Risk Disclosure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

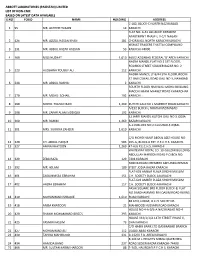

Abbott Laboratories (Pakistan) Limited List of Non-Cnic Based on Latest Data Available S.No Folio Name Holding Address 1 95

ABBOTT LABORATORIES (PAKISTAN) LIMITED LIST OF NON-CNIC BASED ON LATEST DATA AVAILABLE S.NO FOLIO NAME HOLDING ADDRESS C-182, BLOCK-C NORTH NAZIMABAD 1 95 MR. AKHTER HUSAIN 14 KARACHI FLAT NO. A-31 ALLIANCE PARADISE APARTMENT PHASE-I, II-C/1 NAGAN 2 126 MR. AZIZUL HASAN KHAN 181 CHORANGI, NORTH KARACHI KARACHI. KISMAT TRADERS THATTAI COMPOUND 3 131 MR. ABDUL RAZAK HASSAN 53 KARACHI-74000. 4 169 MISS NUZHAT 1,610 469/2 AZIZABAD FEDERAL 'B' AREA KARACHI NAZRA MANZIL FLAT NO 2 1ST FLOOR, RODRICK STREET SOLDIER BAZAR NO. 2 5 223 HUSSAINA YOUSUF ALI 112 KARACHI NADIM MANZIL LY 8/44 5TH FLOOR, ROOM 37 HAJI ESMAIL ROAD GALI NO 3, NAYABAD 6 244 MR. ABDUL RASHID 2 KARACHI FOURTH FLOOR HAJI WALI MOHD BUILDING MACCHI MIANI MARKET ROAD KHARADHAR 7 270 MR. MOHD. SOHAIL 192 KARACHI 8 290 MOHD. YOUSUF BARI 1,269 KUTCHI GALI NO 1 MARRIOT ROAD KARACHI A/192 BLOCK-L NORTH NAZIMABAD 9 298 MR. ZAFAR ALAM SIDDIQUI 192 KARACHI 32 JAFRI MANZIL KUTCHI GALI NO 3 JODIA 10 300 MR. RAHIM 1,269 BAZAR KARACHI A-113 BLOCK NO 2 GULSHAD-E-IQBAL 11 301 MRS. SURRIYA ZAHEER 1,610 KARACHI C/O MOHD HANIF ABDUL AZIZ HOUSE NO. 12 320 CH. ABDUL HAQUE 583 265-G, BLOCK-6 EXT. P.E.C.H.S. KARACHI. 13 327 AMNA KHATOON 1,269 47-A/6 P.E.C.H.S. KARACHI WHITEWAY ROYAL CO. 10-GULZAR BUILDING ABDULLAH HAROON ROAD P.O.BOX NO. 14 329 ZEBA RAZA 129 7494 KARACHI NO8 MARIAM CHEMBER AKHUNDA REMAN 15 392 MR. -

Formerly: Karachi Stock Exchange Limited) Stock Exchange Building, Stock Exchange Road, Karachi-74000, Phones: 111-001-122

PAKISTAN STOCK EXCHANGE LIMITED (Formerly: Karachi Stock Exchange Limited) Stock Exchange Building, Stock Exchange Road, Karachi-74000, Phones: 111-001-122 CRITERIA FOR SELECTION OF TOP 25 COMPANIES FOR THE YEAR 2016 1) Prerequisites for Selection of Top Companies: a) A minimum distribution of 30% (including at least 15% cash dividend) for the year; b) The Shares of the company are traded 50% of the total trading days during the year c) The company should not be in the Defaulters’ Segment of the Exchange or trading in its shares has not been suspended on account of violation of Listing of Companies & Securities Regulations of the Exchange during the year. 2) The Companies that Qualify above Prerequisites will be selected on the Basis of Highest Marks Obtained as per the following Criteria: a) Capital Efficiency: (i) Shareholders Return on Equity (on the basis of before tax profit) 15% (ii) Ratio of Capital Expenditure to Total Assets 3% (iii) Change in Market Value Added (MVA of a year in the difference 2.5% between Market Value minus Book Value for that year.) b) Dividend Distribution (including Bonus) (i) Total Distribution out of Current Year’s Profit only. (In case 10% dividend/bonus is paid out of prior year’s earnings/reserves, than the dividend/bonus shall be adjusted proportionately) (ii) Payout Ratio (DPS / EPS) 10% c) Growth in Operating Revenue 6% Change in EBITDA Margin (Operating margin) in absolute terms 6% d) Free-Float of Shares 10% Free-Float of shares as a percentage of total shares outstanding e) Turnover of Shares -

