West Africa's Mining Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ore Genesis and Modelling of the Sadiola Hill Gold Mine, Mali Geology Honours Project

ORE GENESIS AND MODELLING OF THE SADIOLA HILL GOLD MINE, MALI GEOLOGY HONOURS PROJECT Ramabulana Tshifularo Student number: 462480 Supervisor: Prof Kim A.A. Hein Acknowledgements I would like to thank my supervisor, Prof. Kim Hein for giving me the opportunity to be part of her team and, for helping and motivating me during the course of the project. Thanks for your patience, constructive comments and encouragement. Thanks to my family and my friends for the encouragements and support. Table of contents Abstract……………………………………………………………………………………..i Chapter: 1 1.1 Introduction……………………………………………………..........................................1 1.2 Location and Physiography……………………………………………………………...2 1.3 Aims and Objectives…………………………………………………………………….3 1.4 Abbreviations and acronyms…………………………………………………………….3 Chapter 2 2.1 Regional Geology………………………………………………………………………..4 2.1.1 Geology of the West African Craton…………………………………………………..4 2.1.2 Geology of the Kedougou-Kéniéba Inlier……………………………………………..5 2.2 Mine geology…………………………………………………………………………….6 Lithology………………………………………………………………………………8 Structure……………………………………………………………………………….8 Metamorphism………………………………………………………………………...9 Gold mineralisation and metallogenesis………………………………………………9 2.4 Previously suggested genetic models…………………………………………………..10 Chapter3: Methodology…………………………………………………………………....11 Chapter 4: Host rocks in drill core…......................................................................................13 4.1 Drill core description….........................................................................................................13 -

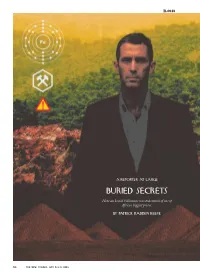

4C Buried Secrets

R-0048 a reporter at laRgE bURiEd sEcrets How an Israeli billionaire wrested control of one of Africa’s biggest prizes. bY paTRick radden keefE 50 THE NEW YORKER, JULY 8 & 15, 2013 TNY—2013_07_08&15—PAGE 50—133SC.—Live art r23707—CritiCAL PHOTOGRAPH TO BE WATCHED THROUGHOUT THE ENTIRE PRESS run—pLEASE PULL KODAK APPROVAL PROOF F0R PRESS COLOR GUID- ANCE 4C ne of the world’s largest known de- As wealthy countries confront the posits of untapped iron ore is buried prospect of rapidly depleting natural re- insideO a great, forested mountain range in sources, they are turning, increasingly, the tiny West African republic of Guinea. to Africa, where oil and minerals worth In the country’s southeast highlands, far trillions of dollars remain trapped in the from any city or major roads, the Siman- ground. By one estimate, the continent dou Mountains stretch for seventy miles, holds thirty per cent of the world’s min- looming over the jungle floor like a giant eral reserves. Paul Collier, who runs the dinosaur spine. Some of the peaks have Center for the Study of African Econo- nicknames that were bestowed by geolo- mies, at Oxford, has suggested that “a gists and miners who have worked in the new scramble for Africa” is under way. area; one is Iron Maiden, another Metal- Bilateral trade between China and Af- lica. Iron ore is the raw material that, once rica, which in 2000 stood at ten billion smelted, becomes steel, and the ore at Si- dollars, is projected to top two hundred mandou is unusually rich, meaning that billion dollars this year. -

New Records of the Togo Toad, Sclerophrys Togoensis, from South-Eastern Ivory Coast

