Evidence from the Karachi Stock Exchange

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Role of Terrorist Events

International Journal of Disaster Recovery and Business Continuity Vol. 12, No. 1, (2021), pp. 1063-1075 Examination of Stock Markets Performance in Emerging Economies during Difficult Times: Role of Terrorist Events Dr. Ashfaq Ahmad Aamir Sohail Adil Riaz Farhad Hussain Iqra Ihsan Associate Professor, Hailey College of Commerce, University of the Punjab, Lahore. Email:[email protected] Lecturer Commerce, University of Sargodha (Sub Campus Bhakkar) [email protected] Lecturer Commerce, Government College University Faisalabad (Sub- Campus Hafiz Abad), Pakistan. , Ph.D. Scholar, Hubei University, China M.Com Scholar, Hailey College of Commerce, University of the Punjab, Lahore Abstract This study examines the effect of selected local and global terrorist events on Pakistan Stock Exchange by assessing KMI-30 and KSE-30 during the last decade. Data was collected for the daily closing stock prices of KMI-30 and KSE-30 for a period of 10 years (2010 to 2019). Twelve major terrorist events were selected from the South Asian Terrorism Portal (SATP) creating negative outcomes (deaths, injuries and other damages). Event study method was applied through estimation windows for Pre-Event, Event and Post-Event. Results indicate that the majority of the events have a significant impact on KSE-30 and KMI-30. More specifically the findings suggested that, Suicide attack on political offices, Attack on the Jamia masjid Madina, Twin suicide assaults at Parachinar, Assault on Army Public School, Paris, France bombing at bar, restaurant, theater and stadium, Self- destruction bombarding in Belgium, Suicide bombarding at Quetta’s Civil Hospital, Attack on Shrine of Lal Shahbaz and Attack on the political rally of the Balochistan Awami Party has significant effect on both markets. -

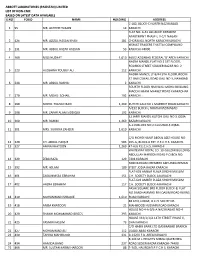

Abbott Laboratories (Pakistan) Limited List of Non-Cnic Based on Latest Data Available S.No Folio Name Holding Address 1 95

ABBOTT LABORATORIES (PAKISTAN) LIMITED LIST OF NON-CNIC BASED ON LATEST DATA AVAILABLE S.NO FOLIO NAME HOLDING ADDRESS C-182, BLOCK-C NORTH NAZIMABAD 1 95 MR. AKHTER HUSAIN 14 KARACHI FLAT NO. A-31 ALLIANCE PARADISE APARTMENT PHASE-I, II-C/1 NAGAN 2 126 MR. AZIZUL HASAN KHAN 181 CHORANGI, NORTH KARACHI KARACHI. KISMAT TRADERS THATTAI COMPOUND 3 131 MR. ABDUL RAZAK HASSAN 53 KARACHI-74000. 4 169 MISS NUZHAT 1,610 469/2 AZIZABAD FEDERAL 'B' AREA KARACHI NAZRA MANZIL FLAT NO 2 1ST FLOOR, RODRICK STREET SOLDIER BAZAR NO. 2 5 223 HUSSAINA YOUSUF ALI 112 KARACHI NADIM MANZIL LY 8/44 5TH FLOOR, ROOM 37 HAJI ESMAIL ROAD GALI NO 3, NAYABAD 6 244 MR. ABDUL RASHID 2 KARACHI FOURTH FLOOR HAJI WALI MOHD BUILDING MACCHI MIANI MARKET ROAD KHARADHAR 7 270 MR. MOHD. SOHAIL 192 KARACHI 8 290 MOHD. YOUSUF BARI 1,269 KUTCHI GALI NO 1 MARRIOT ROAD KARACHI A/192 BLOCK-L NORTH NAZIMABAD 9 298 MR. ZAFAR ALAM SIDDIQUI 192 KARACHI 32 JAFRI MANZIL KUTCHI GALI NO 3 JODIA 10 300 MR. RAHIM 1,269 BAZAR KARACHI A-113 BLOCK NO 2 GULSHAD-E-IQBAL 11 301 MRS. SURRIYA ZAHEER 1,610 KARACHI C/O MOHD HANIF ABDUL AZIZ HOUSE NO. 12 320 CH. ABDUL HAQUE 583 265-G, BLOCK-6 EXT. P.E.C.H.S. KARACHI. 13 327 AMNA KHATOON 1,269 47-A/6 P.E.C.H.S. KARACHI WHITEWAY ROYAL CO. 10-GULZAR BUILDING ABDULLAH HAROON ROAD P.O.BOX NO. 14 329 ZEBA RAZA 129 7494 KARACHI NO8 MARIAM CHEMBER AKHUNDA REMAN 15 392 MR. -