Abbott Laboratories (Pakistan) Limited List of Non-Cnic As at May 13, 2019 S.No Folio Name Address Holding 1 95 Mr

ABBOTT LABORATORIES (PAKISTAN) LIMITED LIST OF NON-CNIC AS AT MAY 13, 2019 S.NO FOLIO NAME ADDRESS HOLDING 1 95 MR. AKHTER HUSAIN C-182, BLOCK-C 14 NORTH NAZIMABAD KARACHI 2 126 MR. AZIZUL HASAN KHAN FLAT NO. A-31 181 ALLIANCE PARADISE APARTMENT PHASE-I, II-C/1 NAGAN CHORANGI, NORTH KARACHI KARACHI. 3 131 MR. ABDUL RAZAK HASSAN KISMAT TRADERS 53 THATTAI COMPOUND KARACHI-74000. 4 169 MISS NUZHAT 469/2 AZIZABAD 1,610 FEDERAL 'B' AREA KARACHI 5 223 HUSSAINA YOUSUF ALI NAZRA MANZIL FLAT NO 2 112 1ST FLOOR, RODRICK STREET SOLDIER BAZAR NO. 2 KARACHI 6 244 MR. ABDUL RASHID NADIM MANZIL LY 8/44 2 5TH FLOOR, ROOM 37 HAJI ESMAIL ROAD GALI NO 3, NAYABAD KARACHI 7 270 MR. MOHD. SOHAIL FOURTH FLOOR 192 HAJI WALI MOHD BUILDING MACCHI MIANI MARKET ROAD KHARADHAR KARACHI 8 290 MOHD. YOUSUF BARI KUTCHI GALI NO 1 1,269 MARRIOT ROAD KARACHI 9 298 MR. ZAFAR ALAM SIDDIQUI A/192 BLOCK-L 192 NORTH NAZIMABAD KARACHI 10 300 MR. RAHIM 32 JAFRI MANZIL 1,269 KUTCHI GALI NO 3 JODIA BAZAR KARACHI 11 301 MRS. SURRIYA ZAHEER A-113 BLOCK NO 2 1,610 GULSHAD-E-IQBAL KARACHI 12 320 CH. ABDUL HAQUE C/O MOHD HANIF ABDUL AZIZ 583 HOUSE NO. 265-G, BLOCK-6 EXT. P.E.C.H.S. KARACHI. 13 327 AMNA KHATOON 47-A/6 1,269 P.E.C.H.S. KARACHI 14 329 ZEBA RAZA WHITEWAY ROYAL CO. 129 10-GULZAR BUILDING ABDULLAH HAROON ROAD P.O.BOX NO. -

