Competitive Advantage the Cambridge Cluster Report – 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fuller's Hill Cottages Access Statement

Fuller’s Hill Cottages Access Statement CONTENTS: Contents page 2 Introduction 3 Accommodation: The Stables, The Tack Room & Garden 4 Useful, local telephone numbers 9 Local pubic transport 10 Visiting Cambridge 11 Parking in Cambridge 12 Other useful contacts 15 Restaurants, pubs and bars in Cambridge 19 Churches 33 Cinemas 37 Concert venues 40 Guided Tours 48 Museums & galleries in Cambridge 50 Parks & gardens 62 Places of interest outside Cambridge 65 Shopping in Cambridge 75 Sports centres 82 Theatres 85 Transport in Cambridge 91 University Colleges 94 For more information… 105 2 FULLER’S HILL COTTAGES’ ACCESS STATEMENT Fuller’s Hill Cottages is a large converted 1840 barn, made into four, luxury cottages, which were opened in 2012. Two of our cottages are disabled accessible; The Stables and The Tack Room. We have tried to provide as much information as possible in this statement but if you have any queries please do call Jenny Jefferies on 07544 208959. We look forward to welcoming you. Pre – Arrival Bookings/enquiries can be made via either website or by direct telephone to Jenny on 07544 208959. It is possible to do your grocery shopping through www.tesco.com or www.asda.co.uk or www.Sainsburys.co.uk. Delivery should be made after your arrival time. Alternatively we can arrange for a deluxe or standard breakfast hamper to be in your cottage for your arrival. We can also arrange for a personalised Supper Box to be delivered - please contact Jenny for further details. Arrival & Car Parking Facilities You may park your car directly in front of each apartment The Car Park is level and pebble-dashed, with space for around 12 cars The Car Park lighting at night is by remote sensors that come on automatically. -

Pooled CRISPR-Activation Screening Coupled with Single-Cell RNA-Seq in Mouse Embryonic Stem Cells

ll OPEN ACCESS Protocol Pooled CRISPR-activation screening coupled with single-cell RNA-seq in mouse embryonic stem cells Celia Alda-Catalinas, Melanie A. Eckersley-Maslin, Wolf Reik celia.x.aldacatalinas@gsk. com (C.A.-C.) [email protected]. uk (W.R.) Highlights Protocol for CRISPRa screens with single- cell readout to interrogate gene function Detailed description of CRISPRa screening procedures in mouse embryonic stem cells Detailed steps on how to construct derived single-cell sgRNA amplicon libraries CRISPR/Cas9 screens are a powerful approach to identify key regulators of biological processes. By combining pooled CRISPR/Cas9 screening with a single-cell RNA-sequencing readout, individual perturbations can be assessed in parallel both comprehensively and at scale. Importantly, this allows gene function and regulation to be interrogated at a cellular level in an unbiased manner. Here, we present a protocol to perform pooled CRISPR-activation screens in mouse embryonic stem cells using 103 Genomics scRNA-seq as a readout. Alda-Catalinas et al., STAR Protocols 2, 100426 June 18, 2021 ª 2021 The Authors. https://doi.org/10.1016/ j.xpro.2021.100426 ll OPEN ACCESS Protocol Pooled CRISPR-activation screening coupled with single-cell RNA-seq in mouse embryonic stem cells Celia Alda-Catalinas,1,4,7,* Melanie A. Eckersley-Maslin,1,5,6 and Wolf Reik1,2,3,8,* 1Epigenetics Programme, Babraham Institute, Cambridge CB22 3AT, UK 2Wellcome Trust Sanger Institute, Hinxton, Cambridge CB10 1SA, UK 3Centre for Trophoblast Research, University of -