An Evaluation of Investors' Behavior and Sentiments During Heavy Fluctuation in Stock Index; a Case Study of Pakistan Stock Exchange

Bahria University Journal of Management & Technology: Vol.3, No. 2 An evaluation of investors' behavior and sentiments during heavy fluctuation in stock index; A case study of Pakistan Stock Exchange 1Sumair Farooq, 2Dr. Syed Shabib ul Hassan 1,2 Department of Public Administration, University of Karachi ABSTRACT The role of stock exchange is highly dynamic regarding the capital mobilization in Pakistan and contributes an important role in overall financial sector of economy. The chief purpose of this article is to analyze the behavior and sentiment of investors during the heavy fluctuation in Stock Index at Pakistan Stock Exchange (PSX). The sentiment indexes for stock exchange selected for this research are Total Market Capitalization, Total Listed Capital - Rs., KSE-100" Index, KSE-30" Index, KMI-30 Index, PSX-KMI All Shares Index, New Companies Listed during the year, Listed Capital of New Companies - Rs., New Debt Instruments Listed during the year, Listed Capital of New Debt Instruments - Rs., Average Daily Turnover - Shares in million, Average value of daily turnover - Rs And Average Daily Turnover (Future). The indicators are analyzed by Correlation Analysis. The results prove that investor sentiment has positive effect on market returns. Keywords: Stock Exchange, Investor’s sentiments, Fluctuation, Average value of daily turnover, Market capitalization INTRODUCTION The sentiment of investors refers to common belief, mood and performance expectation of market. It is considered as an emotional factor that might have a direct impact on decision making of investors. The sentiments are rather irrational and based on some noisy information that doesn’t indicate the basic stock characteristics with limited experience of trading, skills or knowledge and might stimulate the investors for trading at illogical times or either led to under or overestimation of performance of stock (Neupane, Paudyal, & Thapa, 2014). -

Formerly: Karachi Stock Exchange Limited) Stock Exchange Building, Stock Exchange Road, Karachi-74000, Phones: 111-001-122

PAKISTAN STOCK EXCHANGE LIMITED (Formerly: Karachi Stock Exchange Limited) Stock Exchange Building, Stock Exchange Road, Karachi-74000, Phones: 111-001-122 CRITERIA FOR SELECTION OF TOP 25 COMPANIES FOR THE YEAR 2016 1) Prerequisites for Selection of Top Companies: a) A minimum distribution of 30% (including at least 15% cash dividend) for the year; b) The Shares of the company are traded 50% of the total trading days during the year c) The company should not be in the Defaulters’ Segment of the Exchange or trading in its shares has not been suspended on account of violation of Listing of Companies & Securities Regulations of the Exchange during the year. 2) The Companies that Qualify above Prerequisites will be selected on the Basis of Highest Marks Obtained as per the following Criteria: a) Capital Efficiency: (i) Shareholders Return on Equity (on the basis of before tax profit) 15% (ii) Ratio of Capital Expenditure to Total Assets 3% (iii) Change in Market Value Added (MVA of a year in the difference 2.5% between Market Value minus Book Value for that year.) b) Dividend Distribution (including Bonus) (i) Total Distribution out of Current Year’s Profit only. (In case 10% dividend/bonus is paid out of prior year’s earnings/reserves, than the dividend/bonus shall be adjusted proportionately) (ii) Payout Ratio (DPS / EPS) 10% c) Growth in Operating Revenue 6% Change in EBITDA Margin (Operating margin) in absolute terms 6% d) Free-Float of Shares 10% Free-Float of shares as a percentage of total shares outstanding e) Turnover of Shares -

