Wanxiang Group Strategic Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

On the Road Again a Financial and Extra-Financial Analysis of the Auto Industry

SRI - EFI Sector Research On the road again A Financial and Extra-financial Analysis of the Auto Industry p Caught in the void Î fuel prices, carbon and pollution p Charting new terrain becomes key Î alternative power trains p Cost is king Î it determines the way forward p Don’t forget Î governance, BRICs, legacy costs and offshoring p Toyota is our global champion Î other winners could emerge Pierre-Yves Quéméner, Financial Analyst +33 1 45 96 77 63 [email protected] November 2005 Valéry Lucas Leclin, SRI Analyst +33 1 45 96 79 23 [email protected] Sarj Nahal, SRI Analyst +33 1 45 96 78 75 [email protected] On the road again This report follows a request from a group of asset managers working with the United Nations to analyse the environmental, social and corporate governance issues that may be material for company performance and to then identify potential impact on company valuations. The United Nations Environment Programme Finance Initiative (UNEP FI) works closely with 160 financial institutions worldwide, to develop and promote linkages between the environment, sustainability and financial performance. UNEP FI Asset Management Working Group (AMWG) explores the association between environmental, social, and governance considerations and investment decision-making. Asset Managers that have participated in this project have combined mandates of 1.7 trillion USD. Asset managers: ABN AMRO Asset Management Brazil Acuity Investment Management BNP Paribas Asset Management BT Financial Group Calvert Group Citigroup Asset Management -

2020 Annual Report Vision

2020 Annual Report Vision To be the global technology leader in efficient power conveyance and energy- management solutions that enable our customers to achieve DANA their sustainability objectives. AT A Mission Our talented people power a customer-centric organization that is continuously improving the performance and efficiency GLANCE of vehicles and machines around the globe. We will consistently deliver superior products and services to our customers and will generate exceptional value for our shareholders. Established in 1904. Employing This mission is embodied in 38,000 people across 141 major our company theme: facilities in 33 countries. Shipping to 14,000 customers in 141 countries. Leveraging a global network Values of technology centers across Honesty and Integrity Good Corporate Citizenship 9 countries. Open Communication Continuous Improvement 2 Sales HIGHLIGHTS FINANCIAL $7.1 billion Adjusted EBITDA1 $593 million Diluted Adjusted EPS2 $0.39 Adjusted Free Cash Flow1 $60 million Future Sales Backlog $700 million All figures as of year-end December 31, 2020. 1 See pages 30-31 of Dana’s 2020 Form 10-K, included herein, for explanation and reconciliation of non-GAAP financial measures. 2 Diluted adjusted EPS is a non-GAAP financial measure, which we have defined as adjusted net income divided by adjusted diluted shares. See the “Quarterly Financial Information and Reconciliations of Non-GAAP Information” on Dana’s Investor Relations website at Dana.com/investors for explanation and calculation of diluted adjusted EPS. 3 SALES -

Annual Report

ai158746681363_GAC AR2019 Cover_man 29.8mm.pdf 1 21/4/2020 下午7:00 Important Notice 1. The Board, supervisory committee and the directors, supervisors and senior management of the Company warrant the authenticity, accuracy and completeness of the information contained in the annual report and there are no misrepresentations, misleading statements contained in or material omissions from the annual report for which they shall assume joint and several responsibilities. 2. All directors of the Company have attended meeting of the Board. 3. PricewaterhouseCoopers issued an unqualified auditors’ report for the Company. 4. Zeng Qinghong, the person in charge of the Company, Feng Xingya, the general manager, Wang Dan, the person in charge of accounting function and Zheng Chao, the manager of the accounting department (Accounting Chief), represent that they warrant the truthfulness and completeness of the financial statements contained in this annual report. 5. The proposal for profit distribution or conversion of capital reserve into shares for the reporting period as considered by the Board The Board proposed payment of final cash dividend of RMB1.5 per 10 shares (tax inclusive). Together with the cash dividend of RMB0.5 per 10 shares (including tax) paid during the interim period, the ratio of total cash dividend payment for the year to net profit attributable to the shareholders’ equity of listed company for the year would be approximately 30.95%. 6. Risks relating to forward-looking statements The forward-looking statements contained in this annual report regarding the Company’s future plans and development strategies do not constitute any substantive commitment to investors and investors are reminded of investment risks. -

