The Pfizer-Wyeth and Merck-Schering Plough Mergers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Print Layout 1

TECHNICAL PROGRAM Monday, March 19 5:00 – 8:00 pm Welcome Reception Tuesday, March 20 8:00 – 10:00 Session 1: Setting the Conference Context and Drivers Chair: Geoff Slaff (Amgen) Roger Perlmutter (Amgen) Conquering the Innovation Deficit in Drug Discovery Helen Winkle (CDER, FDA) Regulatory Modernization 10:00 – 10:30 Break Vendor and poster review 10:30 – 12:30 Session 2: Rapid Cell Line Development and Improved Expression System Development Chairs: Timothy Charlebois (Wyeth) and John Joly (Genentech) Amy Shen (Genentech) Stable Antibody Production Cell-Line Development with an Improved Selection Process and Accelerated Timeline Mark Leonard (Wyeth) High-Performing Cell-Line Development within a Rapid and Integrated Platform Process Control Pranhitha Reddy (Amgen) Applying Quality-by-Design to Cell Line Development Lin Zhang (Pfizer) Development of a Fully-Integrated Automated System for High-Throughput Screening and Selection of Single Cells Expressing Monoclonal Antibodies 12:30 – 2:00 Lunch Vendor and poster review 2:00 – 4:30 Session 3: High-Throughput Bulk Process Development Chairs: Brian Kelley (Wyeth) and Jorg Thommes (Biogen Idec) Colette Ranucci (Merck) Development of a Multi-Well Plate System for High-Throughput Process Development Min Zhang (SAFC Biosciences) CHO Media Library – an Efficient Platform for Rapid Development and Optimization of Cell Culture Media Supporting High Production of Pharmaceutical Proteins in Chinese Hamster Ovary Cells Nigel Titchener-Hooker The Use of Ultra-Scale-Down Approaches to Enable Rapid Investigation -

Pfizer and Mylan Will Own 57% and 43% of the New Company (“Newco”), Respectively

DEAL PROFILE PFIZER | MYLAN VALUES 57% 43% $12.0bn PFIZER SHARE OF NEWCO MYLAN SHARE OF NEWCO NEW DEBT RAISED Pfizer Inc. (NYSE:PFE) Pfizer Inc. (“Pfizer”) is a pharmaceutical company that develops, manufactures, and sells products in internal medicine, vaccines, oncology, inflammation & immunology, and rare diseases. Upjohn, a subsidiary of Pfizer, is composed of Pfizer’s oral solid generics and off-patent drugs franchise, such as Viagra, Lipitor, and Xanax. Upjohn has a strong focus in emerging markets, and is headquartered in Shanghai, China. TEV: $265.4bn LTM EBITDA: $22.5bn LTM Revenue: $55.7bn Mylan N.V. (NASDAQ:MYL) Mylan N.V. (“Mylan”) is a pharmaceutical company that develops, manufactures, and commercializes generic, branded-generic, brand-name, and over-the-counter products. The company focuses in the following therapeutic areas: cardiovascular, CNS and anesthesia, dermatology, diabetes and metabolism, gastroenterology, immunology, infectious disease, oncology, respiratory and allergy, and women’s health. Mylan was founded in 1961 and is headquartered in Canonsburg, PA. TEV: $23.9bn LTM EBITDA: $3.5bn LTM Revenue: $11.3bn Bourne Partners provides strategic and financial advisory services to BOURNE clients throughout the business evolution life cycle. In order to provide PARTNERS the highest level of service, we routinely analyze relevant industry MARKET trends and transactions. These materials are available to our clients and partners and provide detailed insight into the pharma, pharma services, RESEARCH OTC, consumer health, and biotechnology sectors. On July 29, 2019, Pfizer announced the spin-off of its off-patent drug unit, Upjohn, in order to merge the unit with generic drug manufacturer, Mylan. -

