Women Self Help Groups at Thiruvarur District-A Case Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Thiruvallur District

DISTRICT DISASTER MANAGEMENT PLAN FOR 2017 TIRUVALLUR DISTRICT tmt.E.sundaravalli, I.A.S., DISTRICT COLLECTOR TIRUVALLUR DISTRICT TAMIL NADU 2 COLLECTORATE, TIRUVALLUR 3 tiruvallur district 4 DISTRICT DISASTER MANAGEMENT PLAN TIRUVALLUR DISTRICT - 2017 INDEX Sl. DETAILS No PAGE NO. 1 List of abbreviations present in the plan 5-6 2 Introduction 7-13 3 District Profile 14-21 4 Disaster Management Goals (2017-2030) 22-28 Hazard, Risk and Vulnerability analysis with sample maps & link to 5 29-68 all vulnerable maps 6 Institutional Machanism 69-74 7 Preparedness 75-78 Prevention & Mitigation Plan (2015-2030) 8 (What Major & Minor Disaster will be addressed through mitigation 79-108 measures) Response Plan - Including Incident Response System (Covering 9 109-112 Rescue, Evacuation and Relief) 10 Recovery and Reconstruction Plan 113-124 11 Mainstreaming of Disaster Management in Developmental Plans 125-147 12 Community & other Stakeholder participation 148-156 Linkages / Co-oridnation with other agencies for Disaster 13 157-165 Management 14 Budget and Other Financial allocation - Outlays of major schemes 166-169 15 Monitoring and Evaluation 170-198 Risk Communications Strategies (Telecommunication /VHF/ Media 16 199 / CDRRP etc.,) Important contact Numbers and provision for link to detailed 17 200-267 information 18 Dos and Don’ts during all possible Hazards including Heat Wave 268-278 19 Important G.Os 279-320 20 Linkages with IDRN 321 21 Specific issues on various Vulnerable Groups have been addressed 322-324 22 Mock Drill Schedules 325-336 -

Guide to 275 SIVA STHALAMS Glorified by Thevaram Hymns (Pathigams) of Nayanmars

Guide to 275 SIVA STHALAMS Glorified by Thevaram Hymns (Pathigams) of Nayanmars -****- by Tamarapu Sampath Kumaran About the Author: Mr T Sampath Kumaran is a freelance writer. He regularly contributes articles on Management, Business, Ancient Temples and Temple Architecture to many leading Dailies and Magazines. His articles for the young is very popular in “The Young World section” of THE HINDU. He was associated in the production of two Documentary films on Nava Tirupathi Temples, and Tirukkurungudi Temple in Tamilnadu. His book on “The Path of Ramanuja”, and “The Guide to 108 Divya Desams” in book form on the CD, has been well received in the religious circle. Preface: Tirth Yatras or pilgrimages have been an integral part of Hinduism. Pilgrimages are considered quite important by the ritualistic followers of Sanathana dharma. There are a few centers of sacredness, which are held at high esteem by the ardent devotees who dream to travel and worship God in these holy places. All these holy sites have some mythological significance attached to them. When people go to a temple, they say they go for Darsan – of the image of the presiding deity. The pinnacle act of Hindu worship is to stand in the presence of the deity and to look upon the image so as to see and be seen by the deity and to gain the blessings. There are thousands of Siva sthalams- pilgrimage sites - renowned for their divine images. And it is for the Darsan of these divine images as well the pilgrimage places themselves - which are believed to be the natural places where Gods have dwelled - the pilgrimage is made. -

