City of Wakefield Metropolitan District Council

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Historical and Contemporary Archaeologies of Social Housing: Changing Experiences of the Modern and New, 1870 to Present

Historical and contemporary archaeologies of social housing: changing experiences of the modern and new, 1870 to present Thesis submitted for the degree of Doctor of Philosophy at the University of Leicester by Emma Dwyer School of Archaeology and Ancient History University of Leicester 2014 Thesis abstract: Historical and contemporary archaeologies of social housing: changing experiences of the modern and new, 1870 to present Emma Dwyer This thesis has used building recording techniques, documentary research and oral history testimonies to explore how concepts of the modern and new between the 1870s and 1930s shaped the urban built environment, through the study of a particular kind of infrastructure that was developed to meet the needs of expanding cities at this time – social (or municipal) housing – and how social housing was perceived and experienced as a new kind of built environment, by planners, architects, local government and residents. This thesis also addressed how the concepts and priorities of the Victorian and Edwardian periods, and the decisions made by those in authority regarding the form of social housing, continue to shape the urban built environment and impact on the lived experience of social housing today. In order to address this, two research questions were devised: How can changing attitudes and responses to the nature of modern life between the late nineteenth and early twentieth centuries be seen in the built environment, specifically in the form and use of social housing? Can contradictions between these earlier notions of the modern and new, and our own be seen in the responses of official authority and residents to the built environment? The research questions were applied to three case study areas, three housing estates constructed between 1910 and 1932 in Birmingham, London and Liverpool. -

Explanatory Memorandum to the City of Leeds (Mayoral Referendum) Order 2012

GROUPED EXPLANATORY MEMORANDUM TO THE CITY OF BIRMINGHAM (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF BRADFORD (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF BRISTOL (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF COVENTRY (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF LEEDS (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF LIVERPOOL (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF MANCHESTER (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF NEWCASTLE-UPON-TYNE (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF NOTTINGHAM (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF SHEFFIELD (MAYORAL REFERENDUM) ORDER 2012 THE CITY OF WAKEFIELD (MAYORAL REFERENDUM) ORDER 2012 2012 Nos. [XXXX] 1. This grouped explanatory memorandum has been prepared by the Department for Communities and Local Government and is laid before Parliament by Command of Her Majesty. 2. Purpose of the instruments Each of these Orders require the local authority named therein to hold a referendum, on 3 May 2012, on whether it should start to operate a mayor and cabinet executive form of governance (i.e. have a directly elected mayor). 3. Matters of special interest to the Joint Committee on Statutory Instruments None. 4. Legislative Context 4.1 Part 1A (Arrangements with respect to local authority governance in England) and new Schedule A1 (Executive arrangements in England: further provision) of the Local Government Act 2000 (“the 2000 Act”) (as inserted by section 21 of, and Schedule 2 to, the Localism Act 2011 (“the 2011 Act”)), make provision for the governance of local authorities in England. One of the permitted forms of governance, under these provisions, is the mayor and cabinet executive. 4.2 Section 9N of the 2000 Act gives the Secretary of State the power by order to require a specified local authority to hold a referendum on whether the authority should have a directly elected mayor. -

Delivering Better Health and Care for Everyone

Delivering better health and care for everyone Summary of our Five Year Plan You can take a look back at some of the improvements West Yorkshire and Harrogate Health and Care Partnership has been making with local people to improve their lives in our short film here You can also find out more about the positive difference our Partnership is making online here Our Partnership We also want to say thank you to all the ^ Photo credit: Leeds Irish Health and Homes people who’ve shared their stories so far and given their views about health and Clinical Commissioning Groups (CCGs) Harrogate and District NHS care in West Yorkshire and Harrogate. NHS Airedale, Wharfedale Foundation Trust and Craven CCG* Leeds Community Healthcare NHS Trust Watch our thank you film here NHS Bradford City CCG* Leeds and York Partnership NHS NHS Bradford Districts CCG* Foundation Trust NHS Calderdale CCG Leeds Teaching Hospitals NHS Trust NHS Greater Huddersfield CCG Locala Community Partnerships The Mid-Yorkshire Hospitals NHS Trust We are committed to honesty and NHS Harrogate and Rural District CCG transparency in all our work and NHS Leeds CCG South West Yorkshire Partnership NHS also producing this information in NHS North Kirklees CCG Foundation Trust Tees Esk and Wear Valleys NHS accessible formats. Our Five Year NHS Wakefield CCG Plan summary is available in: Foundation Trust Yorkshire Ambulance Service NHS Trust • Audio Local councils • EasyRead City of Bradford Metropolitan District Council Others involved • BSL Calderdale Council Healthwatch • Animated -