Wanxiang Electric Vehicle

WANXIANG TS16949 CERTIFIED Wanxiang Electric Vehicle © Wanxiang, 2011 WANXIANG Wanxiang Electric Vehicle TS16949 CERTIFIED 800,000 Sqr. Ft EV Battery Manufacturing Plant © Wanxiang, 2011 WANXIANG Wanxiang Electric Vehicle TS16949 CERTIFIED Wholly owned by Wanxiang Group ── the largest auto parts company in China Focus on mastering clean-energy technology ,developing saving- energy and environment-protection vehicle Development Strategy: Battery-Motor-Electrical control ── Electrical Vehicle © Wanxiang, 2011 WANXIANG Wanxiang Electric Vehicle TS16949 CERTIFIED Wanxiang Electric Vehicle and Power Batteries 7 projects Awarded by the High-Tech R&D (863) Program of China Electric buses start commercial running since 2006, accumulating millions of miles running experiences EVs and HEVs equipped with WXEV’s Electric Power Train are running in 22 major cities in China. Electric vehicles have been distributed over the country and exported abroad. © Wanxiang, 2011 WANXIANG Wanxiang Electric Vehicle TS16949 CERTIFIED Start making 100Ah LiMnO Electric buses start Production Li-ion Battery Battery EV commercial expansion running 2000 2003 2006 2007 2008 Bought Li-ion battery company in 2000; Trial run on city bus route in China in 2003; JV with City Transit Company, mass production of LiFePO4 in 2006, hundreds of electric vehicles have been equipped with WX’s batteries and have been driven millions miles. Beginning of 2009, WXEV launched into expansion of battery production, invested 1.2 Billion RMB in 1 billion Wh LiFePO4 production. WXEV -

2019 Toyota Land Cruiser Was My “Ride to the Ridge” for NWAPA's

$ June2.00 2019 VISIT www.autonewsonline.com VISIT www.autonewsonline.com “Distributed monthly for 30+ years” LARGEST CONSUMER AUTOMOTIVE NEWSPAPER IN U.S. Distributed at Retail Outlets, Auto Shows & Events 2019 Toyota Land Cruiser was my “RIDE TO THE RIDGE” for NWAPA’s Annual MUDFEST Event (See Page 9 Story) The Best Time To Buy A New Vehicle ................page 2 All New Jeep Gladiator “First Drive” .................. page 3 NWAPA Picks Gladiator As Top Truck ............... page 9 Marysville Toyota Sponsors Strawberry Festival. page 13 Rolls Royce Vancouver Wins Award................. page 14 Showcase Reviews .......................................... page 15 Brandy Falconer “Women In Auto World” ....... page 17 Legend of Auto Gala Partners ......................... page 24 Brent Smith has fond Memories of Nellie ........ page 26 Mecum Indy Auction Tops $70 Million ............ page 27 Case & Galpin Auto Groups, Ryan Falconer, Ed Justice, Jr. & Returning 2019 Toyota Land Cruiser (photo Auto News) Legends to be Honored at Legends Event by Bill McCallum by Bill McCallum in our July Issue. The Toyota Land Cruiser is the highway the Land Cruiser offers in off-road features. As we get closer to the ten year Starting this year we have cre- “big daddy” in the SUV lineup segment leading cargo space for With 10 standard interior fea- anniversary of our Legends of Auto ated a new category to honor at for Toyota. There are very few your next road trip. (81.7 cu. ft.) tures including; Entune touch- Gala Dinner (August 15, 2019) our Legends of Auto Gala Dinner changes with the Land Cruiser in With 18 safety and conve- screen audio system, Premium things are starting to take shape. -

