Hiscox Ltd Report and Accounts 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

22 Bishopsgate London EC2N 4BQ Construction of A

Committee: Date: Planning and Transportation 28 February 2017 Subject: Public 22 Bishopsgate London EC2N 4BQ Construction of a building arranged on three basement floors, ground and 58 upper floors plus mezzanines and plant comprising floorspace for use within Classes A and B1 of the Use Classes Order and a publicly accessible viewing gallery and facilities (sui generis); hard and soft landscaping works; the provision of ancillary servicing and other works incidental to the development. (201,449sq.m. GEA) Ward: Lime Street For Decision Registered No: 16/01150/FULEIA Registered on: 24 November 2016 Conservation Area: St Helen's Place Listed Building: No Summary The planning application relates to the site of the 62 storey tower (294.94m AOD) granted planning permission in June 2016 and which is presently being constructed. The current scheme is for a tower comprising 59 storeys at ground and above (272.32m AOD) with an amended design to the top. The tapering of the upper storeys previously approved has been omitted and replaced by a flat topped lower tower. In other respects the design of the elevations remains as before. The applicants advise that the lowering of the tower in the new proposal is in response to construction management constraints in relation to aviation safeguarding issues. The planning application also incorporates amendments to the base of the building, the public realm and to cycle space provision which were proposed in a S73 amendment application and which your Committee resolved to grant on 28 November 2016, subject to a legal agreement but not yet issued. The building would provide offices, retail at ground level, a viewing gallery with free public access at levels 55 and 56 and a public restaurant and bar at levels 57 and 58. -

Title: the Future of Workplace in Vertical Cities: Hanging Gardens, Roof Terraces and Vertical Plazas Author: Stephan Reinke, Di

ctbuh.org/papers Title: The Future of Workplace in Vertical Cities: Hanging Gardens, Roof Terraces and Vertical Plazas Author: Stephan Reinke, Director, Stephan Reinke Architects Limited Subjects: Occupancy/Lifestyle/User Experience Social Issues Vertical Transportation Keywords: Green Walls Public Space Sky Garden Vertical Urbanism Workplace Publication Date: 2020 Original Publication: International Journal of High-Rise Buildings Volume 9 Number 1 Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Stephan Reinke International Journal of High-Rise Buildings International Journal of March 2020, Vol 9, No 1, 71-79 High-Rise Buildings https://doi.org/10.21022/IJHRB.2020.9.1.71 www.ctbuh-korea.org/ijhrb/index.php The Future of Workplace in Vertical Cities: Hanging Gardens, Roof Terraces and Vertical Plazas Stephan C. Reinke FAIA RIBA Director, Stephan Reinke Architects Level 02, 28 Margaret Street, London W1W 8RZ Abstract As the workplace evolves in our vertical cities, the need for “think spaces” and the public realm to meet, create and innovate will become integral to tall buildings. These people places are designed to address the social challenges and enhance the co- working environments which are emerging in the dense urban context of our future cities. The design of sky terraces and the “spaces between” offer a greener, more humane and smarter work environment for the future. The public realm should no longer be held down, fixed to the ground plane, but rather become part and parcel of the upper levels of our workplace centers. -