Homelessness Prevention Strategy 2018

Wolverhampton WV1 1SH City of Wolverhampton Council, Civic Centre, St. Peter’s Square, St.Peter’s Council,Civic Centre, City ofWolverhampton wolverhampton. audio orinanotherlanguagebycalling01902 551155 You can get this information in large print, braille, WolverhamptonToday Wolverhampton_Today @WolvesCouncil gov.uk gov.uk 01902 551155 WCC 1875 05/2019 wolverhampton. andIntervention #Prevention 2018 -2022 Strategy Prevention Homelessness Chapter title gov.uk Contents Foreword Foreword 3 Introduction 4 Development of the strategy 6 Defining Homelessness 6 National Context 7 Homelessness Data 8 Homelessness Prevention and Relief 9 UK Government Priorities 10 West Midlands Combined Authority 11 Local Context 12 Since the publication of our last Homelessness Strategy, we have seen dramatic changes to the Demographic Data 13 environment in which homelessness services are delivered. Changes resulting from the economic downturn, and in particular welfare reform, are impacting Under One Roof 13 detrimentally on many low- income groups and those susceptible to homelessness. Well documented Strategic Context 15 funding cuts to Councils are coupled with falls in support and funding streams to other statutory agencies, and those in the voluntary and community sector. Homelessness Strategy 2018-2022 16 As a result, this new strategy is being developed in a context of shrinking resources and increasing demand for services. There is also considerable uncertainty over the future. Homelessness prevention 16 These factors weigh heavily on the determination of what can realistically be achieved in the years Rough Sleepers 18 ahead. Nevertheless, the challenge and our aspiration remains to prevent homelessness wherever possible in line with the new Homelessness Reduction Act. Vulnerability and Health 19 The response to this challenge will be based on the same core principle as that which underpinned Vulnerabilities 20 our previous strategies effective partnership working. -

Staffordshire County Council 5 Solihull Metropolitan Borough Council 1 Sandwell 1 Wolverhampton City Council 1 Stoke on Trent Ci

Staffordshire County Council 5 Solihull Metropolitan Borough Council 1 Sandwell 1 Wolverhampton City Council 1 Stoke on Trent City Council 1 Derby City Council 3 Nottinghamshire County Council 2 Education Otherwise 2 Shropshire County Council 1 Hull City Council 1 Warwickshire County Council 3 WMCESTC 1 Birmingham City Council 1 Herefordshire County Council 1 Worcestershire Childrens Services 1 Essex County Council 1 Cheshire County Council 2 Bedfordshire County Council 1 Hampshire County Council 1 Telford and Wrekin Council 1 Leicestershire County Council 1 Education Everywhere 1 Derbyshire County Council 1 Jun-08 Cheshire County Council 3 Derby City Travellers Education Team 2 Derbyshire LA 1 Education Everywhere 1 Staffordshire County Council 6 Essex County Council 1 Gloustershire County Council 1 Lancashire Education Inclusion Service 1 Leicestershire County Council 1 Nottingham City 1 Oxford Open Learning Trust 1 Shropshire County Council 1 Solihull Council 2 Stoke on Trent LA 1 Telford and Wrekin Authority 2 Warwickshire County Council 4 West Midlands Consortium Education Service 1 West Midlands Regional Partnership 1 Wolverhampton LA 1 Nov-08 Birmingham City Council 2 Cheshire County Council 3 Childline West Midlands 1 Derby City LA 2 Derby City Travellers Education Team 1 Dudley LA 1 Education At Home 1 Education Everywhere 1 Education Otherwise 2 Essex County Council 1 Gloucestershire County Council 2 Lancashire Education Inclusion Service 1 Leicestershire County Council 1 Nottinghamshire LA 2 SERCO 1 Shropshire County Council -

The Tort Liability of American Municipalities*

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by University of Kentucky Kentucky Law Journal Volume 40 | Issue 2 Article 1 1951 The orT t Liability of American Municipalities Chester James Antieau Washburn University Follow this and additional works at: https://uknowledge.uky.edu/klj Part of the State and Local Government Law Commons, and the Torts Commons Right click to open a feedback form in a new tab to let us know how this document benefits you. Recommended Citation Antieau, Chester James (1951) "The orT t Liability of American Municipalities," Kentucky Law Journal: Vol. 40 : Iss. 2 , Article 1. Available at: https://uknowledge.uky.edu/klj/vol40/iss2/1 This Article is brought to you for free and open access by the Law Journals at UKnowledge. It has been accepted for inclusion in Kentucky Law Journal by an authorized editor of UKnowledge. For more information, please contact [email protected]. THE TORT LIABILITY OF AMERICAN MUNICIPALITIES* By CHESTER JAMES ANTIEAUT * For torts committed in the performance of activities ultra vires the municipal corporation, the city is customarily immune from liability.1 The great majority of courts further deny municipal liability when negligent torts are committed beyond the author ized powers of particular agents, but infra vires the municipal corporation,2 although there are well-reasoned cases contra. 3 Al- though cities are occasionally held responsible for the wilful torts of employees, 4 the majority rule is contrary - Municipalities have by adoption or ratification been held liable for torts of agents un- authorized but within the power of the municipal corporation.6 Municipalities are regularly not liable for torts when the actor is an independent contractor. -