The Oxford – Cambridge Arc Home of the New Innovation Economy

Economic Vision: The Oxford – Cambridge Arc Home of the New Innovation Economy April 2019 Contents 1 Introduction 3 2 The Economic Vision 8 3 The New Innovation Economy: Sectors 11 4 The Innovation & Growth Network 24 5 Achieving Ambitions 29 6 Conclusion: Critical Mass 35 | Introduction 1 Introduction 1.1 This vision’s purpose The purpose of the Economic Vision is to explain the Oxford - Cambridge Arc’s unified proposition as a globally leading innovation and growth catalyst. The Arc offers access to each of the critical ingredients for business and innovation-led growth. This collective offer represents a powerful and coherent expression of the region’s current assets and future potential. This Economic Vision for the Arc sets out an ambition and series of proposals designed to unlock the economic potential of the region and deliver transformative growth for the UK between now and 2050. It provides a vision for how the Arc can better connect its unique and world-leading assets to become truly globally competitive in frontier markets, both for business investment and for top talent. With a bolder brand and stronger international presence the Arc can continue to lead the whole of the UK to the forefront of global innovation excellence in the coming years and decades. 3 | Introduction This Economic Vision is built upon the foundation of This Economic Vision has been developed in the four local industrial strategies which currently partnership with the three LEPs and the Combined demarcate the Arc’s geographic area. These have Authority, who have been given a mandate by Central been prepared by the Oxfordshire (OxLEP), South Government to drive forwards the Economic Vision for East Midlands (SEMLEP) and Buckinghamshire the Arc: Thames Valley (BTVLEP) Local Enterprise Partnerships, as well as the Cambridgeshire & Peterborough Mayoral Combined Authority (CPCA). -

Aaa Worldwise

AAA FALL 2017 WORLDWISE Route 66 Revival p. 32 Dressing for Access p. 38 South Africa: A Tale of Two Cities p. 48 TWO OF A KIND: THE ORIGINAL COLLEGE TOWNS Cambridge MASSACHUSETTS Just north of Boston and home to Harvard University and the Massachusetts Institute of Technology, this city oozes intellectualism and college spirit. COURTESY OF HARVARD UNIVERSITY HARVARD OF COURTESY Harvard and the Charles River STAY SEE When celebs come to Harvard, they’re put up at Harvard University’s three venerable art the AAA Four Diamond Charles Hotel. Just museums were brought under one roof in minutes from Harvard Yard, The Charles has a 2014 and collectively dubbed the Harvard well-stocked in-house library and one of the best Art Museums. Their collections include some breakfasts in town at Henrietta’s Table. The 250,000 art works dating from ancient times to 31-room luxury Hotel Veritas—described by the present and spanning the globe. The MIT a GQ magazine review as “a classic Victorian Museum, not surprisingly, focuses on science and mansion that went to Art Deco finishing technology. It includes the Polaroid Historical school”—boasts 24-hour concierge service Collection of cameras and photographs, the COURTESY OF HOTEL VERITAS HOTEL OF COURTESY and a location in Harvard Square. Those who MIT Robotics Collection and the world’s Hotel Veritas prefer to bed down near the Massachusetts most comprehensive holography collection. Institute of Technology (MIT) should check in Beyond the universities, visit the Longfellow at The Kendall Hotel, which brings boutique House–Washington’s Headquarters, the accommodations to a converted 19th-century preserved, furnished home of 19th-century poet firehouse. -

Minutes of the Proceedings

MINUTES OF THE PROCEEDINGS at the Thirty‐sixth Meeting of the COUNCIL of the IMPERIAL COLLEGE OF SCIENCE, TECHNOLOGY AND MEDICINE The Thirty‐sixth Meeting of the Council was held in the Council Room, 170 Queen’s Gate, South Kensington Campus, Imperial College London, at 10:00 a.m. on Friday, 16th May 2014, when there were present: The Baroness Manningham‐Buller (Chair), Professor A. Anandalingam, Mr. C. Brinsmead, Dame Ruth Carnall, Mrs. P. Couttie, Professor M.J. Dallman, Mr. P. Dilley, Mr. D. Goldsmith, Professor N. Gooderham, Professor Dame Julia Higgins, Professor D.P.A. Kelleher, Ms. J.R. Lomax, Professor J. Magee, Mr. J. Newsum, Mr. S. Newton, Ms. K. Owen, Mr. M. Sanderson, Professor J Stirling, the President & Rector and the Clerk to the Court and Council. Apologies Mr. I. Conn. MINUTES Council – 7th February 2014 1. The Minutes of the thirty‐fifth Meeting of the Council, held on Friday, 7th February 2014, were taken as read, confirmed and signed. CHAIR’S REPORT 2. The Chair advised members that, following his appointment as Chair of the Chelsea and Westminster Hospital NHS Foundation Trust, Sir Thomas Hughes‐Hallett had resigned as a co‐opted member of the Council on 11 February. PRESIDENT & RECTOR’S REPORT 3. The President & Rector reported that this year’s Imperial Festival, held on 9th and 10th May, had received many visitors at the South Kensington campus to enjoy the various demonstrations, talks 1 Council 16th May 2014 and other activities on offer. What had started as a relatively modest pilot project in 2012 to explore how Imperial College London might share its research with more people had now evolved into a large‐scale and prominent annual fixture in the College’s calendar. -

