The Wealth Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

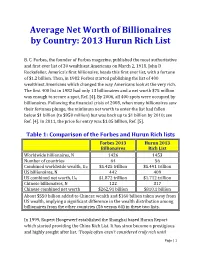

Average Net Worth of Billionaires by Country: 2013 Hurun Rich List

Average Net Worth of Billionaires by Country: 2013 Hurun Rich List B. C. Forbes, the founder of Forbes magazine, published the most authoritative and first ever list of 30 wealthiest Americans on March 2, 1918. John D Rockefeller, America’s first billionaire, heads this first ever list, with a fortune of $1.2 billion. Then, in 1982 Forbes started publishing the list of 400 wealthiest Americans which changed the way Americans look at the very rich. The first 400 list in 1982 had only 13 billionaires and a net worth $75 million was enough to secure a spot, Ref. [4]. By 2006, all 400 spots were occupied by billionaires. Following the financial crisis of 2008, when many billionaires saw their fortunes plunge, the minimum net worth to enter the list had fallen below $1 billion (to $950 million) but was back up to $1 billion by 2010; see Ref. [4]. In 2011, the price for entry was $1.05 billion, Ref. [5]. Table 1: Comparison of the Forbes and Hurun Rich lists Forbes 2013 Hurun 2013 Billionaires Rich List Worldwide billionaires, N 1426 1453 Number of countries 64 56 Combined worldwide wealth, UN $5.425 trillion $5.491 trillion US billionaires, N 442 409 US combined net worth, UN $1.872 trillion $1.712 trillion Chinese billionaires, N 122 317 Chinese combined net worth $262.91 billion $810.1 billion About $550 billion added to Chinese wealth and $160 billion taken away from US wealth, implying a significant difference in the wealth distribution among billionaires from the other countries (56 versus 64) in these two lists. -

Former Fellows Biographical Index Part

Former Fellows of The Royal Society of Edinburgh 1783 – 2002 Biographical Index Part Two ISBN 0 902198 84 X Published July 2006 © The Royal Society of Edinburgh 22-26 George Street, Edinburgh, EH2 2PQ BIOGRAPHICAL INDEX OF FORMER FELLOWS OF THE ROYAL SOCIETY OF EDINBURGH 1783 – 2002 PART II K-Z C D Waterston and A Macmillan Shearer This is a print-out of the biographical index of over 4000 former Fellows of the Royal Society of Edinburgh as held on the Society’s computer system in October 2005. It lists former Fellows from the foundation of the Society in 1783 to October 2002. Most are deceased Fellows up to and including the list given in the RSE Directory 2003 (Session 2002-3) but some former Fellows who left the Society by resignation or were removed from the roll are still living. HISTORY OF THE PROJECT Information on the Fellowship has been kept by the Society in many ways – unpublished sources include Council and Committee Minutes, Card Indices, and correspondence; published sources such as Transactions, Proceedings, Year Books, Billets, Candidates Lists, etc. All have been examined by the compilers, who have found the Minutes, particularly Committee Minutes, to be of variable quality, and it is to be regretted that the Society’s holdings of published billets and candidates lists are incomplete. The late Professor Neil Campbell prepared from these sources a loose-leaf list of some 1500 Ordinary Fellows elected during the Society’s first hundred years. He listed name and forenames, title where applicable and national honours, profession or discipline, position held, some information on membership of the other societies, dates of birth, election to the Society and death or resignation from the Society and reference to a printed biography. -