Nexus of KSE-30 Index

Developing Country Studies www.iiste.org ISSN 2224-607X (Paper) ISSN 2225-0565 (Online) Vol.6, No.1, 2016 Nexus of KSE-30 Index Muhammad Moazam Khan* MBA/MS, Lecturer Bahauddin Zakariya University, Multan, Pakistan Tahira Batool MS/M. Phil Economics Bahauddin Zakariya University, Multan, Pakistan Aisha Khan MSc Banking and Finance Bahauddin Zakariya University, Multan, Pakistan Muhammad Fayyaz Khokhar MS/M. Phil Business Administration, National College of Business Administration & Economics Multan, Pakistan Abstract The Financial development in Pakistan is mostly represented by Karachi stock exchange 100-Index with ignorance of Karachi stock exchange 30-Index which was established to represent financial development Indicator and economic growth indicator as well in Pakistan. So, this study will be investigate the relationship of financial development and economic growth in Pakistan by taking KSE-30 Index, KSE-All Share Index and KSE-100 Index for financial development in Pakistan. In this study time series data varying from 1992 to 2013 is investigated by different econometric tools i.e. Augmented Dickey Fuller (ADF) unit root test, Johansen Cointegration method and Granger causality test. The results of these tools showed that a positive relationship exists between financial development and Economic growth of Pakistan both in long run and short run perspectives. The result also derived that there is bidirectional causality relationship between financial development and economic growth in Pakistan Keywords: Financial Development, Economic Growth, KSE 30-Index 1. Introduction There are many debates in past about the consequences of financial development effecting economic growth. Economic growth is the ability of the economy to increase its productive capacity in terms of goods and services over the period of time. -

Abbott Laboratories (Pakistan) Limited List of Non-Cnic As at May 13, 2019 S.No Folio Name Address Holding 1 95 Mr

ABBOTT LABORATORIES (PAKISTAN) LIMITED LIST OF NON-CNIC AS AT MAY 13, 2019 S.NO FOLIO NAME ADDRESS HOLDING 1 95 MR. AKHTER HUSAIN C-182, BLOCK-C 14 NORTH NAZIMABAD KARACHI 2 126 MR. AZIZUL HASAN KHAN FLAT NO. A-31 181 ALLIANCE PARADISE APARTMENT PHASE-I, II-C/1 NAGAN CHORANGI, NORTH KARACHI KARACHI. 3 131 MR. ABDUL RAZAK HASSAN KISMAT TRADERS 53 THATTAI COMPOUND KARACHI-74000. 4 169 MISS NUZHAT 469/2 AZIZABAD 1,610 FEDERAL 'B' AREA KARACHI 5 223 HUSSAINA YOUSUF ALI NAZRA MANZIL FLAT NO 2 112 1ST FLOOR, RODRICK STREET SOLDIER BAZAR NO. 2 KARACHI 6 244 MR. ABDUL RASHID NADIM MANZIL LY 8/44 2 5TH FLOOR, ROOM 37 HAJI ESMAIL ROAD GALI NO 3, NAYABAD KARACHI 7 270 MR. MOHD. SOHAIL FOURTH FLOOR 192 HAJI WALI MOHD BUILDING MACCHI MIANI MARKET ROAD KHARADHAR KARACHI 8 290 MOHD. YOUSUF BARI KUTCHI GALI NO 1 1,269 MARRIOT ROAD KARACHI 9 298 MR. ZAFAR ALAM SIDDIQUI A/192 BLOCK-L 192 NORTH NAZIMABAD KARACHI 10 300 MR. RAHIM 32 JAFRI MANZIL 1,269 KUTCHI GALI NO 3 JODIA BAZAR KARACHI 11 301 MRS. SURRIYA ZAHEER A-113 BLOCK NO 2 1,610 GULSHAD-E-IQBAL KARACHI 12 320 CH. ABDUL HAQUE C/O MOHD HANIF ABDUL AZIZ 583 HOUSE NO. 265-G, BLOCK-6 EXT. P.E.C.H.S. KARACHI. 13 327 AMNA KHATOON 47-A/6 1,269 P.E.C.H.S. KARACHI 14 329 ZEBA RAZA WHITEWAY ROYAL CO. 129 10-GULZAR BUILDING ABDULLAH HAROON ROAD P.O.BOX NO. -

