Investment in Serbia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

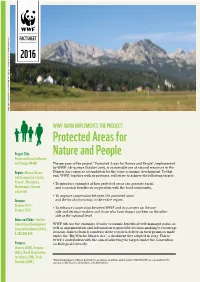

WWF Adria Implements the Project: Protected Areas for Nature And

Protected Areas for Nature and People – NP Durmitor, Montenegro © Martin Šolar, WWF Adria FACTSHEET 2016 WWF ADRIA IMPLEMENTS THE PROJECT: Protected Areas for Project Title: Nature and People Protected Areas for Nature and People, PA4NP The purpose of the project “Protected Areas for Nature and People”, implemented by WWF Adria since October 2015, is sustainable use of natural resources in the Region: Albania, Bosnia Dinaric Arc region as a foundation for the socio-economic development. To that and Herzegovina, Croatia, end, WWF, together with its partners, will strive to achieve the following targets: Kosovo*, Macedonia, • To introduce examples of how protected areas can generate social Montenegro, Slovenia and economic benefits in cooperation with the local community, and Serbia • To improve cooperation between the protected areas Duration: and the local community in the entire region, October 2015 – • To enhance cooperation between WWF and its partners on the one October 2019 side and decision-makers and those who have impact on them on the other side at the national level. Donor and Value: Swedish International Development WWF will use the examples of socio-economic benefits of well-managed parks, as Cooperation Agency (Sida), well as argumentation and information required for decision-making to encourage 4,200,000 EUR decision-makers from 8 countries in the region to deliver on their promises made under the “Big Win for Dinaric Arc”, a document they adopted in 2013. This is WWF’s contribution with the aim of achieving the targets -

Atlas of American Orthodox Christian Monasteries

Atlas of American Orthodox Christian Monasteries Atlas of Whether used as a scholarly introduction into Eastern Christian monasticism or researcher’s directory or a travel guide, Alexei Krindatch brings together a fascinating collection of articles, facts, and statistics to comprehensively describe Orthodox Christian Monasteries in the United States. The careful examina- Atlas of American Orthodox tion of the key features of Orthodox monasteries provides solid academic frame for this book. With enticing verbal and photographic renderings, twenty-three Orthodox monastic communities scattered throughout the United States are brought to life for the reader. This is an essential book for anyone seeking to sample, explore or just better understand Orthodox Christian monastic life. Christian Monasteries Scott Thumma, Ph.D. Director Hartford Institute for Religion Research A truly delightful insight into Orthodox monasticism in the United States. The chapters on the history and tradition of Orthodox monasticism are carefully written to provide the reader with a solid theological understanding. They are then followed by a very human and personal description of the individual US Orthodox monasteries. A good resource for scholars, but also an excellent ‘tour guide’ for those seeking a more personal and intimate experience of monasticism. Thomas Gaunt, S.J., Ph.D. Executive Director Center for Applied Research in the Apostolate (CARA) This is a fascinating and comprehensive guide to a small but important sector of American religious life. Whether you want to know about the history and theology of Orthodox monasticism or you just want to know what to expect if you visit, the stories, maps, and directories here are invaluable. -

Rivers and Lakes in Serbia

NATIONAL TOURISM ORGANISATION OF SERBIA Čika Ljubina 8, 11000 Belgrade Phone: +381 11 6557 100 Rivers and Lakes Fax: +381 11 2626 767 E-mail: [email protected] www.serbia.travel Tourist Information Centre and Souvenir Shop Tel : +381 11 6557 127 in Serbia E-mail: [email protected] NATIONAL TOURISM ORGANISATION OF SERBIA www.serbia.travel Rivers and Lakes in Serbia PALIĆ LAKE BELA CRKVA LAKES LAKE OF BOR SILVER LAKE GAZIVODE LAKE VLASINA LAKE LAKES OF THE UVAC RIVER LIM RIVER DRINA RIVER SAVA RIVER ADA CIGANLIJA LAKE BELGRADE DANUBE RIVER TIMOK RIVER NIŠAVA RIVER IBAR RIVER WESTERN MORAVA RIVER SOUTHERN MORAVA RIVER GREAT MORAVA RIVER TISA RIVER MORE RIVERS AND LAKES International Border Monastery Provincial Border UNESKO Cultural Site Settlement Signs Castle, Medieval Town Archeological Site Rivers and Lakes Roman Emperors Route Highway (pay toll, enterance) Spa, Air Spa One-lane Highway Rural tourism Regional Road Rafting International Border Crossing Fishing Area Airport Camp Tourist Port Bicycle trail “A river could be an ocean, if it doubled up – it has in itself so much enormous, eternal water ...” Miroslav Antić - serbian poet Photo-poetry on the rivers and lakes of Serbia There is a poetic image saying that the wide lowland of The famous Viennese waltz The Blue Danube by Johann Vojvodina in the north of Serbia reminds us of a sea during Baptist Strauss, Jr. is known to have been composed exactly the night, under the splendor of the stars. There really used to on his journey down the Danube, the river that connects 10 be the Pannonian Sea, but had flowed away a long time ago. -