Unconventional & Pioneering A.K.A. London

UNCONVENTIONAL & PIONEERING A.K.A. LONDON Much like Ziggy Stardust ( A.K.A. D av i d Bowie) this ground breaking London landmark has many alter egos... From an iconic part of the City skyline to one of the most future focused addresses in which to locate a forward thinking business. IT’S TIME TO LOOK AT 30 ST. MARY AXE FROM A WHOLE NEW ANGLE. With options ranging from approx. 5,162 to 41,828 sq ft of world class, office space across 3 spectacular floors, this is also known as your next move. 007 A.K.A. James bond A NATIONAL TREASURE WITH STYLE AND MAGNITUDE The available office floors in this suave building offer dramatic Grade A specification workspaces that make a real statement. A.K.A. THE Gherkin 22 BISHOPSGATE THE LEADENHALL BUILDING SALESFORCE TOWER A.K.A. THE GHERKIN 52 Lime Street 100 BISHOPSGATE The Willis Building 70 St Mary Axe AN ICONIC PART OF THE LONDON CITY SKYLINE A.K.A. THE ULTIMATE COMPANY Imagine positioning your business as part of the London Skyline at an address that everybody knows. 30 St. Mary Axe is your opportunity to join a thriving and diverse community of game changers. Unrivalled WORKSPACE INSPIRING VIEWS AND ALL THE ON-SITE AMENITIES YOU CAN DREAM OF. AS SOME MIGHT SAY, A MORE ENERGISED AND PRODUCTIVE WORKFORCE. Reception CGI double height space Reception CGI available office floor Rum & Coke A.K.A. C u b a L i b r e A new twist on an old favourite Historically known as the Insurance District, the immediate area has since become a magnet for a more eclectic range of sectors, from technology to education and media to finance. -

Experts in Central London Planning & Development

EXPERTS IN CENTRAL LONDON PLANNING & DEVELOPMENT PLANNING & DEVELOPMENT Gerald Eve’s planning and development advisory business is one of the most respected in the UK. Consisting of over 100 professionals, we are one of the only fully integrated planning and development teams in our industry. The vast majority of the team are based in central London, working on some of the capital’s largest and most complex projects. Active in all London Acted for Advised all major central boroughs and the London developers and City of London REITS, including British Land, Derwent London, 50% Great Portland Estates, of London First's property Landsec and Stanhope and housing members We act for all the major London million estates, including The Bedford 15 sq ft £12.5 billion Estates, Capital & Counties Covent Garden, The Church of commercial gross development Commissioners, City of London, floorspace approved value The Crown Estate, Grosvenor Britain & Ireland, The Howard de Walden Estate, The Portman Estate, and Soho Estates 2 EXPERTS IN CENTRAL LONDON PLANNING & DEVELOPMENT OUR CENTRAL LONDON CLIENTS OUR CENTRAL LONDON CLIENTS 3 YOUR INTELLIGENT ADVISOR Gerald Eve is recognised among the UK’s leading experts in planning and development. Our clients look to us to help them realise or improve asset value. One of the largest fully integrated planning and development teams in the sector Deep understanding of the entire planning system Harnessing imaginative strategies and a tenacious approach to optimise outcomes Agile, flexible and adaptable to changing -

Investor Presentation

Investor Presentation www.lancashiregroup.com Safe harbour statements NOTE REGARDING FORWARD-LOOKING STATEMENTS: CERTAIN STATEMENTS AND INDICATIVE PROJECTIONS (WHICH MAY INCLUDE MODELLED LOSS SCENARIOS) MADE IN THIS RELEASE OR OTHERWISE THAT ARE NOT BASED ON CURRENT OR HISTORICAL FACTS ARE FORWARD-LOOKING IN NATURE INCLUDING, WITHOUT LIMITATION, STATEMENTS CONTAINING THE WORDS “BELIEVES”, “ANTICIPATES”, “PLANS”, “PROJECTS”, “FORECASTS”, “GUIDANCE”, “INTENDS”, “EXPECTS”, “ESTIMATES”, “PREDICTS”, “MAY”, “CAN”, “LIKELY”, “WILL”, “SEEKS”, “SHOULD”, OR, IN EACH CASE, THEIR NEGATIVE OR COMPARABLE TERMINOLOGY. ALL SUCH STATEMENTS OTHER THAN STATEMENTS OF HISTORICAL FACTS INCLUDING, WITHOUT LIMITATION, THE FINANCIAL POSITION OF THE COMPANY AND ITS SUBSIDIARIES (THE “GROUP”), THE GROUP’S TAX RESIDENCY, LIQUIDITY, RESULTS OF OPERATIONS, PROSPECTS, GROWTH, CAPITAL MANAGEMENT PLANS AND EFFICIENCIES, ABILITY TO CREATE VALUE, DIVIDEND POLICY, OPERATIONAL FLEXIBILITY, COMPOSITION OF MANAGEMENT, BUSINESS STRATEGY, PLANS AND OBJECTIVES OF MANAGEMENT FOR FUTURE OPERATIONS (INCLUDING DEVELOPMENT PLANS AND OBJECTIVES RELATING TO THE GROUP’S INSURANCE BUSINESS) ARE FORWARD-LOOKING STATEMENTS. SUCH FORWARD-LOOKING STATEMENTS INVOLVE KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER IMPORTANT FACTORS THAT COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE GROUP TO BE MATERIALLY DIFFERENT FROM FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. THESE FACTORS INCLUDE, BUT ARE NOT LIMITED TO: THE ACTUAL -