Moderna Vaccine Day Presentation

Zika Encoded VLP mRNA(s) RSV CMV + EBV SARS-CoV- RSV-ped 2 Flu hMPV/PIV3 H7N9 Encoded mRNA(s) Ribosome Protein chain(s) First Vaccines Day April 14, 2020 © 2020 M oderna Therapeutics Forward-looking statements and disclaimers This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, as amended including, but not limited to, statements concerning; the impact of the SARS-CoV-2 pandemic on the Company’s clinical trials and operations; the timing and finalization of a dose-confirmation Phase 2 study and planning for a pivotal Phase 3 study for mRNA-1647; the status and outcome of the Phase 1 clinical trial for mRNA-1273 being conducted by NIH; the next steps and ultimate commercial plan for mRNA-1273; the size of the potential market opportunity for mRNA-1273; the size of the potential commercial market for novel vaccines produced by Moderna or others; the potential peak sales for the Company’s wholly-owned vaccines; the probability of success of the Company’s vaccines individually and as a portfolio; and the ability of the Company to accelerate the research and development timeline for any individual product or the platform as a whole. In some cases, forward-looking statements can be identified by terminology such as “will,” “may,” “should,” “expects,” “intends,” “plans,” “aims,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue,” or the negative of these terms or other comparable terminology, although not all forward-looking statements contain these words. The forward-looking statements in this press release are neither promises nor guarantees, and you should not place undue reliance on these forward-looking statements because they involve known and unknown risks, uncertainties, and other factors, many of which are beyond Moderna’s control and which could cause actual results to differ materially from those expressed or implied by these forward-looking statements. -

Wyeth Pharmaceuticals Inc., a Subsidiary of Pfizer Inc Mylotarg

Mylotarg FDA ODAC Briefing Document 11 July 2017 WYETH PHARMACEUTICALS INC., A SUBSIDIARY OF PFIZER INC MYLOTARG (gemtuzumab ozogamicin; PF-05208747) In combination with chemotherapy for the treatment of previously untreated de novo CD33-positive acute myeloid leukemia and as monotherapy for the treatment of CD33-positive acute myeloid leukemia in first relapse FDA ONCOLOGIC DRUGS ADVISORY COMMITTEE BRIEFING DOCUMENT (BLA 761060) Meeting Date: 11 July 2017 ADVISORY COMMITTEE BRIEFING MATERIALS: AVAILABLE FOR PUBLIC RELEASE 090177e18c1aa788\Approved\Approved On: 12-Jun-2017 13:05 (GMT) Page 1 Mylotarg FDA ODAC Briefing Document 11 July 2017 TABLE OF CONTENTS TABLE OF CONTENTS...........................................................................................................2 LIST OF TABLES.....................................................................................................................5 LIST OF FIGURES ...................................................................................................................6 1. EXECUTIVE SUMMARY .................................................................................................7 1.1. Introduction..............................................................................................................7 1.2. Rationale for Mylotarg Dosing Regimens ...............................................................8 1.3. Mylotarg in Patients With Previously Untreated De Novo AML............................9 1.4. Mylotarg in Patients With AML in First Relapse..................................................11 -

Eople on the Move Eople on the Move

eopleeople onon PPthethe movemove Pierre Cloutier Sylvie Denis Gilles Fortin Nicolas Gauvin Bernard Michaud Anna Kratochvil Abbott Abbott Abbott Abbott Abbott Abbott Laboratories Laboratories Laboratories Laboratories Laboratories Laboratories Gary Schmid Alison Shore Eric Bergey Kal Dreisziger Lidia Krupka Abbott Abbott L’Académie- Allard-Johnson Allard-Johnson Laboratories Laboratories Ogilvy Communications Communications (Montreal) (Montreal) Pierre Cloutier, formerly Business Nicolas Gauvin, formerly Senior Alison Shore, formerly Product Unit Manager, Oncology, Product Manager, GI, has been Manager, has been promoted to Pharmaceutical Products Division, promoted to Marketing Manager, GI, Senior Product Manager, Metabolic has been promoted to Director, Pharmaceutical Products Division, at (Meridia), Pharmaceutical Products Customer Relations (Corporate), at Abbott Laboratories. Division, at Abbott Laboratories. Abbott Laboratories. Bernard Michaud, formerly Senior Eric Bergey, formerly International Sylvie Denis, formerly Business Unit Product Manager, Anti-infectives, has OTC Product Manager at World Manager, Cardiovascular & been promoted to Marketing Headquarters of Pharmacia & Metabolic, has been promoted to Manager, Anti-infectives, Upjohn in Sweden and, most Director of Sales, Primary Care, Pharmaceutical Products Division, at recently, Account Supervisor at Jeffrey Pharmaceutical Products Division, at Abbott Laboratories. Simbrow Associates (Montreal), has Abbott Laboratories. been appointed Account Director at Anna Kratochvil, -