Risk Disclosure

TRE Certicate Holder – 149 Pakistan Stock Exchange Limited (Formerly Karachi Stock Exchange Ltd.) Broker Registration No. BRK-169 JS Global Capital Limited REGISTERED OFFICE: The Center, 17th & 18th Floor, Plot No. 28, S.B.5, Abdullah Haroon Road, Karachi. UAN: (92-21) 111-574-111 Fax: (92-21) 32800167 equity JS Global has also been awarded BMR-1 (Broker Management Rating) ranking by PACR. 1 2 JS Global 3 4 5 Date: Account Holder JS Global Capital Limited Islamabad Branch: Room No. 413, 4th Floor, ISE Towers, The Center, 17th & 18th Floor, Plot No. 28, S.B.5, 55-B,Jinnah Avenue, Islamabad, Pakistan. Abdullah Haroon Road, Karachi. UAN: +92 51 111 574 111, Fax: +92 51 289 4417 UAN: +92 21 111 574 111 Stock Exchange Branch: Room No. 634, 6th Floor, www.jsglobalonline.com Stock Exchange Building, Stock Exchange Road, Karachi, Pakistan. www.jsgcl.com Tel: +92 21 3242 7461, Fax: 92 21 3246 2640, 3241 5136 Pakistan Stock Exchange Karachi Gulshan Branch: Suite No.607/A, 6th Floor, Al Ameen Towers, www.psx.com.pk Plot # E-2, Block-10, Gulshan-e-Iqbal, Main NIPA, Karachi. Securities Exchange Commission of Pakistan Tel: +92 21 3483 5701-9 www.secp.gov.pk Hyderabad Branch: Shop # 20, Ground Floor, Auto Bhan Towers, National Clearing Company of Pakistan Auto Bhan Road, Unit # 3, Latifabad, Hyderabad. www.nccpl.com.pk Tel: +92 22-2114651-55, Central Depositary Company of Pakistan Multan Branch: Oce No. 608 – A, 6th Floor, The United Mall, www.cdc.com Plot # 74, Abdali Road, Multan, Pakistan. Pakistan Mercantile Exchange Tel: +92 61 457 0260 - 66,68,69, Fax: +92 61 457 0267 www.pmex.com.pk Faisalabad Branch: G4, Mezan Executive Tower, Liaquat Road, Faisalabad, Pakistan. -

Institutional Ownership and Corporate Value: Evidence from Karachi Stock Exchange (KSE) 30-Index Pakistan