Birmingham City Council (Appellants) V Ali (FC) and Others (FC) (Respondents) Moran (FC) (Appellant) V Manchester City Council (Respondents)

HOUSE OF LORDS SESSION 2008–09 [2009] UKHL 36 on appeal from: [2008]EWCA Civ 1228 [2008]EWCA Civ 378 OPINIONS OF THE LORDS OF APPEAL FOR JUDGMENT IN THE CAUSE Birmingham City Council (Appellants) v Ali (FC) and others (FC) (Respondents) Moran (FC) (Appellant) v Manchester City Council (Respondents) Appellate Committee Lord Hope of Craighead Lord Scott of Foscote Lord Walker of Gestingthorpe Baroness Hale of Richmond Lord Neuberger of Abbotsbury Counsel Appellant (Birmingham City Council): Respondent: (Ali): Ashley Underwood QC Jan Luba QC Catherine Rowlands Zia Nabi (Instructed by Birmingham City Council) (Instructed by Community Law Partnership) Appellant: (Moran): Respondent (Manchester City Council): Jan Luba QC Clive Freedman QC Adam Fullwood Zoe Thompson (Instructed by Shelter Greater Manchester Housing (Instructed by Manchester City Council) Centre ) Interveners: Secretary of State for Communities and Interveners: Women’s Aid Federation: Local Government: Stephen Knafler Martin Chamberlain Liz Davies (Instructed by Treasury Solicitors) (Instructed by Sternberg Reed ) Hearing dates: 26 JANUARY, 28 and 29 APRIL 2009 ON WEDNESDAY 1 JULY 2009 HOUSE OF LORDS OPINIONS OF THE LORDS OF APPEAL FOR JUDGMENT IN THE CAUSE Birmingham City Council (Appellants) v Ali (FC) and others (FC) (Respondents) Moran (FC) (Appellant) v Manchester City Council (Respondents) [2009] UKHL 36 LORD HOPE OF CRAIGHEAD My Lords, 1. I have had the privilege of reading in draft the opinion which has been prepared by my noble and learned friend Baroness Hale of Richmond, to which my noble and learned friend Lord Neuberger of Abbotsbury has contributed. I agree with it, and for the reasons they have given I would allow both appeals. -

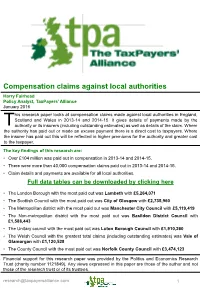

Compensation Claims Against Local Authorities

Compensation claims against local authorities Harry Fairhead Policy Analyst, TaxPayers’ Alliance January 2016 his research paper looks at compensation claims made against local authorities in England, Scotland and Wales in 2013-14 and 2014-15. It gives details of payments made by the T authority or its insurers (including outstanding estimates) as well as details of the claim. Where the authority has paid out or made an excess payment there is a direct cost to taxpayers. Where the insurer has paid out this will be reflected in higher premiums for the authority and greater cost to the taxpayer. The key findings of this research are: • Over £104 million was paid out in compensation in 2013-14 and 2014-15. • There were more than 40,000 compensation claims paid out in 2013-14 and 2014-15. • Claim details and payments are available for all local authorities. Full data tables can be downloaded by clicking here • The London Borough with the most paid out was Lambeth with £5,264,071 • The Scottish Council with the most paid out was City of Glasgow with £2,735,960 • The Metropolitan district with the most paid out was Manchester City Council with £5,119,419 • The Non-metropolitan district with the most paid out was Basildon District Council with £1,588,443 • The Unitary council with the most paid out was Luton Borough Council with £1,910,260 • The Welsh Council with the greatest total claims (including outstanding estimates) was Vale of Glamorgan with £1,120,528 • The County Council with the most paid out was Norfolk County Council with £3,474,123 Financial support for this research paper was provided by the Politics and Economics Research Trust (charity number 1121849). -

Training Requirements to Enable Transport Planners, Engineers and Operators to Respond to the Challenge of Legislative Change