Close Brothers Group Plc (Incorporated with Limited Liability in England and Wales with Registered Number 00520241)

PROSPECTUS DATED 8 JUNE 2021 Close Brothers Group plc (incorporated with limited liability in England and Wales with registered number 00520241) £200,000,000 2.00% Subordinated Tier 2 Notes Issue price: 99.531 per cent. The £200,000,000 2.00% Subordinated Tier 2 Notes (the “Notes”) will be issued by Close Brothers Group plc (the “Issuer”) on or about 11 June 2021 (the “Issue Date”). The terms and conditions of the Notes are set out herein in “Terms and Conditions of the Notes” below (the “Conditions”, and references to a numbered “Condition” shall be construed accordingly). The Notes will bear interest on their outstanding principal amount from (and including) the Issue Date to (but excluding) 11 September 2026 (the “Reset Date”), at a rate of 2.00 per cent. per annum and thereafter at the Reset Interest Rate as provided in Condition 5. Interest will be payable on the Notes semi-annually in arrear on each Interest Payment Date, commencing on 11 September 2021 (with a short first Interest Period from (and including) the Issue Date to (but excluding) 11 September 2021). Unless previously redeemed or purchased and cancelled, or (pursuant to Condition 7(f)) substituted, the Notes will mature on 11 September 2031 and shall be redeemed at their principal amount, together with any accrued and unpaid interest on such date. The Noteholders will have no right to require the Issuer to redeem or purchase the Notes at any time. The Issuer may, in its discretion but subject to Regulatory Approval, elect to (a) redeem all (but not some only) of the -

FTSE Factsheet

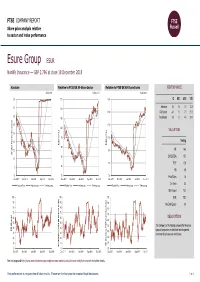

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 18 December 2018 Esure Group ESUR Nonlife Insurance — GBP 2.796 at close 18 December 2018 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 18-Dec-2018 18-Dec-2018 18-Dec-2018 2.8 115 130 1D WTD MTD YTD Absolute 0.0 0.0 0.1 12.5 2.7 110 120 Rel.Sector -0.1 1.0 7.1 21.2 2.6 105 Rel.Market 0.8 1.9 4.5 29.7 2.5 110 100 VALUATION 2.4 (local currency) (local 95 100 2.3 Trailing Relative Price Relative Price 90 2.2 90 PE 14.6 Absolute Price Price Absolute 85 EV/EBITDA 10.7 2.1 80 PCF 12.8 2 80 PB 3.9 1.9 75 70 Price/Sales 1.5 Dec-2017 Mar-2018 Jun-2018 Sep-2018 Dec-2018 Dec-2017 Mar-2018 Jun-2018 Sep-2018 Dec-2018 Dec-2017 Mar-2018 Jun-2018 Sep-2018 Dec-2018 Div Yield 3.4 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Div Payout 70.1 100 100 100 ROE 28.2 90 90 90 Net Debt/Equity 0.4 80 80 80 70 70 70 60 60 DESCRIPTION 60 50 50 50 The Company is the holding company for the esure 40 40 RSI (Absolute) RSI 40 group of companies, established to write general 30 30 insurance for private cars and homes. -