Statements Contained in This Release As the Result of New Information Or Future Events Or Developments

Pfizer and BioNTech Provide Update on Booster Program in Light of the Delta-Variant NEW YORK and MAINZ, GERMANY, July 8, 2021 — As part of Pfizer’s and BioNTech’s continued efforts to stay ahead of the virus causing COVID-19 and circulating mutations, the companies are providing an update on their comprehensive booster strategy. Pfizer and BioNTech have seen encouraging data in the ongoing booster trial of a third dose of the current BNT162b2 vaccine. Initial data from the study demonstrate that a booster dose given 6 months after the second dose has a consistent tolerability profile while eliciting high neutralization titers against the wild type and the Beta variant, which are 5 to 10 times higher than after two primary doses. The companies expect to publish more definitive data soon as well as in a peer-reviewed journal and plan to submit the data to the FDA, EMA and other regulatory authorities in the coming weeks. In addition, data from a recent Nature paper demonstrate that immune sera obtained shortly after dose 2 of the primary two dose series of BNT162b2 have strong neutralization titers against the Delta variant (B.1.617.2 lineage) in laboratory tests. The companies anticipate that a third dose will boost those antibody titers even higher, similar to how the third dose performs for the Beta variant (B.1.351). Pfizer and BioNTech are conducting preclinical and clinical tests to confirm this hypothesis. While Pfizer and BioNTech believe a third dose of BNT162b2 has the potential to preserve the highest levels of protective efficacy against all currently known variants including Delta, the companies are remaining vigilant and are developing an updated version of the Pfizer-BioNTech COVID-19 vaccine that targets the full spike protein of the Delta variant. -

Johnson & Johnson and Pfizer Inc., Analysis of Agreement Containing

ANALYSIS OF AGREEMENT CONTAINING CONSENT ORDERS TO AID PUBLIC COMMENT In the Matter of Johnson & Johnson and Pfizer Inc. File No. 061-0220, Docket No. C-4180 I. Introduction The Federal Trade Commission (“Commission”) has accepted, subject to final approval, an Agreement Containing Consent Orders (“Consent Agreement”) from Johnson & Johnson (“J&J”) and Pfizer Inc. (“Pfizer”), which is designed to remedy the anticompetitive effects that would otherwise result from J&J’s proposed acquisition of Pfizer Consumer Healthcare. Under the terms of the proposed Consent Agreement, the parties will be required to divest: (1) Pfizer’s Zantac® H-2 blocker business; (2) Pfizer’s Cortizone® hydrocortisone anti-itch business; (3) Pfizer’s Unisom® nighttime sleep-aid business; and (4) J&J’s Balmex® diaper rash treatment business. The proposed Consent Agreement has been placed on the public record for thirty (30) days for receipt of comments by interested persons. Comments received during this period will become part of the public record. After thirty (30) days, the Commission will again review the proposed Consent Agreement and will decide whether it should withdraw from the proposed Consent Agreement, modify it, or make final the Decision and Order (“Order”). Pursuant to a Stock and Asset Purchase Agreement dated June 25, 2006, J&J proposes to acquire certain voting securities and assets comprising Pfizer’s Consumer Healthcare business in a transaction valued at approximately $16.6 billion (“Proposed Acquisition”). The Commission’s complaint alleges that the Proposed Acquisition, if consummated, would violate Section 7 of the Clayton Act, as amended, 15 U.S.C. -

Amgen and Wyeth Statement on FDA Announcement About Tumor Necrosis Factor (TNF) Blockers

