PT Lippo Karawaci Tbk 2Q21 Results Presentation 3 August 2021 Shareholder Structure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PT Lippo Karawaci Tbk FY20 Results Presentation 11 May 2021 Shareholder Structure

PT Lippo Karawaci Tbk FY20 Results Presentation 11 May 2021 Shareholder Structure As of 30 December 2020 As of 31 December 2019 No. of No. of Change No. Description No. of Shares % No. of Shares % Investors Investors YTD (%) I. Domestic Insurance 24 1,049,803,440 1.5% 36 629,830,720 0.9% 66.7% Individual 20,166 2,885,379,262 4.1% 10,491 2,134,292,043 3.0% 35.2% Corporation 122 32,802,325,492 46.3% 155 33,642,920,062 47.5% -2.5% Foundation 2 332,500 0.0% 3 14,551,000 0.0% -97.7% Pension Fund 25 52,756,420 0.1% 30 115,585,460 0.2% -54.4% Others 53 219,789,584 0.3% 3 28,149,800 0.0% 680.8% Sub Total 20,392 37,010,386,698 52.2% 10,718 36,565,329,085 51.6% 1.2% II. International Retail 58 30,221,538 0.0% 57 58,961,538 0.1% -48.7% Institutional 253 33,857,410,133 47.8% 291 34,273,727,746 48.3% -1.2% Others - - 0.0% - - 0.0% Sub Total 311 33,887,631,671 47.8% 348 34,332,689,284 48.4% -1.3% Total 20,703 70,898,018,369 100.0% 11,066 70,898,018,369 100.0% 0.0% 2 Contents Business Model 04 - 06 Recent Developments 07 - 14 4Q20 Financial Data 16 - 36 Corporate Governance Initiatives 37 - 42 Subsidiaries 43 - 59 Meikarta 59 - 61 Corporate Data 62 - 65 Appendix 66 - 77 One of Indonesia’s largest integrated real estate developers One of the largest diversified publicly Market leader in property development, lifestyle listed property companies in Indonesia by total malls, and healthcare in Indonesia assets and revenue ◼ Ongoing development of 3 projects (1) with GFA of ◼ Total assets as of 4Q20: $3.71 billion approximately 175,000 sqm (1) ◼ 4Q20 revenue: $228 million ◼ Manage 56 malls with GFA of 3.5 million sqm ◼ 4Q20 Market capitalization: $956 million ◼ Network of 39 hospitals with 3,630 beds Large diversified land bank with 10 Nationwide platform with presence years + worth of development across 40 cities in the country ◼ 1,362 ha available across Indonesia, providing more than 10 years of development pipeline Growing through strategic Integrated business model with ability to partnership across integrated recycle capital. -

Download E-Brochure

REVERSIBILITY INTO EMPTINESS The First in Indonesia. APARTMENT UNIT DESIGNED FOR EFFICIENCY & FLEXIBILITY. The Loggia introduces the Japanese living concept of “Reversibility into Emptiness.” Designed for maximum space efficiency, optimal organization and healthier lifestyle. 3 CHOICES OF UNIT PACKAGE LIMITED WHITE LABEL EDITION STANDARD UPGRADED Discover the freedom to design your Enjoy the extraordinarily spacious Fully-furnished package designed by own apartment unit! layout of Japanese concept apartment. award-winning Japanese Studio. INTERIOR PACKAGE Bare Unit Semi-Furnished unit Fully-Furnished unit by Atelier Bow-Wow LAYOUT Design-It-Yourself Layout Defined Layout by Atelier Bow-Wow Defined Layout by Atelier Bow-Wow FLOORING Bare Flooring Marble & Homogenous Tiles Marble & Homogenous Tiles KITCHEN n/a Franke or equiv. cooking hob, sink & hood. Toto or Franke or equiv. cooking hob, sink & hood. Toto or equiv. Mixer Tap. equiv. Mixer Tap. WARDROBE n/a Wardrobe installed (Master Bedroom) Wardrobe installed (All Bedrooms) BATHROOM Homogenous tile, Toto / equiv. sanitary wares Homogenous tile, Toto / equiv. sanitary wares Homogenous tile, Toto / equiv. sanitary wares CEILING Exposed Ceiling. Up to 3.3 m Gypsum board, emulsion paint finish. Gypsum board, emulsion paint finish. Height up to 3 m. Height up to 3 m. ADDITIONAL ITEMS AC, Smoke / Heat / Gas Detector provided. Hot AC, Smoke / Heat / Gas Detector installed. Hot AC, Smoke / Heat / Gas Detector installed. Hot water supply installed in all bathrooms. water supply installed in all bathrooms. water supply installed in all bathrooms. SAVE BIG! UP TO STARTS AT GET FULLY-FURNISHED WITH ONLY 20% OFF! 1.4 BILLION ADDITIONAL 10% LIMITED 1 WHITE LABEL EDITION UNLEASH YOUR CREATIVITY & BE YOUR OWN DESIGNER. -