Guidance for the Directors of Banks

IFC Corporate Governance Knowledge Publication 11 FOCUS Guidance for the Directors of Banks Richard Westlake, MA (Oxon.) Foreword by Léo Goldschmidt ©Copyright 2013. All rights reserved. International Finance Corporation 2121 Pennsylvania Avenue, NW, Washington, DC 20433 The conclusions and judgments contained in this report should not be attributed to, and do not necessarily represent the views of, IFC or its Board of Directors or the World Bank or its Executive Directors, or the countries they represent. IFC and the World Bank do not guarantee the accuracy of the data in this publication and accept no responsibility for any consequences of their use. The material in this work is protected by copyright. Copying and/or transmitting portions or all of this work may be a violation of applicable law. The International Finance Corporation encourages dissemination of its work and hereby grants permission to users of this work to copy portions for their personal, noncommercial use, without any right to resell, redistribute, or create derivative works there from. Any other copying or use of this work requires the express written permission of the International Finance Corporation. For permission to photocopy or reprint, please send a request with complete information to: The International Finance Corporation c/o the World Bank Permissions Desk Office of the Publisher 1818 H Street, NW Washington, DC 20433 All queries on rights and licenses, including subsidiary rights, should be addressed to: The International Finance Corporation c/o the Office of the Publisher World Bank 1818 H Street, NW Washington, DC 20433 Fax: (202) 522-2422 Guidance for the Directors of Banks Richard Westlake, MA (Oxon.) IFC Global Corporate Governance Forum Focus 11 About The Author Richard Westlake is based in New Zealand, where he established Westlake Governance, an international governance advisory business, in 1999. -

Investor Presentation H1 2021 Update Safe Harbor Statements

Investor Presentation H1 2021 Update www.lancashiregroup.com Safe harbor statements NOTE REGARDING FORWARD-LOOKING STATEMENTS: CERTAIN STATEMENTS AND INDICATIVE PROJECTIONS (WHICH MAY INCLUDE MODELLED LOSS SCENARIOS) MADE IN THIS PRESENTATION OR OTHERWISE THAT ARE NOT BASED ON CURRENT OR HISTORICAL FACTS ARE FORWARD-LOOKING IN NATURE INCLUDING, WITHOUT LIMITATION, STATEMENTS CONTAINING THE WORDS “BELIEVES”, “AIMS”, “ANTICIPATES”, “PLANS”, “PROJECTS”, “FORECASTS”, “GUIDANCE”, “INTENDS”, “EXPECTS”, “ESTIMATES”, “PREDICTS”, “MAY”, “CAN”, “LIKELY”, “WILL”, “SEEKS”, “SHOULD”, OR, IN EACH CASE, THEIR NEGATIVE OR COMPARABLE TERMINOLOGY. SUCH FORWARD-LOOKING STATEMENTS INVOLVE KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER IMPORTANT FACTORS THAT COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE GROUP TO BE MATERIALLY DIFFERENT FROM FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. FOR A DESCRIPTION OF SOME OF THESE FACTORS, SEE THE GROUP’S ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER 2020. ALL FORWARD-LOOKING STATEMENTS IN THIS PRESENTATION OR OTHERWISE SPEAK ONLY AS AT THE DATE OF PUBLICATION. LANCASHIRE EXPRESSLY DISCLAIMS ANY OBLIGATION OR UNDERTAKING (SAVE AS REQUIRED TO COMPLY WITH ANY LEGAL OR REGULATORY OBLIGATIONS INCLUDING THE RULES OF THE LONDON STOCK EXCHANGE) TO DISSEMINATE ANY UPDATES OR REVISIONS TO ANY FORWARD-LOOKING STATEMENT TO REFLECT ANY CHANGES IN THE GROUP’S EXPECTATIONS OR CIRCUMSTANCES ON WHICH ANY SUCH STATEMENT IS BASED. ALL SUBSEQUENT WRITTEN AND ORAL FORWARD-LOOKING STATEMENTS ATTRIBUTABLE TO THE GROUP OR INDIVIDUALS ACTING ON BEHALF OF THE GROUP ARE EXPRESSLY QUALIFIED IN THEIR ENTIRETY BY THIS NOTE. PROSPECTIVE INVESTORS SHOULD SPECIFICALLY CONSIDER THE FACTORS IDENTIFIED IN THIS PRESENTATION WHICH COULD CAUSE ACTUAL RESULTS TO DIFFER BEFORE MAKING AN INVESTMENT DECISION. -