Frank Knight 1933-2007 After Receiving His Ph.D

Frank Knight 1933-2007 After receiving his Ph.D. from Princeton University in 1959, Frank Knight joined the mathematics department of the University of Minnesota. Frank liked Minnesota; the cold weather proved to be no difficulty for him since he climbed in the Rocky Mountains even in the winter time. But there was one problem: airborne flour dust, an unpleasant output of the large companies in Minneapolis milling spring wheat from the farms of Minnesota. Frank discovered that he was allergic to flour dust and decided that he would try to move to another location. His research was already recognized as important. His first four papers were published in the Illinois Journal of Mathematics and the Transactions of the American Mathematical Society. At that time, J.L. Doob was one of the editors of the Illinois Journal and attracted some of the best papers in probability theory to the journal including some of Frank's. He was hired by Illinois and served on its faculty from 1963 until his retirement in 1991. After his retirement, Frank continued to be active in his research, perhaps even more active since he no longer had to grade papers and carefully prepare his classroom lectures as he had always done before. In 1994, Frank was diagnosed with Parkinson's disease. For many years, this did not slow him down mathematically. He also kept physically active. At first, his health declined slowly but, in recent years, more rapidly. He died on March 19, 2007. Frank Knight's contributions to probability theory are numerous and often strikingly creative. -

China Consumer Close-Up

January 13, 2015 The Asian Consumer: A new series Equity Research China Consumer Close-up The who, what and why of China’s true consumer class Few investing challenges have proven more elusive than understanding the Chinese consumer. Efforts to translate the promise of an emerging middle class into steady corporate earnings have been uneven. In the first of a new series on the Asian consumer, we seek to strip the problem back to the basics: Who are the consumers with spending power, what drives their consumption and how will that shift over time? The result is a new approach that yields surprising results. Joshua Lu Goldman Sachs does and seeks to do business with +852-2978-1024 [email protected] companies covered in its research reports. As a result, Goldman Sachs (Asia) L.L.C. investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Sho Kawano Investors should consider this report as only a single factor +81(3)6437-9905 [email protected] Goldman Sachs Japan Co., Ltd. in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Becky Lu Appendix, or go to www.gs.com/research/hedge.html. +852-2978-0953 [email protected] Analysts employed by non- US affiliates are not registered/ Goldman Sachs (Asia) L.L.C. qualified as research analysts with FINRA in the U.S. January 13, 2015 Asia Pacific: Retail Table of contents PM Summary: A holistic view of the Asian consumer 3 China’s cohort in a regional context (a preview of India and Indonesia) 8 What they are buying and what they will buy next: Tracking 7 consumption desires 11 Seven consumption desires in focus 14 1. -

The Chinese Luxury Traveller 2018 Executive Summary

VIEW from ILTM REPORT THE CHINESE LUXURY TRAVELLER 2018 EXECUTIVE SUMMARY Photo by Yiran Ding VIEW from ILTM REPORT FOREWORD The Hurun Research Institute and ILTM China have joined forces to release The Chinese Luxury Traveller 2018 for the eight successive year. The report is based on deep research into travel preferences and consumption among Chinese high-end travellers, and the trends expected to arise in future. The data behind the research are global high-end travel industry leader, drawn from the Chinese Luxury for the twelfth successive year, and Travel and Lifestyle Survey 2018, a that we have collaborated to release cooperative venture between Hurun the Chinese Luxury Traveller for the Report and four travel agencies, past eight years, to explore the trends namely DIADEMA, MAGIC TRAVEL, and trajectories of the high-end ZANADU and 8 Continents. travel market.” The quantitative survey encompasses ILTM China Event Manager Andy data from 236 respondents hailing Ventris added, “ILTM China has been from 43 cities nationwide, including created as a platform for the most first-tier cities such as Beijing, valuable luxury travel advisors from Shanghai, Guangzhou and Shenzhen, across China to meet with the world’s and second- and third-tier cities such very best luxury travel providers. We as Xi’an, Qingdao, Hangzhou, Nanjing, are delighted to once again partner Nanchang, Qingdao, Dalian and with Hurun Report, who are a leading Suzhou. Further details concerning voice in the conversation concerning the respondents demographic can be China’s high-net worth consumers. found in the methodology. The findings of the Chinese Luxury Traveller 2018 will continue to help Rupert Hoogewerf, Chairman & our partners and clients grow their Chief Researcher of Hurun Report, businesses in this region.” said: “Chinese high-end travellers more and more recognise the value The following report includes insights of services, and are less concerned such as the emergence of parent- about the prices compared to the child travel, the rise of holiday home past. -