Herpetology Notes, volume 12: 501-508 (2019) (published online on 19 May 2019) New records of the Togo Toad, Sclerophrys togoensis, from south-eastern Ivory Coast Basseu Aude-Inès Gongomin1, N’Goran Germain Kouamé1,*, and Mark-Oliver Rödel2 Abstract. Reported are new records of the forest toad, Sclerophrys togoensis, from south-eastern Ivory Coast. A small population was found in the rainforest of Mabi and Yaya Classified Forests. These forests and Taï National Park in the western part of the country are the only known and remaining Ivorian habitats of this species. Sclerophrys togoensis is confined to primary and slightly degraded rainforest. Known sites should be urgently and effectively protected from further forest loss. Keywords. Amphibia, Anura, Bufonidae, Conservation, Distribution, Mabi/Yaya Classified Forests, Upper Guinea forest Introduction In Ivory Coast the known records of S. togoensis are from the Cavally and Haute Dodo Classified Forests The toad Sclerophrys togoensis (Ahl, 1924) has been (Rödel and Branch, 2002), and the Taï National Park described from Bismarckburg in Togo (Ahl, 1924). Apart and its surroundings (e.g. Ernst and Rödel, 2006; Hillers from a parasitological study (Bourgat, 1978), no recent et al., 2008), all situated in the westernmost part of the records are known from that country (Ségniagbeto et al., country (Fig. 1). During a decade of conflict, both 2007; Hillers et al., 2009). Further records have been classified forests have been deforested (P.J. Adeba, pers. published from southern Ghana (Kouamé et al., 2007; comm.), thus restricting the species known Ivorian range Hillers et al., 2009), western Ivory Coast (e.g. -

The Politics Behind the Ebola Crisis

The Politics Behind the Ebola Crisis Africa Report N°232 | 28 October 2015 International Crisis Group Headquarters Avenue Louise 149 1050 Brussels, Belgium Tel: +32 2 502 90 38 Fax: +32 2 502 50 38 [email protected] Table of Contents Executive Summary ................................................................................................................... i Recommendations..................................................................................................................... iii I. Introduction ..................................................................................................................... 1 II. Pre-epidemic Situation ..................................................................................................... 3 A. Liberia ........................................................................................................................ 4 B. Sierra Leone ............................................................................................................... 5 C. Guinea ........................................................................................................................ 7 III. How Misinformation, Mistrust and Myopia Amplified the Crisis ................................... 8 A. Misinformation and Hesitation ................................................................................. 8 B. Extensive Delay and its Implications ........................................................................ 9 C. Quarantine and Containment ................................................................................... -

Unintended Consequences of the 'Bushmeat Ban' in West Africa During the 2013–2016 Ebola Virus Disease Epidemic

King’s Research Portal DOI: 10.1016/j.socscimed.2017.12.028 Document Version Publisher's PDF, also known as Version of record Link to publication record in King's Research Portal Citation for published version (APA): Bonwitt, J., Dawson, M., Kandeh, M., Ansumana, R., Sahr, F., Brown, H., & Kelly, A. H. (2018). Unintended consequences of the ‘bushmeat ban’ in West Africa during the 2013–2016 Ebola virus disease epidemic. Social Science & Medicine, 200, 166-173. https://doi.org/10.1016/j.socscimed.2017.12.028 Citing this paper Please note that where the full-text provided on King's Research Portal is the Author Accepted Manuscript or Post-Print version this may differ from the final Published version. If citing, it is advised that you check and use the publisher's definitive version for pagination, volume/issue, and date of publication details. And where the final published version is provided on the Research Portal, if citing you are again advised to check the publisher's website for any subsequent corrections. General rights Copyright and moral rights for the publications made accessible in the Research Portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognize and abide by the legal requirements associated with these rights. •Users may download and print one copy of any publication from the Research Portal for the purpose of private study or research. •You may not further distribute the material or use it for any profit-making activity or commercial gain •You may freely distribute the URL identifying the publication in the Research Portal Take down policy If you believe that this document breaches copyright please contact [email protected] providing details, and we will remove access to the work immediately and investigate your claim. -

