saling percaya dan menghormati merupakan nilai yang kami tanam dalam setiap kerja sama yang dijalani antara karyawan, pemasok, dealer-dealer diseluruh Indonesia. PT. Indomobil Suzuki International (ISI) dirubah menjadi PT. Suzuki Indomobil Motor (SIM) merupakan sebuah perusahaan penanaman modal asing (PMA) yang berdiri dengan kekuatan 5 (Lima) buah perusahaan. Perusahaan tersebut adalah sebagai berikut : 1. PT. Indohero Steel & Engineering Co. 2. PT. Indomobil Utama. 3. PT. Suzuki Indonesia Manufacturing. 4. PT. Suzuki Engine Industry. 5. PT. First Chemical Industry. Lima perusahaan tersebut bergabung (Merger) dengan persetujuan dari Presiden Republik Indonesia melalui surat pemberitahuan tentang persetujuan Presiden dari Ketua Badan Koordinasi Penanaman Modal (BKPN) nomor 05 / I / PMA / 90 tertanggal 1 Januari 1990, dan diperingati sebagai berdirinya PT. Suzuki Indomobil Motor, yang bergerak dalam bidang usaha Industri Komponen dan Perakitan kendaraan bermotor Merek SUZUKI roda dua (Sepeda Motor) dan roda empat (Mobil). Lokasi kantor pusat PT. Suzuki Indomobil Motor berada di Wisma Indomobil di Jalan. -

Asia's Low-Cost Compact Vehicle Development

Order Form Special Offer for Orders! Please check the appropriate box below and E-mail or fax this form to FOURIN, Inc. E-mail: [email protected] FAX from overseas:+81-52-789-1147 FAX from Japan: 052-789-1147 Asia’s Low-Cost Compact Vehicle Development □Asia’s Low-Cost Compact Vehicle Development (Publishing date: May 2009) - Present Situation and Future Market Perspective of Emerging Nations - A4 Size: 214 pages Price: 95,000JPY / 1,030USD (free shipping but VAT for Japan orders)* ■Format: A4, 215 pages ■Publication date: May 2009 ■Price: 95,000JPY / 1,030USD (free shipping but VAT for Japan orders) □Asia Automotive Industry Yearbook 2009 (Publishing date: Nov. 2008) ■Analysis of competitiveness on 48 major strategic models for emerging countries based on product outlines, product A4 Size: 177 pages Price: 95,000 JPY / 1,030 USD (free shipping but VAT for Japan orders)* concepts, manufacturing and sales schedule. *Exchange rate: 1 USD = 92 JPY (Exchange rate as of January 5, 2009). USD prices: If the exchange rate changes 10% or more from the original rate, ■Increasing significance of emerging countries is changing the roles of each country for concept designing, development, the prices in USD are recalculated based on the new exchange rate the following day. Prices are rounded down to the nearest whole number. manufacturing and export of strategic vehicles for emerging countries. Shipping fee: FOURIN pays for shipping fee (Campaign for 2009). Japan VAT: VAT is applied to orders placed by customers in Japan. ■Analysis on current status and forecast of motorization in Asia based on sales trends by vehicle segments and replacement ■ Special Offer ■ demands from motorcycles. -

Hapiz Islamsyah Fakultas Industri Kreatif Dan Telematika Universitas Trilogi [email protected]

