Cheshire and Warrington Rural Workspace Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

For Sale Inglewood Farm, Minshull Vernon, Middlewich

Inglewood Farm, Minshull Vernon, Middlewich, Cheshire, CW10 0LS FOR SALE Development Opportunity INGLEWOOD FARM, MINSHULL VERNON, MIDDLEWICH, CW10 0LS • Fantastic village development opportunity • Reserved Matters Consent for erection of 8 new dwellings • Desirable Village Location • Approximately 1.12 hectares (2.49 acres) gross lsh.co.uk Inglewood Farm, Minshull Vernon, Middlewich, Cheshire, CW10 0LS Site Location The site is located on Middlewich Road, Minshull Vernon, a hamlet in Cheshire East borough. The site lies 3 miles to the north west of Crewe and to the south of Middlewich. The site is surrounded. by residential and agricultural land uses, giving the site a rural feel. The nearest major town is Crewe, which offers excellent transport links to London and Manchester, as well as being the site of a proposed HS2 terminal. The site is close to junctions 17 and 18 of the M6 motorway, and is approximately 20 miles away from Manchester Airport which is the nearest international airport. Inglewood Farm, Minshull Vernon, Middlewich, Cheshire, CW10 0LS Site Description The plot is relatively level and of an L shape configuration with a short frontage to Nantwich Road, which provides access to the site and is an adopted highway. There is also an additional area of land to the rear of the site which is denoted in blue below, but does not form part of the site planning consent. The site was previously used as a builders yard which accommodated a two storey dwelling and a series of storage buildings which have now been demolished and cleared to make way for the proposed scheme. -

The Story of the 1986 Domesday Project

The Story of the 1986 Domesday Project In 1986, 900 years after William the Conqueror’s original Domesday Book, the BBC published the Domesday Project . The project was probably the most ambitious attempt ever to capture the essence of life in the United Kingdom. Over a million people contributed to this digital snapshot of the country. People were asked to record what they thought would be of interest in another 1000 years. The whole of the UK was divided into 23,000 4x3km areas called Domesday Squares or “D- Blocks”. Church Minshull was d-block 364000-360000. Schools and community groups surveyed over 108,000 square km of the UK and submitted more than 147,819 pages of text articles and 23,225 amateur photos, cataloguing what it was like to live, work and play in their community. Website address: http://www.bbc.co.uk/history/domesday/dblock/GB-364000-360000 The project was about documenting everyday life - the ordinary, rather than the extraordinary and residents of Church Minshull in 1986, responded with their written accounts… The categories below contain the Church Minshull snapshot of life in 1986… The Village Church Minshull is a village situated at a bend in the R. Weaver. It was called Maneshale (Old English = nook or corner) in the first Domesday book. The village is the centre of the area in which agriculture, mainly dairy farming, is the principle industry. There are 286 people on the electoral role, the main centres of population being the village and the mobile home site at Lea Green. So far, there are not too many commuters living here, but there has been a noticeable increase in the turn-over of property in the last five years. -

Local Plan Strategy Statement of Consultation (Regulation 22) C

PreSubmission Front green Hi ResPage 1 11/02/2014 14:11:51 Cheshire East Local Plan Local Plan Strategy Statement of Consultation (Regulation 22) C M Y CM MY CY May 2014 CMY K Chapters 1 Introduction 2 2 The Regulations 4 3 Core Strategy Issues and Options Paper (2010) 6 4 Place Shaping (2011) 11 5 Rural Issues (2011) 17 6 Minerals Issues Discussion Paper (2012) 21 7 Town Strategies Phase 1 (2012) 27 8 Wilmslow Vision (Town Strategies Phase 2) (2012) 30 9 Town Strategies Phase 3 (2012) 32 10 Development Strategy and Policy Principles (2013) 36 11 Possible Additional Sites (2013) 43 12 Pre-Submission Core Strategy and Non-Preferred Sites (2013) 46 13 Local Plan Strategy - Submission Version (2014) 52 14 Next Steps 58 Appendices A Consultation Stages 60 B List of Bodies and Persons Invited to Make Representations 63 C Pre-Submission Core Strategy Main Issues and Council's Responses 72 D Non-Preferred Sites Main Issues and Council's Reponses 80 E Local Plan Strategy - Submisson Version Main Issues 87 F Statement of Representations Procedure 90 G List of Media Coverage for All Stages 92 H Cheshire East Local Plan Strategy - Submission Version: List of Inadmissible Representations 103 Contents CHESHIRE EAST Local Plan Strategy Statement of Consultation (Reg 22): May 2014 1 1 Introduction 1.1 This Statement of Consultation sets out the details of publicity and consultation undertaken to prepare and inform the Cheshire East Local Plan Strategy. It sets out how the Local Planning Authority has complied with Regulations 18, 19, 20 and 22 of the Town and Country Planning (Local Planning)(England) Regulations 2012 in the preparation of the Local Plan Strategy (formerly known as the Core Strategy). -