Laporan Tahunan | 2012 | Annual Report Penjelasan Tema | THEME EXPLANATION

Laporan Tahunan | 2012 | Annual Report Penjelasan Tema | THEME EXPLANATION 50 Tahun Dari Sarinah Untuk Indonesia 50 YEARS FROM SARINAH FOR INDONESIA Dalam pengantar bukunya yang berjudul Sarinah, Soekarno menuliskan “Dari Mbok Sarinah, saya mendapat pelajaran mencintai 'orang kecil'. Ia orang kecil, tapi jiwanya selalu besar”. Sosok Mbok Sarinah yang merupakan pengasuh Presiden Soekarno telah memberikan warna dalam tonggak perjalanan Sarinah sebagai sebuah Perusahaan. Sarinah merupakan Department Store pertama Indonesia yang didirikan saat ekonomi Indonesia sedang runtuh di tahun 1959. Daya beli lemah, taraf hidup merosot sampai level terendah. Ketika Sarinah didirikan, Sarinah memiliki fasilitas tercanggih di zamannya. Dalam perjalanannya, Sarinah menghadapi berbagai tantangan, namun Sarinah tetap bertahan dan tidak jatuh. Berbagai tantangan tersebut dibenahi dan Sarinah pun kembali cantik. Kini…… Di usia yang mencapai 50 Tahun, Sarinah terus tumbuh dan berkembang dalam memberikan pelayanan serta mewarnai Indonesia. Di usia yang mencapai 50 tahun, Sarinah bukanlah terpaku mengenang masa lalu, akan tetapi menghormati mereka yang telah menjadi bagian dari masa lalu, dan yang akan datang. Di usia yang mencapai 50 tahun, Sarinah terus berbenah untuk menjadi profesional. Tetap tampil percaya diri, Sarinah tidak berada dalam arus besar dunia kapital. Sarinah tetap mempunyai arus sendiri. Menjadi Sarinah yang tetap memihak “orang kecil” dengan cara yang berbeda. Sarinah terus melangkah maju menuju era baru, melakukan upaya perubahan, sebuah transformasi menuju pertumbuhan jangka panjang yang berkesinambungan. Sarinah berkeinginan menjadi Great Company yang mengutamakan kualitas pelayanan serta dikelola oleh sumber daya manusia yang profesional sehingga memiliki makna di masyarakat untuk mendorong kinerja perusahaan secara berkesinambungan. Di usia Emas Sarinah, perjalanan belum akan berakhir dan tak mengenal kata akhir. -

