Oilfield Services Companies' Response to Low Oil Prices

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TEACHERS' RETIREMENT SYSTEM of the STATE of ILLINOIS 2815 West Washington Street I P.O

Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Performed as Special Assistant Auditors for the Auditor General, State of Illinois Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Table of Contents Schedule Page(s) System Officials 1 Management Assertion Letter 2 Compliance Report Summary 3 Independent Accountant’s Report on State Compliance, on Internal Control over Compliance, and on Supplementary Information for State Compliance Purposes 4 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 8 Schedule of Findings Current Findings – State Compliance 10 Supplementary Information for State Compliance Purposes Fiscal Schedules and Analysis Schedule of Appropriations, Expenditures and Lapsed Balances 1 13 Comparative Schedules of Net Appropriations, Expenditures and Lapsed Balances 2 15 Comparative Schedule of Revenues and Expenses 3 17 Schedule of Administrative Expenses 4 18 Schedule of Changes in Property and Equipment 5 19 Schedule of Investment Portfolio 6 20 Schedule of Investment Manager and Custodian Fees 7 21 Analysis of Operations (Unaudited) Analysis of Operations (Functions and Planning) 30 Progress in Funding the System 34 Analysis of Significant Variations in Revenues and Expenses 36 Analysis of Significant Variations in Administrative Expenses 37 Analysis -

2021 Annual General Meeting and Proxy Statement 2020 Annual Report

2020 Annual Report and Proxyand Statement 2021 Annual General Meeting Meeting General Annual 2021 Transocean Ltd. • 2021 ANNUAL GENERAL MEETING AND PROXY STATEMENT • 2020 ANNUAL REPORT CONTENTS LETTER TO SHAREHOLDERS NOTICE OF 2021 ANNUAL GENERAL MEETING AND PROXY STATEMENT COMPENSATION REPORT 2020 ANNUAL REPORT TO SHAREHOLDERS ABOUT TRANSOCEAN LTD. Transocean is a leading international provider of offshore contract drilling services for oil and gas wells. The company specializes in technically demanding sectors of the global offshore drilling business with a particular focus on ultra-deepwater and harsh environment drilling services, and operates one of the most versatile offshore drilling fleets in the world. Transocean owns or has partial ownership interests in, and operates a fleet of 37 mobile offshore drilling units consisting of 27 ultra-deepwater floaters and 10 harsh environment floaters. In addition, Transocean is constructing two ultra-deepwater drillships. Our shares are traded on the New York Stock Exchange under the symbol RIG. OUR GLOBAL MARKET PRESENCE Ultra-Deepwater 27 Harsh Environment 10 The symbols in the map above represent the company’s global market presence as of the February 12, 2021 Fleet Status Report. ABOUT THE COVER The front cover features two of our crewmembers onboard the Deepwater Conqueror in the Gulf of Mexico and was taken prior to the COVID-19 pandemic. During the pandemic, our priorities remain keeping our employees, customers, contractors and their families healthy and safe, and delivering incident-free operations to our customers worldwide. FORWARD-LOOKING STATEMENTS Any statements included in this Proxy Statement and 2020 Annual Report that are not historical facts, including, without limitation, statements regarding future market trends and results of operations are forward-looking statements within the meaning of applicable securities law. -

To Arrive at the Total Scores, Each Company Is Marked out of 10 Across

BRITAIN’S MOST ADMIRED COMPANIES THE RESULTS 17th last year as it continues to do well in the growing LNG business, especially in Australia and Brazil. Veteran chief executive Frank Chapman is due to step down in the new year, and in October a row about overstated reserves hit the share price. Some pundits To arrive at the total scores, each company is reckon BG could become a take over target as a result. The biggest climber in the top 10 this year is marked out of 10 across nine criteria, such as quality Petrofac, up to fifth from 68th last year. The oilfield of management, value as a long-term investment, services group may not be as well known as some, but it is doing great business all the same. Its boss, Syrian- financial soundness and capacity to innovate. Here born Ayman Asfari, is one of the growing band of are the top 10 firms by these individual measures wealthy foreign entrepreneurs who choose to make London their operating base and home, to the benefit of both the Exchequer and the employment figures. In fourth place is Rolls-Royce, one of BMAC’s most Financial value as a long-term community and environmental soundness investment responsibility consistent high performers. Hardly a year goes past that it does not feature in the upper reaches of our table, 1= Rightmove 9.00 1 Diageo 8.61 1 Co-operative Bank 8.00 and it has topped its sector – aero and defence engi- 1= Rotork 9.00 2 Berkeley Group 8.40 2 BASF (UK & Ireland) 7.61 neering – for a decade. -