Wrightmarshall.Co.Uk Fineandcountry.Com

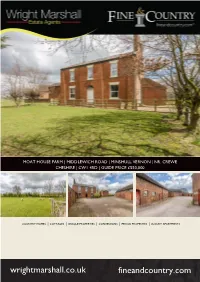

MOAT HOUSE FARM | MIDDLEWICH ROAD | MINSHULL VERNON | NR. CREWE CHESHIRE | CW1 4RD | GUIDE PRICE £550,000 COUNTRY HOMES │ COTTAGES │ UNIQUE PROPERTIES │ CONVERSIONS │ PERIOD PROPERTIES │ LUXURY APARTMENTS wrightmarshall.co.uk fineandcountry.com Moat House Farm, Middlewich Road Minshull Vernon, Nr. Crewe, Cheshire, CW1 4RD An imposing and substantial, eight Bedroom Detached Farmhouse, arranged over three floors offering extensive family sized accommodation. The property has been improved, but potential remains to remodel and further enhance the versatile and extensive layout, if required. Due to the property’s location, substantial range of traditional brick and slate outbuildings and eight existing bedrooms, certain purchasers may consider the property ideal for alternative commercial uses, such as bed and breakfast/holiday lets etc. (subject to any necessary consents). Gardens including a detached former cart house extend to approx. 1.256 Acres (0.508 ha). OPTION TO PURCHASE 10.479 ACRES BY SEPARATE NEGOTIATION DIRECTIONS GENERAL REMARKS AND COMMENTS (See also attached plan edged red) Moat House Farm is a large detached farmhouse enjoying open aspects Proceed out of Nantwich along the A530 Middlewich Road, passed in a convenient rural location along the A530 Middlewich Road. Leighton Hospital, through the traffic lights and Moat House Farm will be observed on the right hand side. The detached range of traditional farm buildings on the rear boundary are offered for sale with no planning permissions at the present time. LOCATION Prospective purchasers will be able to make their own enquiries to Minshull Vernon is a hamlet which lies 3 miles (5km) to the north west establish what alternative uses could be available to them in the future of Crewe, south east of Winsford and south west of Middlewich. -