Nagapattinam District 64

COASTAL DISTRICT PROFILES OF TAMIL NADU ENVIS CENTRE Department of Environment Government of Tamil Nadu Prepared by Suganthi Devadason Marine Research Institute No, 44, Beach Road, Tuticorin -628001 Sl.No Contents Page No 1. THIRUVALLUR DISTRICT 1 2. CHENNAI DISTRICT 16 3. KANCHIPURAM DISTRICT 28 4. VILLUPURAM DISTRICT 38 5. CUDDALORE DISTRICT 50 6. NAGAPATTINAM DISTRICT 64 7. THIRUVARUR DISTRICT 83 8. THANJAVUR DISTRICT 93 9. PUDUKOTTAI DISTRICT 109 10. RAMANATHAPURAM DISTRICT 123 11. THOOTHUKUDI DISTRICT 140 12. TIRUNELVELI DISTRICT 153 13. KANYAKUMARI DISTRICT 174 THIRUVALLUR DISTRICT THIRUVALLUR DISTRICT 1. Introduction district in the South, Vellore district in the West, Bay of Bengal in the East and i) Geographical location of the district Andhra Pradesh State in the North. The district spreads over an area of about 3422 Thiruvallur district, a newly formed Sq.km. district bifurcated from the erstwhile Chengalpattu district (on 1st January ii) Administrative profile (taluks / 1997), is located in the North Eastern part of villages) Tamil Nadu between 12°15' and 13°15' North and 79°15' and 80°20' East. The The following image shows the district is surrounded by Kancheepuram administrative profile of the district. Tiruvallur District Map iii) Meteorological information (rainfall / ii) Agriculture and horticulture (crops climate details) cultivated) The climate of the district is moderate The main occupation of the district is agriculture and allied activities. Nearly 47% neither too hot nor too cold but humidity is of the total work force is engaged in the considerable. Both the monsoons occur and agricultural sector. Around 86% of the total in summer heat is considerably mitigated in population is in rural areas engaged in the coastal areas by sea breeze. -

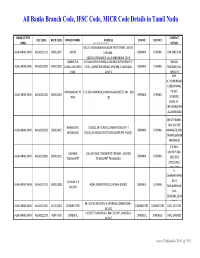

Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu

All Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu NAME OF THE CONTACT IFSC CODE MICR CODE BRANCH NAME ADDRESS CENTRE DISTRICT BANK www.Padasalai.Net DETAILS NO.19, PADMANABHA NAGAR FIRST STREET, ADYAR, ALLAHABAD BANK ALLA0211103 600010007 ADYAR CHENNAI - CHENNAI CHENNAI 044 24917036 600020,[email protected] AMBATTUR VIJAYALAKSHMIPURAM, 4A MURUGAPPA READY ST. BALRAJ, ALLAHABAD BANK ALLA0211909 600010012 VIJAYALAKSHMIPU EXTN., AMBATTUR VENKATAPURAM, TAMILNADU CHENNAI CHENNAI SHANKAR,044- RAM 600053 28546272 SHRI. N.CHANDRAMO ULEESWARAN, ANNANAGAR,CHE E-4, 3RD MAIN ROAD,ANNANAGAR (WEST),PIN - 600 PH NO : ALLAHABAD BANK ALLA0211042 600010004 CHENNAI CHENNAI NNAI 102 26263882, EMAIL ID : CHEANNA@CHE .ALLAHABADBA NK.CO.IN MR.ATHIRAMIL AKU K (CHIEF BANGALORE 1540/22,39 E-CROSS,22 MAIN ROAD,4TH T ALLAHABAD BANK ALLA0211819 560010005 CHENNAI CHENNAI MANAGER), MR. JAYANAGAR BLOCK,JAYANAGAR DIST-BANGLAORE,PIN- 560041 SWAINE(SENIOR MANAGER) C N RAVI, CHENNAI 144 GA ROAD,TONDIARPET CHENNAI - 600 081 MURTHY,044- ALLAHABAD BANK ALLA0211881 600010011 CHENNAI CHENNAI TONDIARPET TONDIARPET TAMILNADU 28522093 /28513081 / 28411083 S. SWAMINATHAN CHENNAI V P ,DR. K. ALLAHABAD BANK ALLA0211291 600010008 40/41,MOUNT ROAD,CHENNAI-600002 CHENNAI CHENNAI COLONY TAMINARASAN, 044- 28585641,2854 9262 98, MECRICAR ROAD, R.S.PURAM, COIMBATORE - ALLAHABAD BANK ALLA0210384 641010002 COIIMBATORE COIMBATORE COIMBOTORE 0422 2472333 641002 H1/H2 57 MAIN ROAD, RM COLONY , DINDIGUL- ALLAHABAD BANK ALLA0212319 NON MICR DINDIGUL DINDIGUL DINDIGUL -