Evidence from Karachi Stock Exchange

CORE Metadata, citation and similar papers at core.ac.uk Provided by International Institute for Science, Technology and Education (IISTE): E-Journals Developing Country Studies www.iiste.org ISSN 2224-607X (Paper) ISSN 2225-0565 (Online) Vol.5, No.9, 2015 Investment Behavior and Stock Preference of an Individual Investor: Evidence from Karachi Stock Exchange Muhammad Waseem Ur Rehman 1 Kashif Arif 2* 1.MS-Finance Scholar, Mohammad Ali Jinnah University, Karachi 2.Faculty of Business Administration, Mohammad Ali Jinnah University, Karachi *Corresponding Author: Email: [email protected] Abstract The purpose of the research is to study the individual investor’s behavior in Karachi Stock Exchange. In this study data was collected from individual clients at Karachi Stock Exchange. Type of the study is descriptive and deductive approach was used. The data was collected from 389 respondents at Karachi Stock Exchange with the help of designed questionnaire. The individual behavior is tested with the help of regression analysis. There are three regression models developed to study the relationship and impact of Independent variables (Accounting information & financial literacy, overconfidence, irrationality and biasness in decision making) on three different dependent variables (Preference of capital gain, preference of dividend and gambling). Results explain no relationship toward preference of capital gain but the significant relationships found toward preference of dividend and gambling. So it can be easily concluded that the investors at Karachi Stock Exchange do not prefer capital gain but they want better payout and speculation in the market. There were also studied that the accounting information & financial literacy increase the behavior toward preference of dividend and decrease toward gambling. -

The Impact of Macroeconomic Variables on Stock Prices: a Case Study of Karachi Stock Exchange

Journal of Economics and Sustainable Development www.iiste.org ISSN 2222-1700 (Paper) ISSN 2222-2855 (Online) Vol.9, No.13, 2018 The Impact of Macroeconomic Variables on Stock Prices: A Case Study of Karachi Stock Exchange Jawad Khan MS student, COMSATS Institute of Information Technology, Abbottabad Dr. Imran Khan Assistant Professor, COMSATS Institute of Information Technology, Abbottabad Abstract Investment decisions are highly influenced by macroeconomic variables as changes in macroeconomic variables effect stock markets differently according to the country economic conditions and government policies. The study contributes by determining the effect of various macroeconomic variables on stock prices of Pakistan by analyzing the monthly data from May 2000 - August 2016. As all the variables are stationary at first difference thus ideal ARDL approach of bound testing is applied to check the short term and long term cointegration of the macroeconomic variables on stock prices. The findings suggest that stock prices of Karachi Stock Exchange in long term are significantly affected by money supply, exchange rate, and interest rate. In short term all the variables are insignificant except exchange rate which is negatively cointegrated with stock prices. The central bank shall be vigilant while changing the money supply in market because too much increase in money supply could effect investment as well as stock market. The regulator should keep interest rate relatively low to encourage economic activities, improve external economic environment through rule based exchange rate policy and avoid discretionary measures. Keywords : Karachi Stock Exchange, Macroeconomic variables, Time series analysis, KSE-100 index, Cointegration, ARDL, Bound testing approach. Introduction Emerging markets keep on attracting an expanding level of investments by specialized and institutional investors. -

To Open Bankislami Pakistan Limited Details

S.No Branch Name Address City Province Supply Bazar 1 Plot # 195-207, Khasra # 2302-2305, Abbottabad Business Complex, Moza Shaikul Bandi, Amir Shaheed Road, Supply Bazar, Manshera Road, Abbottabad. Abbottabad KPK 2 Arifwala Plot No.115, H-Block, Thana Bazar, Arifwala Arifwala Punjab 3 Attock Omair Arcade, Opposite Peoples Colony, Main Attock Road, Attock. Attock Punjab 4 Ghourghusti Miskeenabad, Ghourghusti, Tehsil Hazro, District Attock Attock Punjab 5 Badin Mani Quaid-e-azam Road, Near Qazia Wah, Badin Badin Sindh 6 Golarchi Plot No. A-4, Golarchi Town, Taluka Shaheed Fazil Rao, District Badin Badin Sindh 7 Satellite Town Plot # 53-C, Commercial Area, Satellite Town, Bahawalpur Bahawalpur Punjab 8 Circular Road Block No. 915, Circular Road Bahawalpur. Bahawalpur Punjab 9 Balakot Plot, Khasra No.3626/1046, Moza Balakot,Tehsil Balakot, District Mansehra Balakot KPK 10 Batagram Khasra No.792, Moza Ajmairah, Tehsil & District Batgram. Batagram KPK 11 Batkhela Main Bazar Batkhela, Tehsil Sawat Ranizai, District Malakand Batkhela KPK 12 Beesham Plot Khasra No.583, Moza Butyal, Main Road Besham, Tehsil Besham, District Shangla Beesham KPK 13 Booni Booni Bazar, Village & P.O Booni, Tehsil Mastaj, District Chitral Booni KPK 14 Chaksawari, AJK Main Mirpur Road, Near Attock Petrol Pump, Chaksawari, District Mirpur, Azad Kashmir Chaksawari AJK 15 Chakwal Khasra # 4516 Jhelum Road Chakwal. Chakwal Punjab 16 Chaman Khasra # 208 & 209, Mall Road, Chaman Chaman Balochistan 17 Chichawatni Plot No.146, Khatooni # 239, G.T. Road, Chichawatni Chichawatni Punjab 18 Chilas Main Bazar, DC Chowk, Rani Road Chillas, District Diamer. Chilas KPK 19 Chiniot 1- A Shahra-e- Quaid Azam , Chiniot. -

