E. What Role for International Cooperation on Services Trade Policy?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Great Divergence the Princeton Economic History

THE GREAT DIVERGENCE THE PRINCETON ECONOMIC HISTORY OF THE WESTERN WORLD Joel Mokyr, Editor Growth in a Traditional Society: The French Countryside, 1450–1815, by Philip T. Hoffman The Vanishing Irish: Households, Migration, and the Rural Economy in Ireland, 1850–1914, by Timothy W. Guinnane Black ’47 and Beyond: The Great Irish Famine in History, Economy, and Memory, by Cormac k Gráda The Great Divergence: China, Europe, and the Making of the Modern World Economy, by Kenneth Pomeranz THE GREAT DIVERGENCE CHINA, EUROPE, AND THE MAKING OF THE MODERN WORLD ECONOMY Kenneth Pomeranz PRINCETON UNIVERSITY PRESS PRINCETON AND OXFORD COPYRIGHT 2000 BY PRINCETON UNIVERSITY PRESS PUBLISHED BY PRINCETON UNIVERSITY PRESS, 41 WILLIAM STREET, PRINCETON, NEW JERSEY 08540 IN THE UNITED KINGDOM: PRINCETON UNIVERSITY PRESS, 3 MARKET PLACE, WOODSTOCK, OXFORDSHIRE OX20 1SY ALL RIGHTS RESERVED LIBRARY OF CONGRESS CATALOGING-IN-PUBLICATION DATA POMERANZ, KENNETH THE GREAT DIVERGENCE : CHINA, EUROPE, AND THE MAKING OF THE MODERN WORLD ECONOMY / KENNETH POMERANZ. P. CM. — (THE PRINCETON ECONOMIC HISTORY OF THE WESTERN WORLD) INCLUDES BIBLIOGRAPHICAL REFERENCES AND INDEX. ISBN 0-691-00543-5 (CL : ALK. PAPER) 1. EUROPE—ECONOMIC CONDITIONS—18TH CENTURY. 2. EUROPE—ECONOMIC CONDITIONS—19TH CENTURY. 3. CHINA— ECONOMIC CONDITIONS—1644–1912. 4. ECONOMIC DEVELOPMENT—HISTORY. 5. COMPARATIVE ECONOMICS. I. TITLE. II. SERIES. HC240.P5965 2000 337—DC21 99-27681 THIS BOOK HAS BEEN COMPOSED IN TIMES ROMAN THE PAPER USED IN THIS PUBLICATION MEETS THE MINIMUM REQUIREMENTS OF ANSI/NISO Z39.48-1992 (R1997) (PERMANENCE OF PAPER) WWW.PUP.PRINCETON.EDU PRINTED IN THE UNITED STATES OF AMERICA 3579108642 Disclaimer: Some images in the original version of this book are not available for inclusion in the eBook. -

The First Great Divergence

Mellon-Sawyer Seminar 2007/8 “The first great divergence: China and Europe, 500-800 CE” Organized by Ian Morris, Walter Scheidel, and Mark Lewis, Departments of Classics and History, Stanford University Sponsored by the Andrew W. Mellon Foundation Six hundred years ago China was the most powerful state on earth. The eunuch admiral Zheng He spent 1406 cruising around the Indian Ocean at the head of 30,000 crew in a fleet of giant Chinese “treasure ships,” trading, collecting tribute, and setting up and deposing client kings at will. By 1433, Chinese ships were visiting Arabia, Ethiopia, and Kenya, and probably Australia too. By any reasonable estimate, China seemed set to become the world’s first global power. But that did not happen. Anti-trade Confucian factions won out in struggles at the Ming court, and long-distance voyages were banned. By 1467, most records of Zheng’s voyages were lost or destroyed. Half a millennium later, far from dominating as the world, China seemed – at least to western observers – to be going backward. When a dispute over opium trading escalated uncontrollably in 1839, the British sent a small naval force to claim damages from the governor of Canton. A single ironclad gunboat blasted its way through all the Chinese defenses, and in 1842, with the Grand Canal under British control, Nanjing facing plunder, and famine closing in on Beijing, China conceded British demands for open ports and the right to send missionaries deep into the country. This defeat triggered crises that brought China to the verge of partition. One Hong Xiuquan, a failed civil service candidate who developed his own bizarre version of Christianity out of the teachings of the missionaries at Canton, led the massive Taiping Rebellion to install a Heavenly Kingdom of Great Peace. -