List Store Ibox

List Store iBox NO Store Name Addres 1 IBOX NEW KOTA KASABLANKA JL. Casablanca Raya Kav. 88, Jakarta Selatan, DKI 2 IBOX CILANDAK TOWN SQUARE Cilandak Town Square Ground Floor #065, Jl. T.B. 3 IBOX GANDARIA CITY Gandaria City 1st Floor #189, Jl. KH. M. Syafi'i Hadzami 4 IBOX KEMANG Lippo Mall Kemang 2nd Floor L2-27, Jl. Pangeran 5 IBOX PEJATEN VILLAGE Pejaten Village Lt. L2 – 08-09 Jl. Warung Jati Barat No. 6 IBOX RATU PLAZA 2 Ratu Plaza 1st Floor #8, Jl. Jendral Sudirman No. 9 7 IBOX MALL OF AMBASSADOR II Mal Ambasador 3rd Floor #18, Jl. Prof. Dr. Satrio Kav. FIRST FLOOR, UNIT NO. FL1 - 22 MARGO CITY, JL. 8 IBOX MARGO CITY MARGONDA RAYA NO. 358, DEPOK 16423 Ground Floor / 01 Jl. Juanda No. 99 Bakti Jaya Sukma 9 IBOX PESONA SQUARE DEPOK Jaya, Kota Depok, Jawa Barat 16418 10 IBOX FLAGSHIP SENAYAN CITY Senayan City 4th Floor #4-29 Jl. Asia Afrika Lot 19 Kode IBOX FLAGSHIP SUMMARECON Jl. Boulevard raya Gading Serpong Pakulonan Barat 11 MALL SERPONG Kelapa Dua Unit #GF211-212-215 IBOX BAYWALK MALL (GREEN Bay Walk Mall 4th Floor #36 Green Bay Pluit Jl. Pluit 12 BAY PLUIT) Karang Ayu, Penjaringan, Jakarta Utara 14450 Unit GF A3 001,002,016,017 Jl. Boulevard Artha Gading 13 IBOX MAL ARTHA GADING No.1, RT.18/RW.8, Klp. Gading Bar., Kec. Klp. Gading, Kota Jkt Utara, Daerah Khusus Ibukota Jakarta 14240 Mall of Indonesia Ground Floor #GF–A5 Jl. Raya 14 IBOX MALL OF INDONESIA NEW Boulevard Barat, Kelapa Gading, Jakarta Utara 14240 Jl. -

Living, Reimagined

ARCHITECTURE IS THE WILL OF AN EPOCH TRANSLATED INTO SPACE. Ludwig Mies van der Rohe Living, Reimagined. The Loggia welcomes you home with an open-air living space in South Jakarta. Designed by award-winning international architects, the development offers two, 20 stories towers with two & three-bedroom types of apartment units and with dozens of recreational amenities. It is located just minutes away from education and health institutions, and easy access to international airports. Perfect for couples and small family, the residence favors simplicity and clean design. Putting functionality as a vital role in today’s lifestyle needs. THINK BEYOND TRUST BEYOND THE ERA FARPOINT is an Indonesian real estate developer Tokyo Tatemono Co. Ltd. was established in 1896 that delivers and manages distinctive properties and is now the oldest property developer in Japan. of high quality standard and design. We are part With diverse interests in the property business, of the Gunung Sewu Group, a respected and well- Tokyo Tatemono is responsible for prestigious urban established business group in Indonesia. commercial developments, including the renowned Otemachi Tower where AMAN Tokyo is located on Embracing the vision, “To be a trusted real estate the top floors, premium residential developments, company with passionate employees delivering property management, and hospitality business. innovative products and quality experiences, creating value for stakeholders”, FARPOINT is backed by more Tokyo Tatemono Asia Pte. Ltd., established in than 30 years of solid experience in the development Singapore in 2014, is striving for further business and asset management of residential, commercial, opportunities in South East Asia by extending its hospitality and retail properties. -