Jurnal I D E A L O G Ide dan Dialog Indonesia Vol.2 No.2, Agustus 2017 ISSN Cetak 2477 – 0566 ISSN Elektronik 2615 - 6776 Hapiz Islamsyah Fakultas Industri Kreatif dan Telematika Universitas Trilogi [email protected] PERANAN STYLING DAN ERGONOMI PADA CITY CAR TERHADAP MASYARAKAT URBAN JAKARTA (STUDI KASUS EKSTERIOR DAN INTERIOR SUZUKI KARIMUN WAGON R DAN DAIHATSU AYLA) Abstrak. Ketika kita berbicara tentang desain sangat berkaitan dengan banyak aspek, hal yang paling penting dari aspek ini adalah fungsi dan estetika, desain tanpa estetika menjadi kekosongan dan desain tanpa fungsi menjadi tidak berguna. Saai ini ilmu pengetahuan, teknologi dan budaya hari ini menjadi bagian gaya hidup. Sebagian besar objek yang digunakan oleh manusia, dirancang oleh desainer, untuk memenuhi kebutuhan dasar dan keinginan manusia, gaya hidup manusia modern adalah kebanggaan paling penting, alat elektronik dan otomotif yang sebagian besar terhubung dengan kehidupan mereka. Dalam penelitian ini dibahas tentang kinerja LCGC (Low Cost Green Car) yang paling umum digunakan masyarakat urban di Jakarta dengan melihat dari segi styling dan ergonomis, penelitian ini dimulai dengan mengumpulkan data melalui observasi dan wawancara dari resoponden dan ahli. Semua data akan diolah dan hasil dari penelitian ini adalah untuk mendorong industri manukfaktur dan desainer produk otomotif untuk membuat mobil dengan aspek estetika dan aspek ergomonik yang sangat penting. Kata kunci: gaya hidup, fungsi, ergonomis, styling, LCGC Abstract. When we talk about Design is related to many aspect, the most important things of this aspect is functions and aesthetic, design witout aesthetic becomes emptiness adnd design without function becomes useless. Now day’s science, technology and culture become part of life style. -

Vehicle Quality in Indonesia Improves Again from Five Years Ago, J.D. Power Finds

Vehicle Quality in Indonesia Improves Again from Five Years Ago, J.D. Power Finds Honda Receives Two Model-Level Awards for Initial Quality; Toyota and Suzuki Each Receive One SINGAPORE: 21 Dec. 2016 — New-vehicle quality in Indonesia continues to improve from five years ago, specifically in areas pertaining to noise and function-related problems, according to the J.D. Power 2016 Indonesia Initial Quality StudySM (IQS), released today. The study measures problems experienced by new-vehicle owners during the first two to six months of ownership and examines more than 200 problems in eight vehicle categories (listed in order of frequency of reported problems): engine and transmission; driving experience; vehicle interior; vehicle exterior; features, controls and displays; heating, ventilating and air conditioning (HVAC); audio, entertainment and navigation; and seats. Initial quality is determined by the average number of problems experienced per 100 vehicles (PP100), with a lower score reflecting higher quality. The industry averages 70 PP100 in 2016, compared with 82 PP100 in 2012. The numbers of reported problems related to vehicle noise and function have dropped by 6 PP100 and 3 PP100, respectively. However, design-related problems do not show an improvement in the same time period, increasing to 19 PP100 in 2016 from 18 PP100 in 2012. “Strong focus over the years on manufacturing execution is yielding results,” said Kaustav Roy, director at J.D. Power in Singapore. “Customers are clearly appreciating the same by reporting fewer problems during their initial vehicle ownership.” Roy added, however, that the challenge lies in aligning vehicle design with a set of optimized requirements for customers in Indonesia. -

Explore Bali in Style and Comfort CAR & VAN RENTAL Wherever You Go Becomes a Part of You Somehow

Explore Bali in style and comfort CAR & VAN RENTAL Wherever you go becomes a part of you somehow. " - Anita Desai Bali Kresna Rent Car (BKR) ABOUT Bali Kresna Rent Car is a company providing Car Rental In Bali that is 100% Balinese owned. We know the Bali is still a wonderful place to visit and a number one tourist destination. As proof, more and more people are coming to stay in Bali for short and long periods. Many non-Indonesians now live and own houses here. In this way visitors love Bali Island and love to have their own way to explore the beauty of Balinese nature and feel the warmth of Balinese people. We are located the center of Legian (just 10 minutes from Bali International airport) and for your convenience we are pleased to offer a drop off and pick up services at the airport or delivery a vehicle to your hotel or holiday home on Bali. Our service can include with a driver, you can drive by yourself, or request a tour guide. Our service can include a driver, or you can drive by yourself. A tour guide is also available upon request. Daily self-driving is inclusive of car insurance, free airport / hotel pick up or drop only for service self drive off can be made to the Nusa Dua, Jimbaran, Kuta, Legian, Sanur, Ubud, Denpasar areas. Website: www.balikresnarentcar.com Image: Toyota Car Selection Toyota Avanza Daihatsu Xenia Toyota Innova Toyota Yaris Self drive - $22 to $28 per day (min. 2 days) Self drive - $22 to $28 per day (min.