SNO APP.No Name Contact Address Reason 1 AP-1 K

SNO APP.No Name Contact Address Reason 1 AP-1 K. Pandeeswaran No.2/545, Then Colony, Vilampatti Post, Intercaste Marriage certificate not enclosed Sivakasi, Virudhunagar – 626 124 2 AP-2 P. Karthigai Selvi No.2/545, Then Colony, Vilampatti Post, Only one ID proof attached. Sivakasi, Virudhunagar – 626 124 3 AP-8 N. Esakkiappan No.37/45E, Nandhagopalapuram, Above age Thoothukudi – 628 002. 4 AP-25 M. Dinesh No.4/133, Kothamalai Road,Vadaku Only one ID proof attached. Street,Vadugam Post,Rasipuram Taluk, Namakkal – 637 407. 5 AP-26 K. Venkatesh No.4/47, Kettupatti, Only one ID proof attached. Dokkupodhanahalli, Dharmapuri – 636 807. 6 AP-28 P. Manipandi 1stStreet, 24thWard, Self attestation not found in the enclosures Sivaji Nagar, and photo Theni – 625 531. 7 AP-49 K. Sobanbabu No.10/4, T.K.Garden, 3rdStreet, Korukkupet, Self attestation not found in the enclosures Chennai – 600 021. and photo 8 AP-58 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Community Certificate Wrongly enclosed Pondicherry – 605 007. 9 AP-60 V.A.Kishor Kumar No.19, Thilagar nagar, Ist st, Kaladipet, Only one ID proof attached. Thiruvottiyur, Chennai -600 019 10 AP-61 D.Anbalagan No.8/171, Church Street, Only one ID proof attached. Komathimuthupuram Post, Panaiyoor(via) Changarankovil Taluk, Tirunelveli, 627 761. 11 AP-64 S. Arun kannan No. 15D, Poonga Nagar, Kaladipet, Only one ID proof attached. Thiruvottiyur, Ch – 600 019 12 AP-69 K. Lavanya Priyadharshini No, 35, A Block, Nochi Nagar, Mylapore, Only one ID proof attached. Chennai – 600 004 13 AP-70 G. -

S. No. App.No. Name Address 1 AP-6 J.R. Rahul 2 AP-16 K. Pradeep

Accepted list for the post of Reader - BC (OTBCM) (NP) -2 S. No. App.No. Name Address 1 AP-6 J.R. Rahul No.23/61, Gokulam Attingarai, Manavalakurichi, Kanyakumari – 629 252 2 AP-16 K. Pradeep Subramanian No.30, Pandiyan Street, Sundar Nagar, Thirunagar, Madurai – 625 006. 3 AP-30 A. John Antony K.Rasiamangalam(Po.), Alangankudi Taluk, Pudhukottai – 622 301. 4 AP-33 M. Subha Door No.6, 2ndFloor, Vasanth Apartments, C Block, No.1, Maduraiswamy Madam Street, Perambur, Chennai – 600 011. 5 AP-35 R. Vijayalakshmi No.26-A, Sathymoorthy Street, Narimedu, Madurai – 625 002. 6 AP-40 P. Ganesh Old No.L/1229, New No.20, 29thCross Street, Thiruvalluvar Nagar, Thiruvanmiyur, Chennai – 600 041. 7 AP-45 K. Balasubramanian No.6/40, Thiruvalluvar Street, Kuladheepamangalam (Post) Thirukovilur Taluk, Villupuram – 605 756. 8 AP-51 L. Babu No.73/45, Munusamy Street, Ayanavaram, Chennai – 600 023. 9 AP-56 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Pondicherry – 605 007. 10 AP-62 R.D. Mathanram No.57, Jeeyar Narayanapalayam St, Kanchipuram – 631 501 11 AP-77 M.Parameswari No.8/4, Alagiri Nagar, 1ststreet, Vadapalani, chennai -26. 12 AP-83 G. Selva Kumari No. 12, G Block, Singara thottam, Police Quarters, Old Washermen pet, Chennai 600 021 13 AP-89 P. Mythili No.137/64, Sanjeeviroyan Koil Street, Old Washermenpet, Chennai – 600 021. 14 AP-124 K. Balaji No.11, Muthumariamman Koil Street, Bharath Nagar, Selaiyur, Chennai – 600 073. 15 AP-134 S. Anitha No.5/55-A, Main Road, Siruvangunam, Iraniyasithi Post, Seiyur Taluk, Kancheepuram – 603 312. -