ALL BRANCHES of OPTIK SEIS

ALL BRANCHES of OPTIK SEIS : City Outlet Address & Location Telpphone PASAR BARU (EXPRESS) Jl. Pasar Baru No. 101 Telp. (021) 3812849, 3812429 PLAZA INDONESIA Lantai 3 No. E14 & E15, Jl. MH Thamrin Telp. (021) 31926924 GRAND INDONESIA SHOPPING TOWN (SIGNATURE) Lt. 2 East Mall Unit EM-2-39, Jl. MH. Thamrin No. 1 Telp. (021) 23580623 PLAZA ATRIUM Lantai Dasar Unit G.43-44, Jl. Senen Raya No.135 Telp. (021) 3862967 JAKARTA PUSAT GAJAH MADA PLAZA Lantai Dasar No. 47 - 49 Jl. Gajah Mada No. 19 - 26 Telp. (021) 6344648 SENAYAN CITY Second Floor No. 32 Jl. Asia Afrika Lot 19 Telp. ( 021) 72781258 PLAZA SENAYAN Lantai 2 No. 257C, 259C, 230B & 232B Jl. Asia Afrika No. 8 Telp. (021) 5725154, 5725121 CENTRAL DEPARTEMENT STORE Lantai Dasar East Mall, Jl. MH. Thamrin No. 1 GREEN PRAMUKA ( EXPRESS ) Ground Floor No.32-33, Jl.Jendral Ahmad Yani Kav 49 Jakarta Pusat (021) 29624938 MELAWAI RAYA No.65 (SIGNATURE) Jl. Melawai Raya No. 65, Kebayoran Baru Telp. (021) 7262206, 7262687 LIPPO MALL KEMANG SIGNATURE Upper Ground No. UG-30, Jl. Pangeran Antasari No.36, Kemang Jakarta 12150 Telp. (021) 29056893 PONDOK INDAH MALL 1 (SIGNATURE) Lantai 1 No. 101A, Jl. Metro Duta Pondok Indah Kav IV/TA Telp. (021) 7506790 PONDOK INDAH MALL 2 Lantai 1 No. 112, Jl. Kartika Utama V - TA Telp. (021) 75920500 LOTTE SHOPPING AVENUE Ciputra World 1, Lantai 1F No. 20A, Jl. Prof. DR. Satrio Kav. 3-5, Setiabudi, Jakarta 12940 Telp. (021) 29889470 TOWN SQUARE CILANDAK Level 2 (First Floor) No. 139, Jl. TB. Simatupang Kav. -

Potensi DIRE Di Kota Surabaya

MINAT PENGEMBANG TERHADAP DIRE Oleh Eddy Hussy Ketua Umum Dewan Pengurus Pusat Persatuan Perusahaan Realestat Indonesia 2016 DIRE & REAL ESTAT Dana Investasi Real Estat disebut DIRE adalah wadah yang dipergunakan untuk menghimpun dana dari masyarakat pemodal untuk selanjutnya diinvestasikan pada aset Real Estat, Aset yang berkaitan dengan Real Estat dan/atau kas dan setara kas. Real Estat adalah tanah secara fisik dan bangunan yang ada di atasnya, yang menghasilkan pendapatan yang berkesinambungan (recurring income). Manfaat DIRE Bagi pengembang, merupakan salah satu sumber alternatif pembiayaan untuk properti dari pasar modal. Bagi investor, bisa memberikan imbal hasil (yield) yang kompetitif. Bagi pembangunan kota, DIRE bisa menjadi ikut mendorong pembangunan proyek-proyek properti baru. Perbandingan Kebijakan Perpajakan DIRE Indonesia Singapura Malayasia Hong Kong Berdasarkan PMK 200 Dalam RPP Lebih kecil dari 5%, Selama 10 tahun (2005- sempat Dibebaskan stamp duty BPHTB sebesar 5% 2015) dibebaskan stamp Maksimal 8,5% diwacanakan di jika dijual ke REITs duty. Stamp Duty (Sisi bawah 1%. Pembeli) Setelah berkembang pesat dan besarnya kapitalisasi pasar REITS dikenakan Stamp duty 3% VAT Atas Transfer PPN 10% dengan PPN 10% dengan 7% GST dikenakan tetapi di 6% GST Tidak Ada Asset restitusi restitusi restitusi Dibebaskan dari pajak Pajak Dari Sisi Tidak ada Tidak Ada Tidak Ada keuntungan penjualan Tidak Ada Penjual properti Pajak Pendapatan PPh Final 10% PPh 0,5% Bebas Pajak Bebas Pajak 16,5% corporate tax Atas Sewa Untuk individu atau non corporate investor (termasuk institusional investor) dikenakan Pajak Atas Dividen witholding tax 10% Tidak Menjadi objek Tidak Menjadi Objek Tidak ada witholding yang Dibagikan ke Tidak Dikenakan Pajak Non Resident corporate pajak Pajak tax Pemegang Unit investor dikenakan witholding tax 25% Resident corporate investor tidak dikenakan witholding tax Contoh Properti Indonesia yang di DIRE kan di Singapura Lippo Mall Indonesian Retail FIRST REITs (LMIR) Trust 1. -