DBJ Annual Report

CORE VALUES Professionalism Integrity VISION Accountability MISSION In 2020 the Development Bank of Jamaica, Innovation The Development Bank of Jamaica an inclusive, innovative, accountable, provides opportunities to all Jamaicans, customer-centric and strategy-focused employer to improve their quality of life through of choice in Jamaica; has facilitated the creation development financing, capacity of over 250,000 new jobs over the past seven years building, public-private partnership and while being a major contributor to the country’s privatisation solutions in keeping with economic growth and social transformation. Government policy. The Development Bank of Jamaica was established in April 2000, the outcome of a merger between two wholly owned Government of Jamaica institutions, the Agricultural Credit Bank of Jamaica Limited and the National Development Bank of Jamaica Limited. In September 2006, the operations of the National Investment Bank of Jamaica were merged with the DBJ. The Ministry of Finance and Planning has portfolio responsibility for the DBJ. BACKGROUND Table of Contents Board of Directors 4 Public-Private Partnerships & Privatisation 42 Management Team 5 42 Project Overviews 43 Privatisation Transactions in Progress Chairman & Managing Director’s Report 6 44 Public-Private Partnerships 6 DBJ Delivers! Transactions in Progress 9 DBJ’s 2014/15 Performance 44 Projects Being Assessed for 10 Capacity Development Development as PPPs 12 The DBJ Receives an Improved Credit 45 Other Developments in the Rating Programme 13 Corporate -

GEORGE J. STIGLER Graduate School of Business, University of Chicago, 1101 East 58Th Street, Chicago, Ill

THE PROCESS AND PROGRESS OF ECONOMICS Nobel Memorial Lecture, 8 December, 1982 by GEORGE J. STIGLER Graduate School of Business, University of Chicago, 1101 East 58th Street, Chicago, Ill. 60637, USA In the work on the economics of information which I began twenty some years ago, I started with an example: how does one find the seller of automobiles who is offering a given model at the lowest price? Does it pay to search more, the more frequently one purchases an automobile, and does it ever pay to search out a large number of potential sellers? The study of the search for trading partners and prices and qualities has now been deepened and widened by the work of scores of skilled economic theorists. I propose on this occasion to address the same kinds of questions to an entirely different market: the market for new ideas in economic science. Most economists enter this market in new ideas, let me emphasize, in order to obtain ideas and methods for the applications they are making of economics to the thousand problems with which they are occupied: these economists are not the suppliers of new ideas but only demanders. Their problem is comparable to that of the automobile buyer: to find a reliable vehicle. Indeed, they usually end up by buying a used, and therefore tested, idea. Those economists who seek to engage in research on the new ideas of the science - to refute or confirm or develop or displace them - are in a sense both buyers and sellers of new ideas. They seek to develop new ideas and persuade the science to accept them, but they also are following clues and promises and explorations in the current or preceding ideas of the science. -

