Industrial Land Use and Employment Policy Plan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Union Station Conceptual Engineering Study

Portland Union Station Multimodal Conceptual Engineering Study Submitted to Portland Bureau of Transportation by IBI Group with LTK Engineering June 2009 This study is partially funded by the US Department of Transportation, Federal Transit Administration. IBI GROUP PORtlAND UNION STATION MultIMODAL CONceptuAL ENGINeeRING StuDY IBI Group is a multi-disciplinary consulting organization offering services in four areas of practice: Urban Land, Facilities, Transportation and Systems. We provide services from offices located strategically across the United States, Canada, Europe, the Middle East and Asia. JUNE 2009 www.ibigroup.com ii Table of Contents Executive Summary .................................................................................... ES-1 Chapter 1: Introduction .....................................................................................1 Introduction 1 Study Purpose 2 Previous Planning Efforts 2 Study Participants 2 Study Methodology 4 Chapter 2: Existing Conditions .........................................................................6 History and Character 6 Uses and Layout 7 Physical Conditions 9 Neighborhood 10 Transportation Conditions 14 Street Classification 24 Chapter 3: Future Transportation Conditions .................................................25 Introduction 25 Intercity Rail Requirements 26 Freight Railroad Requirements 28 Future Track Utilization at Portland Union Station 29 Terminal Capacity Requirements 31 Penetration of Local Transit into Union Station 37 Transit on Union Station Tracks -

City of Portland Union Pacific Railroad

CITY OF PORTLAND UNION PACIFIC RAILROAD CHICAGO AND NORTH WESTERN LINE CITY OF PORTLAND The "City of Port- land" described in this booklet is a 13-car train plus a 3-car Diesel power unit. Perhaps the most outstanding feature of this train is the Observa- tion-Lounge Car, named the "Copper King," embodying remarkable innovations in railroad development. The deft decorations, unique and colorful, are by Mrs. W. A. Harriman, wife of the Chairman of the Board of the Union Pacific. Her contribu- tion to the unusual interior decorations of other Union Pacific streamline trains has created con- siderable favorable comment. The "Copper King" is the first "light-condi- tioned" car in railroading and the first in which copper has been used so extensively for interior decoration, finishings and appointments. The final touch of the selections of color schemes for the furniture, the decorating, upholstering, carpeting and the exquisite buffet and other interior appoint- ments was added by Mrs. Harriman. Pullman passengers enjoy complete relaxation in the -Copper King". The “Copper King" Observation-Lounge Car. • As the name implies, the "Copper King" is resplendent in shimmering copper. The side walls have satin finished copper paneling. Tables, smoke-stands and other accessories are constructed of copper bronze and the same metal has been skillfully used in the specially designed furniture. The service buffet, near the entrance to the car, is a harmonious symphony of copper and glass. As a result of using copper as the dominant decorative note, the interior has a rich glowing beauty enhanced by the contrasting deep green and henna material with which lounges and chairs are upholstered. -

Union Station Appendix a Project Phasing Concept

Appendix A - Project Phasing 1 Portland Union Station Building & Tracks Improvement Project City of Portland (City), Multnomah County, Oregon Implementation Plan/Project Phases The Build Alternative for the Project is comprised of two major work areas: architectural and building related improvements and trackside/rail yard improvements. Each work area has several components. The availability and securing of future funding, the need to maintain passenger and freight rail operations and keep the station building operable/usable during construction activities, and potential impacts to station users necessitate a phased approach to implementing these improvements over time. Because of these constraints, a potential phasing scenario/implementation strategy was recommended by Prosper Portland’s Project consultants in which the Project as a whole could be built, breaking up the work into multiple phases, which are described below. Additional information is available in Proposed Improvements at Portland Union Station-Implementation Plan Report, IBI Group, May 2019. Track Phase Descriptions Proposed Track improvements for Portland Union Station have been subdivided into four phases. • Phase T1 – Passenger Crossing Relocation: This phase would relocate the existing passenger crossing approximately 120 feet to the north in order to allow for increased train berthing capacity at the station. FRA and Amtrak would need to review and approve design plans for this phase to ensure compliance with the Americans with Disabilities Act (ADA) and the US Department of Transportation’s ADA standards for transportation facilities. To accommodate the shift of the passenger crossing, a minimal amount of Main Building reconfiguration is recommended to minimize conflicts between Amtrak baggage/service vehicles and passengers boarding and disembarking trains and passenger movement to/from the Main Building concourse. -