Fighting Ebola: a Strategy for Action

FIGHTING EBOLA: A STRATEGY FOR ACTION Vera Songwe, Nonresident Senior Fellow, Africa Growth Initiative THE PRIORITY Despite these overwhelming numbers, prog- ress is being made in the fight against these African populations continue to suffer under diseases. For example, malaria mortality rates in the heavy burden of disease despite overall sus- children in Africa were reduced by an estimat- tained increases in income levels over the last ed 54 percent between 2002 and 2012. Since decade. Three major diseases are among those 2000, there has been a 49 percent reduction responsible for health crises: malaria, HIV/AIDS in the overall malaria mortality rates in Africa. and tuberculosis, and, in 2014, the Ebola virus For HIV, by the end of 2012, about 68 percent emerged as a fourth virus with pandemic po- of eligible persons were receiving antiretroviral tential. treatment, an increase of more than 90 percent since 2009 (UNAIDS 2013). In 2012, for example, 80 percent of the estimat- ed 207 million malaria cases worldwide were However, 2014 in West Africa will be remem- found in Africa, and 90 percent of the estimat- bered not for progress made in combatting in- ed 627,000 global malaria deaths occurred in fectious diseases but as the year the Ebola virus Africa. On average, malaria kills a child every crippled three countries on the continent and minute, of which 90 percent occur among Afri- inflicted economic damage to many others. can children. Malaria-related anemia is estimat- The 20th Ebola outbreak globally has captured ed to cause thousands of deaths a year—and the attention of the world like none of the oth- for countries with endemic malaria, it is estimat- ers that have preceded it and like no other dis- ed that there is a 1.3 percentage point loss in ease has in recent history. -

The Mineral Industry of Mali in 1998

THE MINERAL INDUSTRY OF MALI By Philip M. Mobbs Gold was the most economically significant mineral the area encompassing the Kéniéba gold district and the commodity produced in Mali during 1998. Gold production exploitation permits at Loulo and Sadiola included Afko Corp. from the Sadiola Hill Mine, the Syama Mine, and artisanal Mali, a subsidiary of Afko Korea Inc., on a Kéniéba area production reached an estimated 25 metric tons. Mali was tied property and African Goldfields Corp., a subsidiary of African for third with Zimbabwe on the list of African gold producers, Selection Mining Corp. of Canada, on the Kofi and the Metedia after South Africa and Ghana. Despite 1998 being a difficult Est concessions. Exploration on the Djlimagara property year for mining companies to raise capital, gold exploration continued as Anglogold (42.5%) joined the venture of Barrick continued during the year in the Birimian Series greenstone Gold Corp. of Canada (42.5%) and the Government (15%). belts in the southern and southwestern parts of the country. Emerging Africa Gold (EAG) Inc. of Canada explored the The gross domestic product (GDP) of landlocked Mali was Mankouke West, the Kourou, and the Siribaya permits. The $2.5 billion in 1997, the latest year for which data are joint venture of Emerging African Gold (75%) and Geo-L of available. The agriculture sector contributed nearly 50% to the Russia (25%) held the Koulo permit. Golden Eagle Mining GDP. Gold accounted for about 36% of the country’s 1997 Ltd. was earning a percentage of African Selection Mining’s exports of $562 million. -

SHEINI+FISCALS+PAPER.Pdf

NOVEMBER, 2016 Avenue D, Hse. No. 119 D, North Legon P. O. Box CT2121 Cantonment, A POLICY BRIEF ON Accra-Ghana Tel: 030-290 0730 THE POTENTIAL FISCAL CONTRIBUTION facebook: Africa Centre for Energy Policy SPONSORED BY: OF THE SHEINI IRON ORE DEPOSITS IN twitter@AcepPower www.acepghana.com NORTHERN GHANA Executive Summary In the wake of increasing global economic challenges amidst unprecedented political events that may have significant impact on the world economies, Ghana is again blessed with an iron ore mine which is yet to be developed. The mine has the potential to expand the country’s economic progress and have trickling down effects of social progress and sustainable development for its peoples. It therefore becomes imperative to understand the extent of fiscal impacts that Ghana’s Sheini iron ore project is likely to bring. It is against this backdrop that the Africa Centre for Energy Policy (ACEP), through its partnership with WACAM under the auspices of OSIWA, undertook this fiscal benchmarking study. The approach to the study was quantitative. Using an excel fiscal model, the Sheini iron ore project was situated within the geological and project context of Guinea’s Simandou iron ore project to compare Ghana’s mining fiscal policy against the fiscal provisions of the contract between the Government of Guinea and Simfer S.A. The purpose was to determine the level of fiscal convergence between the two projects and use findings as an important guide for improving on the fiscal take from Ghana’s Sheini iron ore project. The following were the key findings about the competitiveness of Ghana’s mining fiscal terms and how equitable they are in ensuring that the government and its people benefit from the mining sector: From Government Perspective 1. -