CHAPTER 2020 Wanting Robustness in Macroeconomics$

CHAPTER 2020 Wanting Robustness in Macroeconomics$ Lars Peter Hansen* and Thomas J. Sargent{ * Department of Economics, University of Chicago, Chicago, Illinois. [email protected] { Department of Economics, New York University and Hoover Institution, Stanford University, Stanford, California. [email protected] Contents 1. Introduction 1098 1.1 Foundations 1098 2. Knight, Savage, Ellsberg, Gilboa-Schmeidler, and Friedman 1100 2.1 Savage and model misspecification 1100 2.2 Savage and rational expectations 1101 2.3 The Ellsberg paradox 1102 2.4 Multiple priors 1103 2.5 Ellsberg and Friedman 1104 3. Formalizing a Taste for Robustness 1105 3.1 Control with a correct model 1105 3.2 Model misspecification 1106 3.3 Types of misspecifications captured 1107 3.4 Gilboa and Schmeidler again 1109 4. Calibrating a Taste for Robustness 1110 4.1 State evolution 1112 4.2 Classical model detection 1113 4.3 Bayesian model detection 1113 4.3.1 Detection probabilities: An example 1114 4.3.2 Reservations and extensions 1117 5. Learning 1117 5.1 Bayesian models 1118 5.2 Experimentation with specification doubts 1119 5.3 Two risk-sensitivity operators 1119 5.3.1 T1 operator 1119 5.3.2 T2 operator 1120 5.4 A Bellman equation for inducing robust decision rules 1121 5.5 Sudden changes in beliefs 1122 5.6 Adaptive models 1123 5.7 State prediction 1125 $ We thank Ignacio Presno, Robert Tetlow, Franc¸ois Velde, Neng Wang, and Michael Woodford for insightful comments on earlier drafts. Handbook of Monetary Economics, Volume 3B # 2011 Elsevier B.V. ISSN 0169-7218, DOI: 10.1016/S0169-7218(11)03026-7 All rights reserved. -

Healthcare Investments and Exits | Mid-Year Report 2020 6 Date

MIDANUAL-YEAR REPORT Healthcare 2020 Investments and Exits Biopharma | HealthTech | Dx/Tools | Device Follow @SVB_Financial Engage #SVBHealthcare MID-YEAR Table of Contents REPORT 2020 Page Page Page Page 3 5 24 35 Highlights Investments Exits 2020 Outlook HealthcareHealthcare Investments Investments and & Exits | Mid-Year Report 2020 2 Healthcare Investments: Mid-Year 2020 Venture fundraising in healthcare soared to $10.4B in the first half of 2020, nearly Silicon Valley Bank Market Stats* matching 2019’s full-year record. Mezzanine “Mezz” markups and great IPO performance have driven outsized returns, allowing investors to raise new funds, many of which were larger than their previous fund. Company investment also spiked. 1H 2020 produced the largest two-quarter investment 53% period ever for venture-backed healthcare companies. Biopharma and dx/tools saw increases in investment vs. 1H 2019, despite financial market turbulence and negative of all VC-backed US impacts to many companies due to COVID-19. healthcare companies that raised rounds in 1H 2020 Biopharma Series A was stable in the first half, while overall investment is on pace for worked with SVB. record dollars in 2020. We continued to see a significant number of large crossover-led mezzanine financings in Q1 and Q2 2020. This mezzanine activity exceeds 2019’s pace and is a strong, positive sign for continued IPO activity. of the $15B in venture funding HealthTech investments remained steady in 1H 2020 but showed an 18% increase in deals raised in the US in 1H 2020 was vs. 1H 2019, solidifying healthtech as the most prolific deal sector. Alternative care, which $1 0B by companies that work with SVB. -

ECONOMIC MAN Vs HUMANITY Lyrics

DOUGHNUT ECONOMICS PRESENTS . ECONOMIC MAN vs. HUMANITY: A PUPPET RAP BATTLE STARRING: Storyline and lyrics by Simon Panrucker, Emma Powell and Kate Raworth Key concepts and quotes are drawn from Chapter 3 of Doughnut Economics. * VOICE OVER And so this concept of rational economic man is a cornerstone of economic theory and provides the foundation for modelling the interaction of consumers and firms. The next module will start tomorrow. If you have any questions, please visit your local Knowledge Bank. POTATO Hello? BRASH Hello? FACTS Shall we go to the knowledge bank? BRASH Yeah that didn’t make any sense! POTATO See you outside. They pop up outside. BRASH Let’s go! They go to The Knowledge Bank. PROF Welcome to The Knowledge Ba… oh, it’s you lot. What is it this time? FACTS The model of rational economic man PROF Look, it's just a starting point for building on POTATO Well from the start, something doesn’t sit right with me BRASH We’ve got questions! PROF sighs. PROF Ok, let me go through it again . THE RAP BEGINS PROF Listen, it’s quite simple... At the heart of economics is a model of man A simple distillation of a complicated animal Man is solitary, competing alone, Calculator in head, money in hand and no Relenting, his hunger for more is unending, Ego in heart, nature’s at his will for bending POTATO But that’s not me, it can’t be true! There’s much more to all the things humans say and do! BRASH It’s rubbish! FACTS Well, it is a useful tool For economists to think our reality through It’s said that all models are wrong but some -