Kcaa Members List.Pdf

KARACHI CUSTOMS AGENTS ASSOCIATION Members List NAME OF AUTHORIZED S. # CHAL # COMPANY NAME ADDRESS TEL NOS FAX NOS Email Address REPRESENTATIVE Office No.614, 6th Floor, Uni Plaza, I. I. 391 2724 3- Star Enterprises 32466518 32466518 [email protected] Akbar Jan Chundrigar Road, Karachi Room No. 411, 4th Floor, Shams Chamber, 1868 2785 3a Sons Cargo Logistics 32423284 NIL [email protected] Sheikh Safdar Alam Shahrah-e-liaquat, Khi 10-11, Ayub Plaza Ground Floor Hamayoon 203 2211 7- Seas Cargo Services 32425407 32419470 [email protected] Muhammad Shahid Rafiq Muhammad Khan Road Keamari, Karachi. Room No. 713-a, Uni Plaza, 7th Floor, I. I. 495 2550 7- Star Enterprises 32412964 0213-7013682 [email protected] Dil Nawaz Ahmed Chundrigar Road, Karachi Al Saihat Centre, Suite 405, 4th Floor, 35653457- 441 1998 786 Business Syndicate Annexe To Hotel Regent Plaza, Shahrah E 35653675 [email protected] Saleem Ahmed Abbasi 35653675 Faisal, Karachi Suit No# 104, Abdullah Square, Altaf 1077 2365 A & S Enterprises 32420422 nil [email protected] Muhammad Saleem Hussain Road, New Challi, Karachi Poonawala View, Office # A-9 Opposite 32313616, 95 2986 A M S Enterprises - [email protected] Malik Allah Nawaz Custom House Karachi 32310680 Office No. 212, 2nd Floor, Uni Plaza, I. I. 983 967 A. A. Ahmad & Co 32420506 32420456 [email protected] Danish Wakil Chundrigar Road, Karachi Room #801, Jilani Tower, M. A. Jinnah 1965 924 A. A. Enterprises 32439802 32477355 [email protected] Aoun Mohammed Choudhary Road, Tower, Khi Office No.b-4 & 5, 1st Floor, Eidgah 889 2301 A. -

Karachi, Pakistan by Arif Hasan Masooma Mohib Source: CIA Factbook

The case of Karachi, Pakistan by Arif Hasan Masooma Mohib Source: CIA factbook Contact Arif Hasan, Architect and Planning Consultant, 37-D, Mohd. Ali Society, Karachi – 75350 Tel/Fax. +92.21 452 2361 E-mail: [email protected] I. INTRODUCTION: THE CITY A. URBAN CONTEXT 1. National Overview Table A1.1 below gives an overview of demographic 1951 – 1961: During this period, there was a sharp and urbanisation trends in Pakistan. The urban popula- fall in infant mortality rates. This was because of the tion has increased from 4,015,000 (14.2 per cent of the eradication of malaria, smallpox and cholera through the total) in 1941 to 42,458,000 (32.5 per cent of total) in use of pesticides, immunisation and drugs. Urban popu- 1998. The 1998 figures have been challenged since lations started to increase due to the push factor created only those settlements have been considered as urban by the introduction of Green Revolution technologies in which have urban local government structures. agricultural production. Population density as a whole has also increased from 42.5 people per km2 in 1951 to 164 in 1998. 1961 – 1972: An increase in urbanisation and overall Major increases in the urban population occurred demographic growth continued due to the trends during the following periods: explained above. In addition, Pakistan started to indus- trialise during this decade. This created a pull factor 1941 – 1951: This increase was due to the migration which increased rural-urban migration. These trends from India in 1947 when the subcontinent was parti- continued during the next decade. -