Issue 4 (December, 2019)

Geological Society of Africa Newsletter Volume 9 - Issue 4 (December, 2019) Since the Nobel prize was established, 27 African and African-born persons and African organizations got it. YES Africa can do it !!! Stories inside the issue Africa and Nobel prize CAG28 is approaching Toward a better communication Edited by Tamer Abu-Alam Editor of the GSAf Newsletter In the issue GSAF MATTERS 1 KNOW AFRICA (COVER STORY) 10 GEOLOGY COMIC 11 GEOLOGICAL EXPRESSIONS 11 AFRICAN GEOPARK AND GEOHERITAGE 13 AFRICA'S NOBEL PRIZE WINNERS: A LIST 14 NEWS 23 LITERATURE 30 OPPORTUNITIES 38 CONTACT THE COUNCIL 42 Geological Society of Africa – Newsletter Volume 9 – Issue 4 December 2019 © Geological Society of Africa http://gsafr.org Temporary contact: [email protected] GSAf MATTERS Toward a better and a faster communication among the African community of Geosciences By Tamer Abu-Alam (GSAf newsletter editor and information officer) Information and news should be communicated in a faster way than a newsletter. For example, a deadline to apply for a scholarship can be easily missed if it is not posted to the community at a proper time. As a result, and for better and faster communication among the geological society of Africa, the GSAf will use a Gmail group ([email protected]) to facilitate the communication between society members. Some advice and rules: Since any member can post and all the members will receive your message, please do not overload the society by un-related news. Post only important news that wants immediate action from members. Improper messages can lead its owner to be blocked from posting. -

Appraisal Report Relating to the Above-Mentioned Project

AFRICAN DEVELOPMENT BANK AFRICAN DEVELOPMENT FUND ADB/BD/WP/2014/159 ADF/BD/WP/2014/108 26 September 2014 Prepared by: OSHD Original: English Probable Date of Board Presentation 1st October 2014 FOR CONSIDERATION MEMORANDUM TO : THE BOARDS OF DIRECTORS FROM : Cecilia AKINTOMIDE Secretary General SUBJECT : MULTINATIONAL- EBOLA SECTOR BUDGET SUPPORT - FIGHT BACK PROGRAMME (EFBP)* ADF LOAN OF UA 67.2 MILLION TSF LOAN OF UA 12.6 MILLION ADF GRANT OF UA 17.6 MILLION TSF GRANT OF UA 2.8 MILLION Please find attached the Appraisal Report relating to the above-mentioned project. The Outcome of Negotiations and draft Resolutions will be submitted to you as an addendum. Attach: Cc: The President *Questions on this document should be referred to: Mr. K. J. LITSE Officer-In-Charge/Director ORVP/ORWA Extension 4047 Ms. A. SOUCAT Director OSHD Extension 2046 Mr. S. TAPSOBA Director ORFS Extension 2075 Mr. F. ZHAO Division Manager OSHD.3 Extension 2117 Mr. F. SERGENT Task Manager OSHD.3 Extension 1519 Mr. I. SANOGO Co-Task Manager OSHD.3 Extension 4206 SCCD:F.S. AFRICAN DEVELOPMENT BANK GROUP MUTINATIONAL EBOLA SECTOR BUDGET SUPPORT- FIGHT BACK PROGRAMME (EFBP) COUNTRIES: THE REPUBLICS OF CÔTE D’IVOIRE, GUINEA, LIBERIA AND SIERRA LEONE APPRAISAL REPORT Date: September 2014 Team Leader: Fabrice Sergent, Chief Health Analyst, OSHD 3 Co-Team Leader: I. Sanogo, Principal Health Specialist, OSHD.3 Team Members: Ms. M. Sharan, Senior Gender Specialist, OSHD.3 Mr. V. Durairaj, Chief Health Insurance & Social protection officer, OSHD.3 Mr. J. Murara, Chief Poverty Alleviation Officer, OSHD.1 Ms. C. -