Counciltaxbase201819appendix , Item 47

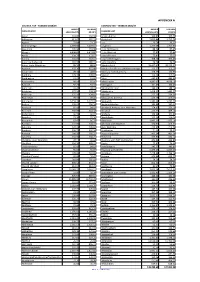

APPENDIX A COUNCIL TAX - TAXBASE 2018/19 COUNCIL TAX - TAXBASE 2018/19 BAND D TAX BASE BAND D TAX BASE CHESHIRE EAST EQUIVALENTS 99.00% CHESHIRE EAST EQUIVALENTS 99.00% Acton 163.82 162.18 Kettleshulme 166.87 165.20 Adlington 613.67 607.53 Knutsford 5,813.84 5,755.70 Agden 72.04 71.32 Lea 20.78 20.57 Alderley Edge 2,699.00 2,672.01 Leighton 1,770.68 1,752.97 Alpraham 195.94 193.98 Little Bollington 88.34 87.45 Alsager 4,498.81 4,453.82 Little Warford 37.82 37.44 Arclid 154.71 153.17 Lower Peover 75.81 75.05 Ashley 164.05 162.41 Lower Withington 308.54 305.45 Aston by Budworth 181.97 180.15 Lyme Handley 74.74 74.00 Aston-juxta-Mondrum 89.56 88.66 Macclesfield 18,407.42 18,223.35 Audlem 937.36 927.98 Macclesfield Forest/Wildboarclough 112.25 111.13 Austerson 49.34 48.85 Marbury-cum-Quoisley 128.25 126.97 Baddiley 129.37 128.07 Marton 113.19 112.06 Baddington 61.63 61.02 Mere 445.42 440.96 Barthomley 98.14 97.16 Middlewich 4,887.05 4,838.18 Basford 92.23 91.31 Millington 101.43 100.42 Batherton 24.47 24.23 Minshull Vernon 149.65 148.16 Betchton 277.16 274.39 Mobberley 1,458.35 1,443.77 Bickerton 125.31 124.05 Moston 277.53 274.76 Blakenhall 70.16 69.46 Mottram St Andrew 416.18 412.02 Bollington 3,159.33 3,127.74 Nantwich 5,345.68 5,292.23 Bosley 208.63 206.54 Nether Alderley 386.48 382.61 Bradwall 85.68 84.82 Newbold Astbury-cum-Moreton 374.85 371.10 Brereton 650.89 644.38 Newhall 413.32 409.18 Bridgemere 66.74 66.07 Norbury 104.94 103.89 Brindley 73.30 72.56 North Rode 125.29 124.04 Broomhall 87.47 86.59 Odd Rode 1,995.13 1,975.18 Buerton -

Index of Cheshire Place-Names

INDEX OF CHESHIRE PLACE-NAMES Acton, 12 Bowdon, 14 Adlington, 7 Bradford, 12 Alcumlow, 9 Bradley, 12 Alderley, 3, 9 Bradwall, 14 Aldersey, 10 Bramhall, 14 Aldford, 1,2, 12, 21 Bredbury, 12 Alpraham, 9 Brereton, 14 Alsager, 10 Bridgemere, 14 Altrincham, 7 Bridge Traffbrd, 16 n Alvanley, 10 Brindley, 14 Alvaston, 10 Brinnington, 7 Anderton, 9 Broadbottom, 14 Antrobus, 21 Bromborough, 14 Appleton, 12 Broomhall, 14 Arden, 12 Bruera, 21 Arley, 12 Bucklow, 12 Arrowe, 3 19 Budworth, 10 Ashton, 12 Buerton, 12 Astbury, 13 Buglawton, II n Astle, 13 Bulkeley, 14 Aston, 13 Bunbury, 10, 21 Audlem, 5 Burton, 12 Austerson, 10 Burwardsley, 10 Butley, 10 By ley, 10 Bache, 11 Backford, 13 Baddiley, 10 Caldecote, 14 Baddington, 7 Caldy, 17 Baguley, 10 Calveley, 14 Balderton, 9 Capenhurst, 14 Barnshaw, 10 Garden, 14 Barnston, 10 Carrington, 7 Barnton, 7 Cattenhall, 10 Barrow, 11 Caughall, 14 Barthomley, 9 Chadkirk, 21 Bartington, 7 Cheadle, 3, 21 Barton, 12 Checkley, 10 Batherton, 9 Chelford, 10 Bebington, 7 Chester, 1, 2, 3, 6, 7, 10, 12, 16, 17, Beeston, 13 19,21 Bexton, 10 Cheveley, 10 Bickerton, 14 Chidlow, 10 Bickley, 10 Childer Thornton, 13/; Bidston, 10 Cholmondeley, 9 Birkenhead, 14, 19 Cholmondeston, 10 Blackden, 14 Chorley, 12 Blacon, 14 Chorlton, 12 Blakenhall, 14 Chowley, 10 Bollington, 9 Christleton, 3, 6 Bosden, 10 Church Hulme, 21 Bosley, 10 Church Shocklach, 16 n Bostock, 10 Churton, 12 Bough ton, 12 Claughton, 19 171 172 INDEX OF CHESHIRE PLACE-NAMES Claverton, 14 Godley, 10 Clayhanger, 14 Golborne, 14 Clifton, 12 Gore, 11 Clive, 11 Grafton, -

CHESHIRE. [KELLY's from Nantwich, 4 Fiouth-South-East from Over, and 5 Miles and Afterwards Was Vested in the Lovels

