International Energy Module

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WTI Crude Oil West Texas Intermediate

WTI Crude Oil West Texas Intermediate Alexander Filitz Minh Khoa Nguyen Outline • Crude Oil • Value Chain • Politics • Market • Demand • Facts & Figures • Discussion Crude Oil • Flammable liquid consisting of a complex mixture of hydrocarbons of various molecular weights and other liquid organic compounds • Is recovered mostly through oil drilling • In its strictest sense, petroleum includes only crude oil, but in common usage it includes all liquid, gaseous, and solid hydrocarbons. • An oil well produces predominantly crude oil, with some natural gas dissolved in it Classification • By the geographic location it is produced in • Its API gravity (an oil industry measure of density) • Its sulfur content • Some of the common reference crudes are: • West Texas Intermediate (WTI), a very high-quality, sweet, light oil delivered at Cushing, Oklahoma for North American oil. • Brent Blend, comprising 15 oils from fields in the North Sea. • Dubai-Oman, used as benchmark for Middle East sour crude oil flowing to the Asia-Pacific region • The OPEC Reference Basket, a weighted average of oil blends from various OPEC (The Organization of the Petroleum Exporting Countries) countries West Texas Intermediate • Also known as Texas light sweet, used as a benchmark in oil pricing • API gravity of around 39.6 and specific gravity of 0.827 and 0.24% sulfur • WTI is refined mostly in the Midwest and Gulf Coast regions in the U.S • It is the underlying commodity of New York Mercantile Exchange's (NYMEX) oil futures contracts • Often referenced in news reports -

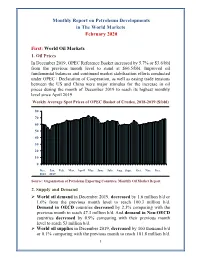

Monthly Report on Petroleum Developments in the World Markets February 2020

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Crude Oil Prices Also Affect a Wide Range of Other Non-Petroleum Forecasts Produced by STIFS

Short-Term Energy Outlook Crude Oil Price Forecasts Independent Statistics & Analysis U.S. Department of Energy www.eia.gov Washington, DC 20585 Last Updated 2020 This report was prepared by the U.S. Energy Information Administration (EIA), the statistical and analytical agency within the U.S. Department of Energy. By law, EIA’s data, analyses, and forecasts are independent of approval by any other officer or employee of the United States Government. The views in this report therefore should not be construed as representing those of the Department of Energy or other federal agencies. U.S. Energy Information Administration | Short-Term Energy Outlook Crude Oil Price Forecasts i 1. Introduction In the Short-Term Energy Outlook (STEO), EIA’s forecasts for monthly average Brent and West Texas Intermediate (WTI) spot prices are calculated outside of the Short-Term Integrated Forecasting System (STIFS). The crude oil price forecast is one of the main determinants of the forecast for many of the petroleum price, consumption, and production variables within STIFS. Crude oil prices also affect a wide range of other non-petroleum forecasts produced by STIFS. EIA first formulates a forecast for Brent crude oil spot prices and then forecasts WTI spot prices by creating a forecast for the spot price spread between Brent and WTI. EIA considers three main inputs to determine its Brent price forecast: • A pooling model that provides a single Brent price series that is an average of five separate models • A linear regression using independent variables from the STEO forecast • Analyst judgment based on an understanding of global oil market dynamics and EIA’s forecast for supply and demand balances In sections three through five below, we discuss each of these inputs separately. -

Peak Oil Demand and Long-Run Oil Prices

January 2018 Peak Oil Demand and Long-Run Oil Prices Abstract The prospect that global oil demand will gradually slow and eventually peak has created a cottage industry of executives and commentators trying to predict the point at which demand will peak. In this Energy Insight, we argue that this focus seems misplaced. The date at which oil demand will stop growing is highly uncertain and small changes in assumptions can lead to vastly different estimates. More importantly, there is little reason to believe that once it does peak, that oil demand will fall sharply. The world is likely to demand large quantities of oil for many decades to come. Rather, the significance of peak oil is that it signals a shift in paradigm – from an age of (perceived) scarcity to an age of abundance – and with it is likely to herald a shift to a more competitive market environment. This change in paradigm is also likely to pose material challenges for oil producing economies as they try both to ensure that their oil is produced and consumed, and at the same time diversify their economies fit for a world in which they can no longer rely on oil revenues to provide their main source of revenue for the indefinite future. We argue that the extent and pace of this diversification is likely to have an important bearing on oil prices over the next 20 or 30 years. It seems likely that many low-cost producers will delay the pace at which they adopt a more competitive “higher volume, lower price” strategy until they have made material progress in reforming their economies. -