Portland Rose

PORTLAND ROSE Coach – Stabled at Council Bluffs The Portland Rose was built by American Car & Foundry in 1947, the Portland Rose was re-routed to run between Denver 1953 as 44-seat coach No. 5473. It was renamed the Portland and Portland. On Jan. 10, 1954, service was extended to Kansas Rose in 1990. City, Mo., replacing Pony Express trains between Kansas City This coach was named after the train Portland Rose, which and Denver. Portland Rose service ended May 1, 1971. began service between Chicago and Portland, Ore., on Sept. 12, 1930. The Portland Rose was heralded as “A Triumph in Train Comfort,” with its own china pattern and specially decorated club observation car, the Portland Club. This car featured a radio, soda fountain, maid service, hairdresser, barber, valet and bath. The rose was the decorative motif for this train. The soft, deep pink of “Madame Caroline Testout,” the official rose of Portland, was the prevailing color. Through the Columbia River Gorge, between The Dalles and Portland, an open top observation car was added on the rear of the train. In 1941, the Portland Rose took on a Challenger section with meal prices of 35 cents for breakfast, 40 cents for lunch and 50 cents for dinner. The entire train was air-conditioned, but the luxury accommodations were found on the streamliner PASSAGEWAY RESTROOM City of Portland and the Portland Rose. This second section PASSAGEWAY RESTROOM ran 10 minutes behind and combined with the Portland Rose PASSAGEWAY at Green River, Wyo., to finish the trip to Portland. When Configuration: Portland Rose is a Flat Coach Car with public restrooms at each end of streamliner City of Portland began daily operation on Feb. -

Washington State Long-Range Plan for Amtrak Cascades

Washington State Long-Range Plan for Amtrak Cascades February 2006 Prepared by the Freight Systems Division Washington State Department of Transportation February 2006 For more information, contact: z Call the WSDOT State Rail Office at (360) 705-7900 or 1-800-822-2015; z Write to the WSDOT State Rail Office at P.O. Box 47407, Olympia, WA 98504-7407; z Fax your comments to (360) 705-6821; or z E-mail your comments to [email protected] Persons with disabilities may request this information be prepared and supplied in alternate forms by calling the WSDOT ADA Accommodation Hotline collect 206-389-2839. Persons with vision or hearing impairments may access the WA State Telecommunications Relay Service at TT 1-800-833-6388, Tele-Braille 1-800-833-6385, or Voice 1-800-833-6384, and ask to be connected to 360-705-7097. Washington State Long-Range Plan for Amtrak Cascades Prepared for the Washington State Department of Transportation By The Resource Group Consultants, Inc. Transit Safety Management, Inc. HDR Engineering, Inc. Berk & Associates, Inc. AECOM Consult, Inc. February 2006 Table of Contents List of Exhibits .......................................................................................................iii Executive Summary................................................................................................v Chapter One: Introduction ..................................................................................1-1 What is intercity passenger rail? ......................................................................................... -

Union Pacific's E-9 No. 951 Union Pacific's E·9 No. 951 Vishs Portola

Union Pacific's E·9 No. 951 visHs Portola, California during Railroad Days in August 1988 -Norman Holmes Photo Union Pacific's E-9 No. 951 Union Pacific Locomotive No. 951 is the last of Union Pacific's high Union Pacific for use on special trains such as inspection speed diesel-electrics built for service on the famous specials and occasional employee special trains. streamliner and domeliner passenger trains. In 1974, No. 951 was loaned to the sponsors of the The 2400 horsepower locomotive was built for Union American Freedom Train to promote the AFT's bicentennial Pacific Railroad by the Electro-Motive Division (EMD) of tour. The locomotive was repainted into a bicentennial paint General Motors and delivered in June 1955. scheme of red, white and blue and toured much of the nation r The unit, one of 69 EMD model E-9 units on the Union pulling the "Preamble Express" in advance of the widely Pacific, pulled such famous trains as the City of Los Angeles, publicized steam-powered Freedom Train tours in 1975 and City of Portland, City of San Francisco, City of St. Louis and 1976. The locomotive maintained it's patriotic look until 1978 Challenger. when it was repainted in it's original Union Pacific armour The sleek units, considered among the most graceful yellow colors. locomotives in American railroading, evolved from the first In August 1980, the eight units were retired. Seven were Union Pacific streamlined locomotives back in 1934. The "E" sold or donated to museums. No. 951 was kept as UP's last E series was started by EMD in the late 1930's. -