Understanding Robert Lucas (1967-1981): His Influence and Influences

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Andrada, Alexandre F.S. Article Understanding Robert Lucas (1967-1981): his influence and influences EconomiA Provided in Cooperation with: The Brazilian Association of Postgraduate Programs in Economics (ANPEC), Rio de Janeiro Suggested Citation: Andrada, Alexandre F.S. (2017) : Understanding Robert Lucas (1967-1981): his influence and influences, EconomiA, ISSN 1517-7580, Elsevier, Amsterdam, Vol. 18, Iss. 2, pp. 212-228, http://dx.doi.org/10.1016/j.econ.2016.09.001 This Version is available at: http://hdl.handle.net/10419/179646 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. https://creativecommons.org/licenses/by-nc-nd/4.0/ www.econstor.eu HOSTED BY Available online at www.sciencedirect.com ScienceDirect EconomiA 18 (2017) 212–228 Understanding Robert Lucas (1967-1981): his influence ଝ and influences Alexandre F.S. -

World Adds 346 Billionaires to Take Total to Record

WORLD ADDS 346 BILLIONAIRES TO TAKE TOTAL TO RECORD 2,816 BILLIONAIRES CHINA AND USA LEAD WITH 799 AND 626 BILLIONAIRES, MAKING UP OVER HALF OF ’KNOWN’ BILLIONAIRES IN WORLD. INDIA, GERMANY AND UK FOLLOW WITH 100+ EACH. 479 NEW FACES AND 130 DROP OFFS CHINA 182 NEW FACES, DESPITE TRADE WAR, THREE TIMES THAT OF USA WITH 59 NEW FACES JEFF BEZOS, 56, OF AMAZON, RICHEST MAN IN WORLD FOR THIRD YEAR RUNNING, WITH US$140BN, DOWN US$7BN. EX-WIFE MACKENZIE MAKES LIST FOR FIRST TIME WITH US$44BN AT 22ND PLACE. PARIS-BASED BERNARD ARNAULT UP US$21BN TO 2ND PLACE WITH US$107BN, ON BACK OF SURGE IN LVMH SHARE PRICE. RECORD FOUR INDIVIDUALS CROSS US$100BN CUT-OFF. BILL GATES AND WARREN BUFFETT IN THIRD AND FOURTH PLACES WITH US$106BN AND US$102BN. TOP 10 HAS US$1TN. ELON MUSK HAS A STORMING YEAR, UP 10 PLACES TO 20TH WITH US$46BN, ON BACK OF TESLA SHARE PRICE DOUBLING, OVERTAKING CHINA NUMBER ONE JACK MA OF ALIBABA ON US$45BN DESPITE US-CHINA TRADE WAR, REN ZHENGFEI OF HUAWEI UP 7% TO US$3BN, SAME AS DONALD TRUMP AT 900TH IN THE WORLD. COSMETICS QUEEN KYLIE JENNER, 22, YOUNGEST SELF-MADE BILLIONAIRE WITH US$1.1BN ADAM NEUMANN, 40, OF WEWORK BIGGEST LOSER, WITH WEALTH DOWN 80% TO US$1.3BN BEIJING IS WORLD‘S BILLIONAIRE CAPITAL FOR 5TH YEAR RUNNING WITH 110 BILLIONAIRES LIVING THERE, 12 AHEAD OF NEW YORK. SHANGHAI OVERTAKE HONG KONG. CORONOVIRUS DRIVES UP STOCKS OF CHINESE ONLINE EDUCATION, ONLINE GAMES AND PHARMACEUTICAL COMPANIES DOING VACCINES.