Amgen and Wyeth Statement on FDA Announcement About Tumor Necrosis Factor (TNF) Blockers August 4, 2009 THOUSAND OAKS, Calif. and COLLEGEVILLE, Pa., Aug. 4 /PRNewswire-FirstCall/ -- Amgen (Nasdaq: AMGN) and Wyeth Pharmaceuticals, a division of Wyeth (NYSE: WYE), issued a statement in response to the Food and Drug Administration (FDA) announcement regarding the results of a safety review of Tumor Necrosis Factor (TNF) blockers [marketed as Remicade (infliximab), Enbrel (etanercept), Humira (adalimumab), Cimzia (certolizumab pegol) and Simponi (golimumab)]. This safety review was the subject of an FDA Early Communication in June 2008 pertaining to cases of malignancy in pediatric patients exposed to a TNF blocker. As a result of this review, the FDA has required strengthened warnings about the occurrence of lymphoma and other cancers in children and young adults using these medicines. AMGEN AND WYETH STATEMENT: Amgen and Wyeth believe that ENBREL continues to offer a favorable benefit-risk relationship for patients with the diseases for which it is indicated to treat, including moderate to severe Juvenile Idiopathic Arthritis (JIA). JIA can be a serious and potentially debilitating condition. Amgen will work with the FDA to update the U.S. Prescribing Information, and Medication Guide for ENBREL as described in the FDA communication which can be read at http://www.fda.gov/NewsEvents/Newsroom/PressAnnouncements/ucm175803.htm. In addition, Amgen and Wyeth will communicate the revised product labeling to both physicians and patients. ENBREL was first approved for JIA in the U.S. in 1999. It is estimated through postmarketing data that approximately 13,847 pediatric patients have been treated with ENBREL globally through February 2009, accounting for approximately 44,600 patient-years of exposure. -

Our 2019 Peer Groups – Competitive Pay Positioning

94228_04_Pfizer_Exec_Comp_Part 1.qxp_04 3/5/20 6:48 PM Page 72 ExEcutivE compEnsation SECTION 2 – HOW WE DETERMINE EXECUTIVE COMPENSATION This chart explains the Compensation Committee’s process for determining our executive pay targets. Analysis/Tools How We Use This Information Purpose Peer and • We target the median compensation values of our peer and comparator groups to help determine Establishes a competitive pay Comparator Group an appropriate total level and pay mix for our executives. framework using comparator Pay Analysis groups’ median compensation • Each compensation target is assigned a numbered salary grade to simplify our compensation values, to help determine an Data source: publicly administration process. optimum pay mix of base pay, available financial – Each salary grade has a range of salary levels: including minimum, midpoint and maximum. annual short-term and long- and compensation term incentive targets information as – minimum and maximum salary range levels for each grade are set 25% below and above the reported by our salary range midpoint to approximate the bottom and top pay quartiles for positions assigned pharmaceutical peer to that grade. and General industry comparator Groups • We review this framework/salary grade as a guide to determine the preliminary salary recommendation, target annual short-term incentive award opportunity, and target annual long-term (typically from incentive value for each executive position. surveys and public filings) note: the actual total compensation and/or amount of each compensation element for an individual executive may be more or less than this median. Tally Sheets • We review a “tally sheet” for each ELt member that includes target and actual total compensation provides additional elements, stock ownership as well as benefits information, accumulated deferred compensation, information that assists the Data source: and outstanding equity award values. -

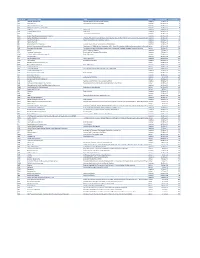

Mvx List.Pdf

MVX_CODE manufacturer_name Notes status last updated date manufacturer_id AB Abbott Laboratories includes Ross Products Division, Solvay Inactive 16-Nov-17 1 ACA Acambis, Inc acquired by sanofi in sept 2008 Inactive 28-May-10 2 AD Adams Laboratories, Inc. Inactive 16-Nov-17 3 ALP Alpha Therapeutic Corporation Inactive 16-Nov-17 4 AR Armour part of CSL Inactive 28-May-10 5 AVB Aventis Behring L.L.C. part of CSL Inactive 28-May-10 6 AVI Aviron acquired by Medimmune Inactive 28-May-10 7 BA Baxter Healthcare Corporation-inactive Inactive 28-May-10 8 BAH Baxter Healthcare Corporation includes Hyland Immuno, Immuno International AG,and North American Vaccine, Inc./acquired somInactive 16-Nov-17 9 BAY Bayer Corporation Bayer Biologicals now owned by Talecris Inactive 28-May-10 10 BP Berna Products Inactive 28-May-10 11 BPC Berna Products Corporation includes Swiss Serum and Vaccine Institute Berne Inactive 16-Nov-17 12 BTP Biotest Pharmaceuticals Corporation New owner of NABI HB as of December 2007, Does NOT replace NABI Biopharmaceuticals in this codActive 28-May-10 13 MIP Emergent BioSolutions Formerly Emergent BioDefense Operations Lansing and Michigan Biologic Products Institute Active 16-Nov-17 14 CSL bioCSL bioCSL a part of Seqirus Inactive 26-Sep-16 15 CNJ Cangene Corporation Purchased by Emergent Biosolutions Inactive 29-Apr-14 16 CMP Celltech Medeva Pharmaceuticals Part of Novartis Inactive 28-May-10 17 CEN Centeon L.L.C. Inactive 28-May-10 18 CHI Chiron Corporation Part of Novartis Inactive 28-May-10 19 CON Connaught acquired by Merieux Inactive 28-May-10 21 DVC DynPort Vaccine Company, LLC Active 28-May-10 22 EVN Evans Medical Limited Part of Novartis Inactive 28-May-10 23 GEO GeoVax Labs, Inc. -