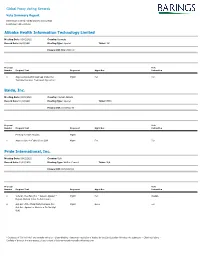

Global Proxy Voting Records

Global Proxy Voting Records Vote Summary Report Date range covered: 03/01/2021 to 03/31/2021 Location(s): All Locations Alibaba Health Information Technology Limited Meeting Date: 03/01/2021 Country: Bermuda Record Date: 02/23/2021 Meeting Type: Special Ticker: 241 Primary ISIN: BMG0171K1018 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction 1 Approve Revised Annual Cap Under the Mgmt For For Technical Services Framework Agreement Baidu, Inc. Meeting Date: 03/01/2021 Country: Cayman Islands Record Date: 01/28/2021 Meeting Type: Special Ticker: BIDU Primary ISIN: US0567521085 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction Meeting for ADR Holders Mgmt 1 Approve One-to-Eighty Stock Split Mgmt For For Pride International, Inc. Meeting Date: 03/01/2021 Country: USA Record Date: 12/01/2020 Meeting Type: Written Consent Ticker: N/A Primary ISIN: US74153QAJ13 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction 1 Vote On The Plan (For = Accept, Against = Mgmt For Abstain Reject; Abstain Votes Do Not Count) 2 Opt Out of the Third-Party Releases (For = Mgmt None For Opt Out, Against or Abstain = Do Not Opt Out) * Instances of "Do Not Vote" are normally owing to: - Share-blocking - temporary restriction of trading by the Sub-Custodian following vote submission - Client restrictions - Conflicts of Interest. For any queries, please contact [email protected] Global Proxy Voting Records Vote Summary Report Date range covered: 03/01/2021 to 03/31/2021 Location(s): All Locations The -

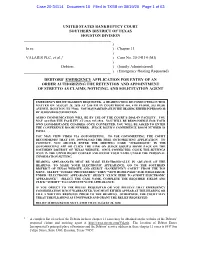

Chapter 11 ) VALARIS PLC, Et Al.,1 ) Case No

Case 20-34114 Document 16 Filed in TXSB on 08/19/20 Page 1 of 63 UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION ) In re: ) Chapter 11 ) VALARIS PLC, et al.,1 ) Case No. 20-34114 (MI) ) Debtors. ) (Jointly Administered) ) (Emergency Hearing Requested) DEBTORS’ EMERGENCY APPLICATION FOR ENTRY OF AN ORDER AUTHORIZING THE RETENTION AND APPOINTMENT OF STRETTO AS CLAIMS, NOTICING, AND SOLICITATION AGENT EMERGENCY RELIEF HAS BEEN REQUESTED. A HEARING WILL BE CONDUCTED ON THIS MATTER ON AUGUST 20, 2020 AT 2:00 PM IN COURTROOM 404, 4TH FLOOR, 515 RUSK AVENUE, HOUSTON, TX 77002. YOU MAY PARTICIPATE IN THE HEARING EITHER IN PERSON OR BY AUDIO/VIDEO CONNECTION. AUDIO COMMUNICATION WILL BE BY USE OF THE COURT’S DIAL-IN FACILITY. YOU MAY ACCESS THE FACILITY AT (832) 917-1510. YOU WILL BE RESPONSIBLE FOR YOUR OWN LONG-DISTANCE CHARGES. ONCE CONNECTED, YOU WILL BE ASKED TO ENTER THE CONFERENCE ROOM NUMBER. JUDGE ISGUR’S CONFERENCE ROOM NUMBER IS 954554. YOU MAY VIEW VIDEO VIA GOTOMEETING. TO USE GOTOMEETING, THE COURT RECOMMENDS THAT YOU DOWNLOAD THE FREE GOTOMEETING APPLICATION. TO CONNECT, YOU SHOULD ENTER THE MEETING CODE “JUDGEISGUR” IN THE GOTOMEETING APP OR CLICK THE LINK ON JUDGE ISGUR’S HOME PAGE ON THE SOUTHERN DISTRICT OF TEXAS WEBSITE. ONCE CONNECTED, CLICK THE SETTINGS ICON IN THE UPPER RIGHT CORNER AND ENTER YOUR NAME UNDER THE PERSONAL INFORMATION SETTING. HEARING APPEARANCES MUST BE MADE ELECTRONICALLY IN ADVANCE OF THE HEARING. TO MAKE YOUR ELECTRONIC APPEARANCE, GO TO THE SOUTHERN DISTRICT OF TEXAS WEBSITE AND SELECT “BANKRUPTCY COURT” FROM THE TOP MENU. -

E-Learning Most Socially Active Professionals

The World’s Most Socially Active Oil & Energy Professionals – September 2020 Position Company Name LinkedIN URL Location Size No. Employees on LinkedIn No. Employees Shared (Last 30 Days) % Shared (Last 30 Days) 1 Rystad Energy https://www.linkedin.com/company/572589 Norway 201-500 282 87 30.85% 2 Comerc Energia https://www.linkedin.com/company/2023479 Brazil 201-500 327 89 27.22% 3 International Energy Agency (IEA) https://www.linkedin.com/company/26952 France 201-500 426 113 26.53% 4 Tecnogera Geradores https://www.linkedin.com/company/2679062 Brazil 201-500 211 52 24.64% 5 Cenit Transporte y Logística de Hidrocarburos https://www.linkedin.com/company/3021697 Colombia 201-500 376 92 24.47% 6 Moove https://www.linkedin.com/company/12603739 Brazil 501-1000 250 59 23.60% 7 Evida https://www.linkedin.com/company/15252384 Denmark 201-500 246 57 23.17% 8 Dragon Products Ltd https://www.linkedin.com/company/9067234 United States 1001-5000 350 79 22.57% 9 Kenter https://www.linkedin.com/company/10576847 Netherlands 201-500 246 54 21.95% 10 Repower Italia https://www.linkedin.com/company/945861 Italy 501-1000 444 96 21.62% 11 Trident Energy https://www.linkedin.com/company/11079195 United Kingdom 201-500 283 60 21.20% 12 Odfjell Well Services https://www.linkedin.com/company/9363412 Norway 501-1000 250 52 20.80% 13 XM Filial de ISA https://www.linkedin.com/company/2570688 Colombia 201-500 229 47 20.52% 14 Energi Fyn https://www.linkedin.com/company/1653081 Denmark 201-500 219 44 20.09% 15 Society of Petroleum Engineers International https://www.linkedin.com/company/23356 United States 201-500 1,477 294 19.91% 16 Votorantim Energia https://www.linkedin.com/company/3264372 Brazil 201-500 443 86 19.41% 17 TGT Oilfield Services https://www.linkedin.com/company/1360433 United Arab Emirates201-500 203 38 18.72% 18 Motrice Soluções em Energia https://www.linkedin.com/company/11355976 Brazil 201-500 214 40 18.69% 19 GranIHC Services S.A. -

Halliburton Company

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A (RULE 14a-101) INFORMATION REQUIRED IN PROXY STATEMENT SCHEDULE 14A INFORMATION Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant Filed by a Party other than the Registrant Check the appropriate box: Preliminary Proxy Statement CONFIDENTIAL, FOR USE OF THE COMMISSION ONLY (AS PERMITTED BY RULE 14a-6(e)(2)) Definitive Proxy Statement Definitive Additional Materials Soliciting Material under §240.14a-12 HALLIBURTON COMPANY (Name of Registrant as Specified in its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): No fee required. Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: Fee paid previously with preliminary materials. Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: To Our Valued Shareholders: April 7, 2020 “Turning to 2020, . -

UK/Netherlands SNS Hackathon Output Report

UK/Netherlands SNS Hackathon Output Report April 2019 Contents Foreword ............................................................................................................................................................. 3 Executive Summary ............................................................................................................................................. 4 Introduction ......................................................................................................................................................... 4 How Does a Hackathon Event Work? ................................................................................................................... 5 Findings ............................................................................................................................................................... 6 Operator Challenges ............................................................................................................................................ 7 Operator 1: Shell .......................................................................................................................................... 7 Operator2: Oranje Nassau Energie B.V. ........................................................................................................ 8 Operator 3: Spirit Energy .............................................................................................................................. 9 Operator 4: Neptune Energy ...................................................................................................................... -

United States Bankruptcy Court Southern District of Texas Houston Division

Case 20-34114 Document 528 Filed in TXSB on 10/19/20 Page 1 of 58 UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION ) In re: ) Chapter 11 ) VALARIS PLC, et al.,1 ) Case No. 20-34114 (MI) ) Debtors. ) (Jointly Administered) ) GLOBAL NOTES, METHODOLOGY, AND SPECIFIC DISCLOSURES REGARDING THE DEBTORS’ SCHEDULES OF ASSETS AND LIABILITIES AND STATEMENTS OF FINANCIAL AFFAIRS Introduction Valaris plc (“Valaris”) and its debtor affiliates, as debtors and debtors in possession in the above-captioned chapter 11 cases (collectively, the “Debtors”), with the assistance of their advisors, have filed their respective Schedules of Assets and Liabilities (the “Schedules”) and Statements of Financial Affairs (the “Statements,” and together with the Schedules, the “Schedules and Statements”) with the United States Bankruptcy Court for the Southern District of Texas (the “Bankruptcy Court”), under section 521 of title 11 of the United States Code (the “Bankruptcy Code”), Rule 1007 of the Federal Rules of Bankruptcy Procedure (the “Bankruptcy Rules”), and Rule 1007-1 of the Bankruptcy Local Rules for the Southern District of Texas (the “Local Rules”). These Global Notes, Methodology, and Specific Disclosures Regarding the Debtors’ Schedules of Assets and Liabilities and Statements of Financial Affairs (the “Global Notes”) pertain to, are incorporated by reference in, and comprise an integral part of all of the Debtors’ Schedules and Statements. The Global Notes should be referred to, considered, and reviewed in connection with any review of the Schedules and Statements. The Schedules and Statements do not purport to represent financial statements prepared in accordance with Generally Accepted Accounting Principles in the United States (“GAAP”), nor are they intended to be fully reconciled with the financial statements of each Debtor. -

(2386 HK) Sinopec Refining, Chems, LNG Capex Tailwind

18 September 2018 Hong Kong EQUITIES Sinopec Engineering Group (2386 HK) 2386 HK Outperform Sinopec refining, chems, LNG capex tailwind Price (at 08:50, 18 Sep 2018 GMT) HK$8.14 Valuation HK$ 7.50-13.20 Key points - EV-EBITDA (Bear-Bull We are constructive on the earnings turnaround at Sinopec Engineering 12-month target HK$ 11.00 (SEG), albeit with below consensus estimates. Upside/Downside % +35.1 Order flow has positively surprised YTD, and we see material incremental 12-month TSR % +40.5 orders from Sinopec’s expansion plans in refining, chemicals, LNG. Volatility Index Low/Medium Our new HK$11.0 price target (prior HK$9.7) with 35% upside potential GICS sector Capital Goods implies 8x 2019 EV-EBITDA, 0.3x EV-Backlog, and 1.6x P/B. Market cap HK$m 36,044 Market cap US$m 4,594 An improved order backlog and revenue outlook for SEG Free float % 31 30-day avg turnover US$m 4.3 Number shares on issue m 4,428 Investment fundamentals Year end 31 Dec 2017A 2018E 2019E 2020E Revenue m 36,199 41,391 45,486 49,484 EBITDA m 1,859 3,285 3,955 4,408 EBITDA growth % -30.3 76.7 20.4 11.4 EBIT m 1,112 2,501 3,187 3,645 EBIT growth % -42.7 124.8 27.4 14.4 Reported profit m 1,703 2,417 2,749 3,071 Adjusted profit m 1,703 2,417 2,749 3,071 EPS rep Rmb 0.38 0.55 0.62 0.69 EPS rep growth % 2.0 41.9 13.7 11.7 EPS adj Rmb 0.38 0.55 0.62 0.69 EPS adj growth % 2.0 41.9 13.7 11.7 PER rep x 18.5 13.1 11.5 10.3 PER adj x 18.5 13.1 11.5 10.3 Source: Company data, Macquarie Research, September 2018 Total DPS Rmb 0.20 0.33 0.37 0.42 Total div yield % 2.8 4.6 5.2 5.8 1. -

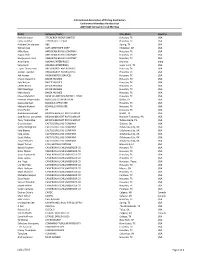

Conference Roster V4.Xlsx

International Association of Drilling Contractors Conference Attendees Handout List 2019 IADC Annual General Meeting Name Company Name City, State Country Niels Meissner 3T ENERGY GROUP LIMITED Houston, TX USA Lizzie Fletcher 7TH DISTRICT TEXAS Houston, TX USA Andrew Christensen ABS Spring, TX USA William Lee ALPS WIRE ROPE CORP Chidester, AR USA Mike Borg AMERICAN BLOCK COMPANY Houston, TX USA Rajani Shah AMERICAN BLOCK COMPANY Houston, TX USA Rocquee Johnson AMERICAN BLOCK COMPANY Houston, TX USA Arun Karle ASKARA ENTERPRISES Mumbai India Sang Karle ASKARA ENTERPRISES Sugar Land, TX USA Espen Thomassen AXESS NORTH AMERICA INC Houston, TX USA Jostein Tverdal AXESS NORTH AMERICA INC Houston, TX USA Jeff Hunter AXON ENERGY SERVICES Houston, TX USA Chuck Chauviere BAKER HUGHES Houston, TX USA Kyle Nelson BAKER HUGHES Houston, TX USA Lester Bruno BAKER HUGHES Houston, TX USA Matt Boerlage BAKER HUGHES Houston, TX USA Mike Bowie BAKER HUGHES Houston, TX USA Chase Mulvehill BANK OF AMERICA MERRILL LYNCH Houston, TX USA Herman Vizcarrondo BESTOLIFE CORPORATION Dallas, TX USA Jessica Bertsch BOSKALIS OFFSHORE Houston, TX USA Michele Richard BOSKALIS OFFSHORE Houston, TX USA Chris Parker BP Houston, TX USA Andrew Hernandez BRIDON‐BEKAERT ROPES GROUP Haslet, TX USA Jose Ramon Cervantes BRIDON‐BEKAERT ROPES GROUP Hanover Township, PA USA Tony Tarabochia BRIDON‐BEKAERT ROPES GROUP Wilkes‐Barre, PA USA Greg Hudson CACTUS DRILLING COMPANY Guthrie, OK USA Kathy Willingham CACTUS DRILLING COMPANY Oklahoma City, OK USA Kyle Blevins CACTUS DRILLING COMPANY -

Petrofac Limited

Petrofac Limited INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 June 2020 Petrofac Limited CONTENTS Group financial highlights 2 Business review 3 Interim condensed consolidated income statement 15 Interim condensed consolidated statement of comprehensive income 16 Interim condensed consolidated balance sheet 17 Interim condensed consolidated statement of cash flows 18 Interim condensed consolidated statement of changes in equity 19 Notes to the interim condensed consolidated financial statements 20 Appendices 40 Statement of Directors’ responsibilities 46 Shareholder information 47 US$2,103 million US$129 million Revenue EBITDA 1,2 Six months ended 30 June 2019: US$2,821 million Six months ended 30 June 2019: US$305 million US$21 million US$(78) million Business performance net profit 1,3 Reported net loss 3 Six months ended 30 June 2019: US$154 million Six months ended 30 June 2019: US$139 million profit nil 6.2 cents Interim dividend per share Diluted earnings per share 1,3 Six months ended 30 June 2019: 12.7 cents Six months ended 30 June 2019: 44.9 cents US$(13) million US$29 million Free cash flow 4 Net debt Six months ended 30 June 2019: US$123 million At 31 December 2019: US$15 million net cash US$6.2 billion 14% Backlog 6 Return on capital employed 1,5 At 31 December 2019: US$7.4 billion 12 months ended 30 June 2019: 26% 1 Business performance before exceptional items and certain 4 Free cash flow is defined as net cash flows generated from re-measurements. This measurement is shown by Petrofac operating activities and investing activities, less interest paid and as a means of measuring underlying business performance.