Tamil Nadu Government Gazette

© [Regd. No. TN/CCN/467/2012-14. GOVERNMENT OF TAMIL NADU [R. Dis. No. 197/2009. 2013 [Price: Rs. 54.80 Paise. TAMIL NADU GOVERNMENT GAZETTE PUBLISHED BY AUTHORITY No. 41] CHENNAI, WEDNESDAY, OCTOBER 23, 2013 Aippasi 6, Vijaya, Thiruvalluvar Aandu–2044 Part VI—Section 4 Advertisements by private individuals and private institutions CONTENTS PRIVATE ADVERTISEMENTS Pages Change of Names .. 2893-3026 Notice .. 3026-3028 NOTICE NO LEGAL RESPONSIBILITY IS ACCEPTED FOR THE PUBLICATION OF ADVERTISEMENTS REGARDING CHANGE OF NAME IN THE TAMIL NADU GOVERNMENT GAZETTE. PERSONS NOTIFYING THE CHANGES WILL REMAIN SOLELY RESPONSIBLE FOR THE LEGAL CONSEQUENCES AND ALSO FOR ANY OTHER MISREPRESENTATION, ETC. (By Order) Director of Stationery and Printing. CHANGE OF NAMES 43888. My son, D. Ramkumar, born on 21st October 1997 43891. My son, S. Antony Thommai Anslam, born on (native district: Madurai), residing at No. 4/81C, Lakshmi 20th March 1999 (native district: Thoothukkudi), residing at Mill, West Colony, Kovilpatti, Thoothukkudi-628 502, shall Old No. 91/2, New No. 122, S.S. Manickapuram, Thoothukkudi henceforth be known as D. RAAMKUMAR. Town and Taluk, Thoothukkudi-628 001, shall henceforth be G. DHAMODARACHAMY. known as S. ANSLAM. Thoothukkudi, 7th October 2013. (Father.) M. v¯ð¡. Thoothukkudi, 7th October 2013. (Father.) 43889. I, S. Salma Banu, wife of Thiru S. Shahul Hameed, born on 13th September 1975 (native district: Mumbai), 43892. My son, G. Sanjay Somasundaram, born residing at No. 184/16, North Car Street, on 4th July 1997 (native district: Theni), residing Vickiramasingapuram, Tirunelveli-627 425, shall henceforth at No. 1/190-1, Vasu Nagar 1st Street, Bank be known as S SALMA. -

Tamil Nadu Government Gazette

© [Regd. No. TN/CCN/467/2012-14. GOVERNMENT OF TAMIL NADU [R. Dis. No. 197/2009. 2015 [Price: Rs. 31.20 Paise. TAMIL NADU GOVERNMENT GAZETTE PUBLISHED BY AUTHORITY No. 9] CHENNAI, WEDNESDAY, MARCH 4, 2015 Maasi 20, Jaya, Thiruvalluvar Aandu – 2046 Part VI—Section 4 Advertisements by private individuals and private institutions CONTENTS PRIVATE ADVERTISEMENTS Pages. Change of Names .. 587-664 NOTICE NO LEGAL RESPONSIBILITY IS ACCEPTED FOR THE PUBLICATION OF ADVERTISEMENTS REGARDING CHANGE OF NAME IN THE TAMIL NADU GOVERNMENT GAZETTE. PERSONS NOTIFYING THE CHANGES WILL REMAIN SOLELY RESPONSIBLE FOR THE LEGAL CONSEQUENCES AND ALSO FOR ANY OTHER MISREPRESENTATION, ETC. (By Order) Director of Stationery and Printing. CHANGE OF NAMES 8469. I, B. Sahayarani, wife of Thiru M. Bergmans, 8472. I, Janaki, wife of Thiru T. Ramesh, born on born on 3rd May 1970 (native district: Madurai), 24th April 1979 (native district: Madurai), residing at residing at No. 27, Xavier Monica Illam, K.P. Street, No. 109/32, Mela Kailasapuram, Madurai-625 018, New Ellis Nagar, Madurai-625 010, shall henceforth be shall henceforth be known as R. MURUGESWARI. known as M. SAGAYARANI. ü£ùA. B. SAHAYARANI. Madurai, 23rd February 2015. Madurai, 23rd February 2015. 8473. I, M. Ravichandran, son of Thiru K. Muthiah, 8470. I, P. Pushpa, wife of Thiru N. Jesukaran Isravel, born on 28th January 1964 (native district: Madurai), born on 16th May 1972 (native district: Kanyakumari), residing residing at Old No. 9, New No. 3/389, Kambar Salai, at No. 940/2, A-1C, S.T.C. College Road, New Zion Street, Dhinamani Nagar, Madurai-625 018, shall henceforth be Perumalpuram, Tirunelveli-627 007, shall henceforth be known as M RICHARD. -