The Basic Economics of Internet Infrastructure

Journal of Economic Perspectives—Volume 34, Number 2—Spring 2020—Pages 192–214 The Basic Economics of Internet Infrastructure Shane Greenstein his internet barely existed in a commercial sense 25 years ago. In the mid- 1990s, when the data packets travelled to users over dial-up, the main internet T traffic consisted of email, file transfer, and a few web applications. For such content, users typically could tolerate delays. Of course, the internet today is a vast and interconnected system of software applications and computing devices, which society uses to exchange information and services to support business, shopping, and leisure. Not only does data traffic for streaming, video, and gaming applications comprise the majority of traffic for internet service providers and reach users primarily through broadband lines, but typically those users would not tolerate delays in these applica- tions (for usage statistics, see Nevo, Turner, and Williams 2016; McManus et al. 2018; Huston 2017). In recent years, the rise of smartphones and Wi-Fi access has supported growth of an enormous range of new businesses in the “sharing economy” (like, Uber, Lyft, and Airbnb), in mobile information services (like, social media, ticketing, and messaging), and in many other applications. More than 80 percent of US households own at least one smartphone, rising from virtually zero in 2007 (available at the Pew Research Center 2019 Mobile Fact Sheet). More than 86 percent of homes with access to broadband internet employ some form of Wi-Fi for accessing applications (Internet and Television Association 2018). It seems likely that standard procedures for GDP accounting underestimate the output of the internet, including the output affiliated with “free” goods and the restructuring of economic activity wrought by changes in the composition of firms who use advertising (for discussion, see Nakamura, Samuels, and Soloveichik ■ Shane Greenstein is the Martin Marshall Professor of Business Administration, Harvard Business School, Boston, Massachusetts. -

Employment Situation of Veterans — 2020

For release 10:00 a.m. (ET) Thursday, March 18, 2021 USDL-21-0438 Technical information: (202) 691-6378 • [email protected] • www.bls.gov/cps Media contact: (202) 691-5902 • [email protected] EMPLOYMENT SITUATION OF VETERANS — 2020 The unemployment rate for veterans who served on active duty in the U.S. Armed Forces at any time since September 2001—a group referred to as Gulf War-era II veterans—rose to 7.3 percent in 2020, the U.S. Bureau of Labor Statistics reported today. The jobless rate for all veterans increased to 6.5 percent in 2020. These increases reflect the effect of the coronavirus (COVID- 19) pandemic on the labor market. In August 2020, 40 percent of Gulf War-era II veterans had a service-connected disability, compared with 26 percent of all veterans. This information was obtained from the Current Population Survey (CPS), a monthly sample survey of about 60,000 eligible households that provides data on employment, unemployment, and persons not in the labor force in the United States. Data about veterans are collected monthly in the CPS; these monthly data are the source of the 2020 annual averages presented in this news release. In August 2020, a supplement to the CPS collected additional information about veterans on topics such as service-connected disability and veterans' current or past Reserve or National Guard membership. Information from the supplement is also presented in this news release. The supplement was co-sponsored by the U.S. Department of Veterans Affairs and the U.S. Department of Labor's Veterans' Employment and Training Service. -

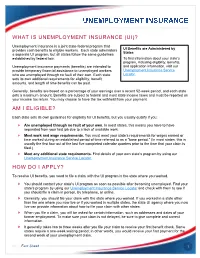

What Is Unemployment Insurance (Ui)? Am I Eligible? How Do I Apply?