Gokana Ramen & Teppan

Gokana Ramen & Teppan Food Junction Surabaya Gokana Ramen & Teppan Jogja City Jogjakarta Gokana Ramen & Teppan Ramayana Garut Garut Gokana Ramen & Teppan Vasanta Innopark Cibitung Gokana Ramen & Teppan AEON BSD Serpong Gokana Ramen & Teppan Bandara Halim Perdana Kusuma Jakarta Gokana Ramen & Teppan Bandung Indah Plaza Bandung Gokana Ramen & Teppan Bintaro Plaza Tangerang Gokana Ramen & Teppan Blok M Plaza Jakarta Gokana Ramen & Teppan Blok M Square Jakarta Gokana Ramen & Teppan Carrefour Lebak Bulus Jakarta Gokana Ramen & Teppan CBD Ciledug Tangerang Gokana Ramen & Teppan Cibinong City Mall Bogor Gokana Ramen & Teppan Cibubur Plaza Jakarta Gokana Ramen & Teppan Cihampelas Plaza Bandung Gokana Ramen & Teppan Cilegon Center Mall Cilegon Gokana Ramen & Teppan Cimahi Mall Cimahi Gokana Ramen & Teppan Cinere Mall Depok Gokana Ramen & Teppan Ciplaz Klender Jakarta Gokana Ramen & Teppan Cirebon Superblok Cirebon Gokana Ramen & Teppan Citraland Jakarta Gokana Ramen & Teppan Citiwalk Cikarang Bekasi Gokana Ramen & Teppan Courts Harapan Indah Bekasi Gokana Ramen & Teppan D'Mall Depok Gokana Ramen & Teppan Emporium Pluit Jakarta Gokana Ramen & Teppan Festival Citylink Bandung Gokana Ramen & Teppan Gajah Mada Plaza Jakarta Gokana Ramen & Teppan Grage CityMal Cirebon Gokana Ramen & Teppan Grand Cakung Jakarta Gokana Ramen & Teppan Grand Taruma Karawang Karawang Gokana Ramen & Teppan Istana Plaza Bandung Gokana Ramen & Teppan Jatinangor Town Square Sumedang Gokana Ramen & Teppan JIEXPO Kemayoran Jakarta Gokana Ramen & Teppan Kalibata City Square Jakarta -

Store Name Ses - Surabaya - Wtc Surabaya - Lt

STORE NAME SES - SURABAYA - WTC SURABAYA - LT. 3 SES - SURABAYA - PAKUWON MALL - LT.2 SES - JAMBI - ROAD AREA SEP - JAMBI - ROAD AREA - JL. KOL ABUNJANI SIPIN SEP - JAMBI - ROAD AREA- JL. GATOT SUBROTO PASAR JAMBI SES - BANJARMASIN - ROAD AREA SES - BALIKPAPAN - ROAD AREA SEP - TARAKAN - ROAD AREA - JL. GAJAH MADA RT 02 SEP - BONTANG - ROAD AREA - JL. AHMAD YANI NO.14D SES - DURI - ROAD AREA SES - PEKANBARU - ROAD AREA SES - PADANG - ROAD AREA SES - BUKIT TINGGI - ROAD AREA SES - TANGERANG - LIVING WORLD MALL SES - JAKARTA BARAT - MALL PURI INDAH SES - JAKARTA SELATAN - PONDOK INDAH MALL 2 - LT. GF SES - JAKARTA UTARA - ARTHA GADING MALL - NO. 30-31 SES - SUKOHARJO - SENTRA NIAGA SOLO SES - JOGJAKARTA - JOGJATRONIK MALL SES - JOGJAKARTA - RAMAI MALL SES - SIDOARJO - ROAD AREA SEP - MADIUN - ROAD AREA SEP - MOJOKERTO - SUNRISE MALL SEP - KEDIRI - ROAD AREA - JL. PATIUNUS NO 44 SEP - SURABAYA - PLAZA MARINA - LT. 2 NO. 201 SEP - SURABAYA - WTC SURABAYA - LT. 1 NO. 109 SES - DENPASAR - ROAD AREA - JL. GATOT SUBROTO NO. 60 SES - DENPASAR - ROAD AREA - JL. TEUKU UMAR NO. 60 SES - JAYAPURA - MALL JAYAPURA SES - TIMIKA - DIANA MALL SEP - JAYAPURA - SAGA MALL - LT.2 SEP - JAYAPURA - ROAD AREA SEP - SORONG - ROAD AREA SEP - MANOKWARI - ROAD AREA - JL. MERDEKA SES - BEKASI - MEGA BEKASI HYPERMALL - NO.136-138 SES - CIKARANG - MALL LIPPO CIKARANG SES - JAKARTA SELATAN - MALL AMBASSADOR - LT. 2 SES - BEKASI - BEKASI CYBERPARK - NO. 177 SES - JAKARTA UTARA - BELLA TERRA KELAPA GADING SEP - JAKARTA BARAT - ITC ROXY MAS - LT. 3 SEP - JAKARTA TIMUR - LIPPO PLAZA KRAMAT JATI SEP - TANGERANG - TANGERANG CITY - LT.1 BLOK D-6 SES - BATAM - BATAM CITY SQUARE MALL SES - BATAM - NAGOYA HILL MALL - NO. -