Institutional ownership and corporate value: Evidence from Karachi Stock Exchange (KSE) 30-Index Pakistan INSTITUTIONAL OWNERSHIP AND CORPORATE VALUE: EVIDENCE FROM KARACHI STOCK EXCHANGE (KSE) 30-INDEX PAKISTAN Datum prijave: 17.02.2015. UDK: 336.7 Datum prihvaćanja: 29.05.2015. Pregledni rad Safdar Hussain Tahir Assistant Professor, Banking and Finance Government College University Faisalabad, Pakistan E-mail: [email protected] Muhammad Saleem MS-Scholar Department of Banking & Finance, Government College University Faisalabad, Pakistan Humaira Arshad MS-Scholar Department of Banking & Finance, Government College University Faisalabad, Pakistan SUMMARY - The study aims to explore the relationship between institutional ownership and firm performance. To obtain the targeted objectives, the required data, ranging from 2008 to 2013 were collected from annual reports and financial statements of concerned firms. Such type of data contains endogeneity problems. In order to deal with endogeneity problem, Durbin-Wu-Houseman test was applied. Among many advance econometric techniques, OLS and 2SLS were found appropriate to estimate the coefficient of interest. Institutional ownership being endogenous variable was found significantly and positively related with firm performance. Firm performance was found negatively related with debt ratio and fix expenditures. Finally it was found that institutional investors take more interest in firms having higher dividend payout ratio. Key Words: Institutional ownership, Firm performance, Agency Problem, Endogeneity, DW and 2SLS JEL Classification: G34 1. INTRODUCTION in the corporate decision making process through their voting right in company’s meetings and try to Institutional investors are important stake influence the firm top management to take care holder of today’s financial market and appeared as the long-term interest of shareholders. -

April 2021 � � �� - ٓ���� ������ SAVE up TO

Smart & Easy Savings! NBP FUNDS Managing Your Savings Fund Manager Report Conventional Schemes April 2021 � � �� - ٓ���� ������ SAVE UP TO OF YOUR INCOME TAX ��� � ��، ���� �� GOOD OPPORTUNITY FOR SALARIED PERSON Note: Detailed monthly reports of NBP Funds are also available on our website www.nbpfunds.com AM1 NBP Fund Management Limited For More Information & Investment Rated by PACRA *Subject to conditions as per section 62 and 63 of the Income Tax Ordinance, 2001. Disclaimer: All investment in mutual funds and pension funds are subject to market risk. Past performance is not necessarily indicative of future results. Please read the Offering Documents to understand the investment policies and the risks involved. NBP Funds or any of its sales representative cannot guarantee preservation / protection of capital and / or expected returns / profit on investments. NBP FUNDS Table of Contents Managing Your Savings Table of Contents Table 1-2 CEO’s Write-up 03 Capital Market Review NBP Government Securities 04 05 NBP Money Market Fund Liquid Fund NGSLF NMMF 06 NBP Government Securities NBP Government Securities Savings Fund 07 Plan - I NGSSF NGSP-I 08 NBP Mahana Amdani Fund 09 NBP Financial Sector Income Fund NMAF NFSIF 10 NBP Income Opportunity Fund 11 NBP Savings Fund NIOF NBP-SF 12 NBP Sarmaya Izafa Fund 13 NBP Balanced Fund NSIF NBF 14 NBP Stock Fund 15 NBP Financial Sector Fund NSF NFSF 16 NBP Pakistan Growth Exchange 17 NAFA Pension Fund NBP-GETF Traded Fund NPF NBP FUNDS Managing Your Savings Historical Performance of Various Investment Avenues The last four years have been challenging for the stock market investors. -

Year Book 2010–2011

i Year Book 2010 – 2011 Government of Pakistan Finance Division Islamabad www.finance.gov.pk CONTENTS ii S. Subject Page No. No. Preface 1 Mission Statement 2 General 3 Functions of the Finance Division 3 Organizational Chart of the Finance Division 5 A. HRM Wing 6 B. Budget Wing 10 Budget and its Functions 10 Budget Wing’s Profile 11 Performance of Budget Wing 12 Medium Term Budgetary Framework (MTBF) 24 Budget Implementation Unit (BIU) 25 C. Corporate Finance Wing 28 D. Economic Adviser’s Wing 30 E. Expenditure Wing 32 F. External Finance Wing 34 G. External Finance (Policy Wing) 38 H. Economic Reforms Unit (ERU) 47 I. Finance Division (Military) 51 J. Development Wing 54 iii K. Internal Finance Wing 57 State Bank of Pakistan 57 National Bank of Pakistan 57 First Women Bank Limited 58 Pakistan Security Printing Corporation 59 House Building Finance Corporation 60 SME Bank Limited 61 Financial Monitoring Unit (FMU) Karachi 62 Zari Taraqiati Bank Ltd. (ZTBL) 63 L. Investment Wing 65 Competitiveness Support Fund (CFS) 65 National Investment Trust Limited (NITL) 66 Competition Commission of Pakistan(CCP) 72 Securities and Exchange Commission of Pakistan 86 Joint Investment Companies in Pakistan 103 Infrastructure Project Development Facility (IPDF) 104 M. Provincial Finance 105 O. Regulations Wing 113 P. Auditor General of Pakistan 121 Central Directorate of National Savings(CDNS) 132 Controller General of Accounts (CGA) 136 Pakistan Mint 139 Debt Policy Coordination Office (DPCO) 141 iv COMPILATION TEAM 1. MR. MUHAMMAD ANWAR KHAN Senior Joint Secretary (HRM) 2. MR. MIR AFZAL KHAN Deputy Secretary (Services) 3. -