Welcome to the 11Th Edition of Energy Perspectives! This Is An

Welcome to the 11th edition of Energy Perspectives! This is an independent report that informs Equinor’s strategy and offers a fact-based contribution to the energy transition debate. This year’s edition is an update of the edition from November last year, and with a lot happening on the global arena the last 6 months, there is a lot to consider when looking 30 years ahead. As always, this report and its data and conclusions would be impossible without the excellent work of many of my colleagues, to whom I extend my appreciation and gratitude. You are the best! 1 Covid19 is not over. In a global perspective, we are still dealing with its impact and the enormous effects it has on people, societies, economies, and markets. We are not through it yet. And we might have to live with recurring infection spikes, especially in parts of the world that do not get sufficient access to vaccines. Recurring lockdowns entailed that energy demand, and in particular oil demand due to its use as a transport fuel, was hit hard. Recovery is in the making, and faster than many feared, but oil demand, as an example, is still not back to pre-Covid19-levels. The map shows how the pandemic has affected economies across the globe, with almost all countries pink or red, that is, with negative economic development. Industrialised countries are on their way out of recession while disabling the virus, but the uncertainty is still high in many emerging economies. 2 We are seeing signs of recovery. Thanks to the development and rollout of vaccines and massive public spending to stimulate demand, there are signs that the situation is being brought under control so that we can live with the virus more like we do with normal flus. -

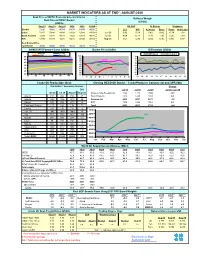

Market Indicators As at End*: August-2020

MARKET INDICATORS AS AT END*: AUGUST-2020 Spot Price of OPEC Basket & Selected Crudes Refiners' Margin Real Price of OPEC Basket (US$/b) (US$/b) Aug-18 Aug-19 Aug-20 2018 2019 2020# US Gulf N. Europe Singapore Basket 72.26 59.62 45.19 69.78 64.04 40.50 LLS WTI A. Heavy Brent Oman Arab Light Dubai 72.47 58.88 43.89 69.68 63.48 41.54 Jun-20 3.92 5.19 0.42 0.42 -0.74 1.02 North Sea Dtd 72.64 58.83 44.79 71.22 64.19 40.88 Jul-20 4.64 6.13 -1.86 1.30 1.26 1.99 WTI 67.99 54.84 42.36 65.16 57.02 38.15 Aug-20 3.67 5.30 -2.05 0.16 0.86 0.87 Real Basket Price Jun01=100 46.86 39.02 28.30 35.22 44.73 26.19 NYMEX WTI Forward Curve (US$/b) Basket Price (US$/b) Differentials (US$/b) May-20 Jun-20 WTI-Brent Brent-Dubai Jul-20 Aug-20 50 100 3 90 2 45 2018 80 1 70 40 0 60 35 2019 -1 50 30 40 -2 2020 -3 25 30 20 -4 20 10 -5 1M 3M 5M 7M 9M 11M J F M A M J J A S O N D 03 05 07 11 13 17 19 21 25 27 31 Crude Oil Production (tb/d) Closing OECD Oil Stocks - Crude/Products Commercial and SPR (Mb) Crude Oil Production (Tb/d) Production: Secondary Sources Change Diff. -