434 CHURCH MINSHULL. CHESHIRE. [KELLY's from Nantwich, 4 fiouth-south-east from Over, and 5 miles and afterwards was vested in the Lovels. The mesne south-w~st from Middlewich, in the Eddisbury division manor was formerly possessed by a family who assumed the local name soon after the Norman accession, and from of the county1 hundred of ;Northwioh., union, county court district and petty sessional division of Nantwich, rural whom it passed through an heiress m the reign of Edward deanery of Middlewich and archdeaconry and diocese of Ill. to the Dutton family. After the death of Sir Thomas Chester. The Shropshire Union canal crosses the border Dutton, in the reign of Henry VII. without male issue, of the parish. The church pf St. Bartholomew, erected it passed to the representatives of Eleanor, his filth in 1702 on tfue site of an older s!Jructure, is a daughter, who married Richard de Cholmondeley; a pla.in edifice of brick and: stone, consisting of younger branch of the Minshulls continued the male line, apsidal chancel, nave of four bays, aisles, and and resided here until the demise of John Minshull, in the a western tower with pinnacles, containing a clock and 5 year r654, when his estate passed in marriage with bells, cast in 1717 ~ the piers of the arcades appear to be Elizabeth, his sole heiress, to Thomas Cholmondeley esq. the remains of the former church: in r861 the church was of Vale Royal, ancestor of the present Lord Delamere; 'COmpletely restored and re-seated at a cost of £Boo, and in he thus became possessed of the whole property, and died rBgr was further restored at an expense of nearly £s6o, in 1652, and the estate was afterwards sold to Thomas under the superintendence of Mr. -

ACTON – St. Mary

CHESHIRE RECORD OFFICE ACTON – St. Mary An ancient parish church, originally serving the townships of Acton [nr. Nantwich], Aston juxta Mondrum, Austerson, Baddington, Brindley, Burland, Cholmondeston, Edleston, Faddiley, Henhull, Hurleston, Poole, Stoke [nr. Nantwich], Worleston, and part of Sound. For later records, see also WORLESTON and NANTWICH. Always use microfilm if available. Not all series of records are complete. For a detailed breakdown of dates covered, refer to the relevant Parish (P) or Bishop’s Transcripts (EDB) lists. Covering Volume Microfilm Covering Volume Microfilm dates: reference: reference: dates: reference: reference: BAPTISMS 1981-1986 Not deposited Mf 39/5 1986-1992 Not deposited Mf 39/5 1653-1718 P 331/8212/1 Mf 39/1 1992-1995 Not deposited Mf 39/5 1718-1741 P 331/8212/2 Mf 39/1 1995-1999 Not deposited Mf 39/5 1741-1805 P 331/8212/3 Mf 39/1 1805-1812 P 331/8212/4 Mf 39/1 1813-1831 P 331/8212/6 Mf 39/1 BURIALS 1831-1859 P 331/8212/7 Mf 39/1 1859-1915 P 331/8212/8 Mf 39/3 1653-1718 P 331/8212/1 Mf 39/1 1915-1943 P 331/8212/9 Mf 39/3 1718-1751 P 331/8212/2 Mf 39/1 1943-1962 P 331/8212/10 Mf 39/3 1751-1812 P 331/8212/5 Mf 39/5 1962-1999 Not deposited Mf 39/3 1813-1840 P 331/8212/23 Mf 39/6 1840-1882 P 331/8212/24 Mf 39/6 1882-1952 P 331/8212/25 Mf 39/6 MARRIAGES 1952-1982 P 331/8212/26 Mf 39/6 1653-1718 P 331/8212/1 Mf 39/1 1718-1754 P 331/8212/2 Mf 39/1 BISHOP'S TRANSCRIPTS 1754-1797 P 331/8212/11 Mf 39/3 1797-1812 P 331/8212/12 Mf 39/3 1586-1815 EDB 1 Mf 213/31 1813-1838 P 331/8212/13 Mf 39/3 1815-1844 EDB 1 Mf 213/32 1837-1857 P 331/8212/14 Mf 39/3 1844-1874 EDB 1 Mf 213/33 1857-1858 P 331/8212/14 Mf 39/4 1874-1886 EDB 1 Mf 213/34 1859-1885 P 331/8212/15 Mf 39/4 1885-1892 P 331/8212/16 Mf 39/4 1892-1910 P 331/8212/17 Mf 39/4 PRINTED COPIES 1910-1928 P 331/8212/18 Mf 39/4 1928-1943 P 331/8212/19 Mf 39/4 1653-1812 PAR/ACT 1944-1962 P 331/8212/20 Mf 39/4 1654-1754 Mar. -