Sustainable Tourism for Rural Lovren, Vojislavka Šatrić and Jelena Development” (2010 – 2012) Beronja Provided Their Contributions Both in English and Serbian

Environment and sustainable rural tourism in four regions of Serbia Southern Banat.Central Serbia.Lower Danube.Eastern Serbia - as they are and as they could be - November 2012, Belgrade, Serbia Impressum PUBLISHER: TRANSLATORS: Th e United Nations Environment Marko Stanojević, Jasna Berić and Jelena Programme (UNEP) and Young Pejić; Researchers of Serbia, under the auspices Prof. Branko Karadžić, Prof. Milica of the joint United Nations programme Jovanović Popović, Violeta Orlović “Sustainable Tourism for Rural Lovren, Vojislavka Šatrić and Jelena Development” (2010 – 2012) Beronja provided their contributions both in English and Serbian. EDITORS: Jelena Beronja, David Owen, PROOFREADING: Aleksandar Petrović, Tanja Petrović Charles Robertson, Clare Ann Zubac, Christine Prickett CONTRIBUTING AUTHORS: Prof. Branko Karadžić PhD, GRAPHIC PREPARATION, Prof. Milica Jovanović Popović PhD, LAYOUT and DESIGN: Ass. Prof. Vladimir Stojanović PhD, Olivera Petrović Ass. Prof. Dejan Đorđević PhD, Aleksandar Petrović MSc, COVER ILLUSTRATION: David Owen MSc, Manja Lekić Dušica Trnavac, Ivan Svetozarević MA, PRINTED BY: Jelena Beronja, AVANTGUARDE, Beograd Milka Gvozdenović, Sanja Filipović PhD, Date: November 2012. Tanja Petrović, Mesto: Belgrade, Serbia Violeta Orlović Lovren PhD, Vojislavka Šatrić. Th e designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the United Nations Environment Programme concerning the legal status of any country, territory, city or area or of its authorities, or concerning delimitation of its frontiers or boundaries. Moreover, the views expressed do not necessarily represent the decision or the stated policy of the United Nations, nor does citing of trade names or commercial processes constitute endorsement. Acknowledgments Th is publication was developed under the auspices of the United Nations’ joint programme “Sustainable Tourism for Rural Development“, fi nanced by the Kingdom of Spain through the Millennium Development Goals Achievement Fund (MDGF). -

The Functioning of the Pensions Insurance System in the Countries of Former Yugoslavia

Velizar Golubović The functioning of the pensions insurance system in the countries of former Yugoslavia Abstract This article analyses the functioning of the pensions insurance system in the coun- tries of the former Socialist Federal Republic of Yugoslavia. The first part of the article shows that the implemented reforms comprised stricter conditions for the realisation of pensions rights through an increase in the retirement age and a de- crease in the statutory replacement rate. The second part of the article presents the main indicators of the functioning of the pensions systems. The analysis of the results achieved reveals an exceptionally unfavourable picture. This primarily refers to the unfavourable ratio of the number of insured and pensions beneficia- ries due to high unemployment, resulting in a high deficit in the pensions system. The third part points to the need for, and direction of, further reforms of the pen- sions systems aiming at the creation of adequate and financially sustainable pen- sions systems. The conclusion summarises the results of the conducted analysis. Keywords: functioning pensions insurance system, pensions reform, countries of the former Yugoslavia, net replacement rate, retirement age Introduction With the downfall of the Socialist Federal Republic of Yugoslavia, the six republics became independent states – Slovenia, Croatia and Macedonia (1991); Bosnia and Herzegovina (1992); and Serbia and Montenegro (2005), the last two remaining united until their independence. The downfall of Yugoslavia was motivated by a desi- re for the creation of nation states, which led to intra-national conflicts in Croatia (1991-1995) and Bosnia and Herzegovina (1992-1995).1 The war conflicts brought a number of victims and mass deportations, as well as large-scale destruction and mate- rial damage. -