TIRUVANNAMALAI DISTRICT (Based on Tiruvannamalai Diagnostic Study)

Government of Tamilnadu Dept of Rural Development & Panchayat Raj Tamilnadu Rural Transformation Project (TNRTP) District Diagnostic Report (DDR) TIRUVANNAMALAI DISTRICT (Based on Tiruvannamalai Diagnostic Study) Government of Tamilnadu Dept of Rural Development & Panchayat Raj Tamilnadu Rural Transformation Project (TNRTP) District Diagnostic Report (DDR) THIRUVANNAMALAI DISTRICT (Based on Tiruvannamalai Diagnostic Study) FOREWORD Thiru.K.S. Kandasamy, I.A.S., District Collector, Tiruvannamalai. TNRTP aims to promote rural enterprise development - including rural enterprise promotion, enterprise development, facilitating access to the business development services, access to finance and strengthening the value chain development of the identified commodities, thereby promoting market led economic empowerment of the rural communities and women. It will target households that are organized into community institutional platforms; and will promote “group enterprises” such as - Producer groups and Producer Collectives, and “individual enterprises” - Nano, Micro & Small Enterprises (NMSE). I appreciate the cooperation of the department officials in bringing the all data for this Distrct Diagnostic Study in systematic manner to understand the resources in better way in the Tiruvannamalai District. Best Wishes Date : District Collector Place : Tiruvannamalai Tiruvannamalai District PREFACE Tmt.S. Rajathi, MBA, MSW., District Executive Officer, Tiruvannamalai. As part of the Tamil Nadu Rural Transformation Project, fact findings is one of the foremost important activity, In order District Diagnostic Study(DDS) is the most vital part of a project to identify the opportunities in Rural sector towards Sustainable development and TNRTP aims to support rural enterprises like Farm, Non-farm & Service sectors, Including empowerment of women 65%, Tribal and Differently abled persons. Based on this DDS report prioritized commodities evaluated through Value chain analysis and it is a strategy tool used to analyze internal firm activities. -

LIST of KUDIMARAMATH WORKS 2019-20 WATER BODIES RESTORATION with PARTICIPATORY APPROACH Annexure to G.O(Ms)No.58, Public Works (W2) Department, Dated 13.06.2019

GOVERNMENT OF TAMILNADU PUBLIC WORKS DEPARTMENT WATER RESOURCES ORGANISATION ANNEXURE TO G.O(Ms.)NO. 58 PUBLIC WORKS (W2) DEPARTMENT, DATED 13.06.2019 LIST OF KUDIMARAMATH WORKS 2019-20 WATER BODIES RESTORATION WITH PARTICIPATORY APPROACH Annexure to G.O(Ms)No.58, Public Works (W2) Department, Dated 13.06.2019 Kudimaramath Scheme 2019-20 Water Bodies Restoration with Participatory Approach General Abstract Total Amount Sl.No Region No.of Works Page No (Rs. In Lakhs) 1 Chennai 277 9300.00 1 - 26 2 Trichy 543 10988.40 27 - 82 3 Madurai 681 23000.00 83 - 132 4 Coimbatore 328 6680.40 133 - 181 Total 1829 49968.80 KUDIMARAMATH SCHEME 2019-2020 CHENNAI REGION - ABSTRACT Estimate Sl. Amount No Name of District No. of Works Rs. in Lakhs 1 Thiruvallur 30 1017.00 2 Kancheepuram 38 1522.00 3 Dharmapuri 10 497.00 4 Tiruvannamalai 37 1607.00 5 Villupuram 73 2642.00 6 Cuddalore 36 815.00 7 Vellore 53 1200.00 Total 277 9300.00 1 KUDIMARAMATH SCHEME 2019-2020 CHENNAI REGION Estimate Sl. District Amount Ayacut Tank Unique No wise Name of work Constituency Rs. in Lakhs (in Ha) Code Sl.No. THIRUVALLUR DISTRICT Restoration by Removal of shoals and Reconstruction of sluice 1 1 and desilting the supply channel in Neidavoyal Periya eri Tank in 28.00 Ponneri 354.51 TNCH-02-T0210 ponneri Taluk of Thiruvallur District Restoration by Removal of shoals and Reconstruction of sluice 2 2 and desilting the supply channel in Voyalur Mamanikkal Tank in 44.00 Ponneri 386.89 TNCH-02-T0187 ponneri Taluk of Thiruvallur District Restoration by Removal of shoals and Reconstruction -