NEWS RELEASE June 15, 2021

925 North Eldridge Parkway Houston, TX 77079 Media Relations: 281-293-1149 www.conocophillips.com/media NEWS RELEASE June 15, 2021 ConocoPhillips to Host Market Update June 30 HOUSTON – ConocoPhillips (NYSE: COP) will host a virtual market update on Wednesday, June 30 beginning at 9:00 a.m. Central time. The meeting will feature presentations by ConocoPhillips executives, including Chairman and Chief Executive Officer Ryan Lance. A live webcast of the meeting will be made available on the ConocoPhillips Investor Relations website, www.conocophillips.com/investor. The event will be archived and available for replay later that day. The presentation, along with a transcript, will also be available on the Investor Relations website. --- # # # --- About ConocoPhillips Headquartered in Houston, Texas, ConocoPhillips had operations and activities in 15 countries, $84 billion of total assets, and approximately 10,300 employees at March 31, 2021. Production excluding Libya averaged 1,488 MBOED for the three months ended March 31, 2021, and proved reserves were 4.5 BBOE as of Dec. 31, 2020. For more information, go to www.conocophillips.com. Contacts Media Dennis Nuss 281-293-1149 [email protected] Investor Relations 281-293-5000 [email protected] CAUTIONARY STATEMENT FOR THE PURPOSES OF THE "SAFE HARBOR" PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 This news release contains forward-looking statements as defined under the federal securities laws. Forward-looking statements relate to future events and anticipated results of operations, business strategies, and other aspects of our operations or operating results. Words and phrases such as “anticipate," “estimate,” “believe,” “budget,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict," “seek,” “should,” “will,” “would,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” and other similar words can be used to identify forward-looking statements. -

Price Forecast December 31, 2018 Resource Evaluation & Advisory This Page Has Been Intentionally Left Blank

Price forecast December 31, 2018 Resource Evaluation & Advisory This page has been intentionally left blank. 2 Forecast commentary 4 Alberta upstream oil and gas investment and royalties 8 Canadian economic outlook 10 Canadian domestic price forecast 12 International price forecast 14 Global trends 15 Canadian domestic price tables 19 International price tables 22 Price philosophy 24 Glossary 25 3 Price Forecast December 31, 2018 | Forecast commentary Forecast commentary “I can’t change the direction of the wind, but I can adjust my sails to always reach my destination.” — Jimmy Dean Volatility continues to be the theme of the reached highs of US$35/bbl. Storage oil and gas sector, with prices fluctuating stockpile volumes in Alberta rose to substantially throughout 2018. International approximately 35 MMbbl due to increased prices started to soften in October as the production from oil sands projects and industry expressed concern about increased temporarily decreased demand due to supply and minimal demand growth. WTI refinery maintenance. Major disruptions prices fell as domestic production volumes to Canadian crude oil exports occurred reached record levels and transport issues in Q4 2018 because of lower-than-usual persisted, primarily in the Permian basin. refinery utilization rates in the US Midwest, Overseas, Brent crude pricing continued where almost 70 percent of Canadian crude to outpace North American pricing, exported to the United States is processed. averaging approximately US$9/bbl higher Refinery utilization rates decreased to than WTI prices in the last quarter of 2018. 73 percent at the end of October from Brent prices decreased substantially in traditional rates of over 90 percent, leaving November, however, as a result of increased Canadian crude oil with nowhere to go. -

The Economic Impact of Oil Prices by Rurik Krymm

The Economic Impact of Oil Prices by Rurik Krymm During the last three months of 1973, the tax-paid costs of typical grades of crude petroleum in the main producing areas of the world, around the Persian Gulf, were roughly quadrupled, rising for typical Iranian and Arabian Ugh t crudes from about $1.85 per barrel in September 1973 to more than $7.00 by 1 January 1974, or from approximately $13.30 to more than $50.00per ton. Since the cost of production represents an insignificantly small fraction of the new cost level (less than 2%) and subject to complex adjustments reflecting varying qualities of crude oils and advantages of geographical location, the producing countries may expect to receive a minimum average revenue of $50.00 per ton of crude oil produced on their territory instead of $12.50. If we ignore the purchases which carried the prices of relatively small amounts of oil to the $100-$ 150range, this figure of $50.00per ton with future adjustments for inflation represents a probable guide line for future cost estimates. The change affects exports of close to 1.4 billion tons of oil and consequently involves an immediate shift of financial resources of close to 60 billion dollars per year from the oil-consuming to the oil-producing countries. Tables 1, 2 and 3 give an idea of the distribution of this burden by main geographical regions and of its possible evolution over the next seven years. The figures involved are so large that comparisons have been made by some authors with the reparations proposals advanced by the Allies at the end of the First World War. -