Evidence from Karachi Stock Exchange

CORE Metadata, citation and similar papers at core.ac.uk Provided by International Institute for Science, Technology and Education (IISTE): E-Journals Developing Country Studies www.iiste.org ISSN 2224-607X (Paper) ISSN 2225-0565 (Online) Vol.5, No.9, 2015 Investment Behavior and Stock Preference of an Individual Investor: Evidence from Karachi Stock Exchange Muhammad Waseem Ur Rehman 1 Kashif Arif 2* 1.MS-Finance Scholar, Mohammad Ali Jinnah University, Karachi 2.Faculty of Business Administration, Mohammad Ali Jinnah University, Karachi *Corresponding Author: Email: [email protected] Abstract The purpose of the research is to study the individual investor’s behavior in Karachi Stock Exchange. In this study data was collected from individual clients at Karachi Stock Exchange. Type of the study is descriptive and deductive approach was used. The data was collected from 389 respondents at Karachi Stock Exchange with the help of designed questionnaire. The individual behavior is tested with the help of regression analysis. There are three regression models developed to study the relationship and impact of Independent variables (Accounting information & financial literacy, overconfidence, irrationality and biasness in decision making) on three different dependent variables (Preference of capital gain, preference of dividend and gambling). Results explain no relationship toward preference of capital gain but the significant relationships found toward preference of dividend and gambling. So it can be easily concluded that the investors at Karachi Stock Exchange do not prefer capital gain but they want better payout and speculation in the market. There were also studied that the accounting information & financial literacy increase the behavior toward preference of dividend and decrease toward gambling. -

Is Pakistan Stock Market Moving

Asian Economic and Financial Review, 2014, 4(6): 808-836 Asian Economic and Financial Review journal homepage: http://www.aessweb.com/journals/5002 IS PAKISTAN STOCK MARKET MOVING TOWARDS WEAK-FORM EFFICIENCY? EVIDENCE FROM THE KARACHI STOCK EXCHANGE AND THE RANDOM WALK NATURE OF FREE-FLOAT OF SHARES OF KSE 30 INDEX Ushna Akber Lahore University of Management Sciences Nabeel Muhammad Lahore University of Management Sciences ABSTRACT In this study, we have attempted to seek evidence for weak-form of market efficiency for KSE 100 Index because over the last five years KSE 100 Index has shown substantial growth as compared to other emerging stock markets. Index returns have been studied from 1st January, 1992 to 30th April, 2013. For further analysis, return series has been divided into sub-periods. The paper has made use of primarily Non-Parametric tests as well as Parametric tests. For further analysis, Runs test has also been run on 20 companies return series for comparison purpose with the results of index return series. In addition, from KSE 30 Index, 20 companies return series based on the free- float of shares have also been analyzed through Runs test to check if increase in numbers of floating shares does increase the randomness in return series or not. To our knowledge, this paper is the first one on KSE 100 Index to study the overall time frame of return series of KSE 100 Index of 22 years with the several random walk and weak-form efficiency tests to ensure the consistency of results; and to compare the results of runs test of index return series with the results of runs test on companies return series from KSE 100 and KSE 30 Indexes.