Realizing the Potential: One Year Later Housing Opportunities Near Transit in a Changing Market

Realizing the Potential: One Year Later Housing Opportunities near Transit in a Changing Market December 2008 prepared for: United States Department of Transportation Federal Transit Administration Funded through a cooperative agreement between Reconnecting America and the Federal Transit Administration (FTA), US Department of Transportation. (C-26.1007.02) ABOUT THIS REPORT Realizing the Potential One Year Later: Housing Opportunities Near Transit in a Changing Market was written by Reconnecting America’s Center for Transit-Oriented Development. The Center for TOD is the only national nonprofit effort dedicated to providing best practices, research and tools to support market-based transit-oriented development. We partner with both the public and private market sectors to strategize about ways to encourage the development of high-performing TOD projects around transit stations and to build transit systems that maximize the development potential. The Center for TOD is a partnership of the national nonprofit Reconnecting America, the Center for Neighborhood Technology, and Strategic Economics, an urban economics firm in Berkeley, CA. Primary Authors Abigail Thorne-Lyman, Strategic Economics Alison Nemirow, Strategic Economics Jeff Wood, Reconnecting America Robert Hickey, Strategic Economics Acknowledgements The Center for Transit-Oriented Development would like to thank the Federal Transit Administration (FTA), U.S. Department of Transportation, U.S. Department of Housing and Urban Development, and local planners and developers in the Boston, Charlotte, Denver, Portland, and Twin Cities regions, for their financial and technical support. Notice This report was funded through a cooperative agreement between Reconnecting America and the Federal Transit Administration (FTA), U.S. Department of Transportation. The views and policies expressed herein do not necessarily represent the views or policies of the Federal Transit Administration. -

Funeral Train Consist

POWER CARS 207, 208 AND 2066 Power Cars – Stabled at Council Bluffs American Car & Foundry built car Nos. 207 and 208 in 1949 as boiler/baggage/dormitory car Nos. 6004 and 6006. They later were rebuilt as steam generator dormitory car Nos. 303 and 304, and renumbered to Nos. 207 and 208 in 1987. Power car 2066 was built as postal storage car No. 5816. Steam locomotives had supplied passenger cars with the steam needed for heat and hot water, but after diesel locomotives were phased in, steam generators were required. They were placed in baggage cars at the front of trains. Locomotive auxiliary generators provided 32-volts of electrical power for the passenger cars that could be “stored” for short periods of time in batteries underneath each car. As Union Pacific’s passenger equipment was modernized and the need for electric power grew, steam generator cars were ENGINE/GENERATOR CONTROL WALK-IN COMMISARY WALK-IN rebuilt into diesel-electric generator cars that provide electricity COMPARTMENT ROOM COOLER STORAGE FREEZER to the entire train. Each passenger car is connected to the PASSAGEWAY power car using a series of “jumper cables” between each car. Configuration: UPP 207, UPP 208 and UPP 2066 are Power Cars with two Deutz diesels in one end and a control room. It has a crew room with private bathroom that sleeps one, Some of Union Pacific’s passenger cars are equipped and a storage room with walk in refrigerator and freezer. with their own electric generators, allowing them to operate without a power car. Power cars also have living quarters for an electrician who monitors the system, and additional refrigerators and freezers for commissary services. -