Cheshire County Council

146 CHORLEY. CHESHIRE. [POST OFFICE Roberts Hugh, Oakhurst Dawson Adam, farraer, Foden lane Pearson Jobn, farmer Schofield FranK, Oakleigh Dawson Charles James, B.A. raaster of Perrin Edward John, grocer. Chapel st S^diuster Frederick, Oatlands elementary day school. School lane Perrin Thomas, farraer, Foden lone Sidebothara Ralph Yardley, Thorn Dawson James, farmer, Grange house Pickering William, draper k clothier grove, Macclesfield road Dobson John, butcher Powell Ann (Mrs.), furniture broker Simpson Williara, Alderley cottage Downes Jas. farmer, registrar of births Poynton Sf Worth Collieries, coal Smith Thoraas, Ivy cottage k deaths, k assistant overseer for merchants (Thos. Clarke, agent) Smithson John, Fern acre, Davy lane township of Chorley, Alderiey Prince Chas. Hen. baker 4c grcr. West st Stohr Endl, The Larches Downes Richard, farmer, Carr's farm Queen's Hotel, L. k N. W. Railway Taylor George. Beancliffe,Macclesfid.rd Dutton John, bookseller 4c stationer Co.(AlfredCollins,maiiager),Alderley Thbraasson John P. Sunnyside I Ford Henrv, butcher. Chapel street Edge station Thorp Samuel, Oak bonk Ford Peter, frmr. k cattle dlr. Lindow Read Thoraas, farraer, Lindow Tonge Richard, Croston towers Foster Samuel, station master Rider Ann Amelia (Mrs), dressmaker, Waterhouse Henry, Oak view Goldthorp John, collector to the Local HUIfield Waterhouse Isaac Crewdson, High lea Board, Davy lane Rider Mary Ann (Mi8s),draper 4c hosier WHters Mrs. Woodbrook Goss William, blacksmith Robinson John, upholsterer VVatson David, Underwood Hayne Jno. frmr. Grange ho. Foden la Rylands Eliza (Mrs), boot 4c shoe raaker Webster Benjn. M.D. Macclesfield road HamUton Elzh.(Mrs.),8hpkpr.Brown8t Schroder Margaret (Miss),ladies'board Welsh Lister WUliam, Elm bank Harslem Margt.(Mrs.),Inner. -

November 2017

Visit Us At: Dog Lane, Nantwich, CW5 5GX Call Us On: 01270 375 390 November 2017 Email Us At: [email protected] Facebook: Nantwich and Rural Children’s Centre (@NantwichAndRuralCC) Monday Tuesday Wednesday Thursday Friday 30. 31. 1. 3. 2 . Baby Massage Stay and Play Sensory Time 10:30-11:30 for Under 5s for under 2’s Please ring to book See overleaf for 9:00-10:30 10:00-11:00 Health and Audlem Health Centre Cherubs Community (Breastfeeding) car park activities in Reaseheath Rural 13:00-14:30 Nantwich Invitation only 11:00—12:00 Childminder Drop In With Babywearers 9:15-11:00 Monthly Dad’s Stuff Sensory Time Autumn Fun for Under 1’s 17:00-20:00 1:30-2:30 at Sandbach Children’s Centre 6. 7. 8. 10. 9 Baby Massage Stay and Play 10:30-11:30 for Under 5s Stories & Rhymes Please ring to book See overleaf for 9:00-10:30 11:00-12:00 Health and Cherubs Wybunbury Primary School Community Stay & Play (Breastfeeding) Baby and Child Health Car park activities in 2:30-3:30 13:00-14:30 First Aid Nantwich Clinic St Oswald’s Primary 11:00-12:30 9:00-10:30 Please ring to book Parenting Journey Sensory Time 1:00-2:30 Stop 5 More details at reverse. for Under 1’s 1:30-2:30 13. 14. 15. 17. 16. Baby Massage Follow us on Stay and Play Stay & Play Sensory Time 10:30-11:30 Facebook @ for Under 5s 10:00-11:00 for Under 1’s Please ring to book Nantwich Children’s 9:00-10:30 Bunbury Pavillion 1:30-2:30 Cherubs Centre (Breastfeeding) & Parenting Journey 13:00-14:30 Cheshire East’s 11:00-12:30 Stop 2 Stay & Play Mobile Children’s 1:00-2:30 Stop 6 1:30-2:30 Dad’s Stuff Centre Please ring to book your place. -