OPEC Annual Statistical Bulletin 2019 1 Contents

2019 OPEC Annual Statistical Bulletin Organization of the Petroleum Exporting Countries 1965 – 2019 th edition 54 Team for the preparation of the OPEC Annual Statistical Bulletin Secretary General Editorial Team Chairman of the Editorial Board Head, Public Relations and Information Department Mohammad Sanusi Barkindo Hasan Hafidh Director, Research Division Editor Ayed S. Al-Qahtani Maureen MacNeill, Mathew Quinn Project Leader Coordinator, Design and Production Head, Data Services Department Carola Bayer Adedapo Odulaja Senior Production Assistant Coordinator, Statistics Team Diana Lavnick Hossein Hassani Graphic Designer Statistics Team Tara Starnegg Pantelis Christodoulides, Klaus Stöger, Mohammad Sattar, Mihni Mihnev, Justinas Pelenis, Ksenia Gutman Coordinator, IT Development Team Mohamed Mekerba IT Development Team Vedran Hrgovcic, Zairul Arifin Online Annual Statistical Bulletin 2019: asb.opec.org Download now: Smart App for OPEC Annual Statistical Bulletin iOS Android Questions on data Data queries: [email protected]. Advertising The OPEC Annual Statistical Bulletin now accepts advertising. For details, please contact the Head, PR and Information Department, at the following address: Organization of the Petroleum Exporting Countries Helferstorferstrasse 17, A-1010 Vienna, Austria Tel: +43 1 211 12/0 Fax: +43 1 216 43 20 Advertising: [email protected] Website: www.opec.org Photographs Courtesy OPEC. © 2019 Organization of the Petroleum Exporting Countries ISSN 0475-0608 Contents Foreword 5 Key messages 6 Tables Page Page Section -

World Oil Outlook 2040

Organization of the Petroleum Exporting Countries 2019 World Oil Outlook 2040 2019 World Oil Outlook 2040 Organization of the Petroleum Exporting Countries Digital access to the WOO: an interactive user experience 24/7 OPEC’s World Oil Outlook (WOO) is part of the Organization’s commitment to market stability. The publication is a means to highlight and further the understanding of the many possible future challenges and opportunities for the oil industry. It is also a channel to encourage dialogue, cooperation and transparency between OPEC and other stakeholders within the industry. As part of OPEC’s ongoing efforts to improve user experience of the WOO and provide data transparency, two digital interfaces are available: the OPEC WOO App and the interactive version of the WOO. The OPEC WOO App provides increased access to the publication’s vital analysis and energy-related data. It is ideal for energy professionals, oil industry stakeholders, policymakers, market analysts, academics and the media. The App’s search engine enables users to easily find information, and its bookmarking function allows them to store and review their favourite articles. Its versatility also allows users to compare graphs and tables interactively, thereby maximizing information extraction and empowering users to undertake their own analysis. The interactive version of the WOO also provides the possibility to download specific data and information, thereby enhancing user experience. Download Access the OPEC WOO App interactive version Available for Android and iOS OPEC is a permanent, intergovernmental organization, established in Baghdad, Iraq, on 10–14 September 1960. The Organization comprises 14 Members: Algeria, Angola, Republic of the Congo, Ecuador, Equatorial Guinea, Gabon, the Islamic Republic of Iran, Iraq, Kuwait, Libya, Nigeria, Saudi Arabia, the United Arab Emirates and Venezuela. -

The US Shale Oil Boom, the Oil Export Ban, and the Economy

NBER WORKING PAPER SERIES THE U.S. SHALE OIL BOOM, THE OIL EXPORT BAN, AND THE ECONOMY: A GENERAL EQUILIBRIUM ANALYSIS Nida Çakir Melek Michael Plante Mine K. Yücel Working Paper 23818 http://www.nber.org/papers/w23818 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 September 2017 For helpful comments and suggestions we thank Nathan Balke, Michael Sposi, Kei-Mu Yi as well as participants of the USAEE 2015 and 2016 conferences, the 2015 NBER Meeting on Hydrocarbon Infrastructure, the 2015 Southern Economic Association Meeting, the 2016 IAEE conference, the 2016 Federal Reserve System Energy Meeting, the 2017 Georgetown Center for Economic Research Biennial Conference, the 2017 IAAE conference in Japan, the 2017 NBER Transporting Hydrocarbons and Economics of Energy Markets Meetings, and the seminar participants at the Federal Reserve Bank of Kansas City. This paper is part of the NBER Hydrocarbon Infrastructure Research Initiative supported by the Alfred P. Sloan Foundation. Navi Dhaliwal, Ruiyang Hu and Elena Ojeda provided excellent research assistance. This paper was previously circulated under the title “A macroeconomic analysis of lifting the U.S. crude oil export ban.” The views expressed herein are solely those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Dallas, the Federal Reserve Bank of Kansas City, the Federal Reserve System, or the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications.