Lancaster City Council Phase 1: Retail Development Strategy Final

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Appendix 5 Fylde

FYLDE DISTRICT - APPENDIX 5 SUBSIDISED LOCAL BUS SERVICE EVENING AND SUNDAY JOURNEYS PROPOSED TO BE WITHDRAWN FROM 18 MAY 2014 LANCASTER - GARSTANG - POULTON - BLACKPOOL 42 via Galgate - Great Eccleston MONDAY TO SATURDAY Service Number 42 42 42 $ $ $ LANCASTER Bus Station 1900 2015 2130 SCOTFORTH Boot and Shoe 1909 2024 2139 LANCASTER University Gates 1912 2027 2142 GALGATE Crossroads 1915 2030 2145 CABUS Hamilton Arms 1921 2036 2151 GARSTANG Bridge Street 1926 2041 2156 CHURCHTOWN Horns Inn 1935 2050 2205 ST MICHAELS Grapes Hotel 1939 2054 2209 GREAT ECCLESTON Square 1943 2058 2213 POULTON St Chads Church 1953 2108 2223 BLACKPOOL Layton Square 1958 2113 2228 BLACKPOOL Abingdon Street 2010 2125 2240 $ - Operated on behalf of Lancashire County Council BLACKPOOL - POULTON - GARSTANG - LANCASTER 42 via Great Eccleston - Galgate MONDAY TO SATURDAY Service Number 42 42 42 $ $ $ BLACKPOOL Abingdon Street 2015 2130 2245 BLACKPOOL Layton Square 2020 2135 2250 POULTON Teanlowe Centre 2032 2147 2302 GREAT ECCLESTON Square 2042 2157 2312 ST MICHAELS Grapes Hotel 2047 2202 2317 CHURCHTOWN Horns Inn 2051 2206 2321 GARSTANG Park Hill Road 2059 2214 2329 CABUS Hamilton Arms 2106 2221 2336 GALGATE Crossroads 2112 2227 2342 LANCASTER University Gates 2115 2230 2345 SCOTFORTH Boot and Shoe 2118 2233 2348 LANCASTER Bus Station 2127 2242 2357 $ - Operated on behalf of Lancashire County Council LIST OF ALTERNATIVE TRANSPORT SERVICES AVAILABLE – Stagecoach in Lancaster Service 2 between Lancaster and University Stagecoach in Lancaster Service 40 between Lancaster and Garstang (limited) Blackpool Transport Service 2 between Poulton and Blackpool FYLDE DISTRICT - APPENDIX 5 SUBSIDISED LOCAL BUS SERVICE EVENING AND SUNDAY JOURNEYS PROPOSED TO BE WITHDRAWN FROM 18 MAY 2014 PRESTON - LYTHAM - ST. -

Lancaster Archaeological and Historical Society Research Group Newsletter

Lancaster Archaeological and Multum in parvo Historical Society http://lahs.archaeologyuk.org/ Research Group Newsletter orem ipsum dolor sit amet, consectetuer adipisci No. 2: August 2020 Welcome to the Research Group e-newsletter We received encouraging feedback from Society amount of research now being conducted online, members following the first issue of the e-newsletter news that the National Archives are allowing people in May 2020 which was much appreciated. The e- to download their digital resources free during the newsletter is open to all Society members and guest pandemic has been very welcome. If you have a authors should they be interested in publishing a brief Lancashire County Library ticket it is possible to letter, or a short article of 500-750 words on an access information online such as the Oxford archaeological or historical subject related to Dictionary of National Biography and several local Lancaster and surrounding areas. Longer articles are papers from the nineteenth century (with thanks to Dr published in Contrebis Michael Winstanley). As lockdown restrictions begin to ease, do not delay in taking advantage when The last five months have been a difficult time for research facilities re-open because with social researchers with the Covid-19 lockdown making distancing measures still in force, there are likely to face-to-face meetings impossible; archive, museum be appointment systems or time-limited visits and library services closed, and employees in many introduced. organisations working from home. Research can be a lonely occupation at the best of times so the surge in If you would like to join the Research Group or online virtual meetings has offered some welcome contribute to the e-newsletter, contact details are relief from social isolation. -

2005 No. 170 LOCAL GOVERNMENT, ENGLAND The

STATUTORY INSTRUMENTS 2005 No. 170 LOCAL GOVERNMENT, ENGLAND The County of Lancashire (Electoral Changes) Order 2005 Made - - - - 1st February 2005 Coming into force in accordance with article 1(2) Whereas the Boundary Committee for England(a), acting pursuant to section 15(4) of the Local Government Act 1992(b), has submitted to the Electoral Commission(c) recommendations dated October 2004 on its review of the county of Lancashire: And whereas the Electoral Commission have decided to give effect, with modifications, to those recommendations: And whereas a period of not less than six weeks has expired since the receipt of those recommendations: Now, therefore, the Electoral Commission, in exercise of the powers conferred on them by sections 17(d) and 26(e) of the Local Government Act 1992, and of all other powers enabling them in that behalf, hereby make the following Order: Citation and commencement 1.—(1) This Order may be cited as the County of Lancashire (Electoral Changes) Order 2005. (2) This Order shall come into force – (a) for the purpose of proceedings preliminary or relating to any election to be held on the ordinary day of election of councillors in 2005, on the day after that on which it is made; (b) for all other purposes, on the ordinary day of election of councillors in 2005. Interpretation 2. In this Order – (a) The Boundary Committee for England is a committee of the Electoral Commission, established by the Electoral Commission in accordance with section 14 of the Political Parties, Elections and Referendums Act 2000 (c.41). The Local Government Commission for England (Transfer of Functions) Order 2001 (S.I. -

Initial Template Document

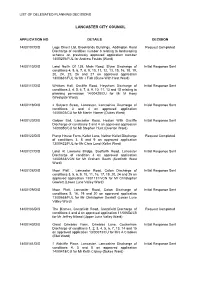

LIST OF DELEGATED PLANNING DECISIONS LANCASTER CITY COUNCIL APPLICATION NO DETAILS DECISION 14/00107/DIS Logs Direct Ltd, Brooklands Buildings, Addington Road Request Completed Discharge of condition number 6 relating to landscaping scheme on previously approved application number 14/00276/FUL for Andrew Foulds (Ward) 14/00110/DIS Land North Of 138, Main Road, Slyne Discharge of Initial Response Sent conditions 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 15, 16, 18, 19, 20, 24, 25, 26 and 27 on approved application 13/00831/FUL for Mr J Fish (Slyne With Hest Ward) 14/00117/DIS Whittam Hall, Oxcliffe Road, Heysham Discharge of Initial Response Sent conditions 3, 4, 5, 6, 7, 8, 9, 10, 11, 13 and 15 relating to planning permission 14/00428/CU for Mr M Hoey (Westgate Ward) 14/00119/DIS 2 Sulyard Street, Lancaster, Lancashire Discharge of Initial Response Sent conditions 3 and 4 on approved application 14/00403/CU for Mr Martin Horner (Dukes Ward) 14/00120/DIS Golden Ball, Lancaster Road, Heaton With Oxcliffe Initial Response Sent Discharge of conditions 3 and 4 on approved application 14/00050/CU for Mr Stephen Hunt (Overton Ward) 14/00122/DIS Pump House Farm, Kellet Lane, Nether Kellet Discharge Request Completed of conditions 3, 8 and 9 on approved application 13/00422/FUL for Mr Chris Lund (Kellet Ward) 14/00127/DIS Land At Lawsons Bridge, Scotforth Road, Lancaster Initial Response Sent Discharge of condition 4 on approved application 14/00633/VCN for Mr Graham Booth (Scotforth West Ward) 14/00128/DIS Moor Platt , Lancaster Road, Caton Discharge -

Der Europäischen Gemeinschaften Nr

26 . 3 . 84 Amtsblatt der Europäischen Gemeinschaften Nr . L 82 / 67 RICHTLINIE DES RATES vom 28 . Februar 1984 betreffend das Gemeinschaftsverzeichnis der benachteiligten landwirtschaftlichen Gebiete im Sinne der Richtlinie 75 /268 / EWG ( Vereinigtes Königreich ) ( 84 / 169 / EWG ) DER RAT DER EUROPAISCHEN GEMEINSCHAFTEN — Folgende Indexzahlen über schwach ertragsfähige Böden gemäß Artikel 3 Absatz 4 Buchstabe a ) der Richtlinie 75 / 268 / EWG wurden bei der Bestimmung gestützt auf den Vertrag zur Gründung der Euro jeder der betreffenden Zonen zugrunde gelegt : über päischen Wirtschaftsgemeinschaft , 70 % liegender Anteil des Grünlandes an der landwirt schaftlichen Nutzfläche , Besatzdichte unter 1 Groß vieheinheit ( GVE ) je Hektar Futterfläche und nicht über gestützt auf die Richtlinie 75 / 268 / EWG des Rates vom 65 % des nationalen Durchschnitts liegende Pachten . 28 . April 1975 über die Landwirtschaft in Berggebieten und in bestimmten benachteiligten Gebieten ( J ), zuletzt geändert durch die Richtlinie 82 / 786 / EWG ( 2 ), insbe Die deutlich hinter dem Durchschnitt zurückbleibenden sondere auf Artikel 2 Absatz 2 , Wirtschaftsergebnisse der Betriebe im Sinne von Arti kel 3 Absatz 4 Buchstabe b ) der Richtlinie 75 / 268 / EWG wurden durch die Tatsache belegt , daß das auf Vorschlag der Kommission , Arbeitseinkommen 80 % des nationalen Durchschnitts nicht übersteigt . nach Stellungnahme des Europäischen Parlaments ( 3 ), Zur Feststellung der in Artikel 3 Absatz 4 Buchstabe c ) der Richtlinie 75 / 268 / EWG genannten geringen Bevöl in Erwägung nachstehender Gründe : kerungsdichte wurde die Tatsache zugrunde gelegt, daß die Bevölkerungsdichte unter Ausschluß der Bevölke In der Richtlinie 75 / 276 / EWG ( 4 ) werden die Gebiete rung von Städten und Industriegebieten nicht über 55 Einwohner je qkm liegt ; die entsprechenden Durch des Vereinigten Königreichs bezeichnet , die in dem schnittszahlen für das Vereinigte Königreich und die Gemeinschaftsverzeichnis der benachteiligten Gebiete Gemeinschaft liegen bei 229 beziehungsweise 163 . -

The First 40 Years

A HISTORY OF LANCASTER CIVIC SOCIETY THE FIRST 40 YEARS 1967 – 2007 By Malcolm B Taylor 2009 Serialization – part 7 Territorial Boundaries This may seem a superfluous title for an eponymous society, so a few words of explanation are thought necessary. The Society’s sometime reluctance to expand its interests beyond the city boundary has not prevented a more elastic approach when the situation demands it. Indeed it is not true that the Society has never been prepared to look beyond the City boundary. As early as 1971 the committee expressed a wish that the Society might be a pivotal player in the formation of amenity bodies in the surrounding districts. It was resolved to ask Sir Frank Pearson to address the Society on the issue, although there is no record that he did so. When the Society was formed, and, even before that for its predecessor, there would have been no reason to doubt that the then City boundary would also be the Society’s boundary. It was to be an urban society with urban values about an urban environment. However, such an obvious logic cannot entirely define the part of the city which over the years has dominated the Society’s attentions. This, in simple terms might be described as the city’s historic centre – comprising largely the present Conservation Areas. But the boundaries of this area must be more fluid than a simple local government boundary or the Civic Amenities Act. We may perhaps start to come to terms with definitions by mentioning some buildings of great importance to Lancaster both visually and strategically which have largely escaped the Society’s attentions. -

St. Paul's Church, Scotforth

St. Paul’s Church, Scotforth Contents Summary 2 Our Vision 3 Who Is God Calling? 3 The Parish and Wider Community 4 Church Organization 7 The Church Community 8 Together we are stronger 10 Our Buildings 11 The Church 12 The Hala Centre 13 The Parish Hall 14 The Vicarage 15 The Church Finances 16 Our Schools 17 Our Links into the Wider Community 20 1 Summary St Paul’s Church Scotforth is a vibrant and accepting community in Lancaster. The church building is a landmark on the A6 south of the city centre, and the vicarage is adjacent in its own private grounds. Living here has many attractive features. We have our own outstanding C of E primary school nearby with which we have strong links. And very close to the parish we also find outstanding secondary schools, Ripley C of E academy and two top-rated grammar schools. In addition Lancaster’s two universities bring lively people and facilities to the area. Traveling to and from Scotforth has many possibilities. We rapidly connect to the M6 and to the west coast main train line. Our proximity to beautiful countryside keeps many residents happy to remain. We are close to the Lake District, the Yorkshire Dales, Bowland forest, Morecambe Bay, to mention just a few such attractions. Our Church is a welcoming and friendly place. Our central churchmanship is consistent with the lack of a central aisle in our unusual “pot” church building! Our regular services (BCP or traditional, in church or in the Hala Centre) use the Bible lectionary to encourage understanding and action, but we also are keen to develop innovative forms of worship. -

What Is a Boggart Hole?1 Simon Young ISI, Florence (Italy)

What is a Boggart Hole?1 Simon Young ISI, Florence (Italy) INTRODUCTION The boggart—a word of uncertain origins (OED, ‘Boggard, -art’; Nodal and Milner 1875, 126; Wright 1898–1905, I, 326)—was once a much feared bogey in the midlands and the north of England. By the nineteenth century it had come to be associated, above all, with what might be called a ‘greater Lancashire’: the County Palatine, the south Pennines and the northern fringes of Cheshire and Derbyshire. Relative to the amount of writing that survives, most of it from the 1800s and much in Lancashire dialect, the boggart is perhaps Britain’s most understudied supernatural creature. This is true of the nineteenth century (Thornber 1837, 38, 99–104 and 329–34; Harland and Wilkinson 1867, 49–62; 1873, 10–12 and 141– 42; Hardwick 1872, 124–42; Bowker 1883, 27–36, 52–58, 63–72, 77–82, 131–39, 152–58, 174–88, 212–20 and 238–42; McKay 1888), and of recent years (Billingsley 2007, 69–74; Turner-Bishop 2010; Roberts 2013, 95–105; Young 2014b). Boggart place-names have particularly been neglected. In fact, there is, to the best of the present writer’s knowledge, no study of boggart toponyms, despite the existence of tens of boggart place-names, many still in use today.2 1 I would like to thank John Billingsley, David Boardman, Ffion Dash, Anna Garrett, Richard Green, Denise Jagger, Stephen Lees, Wendy Lord, Eileen Ormand and the anonymous reviewer for help with the writing and with the improvement of this article. -

FINAL Lancs & S. Cumbria Christmas New Year 1920 POSTER Boxing

Boxing Day 2019 (26th December 2019) Blackburn with Darwen Pharmacy Address Tel Opening hours Beehive Pharmacy Beehive Trading Park Haslingden Road Blackburn BB1 2EE 01254 53585 11am-11pm Chapel Street Pharmacy 62 New Chapel Street Mill Hill Blackburn BB2 4DT 01254 55366 9am-12pm Karims Pharmacy Ltd 140 Mosley Street Blackburn Lancashire BB2 3RX 01254 680890 1pm - 4pm Morrisons Pharmacy Morrisons Store Railway Road Blackburn BB1 5AZ 01254 262159 10am-4pm Everest Pharmacy 21 Cemetery Road Darwen Lancashire BB3 2LZ 01254 777230 10am-4pm Market Street Pharmacy 29-31 Market Street Darwen Lancashire BB3 1PS 01254 873977 4pm-7pm Whalley Range Pharmacy 1 Whalley Range Blackburn Lanacashire BB1 6DX 01254 54988 10am-8pm Blackpool Pharmacy Address Tel Opening hours Whitegate Pharmacy Whitegate Health Centre 150 Whitegate Drive Blackpool FY3 9ES 01253 807 808 8am-9pm Boots Pharmacy 28-38 Bank Hey Street Blackpool Lancashire FY1 4TE 01253 622276 9am-5.30pm Morrisons Pharmacy Morrisons Supermarket Squires Gate Lane Blackpool FY4 2AY 01253 343377 10am-4pm Chorley & South Ribble Pharmacy Address Tel Opening hours Leyland Late Night Pharmacy 6 Hough Lane Leyland Lancs PR25 2SD 01772 905678 1pm-7pm Chorley Pharmacy 13-17 Peel Street Chorley Lancashire PR7 2EY 01257 754754 10am-7pm Boots Pharmacy 40 Hough Lane Leyland Lancashire PR25 2SA 01772 421169 10am-1pm Boots Pharmacy 219-221 Station Road Bamber Bridge Preston PR5 6LD 01772 335458 10am-4pm HBS Pharmacy 30 St Mary's Road Bamber Bridge Preston PR5 6TD 01772 620487 4pm-7pm Rowlands Pharmacy 22 Liverpool -

Local Government Boundary Commission for England Report

Local Government fir1 Boundary Commission For England Report No. 52 LOCAL GOVERNMENT BOUNDARY COMMISSION FOR ENGLAND REPORT NO.SZ LOCAL GOVERNMENT BOUNDARY COMMISSION FOR ENGLAND CHAIRMAN Sir Edmund .Compton, GCB.KBE. DEPUTY CHAIRMAN Mr J M Rankin,QC. - MEMBERS The Countess Of Albemarle,'DBE. Mr T C Benfield. Professor Michael Chisholm. Sir Andrew Wheatley,CBE. Mr P B Young, CBE. To the Rt Hon Roy Jenkins, MP Secretary of State for the Home Department PROPOSAL FOR REVISED ELECTORAL ARRANGEMENTS FOR THE CITY OF LANCASTER IN THE COUNTY OF LANCASHIRE 1. We, the Local Government Boundary Commission for England, having carried out our initial review of the electoral arrangements for the City of Lancaster in . accordance with the requirements of section 63 of, and of Schedule 9 to, the Local Government Act 1972, present our proposals for the future electoral arrangements for that City. 2. In accordance with the procedure laid down in section 60(1) and (2) of the 1972 Act, notice was given on 13 May 197^ that we were to undertake this review. This was incorporated in a consultation letter addressed to the Lancaster City Council, copies of which were circulated to the Lancashire County Council, Parish Councils and Parish Meetings in the district, the Members of Parliament for the constituencies concerned and the headquarters of the main political parties. Copies were also sent to the editors of local newspapers circulating in the area and of the local government press. Notices inserted in the local press announced the start of the review and invited comments from members of the public and from any interested bodies, 3- Lancaster City Council were invited to prepare a draft scheme of representa- tion for our consideration. -

Delegated Planning Decisions PDF 18 KB

LIST OF DELEGATED PLANNING DECISIONS LANCASTER CITY COUNCIL APPLICATION NO DETAILS DECISION 09/01114/FUL Littledale Scout Campsite, Littledale Road, Brookhouse Application Permitted Erection of a toilet block for Lonsdale District Scout Council (Lower Lune Valley Ward) 09/01162/FUL Gardenia Lodge, Haverbreaks Road, Lancaster Single Application Permitted storey rear extension and two storey side extension for Mr & Mrs Gary Hammond (Scotforth West Ward) 10/00008/DIS Orchard House, Sunnyside Lane, Lancaster Discharge Request Completed of conditions nos 4 and 7 on application 07/00519 for Mr And Mrs Martin (Castle Ward) 10/00057/FUL Old School House, Stoney Lane, Ellel Erection of Application Permitted replacement dwelling and replacement garage/light industrial workshop for Mr K Foxcroft (Ellel Ward) 10/00063/FUL The Cedars, Starbank, Bay Horse Erection of a porch Application Refused and first floor balcony above to the north elevation, new rooflight and window to the southern elevation for Mr And Mrs P Mulvenna (Ellel Ward) 10/00070/FUL 79 Sulby Drive, Lancaster, Lancashire Erection of single Application Refused storey extension to the side for Mr Al-Khaled (Scotforth West Ward) 10/00097/FUL Restarigg Farm, Kirkby Lonsdale Road, Arkholme Application Permitted Installation of a 5kW domestic scale Micro Wind Turbine on a 10m mast for Mr Robert Walker (Kellet Ward) 10/00121/FUL Silverdale Golf Club, Red Bridge Lane, Silverdale Application Permitted Renewal of temporary consent for a storage container for a further two years for Silverdale Golf -

Quernmore Park Hall Estate Lancaster, Lancashire

Quernmore Park Hall Estate Lancaster, Lancashire Quernmore Park Hall Estate Lancaster, Lancashire Georgian splendour in the Lune Valley 1 M6 (Jct 34) 2 miles ◆ Lancaster 4 miles ◆ Lake District 20 miles ◆ Preston 25 ⁄2 miles ◆ Blackburn 39 miles 1 Manchester 57 ⁄2 miles ◆ Liverpool 61 miles ◆ (Distances and times approximate) Accommodation and amenities Lot 1 - Quernmore Park Hall (20.598 acres) Portico ◆ Entrance hall ◆ Main hall ◆ Dining room ◆ Billiard room ◆ Drawing room ◆ Sitting room ◆ Chapel ◆ Office Rear hall ◆ Study ◆ Kitchen/Breakfast room ◆ Garden room ◆ Victorain Kitchen ◆ Bakery ◆ Cinema ◆ Extensive cellars Laundry ◆ Banqueting kitchens ◆ Wine cellars ◆ Boiler rooms Master bedroom suite with 2 dressing rooms ◆ 6 principal bedrooms ◆ 6 further bedrooms ◆ 3 further bathrooms Garaging ◆ Summer house ◆ Workshops ◆ Immaculate landscaped gardens and grounds ◆ Woodland Carriage driveway ◆ Outbuildings 2 integral cottages Lot 2 - Gardener’s cottage (2.211 acres) Private entrance ◆ Hall ◆ Sitting room ◆ Kitchen ◆ Utility room ◆ 2 Bedrooms ◆ Bathroom ◆ Shower room Walled Garden Lot 3 - Lodge cottage (0.42 acres) Sitting room ◆ Kitchen ◆ Bedroom ◆ Shower room ◆ Courtyard ◆ Garden For Sale Freehold In all about 9.4 hectares (23.23 acres) (TM/TW/273324) The house is approached off Quernmore Road, past the Lodge cottage to the electric gates which mark the beginning of the private driveway. The driveway continues through beautifully landscaped grounds, a mass of rhododendrons and fine examples of magnificent hard woods which create a secluded setting for this fine house. There are extensive lawns to the south and east of the house, and the approach to the property is dominated by a magnificent cedar. The hall benefits from a mass of original features.