WHAT IS UNEMPLOYMENT INSURANCE (UI)? Unemployment Insurance is a joint state-federal program that provides cash benefits to eligible workers. Each state administers UI Benefits are Administered by States a separate UI program, but all states follow the same guidelines established by federal law. To find information about your state’s program, including eligibility, benefits, Unemployment insurance payments (benefits) are intended to and application information, visit our provide temporary financial assistance to unemployed workers Unemployment Insurance Service who are unemployed through no fault of their own. Each state Locator. sets its own additional requirements for eligibility, benefit amounts, and length of time benefits can be paid. Generally, benefits are based on a percentage of your earnings over a recent 52-week period, and each state sets a maximum amount. Benefits are subject to federal and most state income taxes and must be reported on your income tax return. You may choose to have the tax withheld from your payment. AM I ELIGIBLE? Each state sets its own guidelines for eligibility for UI benefits, but you usually qualify if you: Are unemployed through no fault of your own. In most states, this means you have to have separated from your last job due to a lack of available work. Meet work and wage requirements. You must meet your state’s requirements for wages earned or time worked during an established period of time referred to as a "base period." (In most states, this is usually the first four out of the last five completed calendar quarters prior to the time that your claim is filed.) Meet any additional state requirements. -

A Glossary of Fiscal Terms & Acronyms

AUGUST7,1998VOLUME13,NO .VII A Publication of the House Fiscal Analysis Department on Government Finance Issues A GLOSSARY OF FISCAL TERMS & ACRONYMS 1998 Revised Edition Abstract. This issue of Money Matters is a resource document containing terms and acronyms commonly used by and in legislative fiscal committees and in the discussion of state budget and tax issues. The first section contains terms and abbreviations used in all fiscal committees and divisions. The remaining sections contain terms for particular budget categories and accounts, organized according to fiscal subject areas. This edition has new sections containing economic development, family and early childhood, and housing terms and acronyms. The other sections are revised and updated to reflect changes in terminology, particularly the human services section. For further information, contact the Chief Fiscal Analyst or the fiscal analyst assigned to the respective House fiscal committee or division. A directory of House Fiscal Analysis Department personnel and their committee/division assignments for the 1998 legislative session appears on the next page. Originally issued January 1997 Revised August 1998 House Fiscal Analysis Department Staff Assignments — 1998 Session Committee/Division Fiscal Analyst Telephone Room Chief Fiscal Analyst Bill Marx 296-7176 373 Capital Investment John Walz 296-8236 376 EDIT— Economic Development Finance CJ Eisenbarth Hager 296-5813 428 EDIT— Housing Finance Cynthia Coronado 296-5384 361 Environment & Natural Resources Finance Jim Reinholdz 296-4119 370 Education — Higher Education Finance Doug Berg 296-5346 372 K-12 Education Finance Greg Crowe 296-7165 378 Family & Early Childhood Finance Cynthia Coronado 296-5384 361 Health & Human Services Finance Joe Flores 296-5483 385 Judiciary Finance Gary Karger 296-4181 383 State Government Finance Helen Roberts 296-4117 374 Transportation Finance John Walz 296-8236 376 Taxes — Income, sales, misc. -

The Revenue Functions of a Monopoly

SOLUTIONS 3 Microeconomics ACTIVITY 3-10 The Revenue Functions of a Monopoly At the opposite end of the market spectrum from perfect competition is monopoly. A monopoly exists when only one firm sells the good or service. This means the monopolist faces the market demand curve since it has no competition from other firms. If the monopolist wants to sell more of its product, it will have to lower its price. As a result, the price (P) at which an extra unit of output (Q) is sold will be greater than the marginal revenue (MR) from that unit. Student Alert: P is greater than MR for a monopolist. 1. Table 3-10.1 has information about the demand and revenue functions of the Moonglow Monopoly Company. Complete the table. Assume the monopoly charges each buyer the same P (i.e., there is no price discrimination). Enter the MR values at the higher of the two Q levels. For example, since total revenue (TR) increases by $37.50 when the firm increases Q from two to three units, put “+$37.50” in the MR column for Q = 3. Table 3-10.1 The Moonglow Monopoly Company Average revenue Q P TR MR (AR) 0 $100.00 $0.00 – – 1 $87.50 $87.50 +$87.50 $87.50 2 $75.00 $150.00 +$62.50 $75.00 3 $62.50 $187.50 +$37.50 $62.50 4 $50.00 $200.00 +$12.50 $50.00 5 $37.50 $187.50 –$12.50 $37.50 6 $25.00 $150.00 –$37.50 $25.00 7 $12.50 $87.50 –$62.50 $12.50 8 $0.00 $0.00 –$87.50 $0.00 2. -