Tentative Lists Submitted by States Parties As of 15 April 2021, in Conformity with the Operational Guidelines

World Heritage 44 COM WHC/21/44.COM/8A Paris, 4 June 2021 Original: English UNITED NATIONS EDUCATIONAL, SCIENTIFIC AND CULTURAL ORGANIZATION CONVENTION CONCERNING THE PROTECTION OF THE WORLD CULTURAL AND NATURAL HERITAGE WORLD HERITAGE COMMITTEE Extended forty-fourth session Fuzhou (China) / Online meeting 16 – 31 July 2021 Item 8 of the Provisional Agenda: Establishment of the World Heritage List and of the List of World Heritage in Danger 8A. Tentative Lists submitted by States Parties as of 15 April 2021, in conformity with the Operational Guidelines SUMMARY This document presents the Tentative Lists of all States Parties submitted in conformity with the Operational Guidelines as of 15 April 2021. • Annex 1 presents a full list of States Parties indicating the date of the most recent Tentative List submission. • Annex 2 presents new Tentative Lists (or additions to Tentative Lists) submitted by States Parties since 16 April 2019. • Annex 3 presents a list of all sites included in the Tentative Lists of the States Parties to the Convention, in alphabetical order. Draft Decision: 44 COM 8A, see point II I. EXAMINATION OF TENTATIVE LISTS 1. The World Heritage Convention provides that each State Party to the Convention shall submit to the World Heritage Committee an inventory of the cultural and natural sites situated within its territory, which it considers suitable for inscription on the World Heritage List, and which it intends to nominate during the following five to ten years. Over the years, the Committee has repeatedly confirmed the importance of these Lists, also known as Tentative Lists, for planning purposes, comparative analyses of nominations and for facilitating the undertaking of global and thematic studies. -

Insurance Market Development in the Former Yugoslav Republics, Non-EU Countries

Journal of Economic and Social Studies Insurance Market Development in the Former Yugoslav Republics, Non-EU Countries Nikola Dacev Law Faculty “Justinian the First”, Skopje Macedonia [email protected] Abstract: This paper presents an insurance market research KEYWORDS: of the markets in several Balkan countries that were part of Insurance Markets, Developing former Yugoslavia and are still not members of EU. Being Countries, Life Insurance categorized as developing countries, they have far lower development degree in comparison with the European ARTICLE HISTORY Insurance Federation member countries. By means of Submitted: 29 April 2012 Resubmitted: 30 September 2012 comparison between the basic insurance market Resubmitted: 20 November 2012 development indicators in these countries, the law Accepted: 24 December 2012 regulations, as well as through conducting surveys, based on questionnaires, which appoint the reasons for the underdevelopment in the sphere of life insurance, the paper gives a clearer perception, in terms of the conditions of the insurance markets, placed on the margins of the European insurance market. Its utmost objective is to point and argue several measures, which would improve the insurance market conditions in the already mentioned countries, i.e. would contribute to the development increase and the acceleration of these insurance markets. As a result, that would raise the protection measures and the safety, both to the citizens and their material goods. JEL codes: G22, K22, M31 151 Nikola DACEV Introduction The insurance market role importance in the economy and the contemporary world in general increases rapidly, all the time. Today, there is hardly any economic sphere in which the insurance issue is not included. -

Tara-Drina National Park

Feasibility study on establishing transboundary cooperation in the potential transboundary protected area: Tara-Drina National Park Prepared within the project “Sustaining Rural Communities and their Traditional Landscapes Through Strengthened Environmental Governance in Transboundary Protected Areas of the Dinaric Arc” ENVIRONMENT FOR PEOPLE A Western Balkans Environment & Development in the Dinaric Arc Cooperation Programme Author: Marijana Josipovic Photographs: Tara National Park archive Proofreading Linda Zanella Design and layout: Imre Sebestyen, jr. / UNITgraphics.com Available from: IUCN Programme Office for South-Eastern Europe Dr Ivana Ribara 91 11070 Belgrade, Serbia [email protected] Tel +381 11 2272 411 Fax +381 11 2272 531 www.iucn.org/publications Acknowledgments: A Special “thank you” goes to: Boris Erg, Veronika Ferdinandova (IUCN SEE), Dr. Deni Porej, (WWF MedPO), Ms. Aleksandra Mladenovic for commenting and editing the assessment text. Zbigniew Niewiadomski, consultant, UNEP Vienna ISCC for providing the study concept. Emira Mesanovic Mandic, WWF MedPO for coordinating the assessment process. 2 The designation of geographical entities in this publication, and the presentation of the material, do not imply the expression of any opinion whatsoever on the part of IUCN, WWFMedPO and SNV concerning the legal status of any country, territory, or area, or of its authorities, or concerning the delimitation of its frontiers or boundaries. The views expressed in this publication do not necessarily reflect those of IUCN, WWF MedPO and SNV. This publication has been made possible by funding from the Ministry for Foreign Affairs of Finland. Published by: IUCN, Gland, Switzerland and Belgrade, Serbia in collaboration with WWFMedPO and SNV Copyright: © 2011 International Union for Conservation of Nature Reproduction of this publication for educational or other non-commercial purposes is authorized without prior written permission from the copyright holder, provided the source is fully acknowledged. -