Stock Price, Inflation, Karachi Stock Exchange, KSE 100

Microeconomics and Macroeconomics 2015, 3(4): 83-88 DOI: 10.5923/j.m2economics.20150304.01 The Impact of Inflation on Stock Prices: Evidence from Pakistan Ghulam Muhammad Qamri1,*, Muhammad Abrar Ul Haq2, Farheen Akram3 1Department of Economics, Nankai University, China 2School of Economics, Finance and Banking, University Utara Malaysia, Malaysia 3Department of Commerce, the Islamia University of Bahawalpur, Pakistan Abstract This empirical study design to investigate the association between stock price and inflation in Pakistan. Many previous studies around the globe examine the relationship between stock price and inflation and proposed different results, many of them found that there is positive link between inflation and stock price. On the other hand some studies realized the negative relationship between these two terms. This research is based on past ten years data of Karachi stock exchange (KSE 100) and the statistical results of this research shows that there is negative relationship between stock price and inflation. Furthermore, when prices of stock are low firms avoid to enter in capital market until the central bank provide alternate for firm’s plan to invest in capital market. Moreover, firm’s equity value is also hit by the startling inflation rate. Similarly tightening of monetary policy can reduce inflation and stock prices both as individuals will be left with less money to buy goods or buy stocks. Keywords Stock price, Inflation, Karachi Stock Exchange, KSE 100 Islamabad stock exchange (ISE). However, a Memorandum 1. Introduction of Understanding (MoU) was signed in Islamabad on 27 August 2015 to form Pakistan Stock Exchange, with the History has shown that the price of stocks and other assets merger of Karachi, Lahore and Islamabad stock exchanges. -

Karachi in the Twenty- First Century

Karachi in the Twenty- First Century Karachi in the Twenty- First Century: Political, Social, Economic and Security Dimensions By Mansoor Bin Tahnoon Al Nahyan Karachi in the Twenty-First Century: Political, Social, Economic and Security Dimensions By Mansoor Bin Tahnoon Al Nahyan This book first published 2016 Cambridge Scholars Publishing Lady Stephenson Library, Newcastle upon Tyne, NE6 2PA, UK British Library Cataloguing in Publication Data A catalogue record for this book is available from the British Library Copyright © 2016 by Mansoor Bin Tahnoon Al Nahyan All rights for this book reserved. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the copyright owner. ISBN (10): 1-4438-8706-4 ISBN (13): 978-1-4438-8706-9 TABLE OF CONTENTS List of Figures and Tables ......................................................................... vii Preface ...................................................................................................... viii List of Important Abbreviations ................................................................. xi Chapter One ................................................................................................. 1 Security Implications of Karachi: Mega City, Mega Issues Chapter Two .............................................................................................. 16 The City and its Antiquity Chapter Three ........................................................................................... -

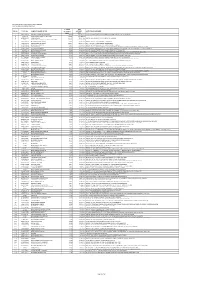

Mughal Iron & Steel Industries Limited List of Unpaid Dividend (D-05) Sr. No. Folio No. Name of Shareholder Number of Shares