OECD Recommendation on Public Service Leadership and Capability

OECD Recommendation on Public Service Leadership and Capability Photo credit / © Shutterstock credit Photo OECD Member countries invest ministries and agencies have a workforce with The Recommendation on PSLC is based on public servants, citizens and experts worldwide. considerable resources in public the capabilities needed now and in the future. a set of commonly shared principles, which The Recommendation presents 14 principles for a employment. have been developed in close consultation fit-for-purpose public service under 3 main pillars: Finally, the Recommendation places a heavy with OECD Member countries. onus on public service leaders, who require 1. Values-driven culture and leadership, In 2015, an average of 9.5% of GDP the mandate, competencies, and conditions The development of the Recommendation also 2. Skilled and effective public servants, was spent in OECD Member countries necessary to provide impartial evidence- benefitted from a broad public consultation, 3. Responsive and adaptive public on general government employee informed advice and speak truth to power. which generated a high level of input from employment systems. compensation, making this the largest input in the production of government goods and services. Historically, this investment has helped to support economic growth and stability. Public servants have been a major actor in modern society’s greatest achievements: health care, education and childcare, access to water and sanitation, energy, VALUES-DRIVEN CULTURE SKILLED AND EFFECTIVE RESPONSIVE AND communication, response to disasters, AND LEADERSHIP PUBLIC SERVANTS ADAPTIVE PUBLIC science and technology, among EMPLOYMENT SYSTEMS others. This underlines the fact that a professional, capable and responsive public service is a fundamental driver of citizens’ trust in public institutions. -

1St Grade Goods and Services

Social Studies Virtual Learning 1st Grade Goods and Services April 6, 2020 1st Grade Social Studies Lesson: April 6, 2020 Learning Target: Students describe examples of goods and services within our school and community Background: This is a new objective in 4th quarter ● Students learn about community in 1st grade ● Students learn about being an active member of the school in 1st grade ● Students learn about being an active member of the community in 1st grade Let’s Get Started: Click this for directions! Watch Videos: 1. Goods and Services 2. Goods and ServicesBrainPopJr.: Goods and Services Click this for Practice #1: directions! Watch Moby and Annie teach us about Goods and Services again. Take the EASY QUIZ when you are finished. Click this for directions. Goods are things Practice #2: Is it a GOOD or a SERVICE? Tell a grown up at your home. that are made or grown. Services are something useful that people do for others. Practice #3: Click this for What goods and services does Mouse want? directions. Listen to the story If You Give a Mouse a Cookie by Laura Numeroff. Does he want more goods or services? Click here for directions. Practice on your own: BrainPopJr.: Goods and Services 1. Click the link and go to Draw About It. 2. Draw about a good or service that you would like to provide for the community. Click this for directions. MORE Practice on your own: Go to this website: BrainPopJr.: Goods and Services 1. Go to Word Play. 2. Draw or write about goods. 3. -

Public Service Leadership and Capability 8

Recommendation of the Council on Public Service Leadership and Capability 8 OECD Legal Instruments This document is published under the responsibility of the Secretary-General of the OECD. It reproduces an OECD Legal Instrument and may contain additional material. The opinions expressed and arguments employed in the additional material do not necessarily reflect the official views of OECD Member countries. This document, as well as any data and any map included herein, are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. For access to the official and upto-date texts of OECD Legal Instruments, as well as other related information, please consult the Compendium of OECD Legal Instruments at http://legalinstruments.oecd.org. Please cite this document as: OECD, Recommendation of the Council on Public Service Leadership and Capability, OECD/LEGAL/0445 Series: OECD Legal Instruments © OECD 2019 This document is provided free of charge. It may be reproduced and distributed free of charge without requiring any further permissions, as long as it is not altered in any way. It may not be sold. This document is available in the two OECD official languages (English and French). It may be translated into other languages, as long as the translation is labelled "unofficial translation" and includes the following disclaimer: "This translation has been prepared by [NAME OF TRANSLATION AUTHOR] for informational purpose only and its accuracy cannot be guaranteed by the OECD. The only official versions are the English and French texts available on the OECD website http://legalinstruments.oecd.org" Date(s) Adopted on 17/01/2019 Background Information The Recommendation on Public Service Leadership and Capability was adopted on 17 January 2019 by the Council on proposal of the Public Governance Committee. -