Diversity of Alien Macroinvertebrate Species in Serbian Waters

water Article Diversity of Alien Macroinvertebrate Species in Serbian Waters Katarina Zori´c* , Ana Atanackovi´c,Jelena Tomovi´c,Božica Vasiljevi´c,Bojana Tubi´c and Momir Paunovi´c Department for Hydroecology and Water Protection, Institute for Biological Research “Siniša Stankovi´c”—NationalInstitute of Republic of Serbia, University of Belgrade, Bulevar despota Stefana 142, 11060 Belgrade, Serbia; [email protected] (A.A.); [email protected] (J.T.); [email protected] (B.V.); [email protected] (B.T.); [email protected] (M.P.) * Correspondence: [email protected] Received: 29 September 2020; Accepted: 7 December 2020; Published: 15 December 2020 Abstract: This article provides the first comprehensive list of alien macroinvertebrate species registered and/or established in aquatic ecosystems in Serbia as a potential threat to native biodiversity. The list comprised field investigations, articles, grey literature, and unpublished data. Twenty-nine species of macroinvertebrates have been recorded since 1942, with a domination of the Ponto-Caspian faunistic elements. The majority of recorded species have broad distribution and are naturalized in the waters of Serbia, while occasional or single findings of seven taxa indicate that these species have failed to form populations. Presented results clearly show that the Danube is the main corridor for the introduction and spread of non-native species into Serbia. Keywords: Serbia; inland waters; allochthonous species; introduction 1. Introduction The Water Framework Directive (WFD) [1] represents key regulation and one of the most important documents in the European Union water legislation since it was adopted in 2000. -

3 | 2016 Megatrend Revija

C M Y K 3 16 Vol. 13 (3) 2016 • UDK 33 • ISSN 1820-3159 | MEGATREND MEGATREND REVIJA REVIEW MEGATREND REVIEW 3 | 2016 MEGATREND REVIJA www.naisbitt.edu.rs C M Y K Vol. 13, № 3, 2016 MEGATREND REVIJA MEGATREND REVIEW 3/2016 Univerzitet „Džon Nezbit”, Beograd “John Naisbitt” University, Belgrade Megatrend revija • Megatrend review № 3/2016 I zdavački savet / Publishing Council: Predsednik / President: Professor Slobodan Pajović, PhD Članovi iz inostranstva / International members: Professor Jean-Jacques CHANARON, PhD – Grenoble Ecole de Management, France Academician Vlado KAMBOVSKI – Macedonian Academy of Sciences and Arts, Skopje, FYR Macedonia Professor Žarko LAZAREVIć, PhD – Institute for Contemporary History, Ljubljana, Slovenia Professor Norbert Pap, PhD – University of Pécs, Hungary Professor Sung Jo PARK, PhD – Free University, Berlin, Germany Professor Ioan TalpOS, PhD – west University of temisoara, romania Članovi iz Srbije / Members from Serbia: Professor Miljojko BAZIć, PhD – “John Naisbitt” University, Belgrade Associate Professor Ana JOVANCAI STAKIć, PhD – “John Naisbitt” University, Belgrade Professor Oskar KOVAč, PhD – “John Naisbitt” University, Belgrade Professor Momčilo MILISAVLJEVIć, PhD – in retirement Professor Dragan NIKODIJEVIć, PhD – “John Naisbitt” University, Belgrade Professor Milivoje PAVLOVIć, PhD – “John Naisbitt” University, Belgrade Professor Vladimir PRVULOVIć, PhD – “John Naisbitt” University, Belgrade Professor Milan STAMATOVIć, PhD – Metropolitan University, Belgrade Professor Slobodan STAMENKOVIć, PhD – “John Naisbitt” University, Belgrade Izdaje i štampa / Published and printed by: Univerzitet „Džon Nezbit”, Beograd / “John Naisbitt” University, Belgrade ISSN 1820-3159 A dresa redakcije / Editorial address: Megatrend revija / Megatrend Review UDK / UDC 33 Bulevar maršala Tolbuhina 8 11070 Novi Beograd, Srbija Svi članci su recenzirani od strane dva recenzenta. Tel.: (381-11) 220 31 50 All papers have been reviewed by two reviewers. -