(“Viatris”) to the Shareholders of Pfizer Inc

NOTIFICATION TO CANADIAN SHAREHOLDERS With respect to the distribution of the shares of Viatris Inc. (“Viatris”) to the shareholders of Pfizer Inc. (“Pfizer”) (the “Distribution”) on November 16, 2020 (the “Distribution Date”), Pfizer filed with the Canada Revenue Agency (“CRA”), within the prescribed time, the information that will allow the CRA to determine whether the Distribution qualifies as an “eligible distribution” for the purposes of section 86.1 of the Income Tax Act (Canada). Provided that the CRA determines that the Distribution qualifies as an eligible distribution, a Canadian resident Pfizer shareholder as of the date of the Distribution who acquires Viatris shares pursuant to the Distribution must elect in writing (filed with the taxpayer's return of income for the year in which the Distribution occurs) to have section 86.1 of the Income Tax Act (Canada) apply to the Distribution, such that the Distribution will not be viewed as a taxable foreign dividend and should not be included in such shareholder’s income. A shareholder who makes such an election will be required to allocate the aggregate cost basis amount of such shareholder’s Pfizer shares held immediately before the Distribution among the Viatris shares received in the Distribution and the Pfizer shares (in respect of which such Viatris shares were received) in proportion to their relative fair market values immediately after the Distribution. Fair market value is not defined for these purposes and shareholders should consult a Canadian tax advisor. One method to determine the fair market value is to use the closing prices of the Pfizer and Viatris common stock on the Distribution Date. -

In the United States District Court for the District of Delaware

Case 1:20-cv-00561-UNA Document 1 Filed 04/24/20 Page 1 of 27 PageID #: 1 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE AMGEN INC. and AMGEN MANUFACTURING, LIMITED, C.A. No. ________ Plaintiffs, v. HOSPIRA, INC. and PFIZER INC., DEMAND FOR JURY TRIAL Defendants. COMPLAINT Plaintiffs Amgen Inc. and Amgen Manufacturing, Limited (collectively, “Plaintiffs”), by and through their undersigned attorneys, for their Complaint against Defendants Hospira, Inc. and Pfizer Inc. (collectively, “Defendants”) hereby allege as follows: THE PARTIES 1. Amgen Inc. is a corporation existing under the laws of the State of Delaware, with its principal place of business at One Amgen Center Drive, Thousand Oaks, California, 91320. Amgen Inc. discovers, develops, manufactures, and sells innovative therapeutic products based on advances in molecular biology, recombinant DNA technology, and chemistry. Founded in 1980, Amgen Inc. is a pioneer in the development of biological human therapeutics. Today, Amgen Inc. is one of the largest biotechnology companies in the world, fueled in part by the success of NEUPOGEN® (filgrastim). 2. Amgen Manufacturing, Limited (“AML”) is a corporation existing under the laws of Bermuda with its principal place of business in Juncos, Puerto Rico. AML manufactures and sells biologic medicines for treating particular diseases in humans. AML is a wholly-owned subsidiary of Amgen Inc. Case 1:20-cv-00561-UNA Document 1 Filed 04/24/20 Page 2 of 27 PageID #: 2 3. On information and belief, Hospira, Inc. (“Hospira”) is a corporation existing under the laws of the State of Delaware, with its principal place of business at 275 North Field Drive, Lake Forest, Illinois 60045.