Investing in the Minerals Industry in Liberia

ANDS, MIN L ES F O & Y GICAL SU E R LO RV N O E T E Y E S G I R G N I Y M R E IA P R UB E LIC OF LIB Investing in the minerals industry in Liberia liberia No4 cover.indd 1 21/01/2016 09:51:14 Investing in the minerals industry in Liberia: ▪▪ Extensive Archean and Proterozoic terranes highly prospective for many metals and industrial minerals, but detailed geology poorly known. ▪▪ Gold, iron ore and diamonds widespread, with new mines opened since 2013 and other projects in the pipeline. ▪▪ Known potentially economic targets for diamonds, base metals, manganese, bauxite, kyanite, phosphate, etc. ▪▪ Little modern exploration carried out for most mineral commodities with the exception of gold and iron ore. ▪▪ National datasets for geology, airborne geophysics and mineral occurrences available in digital form. ▪▪ Modern mineral licensing system. Introduction The Republic of Liberia is located in West Africa, in Liberia. Furthermore, Liberia is richly endowed bordered by Sierra Leone, Guinea, Côte d’Ivoire with natural resources, including minerals, water and to the south-west by the Atlantic Ocean and forests, and has a climate favourable to (Figure 1). With a land area of about 111 000 km2 agriculture. Since the cessation of hostilities the and a population of nearly 4.1 million much of country has made strenuous efforts to strengthen Liberia is sparsely populated comprising rolling its mineral and agricultural industries, mostly plateaux and low mountains away from a narrow timber and rubber. flat coastal plain. The climate is typically tropical, hot and humid at all times, with most rain falling Mineral resources, especially iron ore, have in the in the summer months. -

Key Biodiversity Areas Identification in the Upper Guinea Forest Biodiversity Hotspot

JoTT COMMUNI C ATION 4(8): 2745–2752 Key Biodiversity Area Special Series Key Biodiversity Areas identification in the Upper Guinea forest biodiversity hotspot O.M.L. Kouame 1, N. Jengre 2, M. Kobele 3, D. Knox 4, D.B. Ahon 5, J. Gbondo 6, J. Gamys 7, W. Egnankou 8, D. Siaffa 9, A. Okoni-Williams 10 & M. Saliou 11 1 4744 Kenmore ave # 202, Alexandria, VA, 22304, USA 2 Hse No. 36 Abotsi Street, East Legon P. O. Box KA 9714, Airport Accra 3,11 Guinee Ecologie, 210 DI 501 Dixinn, PoB:3266 Conakry, Guinea 4 The Wharton School, University of Pennsylvania, 3730 Walnut Street, Philadelphia, PA 19104, USA 5 22 BP 918 Abidjan 22 Côte d’Ivoire 6 150 Princeton Arms South II, East Windsor, N.J 08512, USA 7 Conservation International-Liberia, Back Road, Congo Town, Monrovia, Liberia 8 SOS-FORETS, 22 BP 918 Abidjan 22 Côte d’Ivoire 9 11B Becklyn Drive, Off Main Motor Road, Congo Cross, Freetown, Sierra Leone 10 Fourah Bay College, University of Sierra Leone PMB Freetown, Sierra Leone Email: 1 [email protected] (corresponding author), 2 [email protected], 3 [email protected], 4 [email protected], 5 [email protected], 6 [email protected], 7 [email protected], 8 [email protected], 9 [email protected], 10 [email protected], 11 [email protected] Date of publication (online): 06 August 2012 Abstract: Priority-setting approaches and tools are commons ways to support the Date of publication (print): 06 August 2012 rapid extinction of species and their habitats and the effective allocation of resources ISSN 0974-7907 (online) | 0974-7893 (print) for their conservation.