Local Government Review in the Crewe & Nantwich Borough

Local Government Review in the Crewe & Nantwich Borough Council Area, Cheshire Additional Research Research Study Conducted by MORI for The Boundary Committee for England April 2004 Contents Page Introduction 5 Executive Summary 11 1. Attitudes to Local Governance 13 2. Attitudes to Issues under Review 19 3. Preferred Patterns of Local Government 23 Option A 31 Option B 35 Option C 39 4. Preferred New Council Name 43 5. Community Identity 45 APPENDICES 1. Option Showcards 2. Research Methodology 3. Definitions of Social Grade and Area 4. Marked-up Questionnaires Crewe & Nantwich Borough Crewe area Nantwich area 3 Introduction This report presents the findings of research conducted by the MORI Social Research Institute on behalf of The Boundary Committee for England in the Crewe & Nantwich Borough Council area. The aim of the research was to establish residents’ views about alternative patterns of unitary local government. Background to the Research In May 2003, the Government announced that a referendum would take place in autumn 2004 in the North East, North West and Yorkshire and the Humber regions on whether there should be elected regional assemblies. The Government indicated that, where a regional assembly is set up, the current two-tier structure of local government - district, borough or city councils (called in this report ‘districts’) and county councils - should be replaced by a single tier of ‘unitary’ local authorities. In June 2003, the Government directed The Boundary Committee for England (‘the Committee’) to undertake an independent review of local government in two-tier areas in the three regions, with a view to recommending possible unitary structures to be put before affected local people in a referendum at a later date. -

![Cheshire East Local Plan Authority Monitoring Report 2019/20 [Page Left Blank for Printing] Chapter](https://docslib.b-cdn.net/cover/0188/cheshire-east-local-plan-authority-monitoring-report-2019-20-page-left-blank-for-printing-chapter-4920188.webp)

Cheshire East Local Plan Authority Monitoring Report 2019/20 [Page Left Blank for Printing] Chapter

MASTER LDF COVER:Layout 1 08/10/2010 12:39 Page 1 Appendix 1 Cheshire East Local Plan Authority Monitoring Report 2019/20 [Page left blank for printing] Chapter 1 Executive Summary and Main Findings 3 Local Development Scheme 3 The Local Plan 4 2 Introduction 10 Format of the Report 10 3 The Borough 11 4 Local Development Scheme 13 5 Wider Policy Context 15 6 Local Plan Evidence Base 16 7 Duty to Cooperate 17 8 Neighbourhood Planning 19 9 Self/Custom Build Register 21 10 Other Monitoring Reports 23 11 Local Plan 24 Introduction 24 Strategic Priorities 24 Monitoring Framework 26 Sustainability Appraisal Objectives 31 12 Indicators 33 Planning for Growth 34 Infrastructure 46 Enterprise and Growth 71 Stronger Communities 90 Sustainable Environment 97 Connectivity 112 Development Plan Sites and Strategic Locations 115 13 Glossary 133 Contents CHESHIRE EAST LOCAL PLAN Authority Monitoring Report 2019/20 1 Appendices A LPS Housing and employment monitoring 146 Housing growth distribution 146 Employment growth distribution 150 Contents 2 CHESHIRE EAST LOCAL PLAN Authority Monitoring Report 2019/20 1 Executive Summary and Main Findings 1.1 This report is the twelfth Authority Monitoring Report ("AMR") produced by Cheshire East Council and covers the period 1 April 2019 to 31 March 2020. It is being published to comply with Section 35 of the Planning and Compulsory Purchase Act 2004 and Regulation 34 of the Town and Country Planning (Local Planning)(England) Regulations 2012. 1.2 The AMR has been divided into the following sections: The Borough - a spatial portrait of the Borough setting out key characteristics.