Medical Research Council Annual Report and Accounts 2006/07 HC 93

06/07 Annual Report and Accounts © Crown Copyright 2006 The text in this document (excluding any Royal Arms and departmental logos) may be reproduced free of charge in any format or medium providing that it is reproduced accurately and not used in a misleading context. The material must be acknowledged as Crown copyright and the title of the document specified. Any queries relating to the copyright in this document should be addressed to The Licensing Division, HMSO, St Clements House, 2-16 Colegate, Norwich, NR3 1BQ. Fax: 01603 723000 or e-mail: licensing@cabinet-office.x.gsi.gov.uk 2 MRC Annual Report and Accounts 2006/07 Medical Research Council Annual Report and Accounts 2006/07 Presented to Parliament by the Secretary of State, and by the Comptroller and Auditor General in pursuance of Schedule I, Sections 2(2) and 3(3) of the Science and Technology Act 1965. Sir John Chisholm Chairman Professor Sir Leszek Borysiewicz Deputy Chairman and Chief Executive Ordered by and printed on London: The Stationery Office 6 February 2008 Price: £18.55 HC 93 The Medical Research Council The MRC RCUK The Medical Research Council (MRC) was set up in 1913 to administer Research Councils UK (RCUK) is a partnership of the seven (formerly public funds for medical research. It was incorporated under its eight) UK Research Councils – public bodies funded mainly by the UK present title by Royal Charter in 1920. A supplemental charter was Government via OSI. granted in 1993 describing the MRC’s new mission following the 1993 government white paper on science and technology. -

Central Cambridge: a Guide to the University and Colleges: Second Edition Kevin Taylor Frontmatter More Information

Cambridge University Press 978-0-521-88876-9 - Central Cambridge: A Guide to the University and Colleges: Second Edition Kevin Taylor Frontmatter More information Central Cambridge A Guide to the University and Colleges SECOND EDITION Kevin Taylor © in this web service Cambridge University Press www.cambridge.org Cambridge University Press 978-0-521-88876-9 - Central Cambridge: A Guide to the University and Colleges: Second Edition Kevin Taylor Frontmatter More information University Printing House, Cambridge CB2 8BS, United Kingdom Published in the United States of America by Cambridge University Press, New York Cambridge University Press is part of the University of Cambridge. It furthers the University’s mission by disseminating knowledge in the pursuit of education, learning and research at the highest international levels of excellence. www.cambridge.org Information on this title: www.cambridge.org/9780521717182 © Cambridge University Press 2008 This publication is in copyright. Subject to statutory exception and to the provisions of relevant collective licensing agreements, no reproduction of any part may take place without the written permission of Cambridge University Press. First edition published 1994 (reprinted 1996, 1997, 1999, 2003, 2004) Second edition published 2008 (reprinted 2011) 5th printing 2015 Printed in the United Kingdom by Bell and Bain Ltd, Glasgow A catalogue record for this publication is available from the British Library ISBN 978-0-521-88876-9 hardback ISBN 978-0-521-71718-2 paperback II © in this web service Cambridge University Press www.cambridge.org Cambridge University Press 978-0-521-88876-9 - Central Cambridge: A Guide to the University and Colleges: Second Edition Kevin Taylor Frontmatter More information Contents General map of Cambridge Inside front cover Foreword by H.R.H. -

Expenditure by Institution (Summary)