The Destruction of Yugoslavia

Fordham International Law Journal Volume 19, Issue 2 1995 Article 18 The Destruction of Yugoslavia Svetozar Stojanovic∗ ∗ Copyright c 1995 by the authors. Fordham International Law Journal is produced by The Berke- ley Electronic Press (bepress). http://ir.lawnet.fordham.edu/ilj The Destruction of Yugoslavia Svetozar Stojanovic Abstract If my statement about the first Yugoslavia being in many ways a non-synchronized and con- tradictory state is correct, what then can be said about the second Yugoslavia that endeavored, by keeping silent, to fill in the fatal fissure opened in Jasenovac and other places of annihilation of Serbs in the so-called Independent State of Croatia during the Second World War? For that reason, the former intermediator of the “international community” in Yugoslav conflicts, Lord Carrington, has repeatedly stated that with its new Constitution, Croatia rekindled the conflict with the Serbs. The essay will begin by discussing discuss the paralization to the breaking-up of the state, before moving to a discussion of the wars between secessionists and antisecessionists. We will also ex- amine the role of the Yugoslav Army, and Western triumphalism regarding the Yugoslav tragedy. THE DESTRUCTION OF YUGOSLAVIA Svetozar Stojanovic* I. A NON-SYNCHRONIZED AND CONTRADICTORY STATE From its formation in 1918, Yugoslavia was a non-synchronized and contradictory state. It was created mainly by Serbia and Mon- tenegro, countries that were victors in the First World War. The Serbian nation's human and material sacrifice invested in Yugo- slavia was unparalleled. Serbs were convinced that they could best solve their national question in a broader Southern Slav framework. -

Insecta: Heteroptera: Tingidae)

Arch. Biol. Sci., Belgrade, 57 (2), 147-149, 2005. NEW RECORDS OF HETEROPTERA FROM SERBIA (INSECTA: HETEROPTERA: TINGIDAE) LJILJANA PROTIĆ Natural History Museum, 11000 Belgrade, Serbia and Montenegro Abstract - The Serbian fauna of Heteroptera is increased by four new species from the family Tingidae. These species are: Catoplatus fabricii (Stål), Copium teucrii teucrii (Host), Derephysia cristata (Panzer), and Dictyla convergens (Her- rich-Schaeffer). The paper also includes a summary of literature data on the heteropteran biology and distribution. Key words: Distribution, zoogeography, ecology, Heteroptera, Tingidae, Serbia UDC 595.754(497.11) INTRODUCTION Mount Avala is under deciduous and coniferous forests and includes areas under mostly deciduous submediter- The family Tingidae is represented in Serbia with 50 ranean forests. A part of its forested territory under influ- species. The species from this family in Serbia have so ence of humans has been transformed into cultivated far been mostly mentioned only in faunistic papers fields (agrocenoses) or ruderal ground, where a sponta- (Horváth, 1903; Protić, 1993/94, 1998, 2004, neous herbaceous flora has developed. 2004a). Two species distributed in Serbia are of econom- ic importance: Corythuca ciliata (Say) and Stephanitis Mt. Divčibare, 900 m [DP28]. The Divčibare Plateau pyri (Fabricius), and special research has been devoted to is a constituent part of Mt. Maljen, which is about 100 km them (Bogavac, 1964; Balarin et al. 1979; Tomić SW of Belgrade. It is characterized by mesophilous and Mihajlović, 1974). The collection of the Natural meadows. History Museum includes 35 species. Four of them are new for the Serbian Heteroptera fauna: Catoplatus The gorge Jelašnička Klisura [EN98] is situated 15 fabricii (Stål), Copium teucrii teucrii (Host), Derephysia km E of Niš at 250-600 m alt.