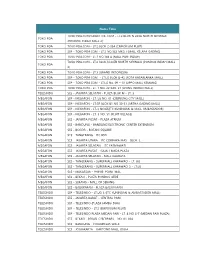

Nama Toko TOKO PDA TOKO PDA.COM/TABLET OK .COM

Nama Toko TOKO PDA.COM/TABLET OK .COM - LT.2 BLOK N 203A NORTH SKYWALK TOKO PDA (PONDOK INDAH MALL 2) TOKO PDA TOKO PDA.COM - LT.2 BLOK 2-35A (EMPORIUM PLUIT) TOKO PDA SEP - TOKO PDA.COM - LT.2 NO.362 MKG I (MALL KELAPA GADING) TOKO PDA TOKO PDA.COM - LT.1 NO.144 A (MALL PURI INDAH) TOKO PDA.COM - LT.2 BLOK N 207B NORTH SKYWALK (PONDOK INDAH MALL TOKO PDA 2) TOKO PDA TOKO PDA.COM - LT.3 (GRAND INDONESIA) TOKO PDA SEP - TOKO PDA.COM - LT.LG BLOK U-42 (KOTA KASABLANKA MALL) TOKO PDA SEP - TOKO PDA.COM - LT.LG No. 09 – 10 (LIPPO MALL KEMANG) TOKO PDA TOKO PDA.COM - LT. 1 NO. 22 KAV. 21 (LIVING WORLD MALL) TELESINDO SES - JAKARTA SELATAN - PLAZA BLOK M - LT. 3 MEGAFON SEP - MEGAFON - LT. LG NO. 01 (CIBINONG CITY MALL) MEGAFON SEP - MEGAFON - LT.GF BLOK B1 NO 30-31 (ARTHA GADING MALL) MEGAFON SEP - MEGAFON - LT-3_NO.65(ITC KUNINGAN & MALL AMBASSADOR) MEGAFON SEP - MEGAFON - LT. 3 NO. 51 (PLUIT VILLAGE) MEGAFON SES - JAKARTA PUSAT - PLAZA ATRIUM MEGAFON SES - BANDUNG - BANDUNG ELECTRONIC CENTER EXTENSION MEGAFON SES - BOGOR - BOTANI SQUARE MEGAFON SES - TANGERANG - ITC BSD MEGAFON SES - JAKARTA UTARA - ITC CEMPAKA MAS - BLOK. L MEGAFON SES - JAKARTA SELATAN - ITC FATMAWATI MEGAFON SES - JAKARTA PUSAT - GAJAH MADA PLAZA MEGAFON SES - JAKARTA SELATAN - MALL KALIBATA MEGAFON SES - TANGERANG - SUPERMALL KARAWACI - LT. UG MEGAFON SES - TANGERANG - SUPERMALL KARAWACI 2 - LT.LG MEGAFON SES - MAKASSAR - PHINISI POINT MAL MEGAFON SES - BEKASI - PLAZA PONDOK GEDE MEGAFON SES - SERANG - MALL OF SERANG MEGAFON SES - BALIKPAPAN - PLAZA BALIKPAPAN TELESINDO SEP - TELESINDO - LT.UG_3 (ITC KUNINGAN & AMBASSADOR MALL) TELESINDO SES - JAKARTA BARAT - CENTRAL PARK TELESINDO SEP - TELESINDO (PLAZA JAMBU DUA) TELESINDO SEP - TELESINDO - LT.2 (EMPORIUM PLUIT) TELESINDO SEP - TELESINDO PLAZA MEDAN FAIR - LT. -