District AC No Name of the Assembly Constituency Email of Returning Officer Contact No

General Elections to TNLA - 2016 - Contact details of Returning Officers District AC No Name of the Assembly Constituency Email of Returning Officer Contact No. THIRUVALLUR 1 Gummidipoondi [email protected] 9444934916 THIRUVALLUR 2 Ponneri [email protected] 9445000410 THIRUVALLUR 3 Tiruttani [email protected] 9445000411 THIRUVALLUR 4 Thiruvallur(AC) [email protected] 9444518299 THIRUVALLUR 5 Poonamallee [email protected] 9445000412 THIRUVALLUR 6 Avadi [email protected] 9095154565 THIRUVALLUR 7 Maduravoyal [email protected] 9443347682 THIRUVALLUR 8 Ambattur [email protected] 9445190007 THIRUVALLUR 9 Madavaram [email protected] 9445461785 THIRUVALLUR 10 Thiruvottiyur [email protected] 9445190001 CHENNAI 11 Dr.Radhakrishnan Nagar - 9840071019 CHENNAI 12 Perambur - 9445000901 CHENNAI 13 Kolathur - 9790977999 CHENNAI 14 Villivakkam - 9443703430 CHENNAI 15 Thiru-Vi-Ka-Nagar - 9952553355 CHENNAI 16 Egmore - 9840889966 CHENNAI 17 Royapuram - 9445006554 CHENNAI 18 Harbour - 9786532747 CHENNAI 19 Chepauk-Thiruvallikeni - 9443602670 CHENNAI 20 Thousand Lights - 8754456039 CHENNAI 21 Anna Nagar - 9498002611 CHENNAI 22 Virugampakkam - 9445029704 CHENNAI 23 Saidapet - 9445074956 CHENNAI 24 Thiyagarayanagar - 9962985626 CHENNAI 25 Mylapore - 9551109044 CHENNAI 26 Velachery - 9444446559 General Elections to TNLA - 2016 - Contact details of Returning Officers District AC No Name of the Assembly Constituency Email of Returning Officer Contact No. KANCHEEPURAM 27 Shozhinganallur [email protected] -

Chapter 3 Tirumurai 7 Sundaramurti Thevaram

Language in India 18:11 November 2018 CHAPTER 3 TIRUMURAI 7 SUNDARAMURTI (THEVARAM) Dr Adi Sankara Singing with Saivite Saints Language in India 18:11 November 2018 Sundaramurti - Tiruvennainallur Dr Adi Sankara Singing with Saivite Saints Language in India 18:11 November 2018 Singing with Saivite Saints 45 SUNDARAMURTI Sundaramurti Nayanar was born in Tirunavarur to Sadaiyanar a Saivite priest and his wife Isaignani. The sthala was called Tirutturaiyur and now is known as Tiruttalur. It is situated on the Villupuram-Cuddalore rail route. Sundarar was then named Nambi Arurar after his grandfather. According to the Siva Puranam, Sundarar is said to be the celestial that collected the poison (Halahala) in his hand and gave it to Lord Siva who absorbed it to protect the world. According to Lord Siva’s wish, Sundarar was to be born as a human being to sing the Tiru Thondat Thogai for the benefi t of mankind. So, when the servants of Goddess Parvati, Aninditi and Kamalini were gathering flowers in Mount Kailash, Sundarar gazed at them. They too, reciprocated his love. God Siva sent them to Earth to take human birth. It happened that one day, King Narasinga Munaiyar who was passing by, noticed the cute child playing with a temple car toy on the streets. The King was at once attracted by the child. He told the parents of Sundarar that he wanted to bring up the small boy. Sadaiyanar and Isaignani agreed to the King’s wish, as they were not attached to anything in the world. Sundarar grew under royal care and was brought up like a prince.