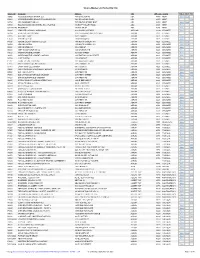

Source Master List Sorted by City

Source Master List Sorted By City Source ID Company Address City ZIP Code County Other* ROP PTI A2402 ACCESS BUSINESS GROUP, LLC 7575 E FULTON RD ADA 49355 KENT View View P0469 ACCESS BUSINESS GROUP-SPAULDING PLAZA 5101 SPAULDING PLAZA ADA 49355 KENT View N1784 ADA COGENERATION LLC 7575 FULTON STREET EAST ADA 49355 KENT View View N5183 HALLIDAY SAND AND GRAVEL, INC. - PLANT #4 866 EGYPT VALLEY ROAD ADA 49301 KENT View U411702145 RESIDENCE 645 ADA DR SE ADA 49341 KENT View B5921 LENAWEE CO ROAD COMMISSION 9293 ROUND LAKE HWY ADDISON 49220 LENAWEE View N7389 A & A CUSTOM CRUSHING GREEN HIGHWAY AND IVES ROAD ADRIAN 49221 LENAWEE View B2285 ACE DRILL CORP 2600 E MAUMEE ADRIAN 49221 LENAWEE View E8510 ADRIAN COLLEGE 110 S MADISON ST ADRIAN 49221 LENAWEE View P0426 ADRIAN ENERGY ASSOCIATES LLC 1900 NORTH OGDEN HWY ADRIAN 49221 LENAWEE View View N2369 ADRIAN LANDFILL 1970 NORTH OGDEN HWY ADRIAN 49221 LENAWEE View View B2288 ADRIAN STEEL CO 906 JAMES ST ADRIAN 49221 LENAWEE View B2289 AGET MANUFACTURING CO 1408 CHURCH ST E ADRIAN 49221 LENAWEE View N0629 ANDERSON DEVELOPMENT 525 GULF STREET ADRIAN 49221 LENAWEE View A2851 ANDERSON DEVELOPMENT COMPANY 1415 EAST MICHIGAN STREET ADRIAN 49221 LENAWEE View View N3196 CLIFT PONTIAC 1115 S MAIN ST ADRIAN 49221 LENAWEE View P1187 CORNERSTONE CRUSHING 1001 OAKWOOD ROAD ADRIAN 49221 LENAWEE View E8117 DAIRY FARMERS OF AMERICA INC 1336 E MAUMEE ST ADRIAN 49221 LENAWEE View B1754 ERVIN AMASTEEL DIVISION 915 TABOR ST. ADRIAN 49221 LENAWEE View View B2621 FLOYD’S RIGGING & MACHINERY MOVERS 831 DIVISION ST ADRIAN 49221 LENAWEE View B7068 GMI - HMA PLANT 19 2675 TREAT RD ADRIAN 49221 LENAWEE View View P0931 GMI CAT RDS-20 PORTABLE CRUSHER 2675 TREAT STREET ADRIAN 49221 LENAWEE View View N8221 GMI EXCEL PORTABLE CRUSHER 2675 TREAT RD ADRIAN 49221 LENAWEE View View B6027 INTEVA PRODUCTS ADRIAN OPERATIONS 1450 E. -

City of Portland V. United States 3

FOR PUBLICATION UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT CITY OF PORTLAND, No. 18-72689 Petitioner, FCC No. v. 18-111 UNITED STATES OF AMERICA; FEDERAL COMMUNICATIONS COMMISSION, Respondents, CITY AND COUNTY OF SAN FRANCISCO; CITY OF ARCADIA; CITY OF BELLEVUE; CITY OF BROOKHAVEN; CITY OF BURIEN; CITY OF BURLINGAME; CITY OF CHICAGO; CITY OF CULVER CITY; CITY OF DUBUQUE; CITY OF GIG HARBOR; CITY OF KIRKLAND; CITY OF LAS VEGAS; CITY OF LINCOLN; CITY OF MONTEREY; CITY OF PHILADELPHIA; CITY OF PIEDMONT; CITY OF PLANO; CITY OF SAN BRUNO; CITY OF SAN JACINTO; CITY OF SAN JOSE; CITY OF SANTA MONICA; CITY OF SHAFTER; COUNTY OF LOS ANGELES; HOWARD COUNTY; MICHIGAN MUNICIPAL LEAGUE; CTIA - THE WIRELESS 2 CITY OF PORTLAND V.UNITED STATES ASSOCIATION; TOWN OF FAIRFAX; TOWN OF HILLSBOROUGH, Intervenors. AMERICAN ELECTRIC POWER No. 19-70490 SERVICE CORPORATION; CENTERPOINT ENERGY HOUSTON FCC No. ELECTRIC, LLC; DUKE ENERGY 18-111 CORPORATION; ENTERGY CORPORATION; ONCOR ELECTRIC DELIVERY COMPANY, LLC; SOUTHERN COMPANY; TAMPA ELECTRIC COMPANY; VIRGINIA ELECTRIC AND POWER COMPANY; XCEL ENERGY SERVICES INC., Petitioners, v. FEDERAL COMMUNICATIONS COMMISSION; UNITED STATES OF AMERICA, Respondents, VERIZON; US TELECOM—THE BROADBAND ASSOCIATION, Respondents-Intervenors. CITY OF PORTLAND V. UNITED STATES 3 SPRINT CORPORATION, No. 19-70123 Petitioner, FCC No. v. 18-133 FEDERAL COMMUNICATIONS COMMISSION; UNITED STATES OF AMERICA, Respondents, CITY OF BOWIE, Maryland; CITY OF EUGENE, Oregon; CITY OF HUNTSVILLE, Alabama; CITY OF WESTMINSTER, Maryland; -