Central London Development Pipeline Q2 2017

Central London Development Pipeline Q2 2017 Development Completions - As at Q2 2017, there is 9.45m sq ft of available space under construction across Central London. 1.32 million sq ft of office space completed in Q2 2017, adding 710,000 sq ft of available office space to the market. - For future 2017 development completions, 49% of the space is prelet, rising to 55% for 2018. - 10% of space has been prelet for 2019 completions, the low figure being largely the result of the commencement of 22 Bishopsgate adding 1.275m sq ft of availability to the market. - Total take-up by prelets in Q2 2017 equalled 520,000 sq ft, 17 % of total take-up in the quarter. The largest prelet of the quarter was to WeWork at Two Southbank Place, taking 280,000 sq ft. In the third largest letting of the quarter, NEX took 120,000 sq ft at London Fruit & Wool Exchange. Development Pipeline - Completion Year Oversite developments 7,000,000 at Crossrail stations are 6,000,000 projected to begin 5,000,000 construction following 4,000,000 ticket office completion. Sq Ft 3,000,000 The oversite 2,000,000 developments are 1,000,000 projected to complete in 0 2020. 2017 2018 2019 2020 Available Office Sq Ft (NIA) Let Office Sq Ft (NIA) - The most active market is City Core with 7.98m sq ft of proposed office space under construction. City Fringe, Midtown and West End have 1.74m, 2.47m, & 1.70m sq ft of space under construction respectively. - The market with the highest percentage of prelets is Southbank with only 19% of under construction space still available. -

CTBUH Research Paper Title: Towards Post-Crisis Tall Buildings

CTBUH Research Paper ctbuh.org/papers Title: Towards Post-Crisis Tall Buildings and Cities Authors: Daniel Safarik, Editor-in-Chief, CTBUH Will Miranda, Research Coordinator, CTBUH Subjects: COVID MEP Social Issues Vertical Transportation Keywords: Commercial COVID-19 MEP Occupancy Vertical Transportation Workplace Publication Date: 2020 Original Publication: CTBUH Journal 2020 Issue IV Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Daniel Safarik; Will Miranda CTBUH Special Report Towards Post-Crisis Tall Buildings and Cities Abstract The COVID-19 pandemic has caused a massive and sudden rethink of how tall office buildings, and cities as a whole, should operate. With national and local government responses varying widely across the globe, and much about the virus still unknown, it is impossible to generate a single safe operational model for the immediate near term. However, the aggregate knowledge of the building industry Daniel Safarik William Miranda can be activated by creating an indicative, general assessment of how today’s tall buildings and their cities could be modified. This report collates the advice of the Authors Council on Tall Buildings and Urban Habitat’s Expert Peer Review Committee and Daniel Safarik, Editor-in-Chief William Miranda, Research Coordinator its database of the global tall building industry, as well as the consultancies and Council on Tall Buildings and Urban Habitat The Monroe Building professional organizations in the wider CTBUH orbit, forming a hypothetical model 104 South Michigan Avenue, Suite 620 Chicago, Illinois of the potential changes coming to the existing stock of tall office buildings and USA 60603 the cities where they are located, and speculates on the urban implications of t: +1 312 283 5599 e: [email protected] extrapolating these changes.