18 January 2011 CAMBRIDGE UNIVERSITY REPORTER 17 Section C: Expenditure by Institution (summary) Note that this analysis takes into account financial accounting adjustments in respect of: the elimination of internal charges; capital expenditure; and depreciation. Costs by activity 2009–10 (£000) Costs by type 2009–10 (£000) Research Adminis- grants tration and Other Total costs Academic Academic and Other central Staff operating Deprec- Interest Total costs 2008–09 departments services contracts activities services Premises costs expenses iation payable 2009–10 (£000) ACADEMIC DEPARTMENTS SCHOOL OF ARTS AND HUMANITIES 231 – – – 7 (13) 197 28 – – 225 277 Anglo-Saxon, Norse and Celtic 634 6 79 10 20 – 669 80 – – 749 763 Architecture 1,309 1 1,547 87 (8) 5 1,725 1,216 – – 2,941 2,933 Architecture and History of Art 458 62 2 16 – 88 417 182 27 – 626 727 Classics and Classical Archaeology 2,927 183 526 83 250 38 3,386 621 – – 4,007 3,808 Divinity 2,319 130 717 29 184 70 2,562 887 – – 3,449 3,305 East Asian Studies 1,266 – – 16 8 – 1,101 189 – – 1,290 1,297 English 3,239 203 240 23 89 78 3,509 351 12 – 3,872 3,726 French 1,302 – 162 8 2 – 1,411 63 – – 1,474 1,438 German 852 3 38 – 5 – 873 25 – – 898 908 History of Art 517 – 29 17 7 – 528 42 – – 570 496 Italian 544 – 44 2 – – 574 16 – – 590 549 Linguistics 508 – 304 31 – – 719 124 – – 843 810 Middle Eastern Studies 961 1 – 1 78 – 840 201 – – 1,041 983 Modern and Medieval Languages 674 188 – 18 77 2 733 226 – – 959 889 Music 1,438 114 134 134 36 67 1,527 372 24 – 1,923 1,619 Oriental Studies -

FOI Ref 6871 Response Sent 17 March Can You Please Provide The

FOI Ref 6871 Response sent 17 March Can you please provide the following details from the most recent records which you hold under The Licensing Act 2003: On-trade alcohol licensed premises, including: Premises Licence Number Date Issued Premises Licence Status (active, expired etc.) Premises Name Premises Address Premises Postcode Premises Telephone Number Premises on-trade Category (e.g. Cafe, Bar, Theatre, Nightclub etc.) Premises Licence Holder Name Premises Licence Holder Address Premises Licence Holder Postcode Designated Premises Supervisor Name Designated Premises Supervisor Address Designated Premises Supervisor Postcode The information you have requested is held and in the attached. However the personal information relating to Designated Premises Supervisors you have requested is refused under the exemption to disclosure at Section 40(2) of the Act Further queries on this matter should be directed to [email protected] Full address Telephone number Licence type Status Date issued Licence holder 1 and 1 Rougamo Ltd, 84 Regent Street, Cambridge, 07730029914 Premises Licence Current Licence 10/03/2020 Yao Qin Cambridgeshire, CB2 1DP 2648 Cambridge, 14A Trinity Street, Cambridge, 01223 506090 Premises Licence Current Registration 03/10/2005 The New Vaults Limited Cambridgeshire, CB2 1TB 2nd View Cafe - Waterstones, 20-22 Sidney Street, Premises Licence Current Registration 17/09/2010 Waterstones Booksellers Ltd Cambridge, Cambridgeshire, CB2 3HG ADC Theatre, Park Street, Cambridge, Cambridgeshire, CB5 01223 359547 Premises Licence -

Michael John Owen Wakelam 1955–2020

obituary Michael John Owen Wakelam 1955–2020 We have lost a distinguished biochemist who dedicated his career to the study of phosphatidylinositol signalling in metabolic regulation and to the advancement of lipidomics. ichael John Owen Wakelam passed away on 31 March, 2020 at the Mage of 64, much too early. He became known to colleagues and friends as a scientist highly regarded for his research. He was honoured in 2018 with the Morton Lectureship of the Biochemical Society and was elected a fellow of the Royal Society of Biology. In 2019, he was elected a member of the Academia Europaea. Academic career It was not by chance that Michael turned his focus to phosphatidylinositols (PIs) and lipid signalling. He was a student and later a professor at the University of Birmingham at a time when Britain was the world’s hub of pioneering phospholipid research, such as that by J. N. Hawthorne and Bob Michell on PI in Birmingham. Bob Michell inspired Michael extraordinarily, and they even published a joint review. Subsequently, Michael moved to Cambridge to serve as the director of the Babraham Institute, where Credit: Babraham Institute Rex Dawson and Robin Irvine studied phospholipids, particularly PI metabolism and signalling. A joint publication by Michael and Irvine appeared as well. the Babraham Institute, and he received an the Keystone Symposia on Molecular and Certainly, Michael’s scientific engagement honorary professorship in lipid signalling at Cellular Biology. can be seen in the tradition of these eminent the University of Cambridge Clinical School. phospholipid scientists. In addition, he was an honorary professor Lipid signalling and metabolism Michael’s career path is impressive. -