DINER NO. 4801 Comprehensive Railroad Reference Libraries in the United States

Robert W. Richardson Railroad Library UNION PACIFIC Built in 1997, the Robert W. Richardson Railroad Library at the Colorado Railroad Museum is designed to look like a small town depot and contains one of the most DINER NO. 4801 comprehensive railroad reference libraries in the United States. From timetables to employee records, photographs to engineering documents, maps to books, it offers a wealth of information on railroads across the nation and around the world. Brochure contents from Iron Horse News Issue #231 article ‘Coming Soon: Upscale Dining at the Railroad Museum” by Larry Dorsey and Wheels Magazine issue March/April 1949. Photographs are from the Colorado Railroad Museum collection, Richard Luckin and Wheels Magazine issue March/April 1949. The Colorado Railroad Museum has many artifacts related to the Dining Cars that ran throughout Colorado including: China, Original Recipe Books, Dinner Chime, Menus, Linens, Chairs and Silverware Mission Statement To acquire, preserve and exhibit to the general public, railroad equipment, artifacts, paper records, books, artwork and photographs emphasizing Rocky Mountain area railroads, The old song lyric says it all, “Dinner in the diner, nothing could be finer.” These rolling restaurants provided to explain and interpret the role of railroads in the history of this region from the 1860s to a unique experience that combined high-class fare and fabulous moving scenery captured through the the present by means of exhibits, a reference library, educational programs, publications and window at every table. information sharing with other historical groups. Furthermore to provide incentives that American Car & Foundry in St. Charles, Missouri built the Union Pacific Dining Cars in 1949 for use on the will enhance interest in railroads and railroading history. -

Moving-To-Work – CARES Act State PHA PHA Name (Recipient)

Moving-to-Work – CARES Act State PHA PHA Name (Recipient) City Award Amount CA CA003 Oakland Housing Authority Oakland $ 2,852,782 CA CA014 Housing Authority of the County of San Mateo BELMONT $ 71,622 CA CA030 Tulare County Housing Authority VISALIA $ 417,598 CT CT004 Housing Authority of the City of New Haven NEW HAVEN $ 815,764 DC DC001 D.C Housing Authority Washington $ 2,731,692 DE DE901 Delaware State Housing Authority Dover $ 137,336 Housing Authority of the City of ATLANTA $ 2,863,928 GA GA006 Georgia Atlanta IL IL002 Chicago Housing Authority CHICAGO $ 919,652 KS KS053 Lawrence/Douglas County Housing Authority LAWRENCE $ 93,488 KY KY001 Louisville Metro Housing Authority Louisville $ 1,145,784 MA MA003 Cambridge Housing Authority Cambridge $ 986,524 NH NH010 Keene Housing KEENE $ 112,522 OH OH031 Portage Metropolitan Housing Authority RAVENNA $ 202,102 PA PA001 Housing Authority of the City of Pittsburgh PITTSBURGH $ 822,696 PA PA002 Philadelphia Housing Authority Philadelphia $ 3,175,744 WA WA001 Seattle Housing Authority SEATTLE $ 1,756,750 WA WA002 HA OF KING COUNTY Seattle $ 1,492,340 TOTAL $20,598,324 Supplemental Administrative Fee Funding (Mainstream) – CARES Act State PHA Name (Recipient) City Award Amount AK Alaska Housing Finance Corporation Anchorage $ 864,930 AL Housing Authority of the Birmingham District BIRMINGHAM $ 606,772 AL MOBILE HOUSING BOARD MOBILE $ 495,324 AL ANNISTON HA ANNISTON $ 33,424 AL PHENIX CITY HOUSING AUTHORITY PHENIX CITY $ 94,806 AL Housing Authority of the City of Montgomery Montgomery $ 365,544