The Function of Ngenteg Linggih Ceremony in Pejaten Tabanan

Jayapangus Press Volume 5 Nomor 2 (2021) Jurnal Penelitian Agama Hindu ISSN : 2579-9843 (Media Online) Terakreditasi Peringkat 2 http://jayapanguspress.penerbit.org/index.php/JPAH THE FUNCTION OF NGENTEG LINGGIH CEREMONY IN PEJATEN TABANAN Ida Ayu Tary Puspa1, Ida Bagus Subrahmaniam Saitya2 12Universitas Hindu Negeri I Gusti Bagus Sugriwa Denpasar [email protected], [email protected] Abstract The Dewa Yajña Ceremony is a ceremony addressed to Ida Sang Hyang Widhi with all of His manifestations as a form of devotion because He has created the universe and everything in it. This gratitude was manifested by the people of Pejaten Village by holding a ceremony to instill the Creator to rest in the sacred temple building. The Ngenteg Linggih ceremony has functions such as religious, ethics, aesthetics, and social. Each of these functions is related to one another which of course will play a role in the ceremony. Such as a religious function in which the ceremony provides a basis for belief in the community through the rites and ritual equipment to convince the public that through the ceremony carried out, religious emotions will grow. The function of ethics is to provide guidance in living through the Ngenteg Linggih ceremony to always live life by thinking, saying, and doing good according to what you are doing in your ceremony. The aesthetic function provides beauty as well as truth and sanctity so that people feel the beauty in regulating life practices as outlined in the means and implementation of the ceremony. The social function is shown by the community who work together hand in hand to load the ceremony and carry it out with the concept of ngayah. -

Announcement Proposed Acquisitions

(Constituted in the Republic of Singapore pursuant to a trust deed dated 8 August 2007 (as amended)) ANNOUNCEMENT PROPOSED ACQUISITIONS 1. INTRODUCTION LMIRT Management Ltd., in its capacity as manager of Lippo Malls Indonesia Retail Trust (“LMIR Trust” and as manager of LMIR Trust, the “Manager”), is pleased to announce that HSBC Institutional Trust Services (Singapore) Limited, in its capacity as trustee of LMIR Trust (the “Trustee”), has today, 23 October 2012, directly and/or through its wholly-owned subsidiaries, entered into conditional sale and purchase agreements, respectively: (i) Acquisition of Pejaten Village with SeaPejaten Pte Ltd (“SeaPejaten”) and PT Gading Nusa Utama (“GNU” and together with SeaPejaten, the “Pejaten Village Vendors”) in relation to the acquisition of Pejaten Village, a six-level retail mall (including one basement level) located in the city of Jakarta, Indonesia, bearing the postal address Jalan Warung Jati Barat No. 39, Jati Padang Sub District, Pasar Minggu District, South Jakarta Region, DKI Jakarta Province and which is covered by three leasehold certificates (Sertipikat Hak Guna Bangunan) (“Pejaten Village”, and the acquisition of Pejaten Village, the “Pejaten Village Acquisition”) (the “Pejaten Village CSPAs”)1. Pejaten Village has a net lettable area (“NLA”) of 41,847 square metres (“sq m”) as at 30 June 2012. Further details in respect of the structure of the Pejaten Village Acquisition are set out in paragraph 3 and Appendix A below; and (ii) Acquisition of Binjai Supermall with: (a) PT Trias Mitra Investama (“TMI”) in relation to the acquisition of Binjai Supermall, a three-level retail mall located in Binjai, North Sumatra, Indonesia, bearing the postal address Jalan Soekarno Hatta No.