The Ohio Motor Vehicle Industry

Research Office A State Affiliate of the U.S. Census Bureau The Ohio Motor Vehicle Report February 2019 Intentionally blank THE OHIO MOTOR VEHICLE INDUSTRY FEBRUARY 2019 B1002: Don Larrick, Principal Analyst Office of Research, Ohio Development Services Agency PO Box 1001, Columbus, Oh. 43216-1001 Production Support: Steven Kelley, Editor; Jim Kell, Contributor Robert Schmidley, GIS Specialist TABLE OF CONTENTS Page Executive Summary 1 Description of Ohio’s Motor Vehicle Industry 4 The Motor Vehicle Industry’s Impact on Ohio’s Economy 5 Ohio’s Strategic Position in Motor Vehicle Assembly 7 Notable Motor Vehicle Industry Manufacturers in Ohio 10 Recent Expansion and Attraction Announcements 16 The Concentration of the Industry in Ohio: Gross Domestic Product and Value-Added 18 Company Summaries of Light Vehicle Production in Ohio 20 Parts Suppliers 24 The Composition of Ohio’s Motor Vehicle Industry – Employment at the Plants 28 Industry Wages 30 The Distribution of Industry Establishments Across Ohio 32 The Distribution of Industry Employment Across Ohio 34 Foreign Investment in Ohio 35 Trends 40 Employment 42 i Gross Domestic Product 44 Value-Added by Ohio’s Motor Vehicle Industry 46 Light Vehicle Production in Ohio and the U.S. 48 Capital Expenditures for Ohio’s Motor Vehicle Industry 50 Establishments 52 Output, Employment and Productivity 54 U.S. Industry Analysis and Outlook 56 Market Share Trends 58 Trade Balances 62 Industry Operations and Recent Trends 65 Technologies for Production Processes and Vehicles 69 The Transportation Research Center 75 The Near- and Longer-Term Outlooks 78 About the Bodies-and-Trailers Group 82 Assembler Profiles 84 Fiat Chrysler Automobiles NV 86 Ford Motor Co. -

Asian Automotive Newsletter

ASIAN AUTOMOTIVE NEW SLETTER September 201 2, ISSUE 72 A Quarterly newsletter of developments in the auto and auto components markets Throwing modesty to the wind, the big Business Development Asia LLC (“BDA”) CONTENTSC O N T E N T S news for BDA this quarter was our is an investment banking firm which C H I N A 1 success in advising on six transactions in specializes in Asian M&A. We have I N D I A 2 the last month – one each in China, offices in all of the major Asian India, Japan, Korea, Europe and the US. automotive markets, as well as London J A P A N 4 All but one of these transactions involved and New York. If you are interested in K O R E A 4 an Asian buyer, seller or asset. This discussing any of the articles in this M A L A Y S I A 4 geographic reach demonstrates the scale newsletter, or how we can help you in of M&A activity in the middle market and this sector, please contact us. T H A I L A N D 4 BDA’s expertise in Asia and global reach. See this press release for more details: http://www.bdallc.com/bda_pdf/Grands Charles Maynard lam-press-release-6Sept12.pdf Senior Managing Director, [email protected] China BMW Brilliance AutoAuto, the JV between German auto manufacturer BMW and Chinese auto manufacturer Brilliance AutoAuto, plans to establish a new engine Auto Sector Stock Indices (12 mon ths ending 06Sep12 ))) facility in Liaoning province, China. -

Hon Hai Precision Industry Co., Ltd. and Subsidiaries Consolidated Financial Statements and Independent Auditors' Review Repor

HON HAI PRECISION INDUSTRY CO., LTD. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS’ REVIEW REPORT MARCH 31, 2021 AND 2020 (STOCK CODE: 2317) Company Address: No. 2, Ziyou St., Tucheng Industrial District, Tucheng Dist., New Taipei City 236, Taiwan (R.O.C.) Tel: (02)2268-3466 For the convenience of readers, the independent auditors’ report and the accompanying consolidated financial statements have been translated into English from the original Chinese version prepared and used in the Republic of China. If there is any conflict between the English version and the original Chinese version or any difference in the interpretation of the two versions, the Chinese-language independent auditors’ report and consolidated financial statements shall prevail. HON HAI PRECISION INDUSTRY CO., LTD. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS’ REVIEW REPORT MARCH 31, 2021 AND 2020 Table of Contents Item Page I. Front Cover 1 II. Table of Contents 2 III. Review Report of Independent Accountants 3 ~ 4 IV. Consolidated Balance Sheets 5 ~ 6 V. Consolidated Statements of Comprehensive Income 7 ~ 8 VI. Consolidated Statements of Changes in Equity 9 ~ 10 VII. Consolidated Statements of Cash Flows 11 ~ 12 VIII. Notes to the Consolidated Financial Statements 13 ~ 115 1. History and Organization 13 2. Date of Authorization for Issuance of the Consolidated 13 Financial Statements and Procedures for Authorization 3. Application of New Standards, Amendments and 13 ~ 14 Interpretations 4. Summary of Significant Accounting Policies 14 ~ 39 5. Critical Accounting Judgments, Estimates and Assumptions 39 ~ 41 on Uncertainty 6. Details of Significant Accounts 41 ~ 82 7. Related Party Transactions 83 ~ 87 8. -