Mail Use & Attitudes in FY 2012

TheThe HouseholdHousehold DiarDiaryy StudyStudy MailMail UseUse && AttitudesAttitudes inin FYFY 20122012 John Mazzone - Financial Economist Samie Rehman - Manager, Revenue and Volume Forecasting Finance and Planning Department United States Postal Service Headquarters 475 L’Enfant Plaza, SW RM 8441 Washington, D.C. 20260-5323 May 2013, Contract #102592-02-B-1502 NuStats 206 Wild Basin Road, Suite A-300 Austin, Texas 78746 Table of Contents E Executive Summary 1 Background 1 Overview 1 Mail Markets 1 1 Chapter 1: Introduction – Volumes & Trends 5 The Survey 5 U.S. Postal Service Volumes 5 Mail Flows 10 Household Mail 10 Classes and Markets 11 Report Organization 12 2 Chapter 2: Profile of Mail Usage 13 Introduction 13 Mail Volume and Demographics 13 Characteristics of Higher- and Lower-Volume Households 14 Demographic Characteristics of U.S. Households 15 Use of the Post Office 18 3 Chapter 3: Correspondence 21 Introduction 21 Correspondence Mail Volume 21 Correspondence Mail and Household Characteristics 21 Personal Correspondence 25 Business Correspondence 28 4 Chapter 4: Transactions 29 Introduction 29 Transactions Mail Volume 29 Transactions Mail and Household Characteristics 30 Bill Payment 32 Bills and Statements Received 36 5 Chapter 5: Advertising Mail 39 Introduction 39 The Advertising Market 39 Advertising Mail Volumes 40 Advertising Mail and Household Characteristics 41 Senders of Advertising Mail 43 Attitudes toward Advertising 44 Effectiveness of Advertising Mail 46 2012 HOUSEHOLD DIARY STUDY Table of Contents 6 Chapter 6: Periodicals 47 Introduction 47 The Periodicals Market 47 Advertising’s Impact on Periodicals 48 Household Periodicals Volume 48 Periodicals Mail and Household Characteristics 50 Subscription Type 52 Volume Drivers 53 7 Chapter 7: Packages 55 Introduction 55 The Package Market 55 Postal Service Package Volume 57 Packages and Household Characteristics 59 Household Package Contents 62 A Appendix A: Comparative Tables 1987, 2011 & 2012 Concordance A1. -

Household Service Vouchers, Austria

Household Service Vouchers, Austria Title of the policy or measure (in Household Service Vouchers (Dienstleistungsscheck) English) Country Austria Sectors Maintenance and cleaning What groups are targeted by - Workers in the personal and household service sector the measure - Families using personal and household services Purpose of measure Legitimising undeclared work Short sentence summarising The household service vouchers are used by households to pay for personal the measure and household services (i.e. childcare, gardening, cleaning etc.). This scheme aims to curb undeclared work, improve the social protection of workers in the sector and to increase employment opportunities. Background Background context driving In 2006, only around 10 000 out of more than 150 000 household workers the implementation of the were legally employed.i In order to legitimise work in the sector, household measure service vouchers were introduced to reduce undeclared work and to improve domestic workers' social protection. When was the measure Since 2006 – ongoing implemented? (including start date and end date/ongoing) Names(s) of The Insurance Association for Railways and Mining Workers authorities/bodies/organisatio (“Versicherungsanstalt für Eisenbahnen und Bergbau” –VAEB) is responsible ns involved for the implementation of the scheme. Scope of the measure (a pilot National project, nationwide, regional wide) Type of (policy) measure Tool If “other”, please specify: Service Voucher Key objectives of the measure The service vouchers legitimise personal and household services, giving people working in households access to accident insurance and voluntary health and pension insurance. Specific measure Description of how the People who perform services like cleaning, shopping, gardening or childcare in measure operates in practice other people’s households receive household service vouchers as compensation.