MUGHAL IRON & STEEL INDUSTRIES LIMITED LIST OF UNPAID DIVIDEND (D-05) NUMBER NET SR. NO. FOLIO NO. NAME OF SHAREHOLDER OF SHARES AMOUNT LAST KNOWN ADDRESS HELD (Rs.) 1 4705087224 FEDERAL BOARD OF REVENUE 63623 139,971.00 CHIEF (INCOME TAX POLICY) CONSTITUITION AVENUE FBR ISLAMABAD 2 9900003 STAY ORDER CASES B-1 (5% TAX) 59451 104,634.00 . 3 4283020762 KHALID RAFIQ 40000 74,800.00 HOUSE NO.6-K, BLOCK - H, GULBERG - II, LAHORE 4 8307 SUSPENSE ACCOUNT (R-1) MCB & SUMMIT 32091 56,480.00 . 5 5264108279 MARIAM BAKAR GOKAL 25000 40,500.00 HOUSE NO.A-29, KDA SCHEME 1, KARACHI 6 4085093003 SYED FARHAT HUSSAIN 15500 24,257.00 367-6-D UNIT # 6 LATIFABAD HYDERABAD 7 10181010825 MIAN IQBAL BARKAT 14500 23,490.00 HOUSE NO 176/186, H BLOCK, MODEL TOWN, LAHORE 8 3038033559 IMRAN KHALIL 9000 15,840.00 WORLD NO. 12, MOHALLAH BILAL PURA SHAHKOT NEAR BILAL MOSQUE SHAHKOT NANKANA SAHIB 9 5264101696 SYED ASAD KAMRAN 8000 14,960.00 EFU GENERAL INSURANCE LTD.,2ND FLOOR, ROOM NO.201,KASHIF CENTER, SHAHRAH-E-FAISAL, KARACHI 10 7419005219 MUHAMMAD MANSOOR 8000 14,080.00 HOUSE # 80/ II STREET 9 KHYABAN-E-SEHR D.H.A VI KARACHI 11 3038037824 FAZAL AHMED 6500 12,155.00 H # 176,STREET # 14,FALCON COMPLEX, PAF SOCIETY,NEAR BALOCH COLONY BRIDGE, KARACHI 12 6684034788 KHAWAJA KASHAN AMIN 6000 11,220.00 MR-1/64 A-12 1ST FLOOR AZIZ MANSION MURAD KHAN ROAD KHORI GARDEN KARACHI 13 6684115926 KHURRAM SHAHZAD 6000 11,220.00 HOUSE NO.237/11 STREET NO.38 KHAYABAN-E-ROMI PHASE 8 KARACHI 14 307104244 ABDUL HAMEED KHAN 6000 10,560.00 HOUSE # 77 Q, FIRST FLOOR,, GHAZALI ROAD,BLOCK -

Evidence from the Karachi Stock Exchange

PA K I S TA N I N S T I T U T E O F D E V E L O P M E N T E C O N O M I C S S R E P The Global Financial Crisis and Investors' A P Behaviour: Evidence from the Karachi Stock Exchange G 6 0 N 1 I . o K N R O Asiya Sohail Attiya Yasmin Javid W E D I P July 2014 PIDE Working Papers No. 106 The Global Financial Crisis and Investors’ Behaviour: Evidence from the Karachi Stock Exchange Asiya Sohail National University of Science and Technology, Islamabad and Attiya Yasmin Javid Pakistan Institute of Development Economics, Islamabad PAKISTAN INSTITUTE OF DEVELOPMENT ECONOMICS ISLAMABAD 2014 Editorial Committee Dr Abdul Qayyum Head Dr Durr-e-Nayab Member Dr Anwar Hussain Secretary All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means—electronic, mechanical, photocopying, recording or otherwise—without prior permission of the Publications Division, Pakistan Institute of Development Economics, P. O. Box 1091, Islamabad 44000. © Pakistan Institute of Development Economics, 2014. Pakistan Institute of Development Economics Islamabad, Pakistan E-mail: [email protected] Website: http://www.pide.org.pk Fax: +92-51-9248065 Designed, composed, and finished at the Publications Division, PIDE. C O N T E N T S Page Abstract v 1. Introduction 1 2. Overview of Financial Crises and Karachi Stock Exchange 4 2.1. The Global Financial Crisis and the Emerging Economies 4 2.2.