The Rise of China's Luxury Automotive Industry

Heritage with a High Price Tag: The Rise of China’s Luxury Automotive Industry Sydney Ella Smith AMES 499S Honors Thesis in the Department of Asian and Middle Eastern Studies Duke University Durham, North Carolina April 2018 Guo-Juin Hong Department of Asian and Middle Eastern Studies Supervising Professor Leo Ching Department of Asian and Middle Eastern Studies Committee Member Shai Ginsburg Department of Asian and Middle Eastern Studies Committee Member Heritage with a High Price Tag: The Rise of China’s Luxury Automotive Industry Sydney Ella Smith, B.A. Duke University, 2018 Supervisor: Guo-Juin Hong TABLE OF CONTENTS Author’s Note ...........................................................................................................ii Introduction: For Automobiles, Failure Builds Resiliency ......................................1 Chapter 1: Strategy Perspectives on the Chinese Automotive Industry ...................9 Michael Porter’s “Five-Forces-Model” ........................................................12 Michael Porter’s “Clusters and the New Economics of Competition” ........23 Chapter 2: Luxury Among the Nouveau Riche: The Chinese Tuhao (土豪) .........32 What is Luxury? ...........................................................................................34 Who Buys Luxury? ......................................................................................39 Evolving Trends in Luxury ..........................................................................45 Conclusion: Cars with Chinese Characteristics ......................................................49 -

PLANNING for INNOVATION Understanding China’S Plans for Technological, Energy, Industrial, and Defense Development

PLANNING FOR INNOVATION Understanding China’s Plans for Technological, Energy, Industrial, and Defense Development A report prepared for the U.S.-China Economic and Security Review Commission Tai Ming Cheung Thomas Mahnken Deborah Seligsohn Kevin Pollpeter Eric Anderson Fan Yang July 28, 2016 UNIVERSITY OF CALIFORNIA INSTITUTE ON GLOBAL CONFLICT AND COOPERATION Disclaimer: This research report was prepared at the request of the U.S.-China Economic and Security Review Commission to support its deliberations. Posting of the report to the Commis- sion’s website is intended to promote greater public understanding of the issues addressed by the Commission in its ongoing assessment of US-China economic relations and their implications for US security, as mandated by Public Law 106-398 and Public Law 108-7. However, it does not necessarily imply an endorsement by the Commission or any individual Commissioner of the views or conclusions expressed in this commissioned research report. The University of California Institute on Global Conflict and Cooperation (IGCC) addresses global challenges to peace and prosperity through academically rigorous, policy-relevant research, train- ing, and outreach on international security, economic development, and the environment. IGCC brings scholars together across social science and lab science disciplines to work on topics such as regional security, nuclear proliferation, innovation and national security, development and political violence, emerging threats, and climate change. IGCC is housed within the School -

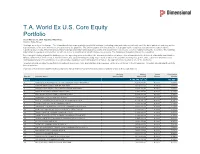

T.A. World Ex U.S. Core Equity Portfolio As of March 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

T.A. World Ex U.S. Core Equity Portfolio As of March 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions -

“New Energy Vehicles”

“New Energy Vehicles” Developments in China, the Netherlands and prospects for Sino-Dutch cooperation in the field of commerce and policy 1 Colophon Place Beijing Assigned by Embassy of the Kingdom of the Netherlands Infrastructure & Environment Department Innovation Department Author(s) Merijn Drenth (intern) Cover Photography by ECNS 2 Index Preface…………………………………………………………………………………………………………………5 Summary………………………………………………………………………………………………………………6 Introduction………………………………………………………………………………..…7 Chapter one – New energy vehicle developments in the Netherlands: Goals & policies...9 - Goals…………………………………………………………………………………...9 - Policies………………………………………………………………………………...9 - Subsidies and fiscal incentives………………………………………………………..10 - Industry and innovation………………………………………………………………11 - Charging infrastructure……………………………………………………………….11 - Results……………………………………………………………………………..…12 - Number of registered NEVs in the Netherlands………………………...…………….12 - Amount of charging points in the Netherlands………………………………………..13 Chapter two – New energy vehicle developments in the Netherlands: Industry & entrepreneurship…………………………………………………………………………....14 - Development Dutch NEV sector…………………………………………………..…14 - Charging infrastructure and smart grids……………………………………………...15 - Propulsion technology and components……………………………………………...16 - Manufacturing and conversion……………………………………………………….17 - Services………………………………………………………………………………18 - International footprint………………………………………………………………...19 Chapter three – New energy vehicle developments in China: Goals & central policies….............................................................................................................................…20