New VC Nominated Save Popular Post » Top Medical Scientist Set to Be 345Th Vice-Chancellor Office

Sportp30-32 Noughties reviewedp13-15 Featuresp20 Varsity match As the first decade of the new millenium draws Britain’s finest preview: profiling the to a close, we look over the cultural triumphs of stage actor Simon players and weighing the naughty years Russell Beale on up our odds for ‘chutzpah’ and the Twickenham need to be directed Friday November 27th 2009 e Independent Student Newspaper since 1947 Issue no 708 | varsity.co.uk BEATRICE RAMSAY Trinity steps in to New VC nominated save popular post » Top medical scientist set to be 345th Vice-Chancellor office the College’s academic and scientifi c Emma Mustich development, focusing especially on Jenny Morgan News Editor fostering interdisciplinary research Associate Editor between medicine and other science subjects. COLLEGE ProfessorCOLLEGE Sir Leszek Borysiewicz Born in Wales, Borysiewicz has Trinity Street Post Offi ce has been has been nominated to replace Alison previously worked as Head of the saved from closure this Christmas Richard as Vice-Chancellor of the Department of Medicine at the Uni- after a last-minute intervention University. versity of Wales, and was Lecturer from Trinity College. If his nomination is approved by in Medicine at Cambridge from 1988 The historic post office had Regent House, Professor Borysiewicz to 1991. He is an Honorary Fellow of announced that it would be shut- will step into the University’s top role Wolfson College. ting the shop side of the business on on October 1st 2010, when Professor He was awarded his knighthood in December 11th, with the post offi ce Richard’s seven-year term ends. -

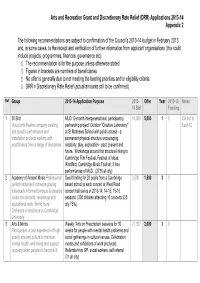

Arts and Recreation Grant and Discretionary Rate Relief (DRR) Applications 2013-14 Appendix 2

Arts and Recreation Grant and Discretionary Rate Relief (DRR) Applications 2013-14 Appendix 2 The following recommendations are subject to confirmation of the Council’s 2013-14 budget in February 2013 and, in some cases, to the receipt and verification of further information from applicant organisations (this could include projects, programmes, finances, governance etc). § The recommendation is for the purpose unless otherwise stated § Figures in brackets are numbers of beneficiaries § No offer is generally due to not meeting the funding priorities and/or eligibility criteria § DRR = Discretionary Rate Relief (actual amounts still to be confirmed) Ref Group 2013-14 Application Purpose 2013- Offer Year 2012-13 Notes 14 Bid Funding 1 30 Bird MUD 12-month intergenerational, participatory, 10,000 5,000 1 0 £5k bid to Visual arts theatre company creating partnership project. Outdoor "Creative Laboratory" East AC site specific performance and at St Matthews School with public access - a installation projects working with permanent physical structure encouraging practitioners from a range of disciplines creativity, play, exploration - past, present and future. Workshops around this structure linking to Cambridge Film Festival, Festival of Ideas, Wordfest, Cambridge Music Festival; 3 free performances of MUD. (2736 all city) 2 Academy of Ancient Music Professional Seed funding for 20 pupils from a Cambridge 3,500 1,500 3 0 period instrument orchestra playing based school to each concert at West Road historically informed baroque & classical concert hall series in 2013-14; 14-15; 15-16 music via concerts, recordings and seasons. (300 children attending 15 concerts 225 educational work. World tours. city 75%) Orchestra in residence at Cambridge University.