This is a repository copy of Training Requirements to Enable Transport Planners, Engineers and Operators to Respond to the Challenge of Legislative Change. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/2322/ Monograph: Turvey, I.G. (1987) Training Requirements to Enable Transport Planners, Engineers and Operators to Respond to the Challenge of Legislative Change. Working Paper. Institute of Transport Studies, University of Leeds , Leeds, UK. Working Paper 234 Reuse Unless indicated otherwise, fulltext items are protected by copyright with all rights reserved. The copyright exception in section 29 of the Copyright, Designs and Patents Act 1988 allows the making of a single copy solely for the purpose of non-commercial research or private study within the limits of fair dealing. The publisher or other rights-holder may allow further reproduction and re-use of this version - refer to the White Rose Research Online record for this item. Where records identify the publisher as the copyright holder, users can verify any specific terms of use on the publisher’s website. Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. [email protected] https://eprints.whiterose.ac.uk/ White Rose Research Online http://eprints.whiterose.ac.uk/ Institute of Transport Studies University of Leeds This is an ITS Working Paper produced and published by the University of Leeds. ITS Working Papers are intended to provide information and encourage discussion on a topic in advance of formal publication. -

GB 0740 Goodchild

GB 0740 Goodchild Wakefield Libraries and Information Services, Local Studies This catalogue was digitised by The National Archives as part of the National Register of Archives digitisation project NRA 23091 The National Archives ^ m ill' CITY OF WAKEFIELD MD ARCHIVES GOODCRTLD "jJOAlMtg j^j W ALDAM Mf3 GRAND WESTERN CANAL: Report and accounts 1832-33 1839 1843 I845-46 I848-5I Circulars and correspondence I85O-65 Also (loose) : Map of Lines of Canal, notice report 1830 Lines of proposed English & Bristol Channels Ship Canal 1824 Canal Association report: (See W. Aldam ACN MSS. above) EREWASH CANAL: Accounts I885 Notices of Meetings 1883 1884 BRADFORD CANAL: Bradford Canal Co, Reports - Half year ending June 1874 " " " December 1874 Joint Committee Accounts - December I89O November (final) 1923 WILTS AND BERKS CANAL: Reports and accounts 1825 1827-38 1840-42 1845-51 1853-58 1867-72 Subscription List I84O Winding up, case re 1868 Winding up of Company, correspondence and papers re 1875-78 ROCHDALE CANAL: Accounts 1828 Notices of amalgamation meetings I855 ROCHDALE CANAL : (Continued) Accounts 1828 Notices of amalgamation meetings 1855 Notice of dividend warrants I864 1866 1869 1870 1871 (2 copies) 1872 1873 1874 Dividend warrants 1879 (2 copies) 1880 1881 1883 ROADS AND BRIDGES: TINSLEY & DONCASTER ROAD: Acts 1826 I84I Branch to Mexborough, plan I84O Case on Bill I84I Notices of meetings and papers 1853-70 Statements of accounts 1842 1844 1847 I848 I869 BAY/TRY AND TINSLEY ROAD: Acts 1825 I856 Statements of accounts I855-58 BALBY AND WORKSOP ROAD: Act I858 Statements of accounts I85O-58 BARNSDALE AND LEEDS ROAD: Plan of roads between Leeds and Doncaster 1822 Statements of accounts 1831-32 Scale of tolls n*d* Proposal to pay off £500 1859 Opposition to Bill l85 6 JESDS AND LIVERPOOL CANAL Accounts (with some additional notes) 1787 1809-41 I843-44 1847-59 I86I-64 1867-68 1882 Correspondence, reports, newspaper cuttings, etc. -

Mifriendly Cities – Migration Friendly Cities Birmingham, Coventry and Wolverhampton 2017/18-2020/21

MiFriendly Cities – Migration Friendly Cities Birmingham, Coventry and Wolverhampton 2017/18-2020/21 Summary In partnership with Coventry City and Wolverhampton City Councils, Birmingham City Council has been successful in securing EU funding to deliver a three year MiFriendly Cities project. The project, which is backed by West Midlands Combined Authority, will see the three Councils working together to develop new and innovative activity which can help integrate economic migrants, refugees and asylum seekers into the West Midlands. This approach provides an opportunity for Birmingham City Council to explore how it can work with partners and migrants in a way which can help to expand the current range of activity, which mostly focuses on addressing the basic needs and legal rights of migrants. As part of this approach there is a particular focus on changing attitudes to migrants, developing employment pathways, social enterprise and active citizenship. Coventry City Council will be managing the whole project but Birmingham City Council will be required to project manage and coordinate activity which specifically relates to Birmingham, across all the different work packages and activities. Birmingham has also been asked to lead the regional work on “Active Citizenship”. Introduction Following a competitive bidding process “MiFriendly Cities” was chosen by the European Regional Development Fund (ERDF) as one of three projects across Europe which they would like to support. This was from two hundred proposals which were submitted. To support the delivery of the MiFriendly Cities project the EU is providing €4,280,640 over three years to Birmingham, Coventry and Wolverhampton City Councils. This is irrespective of the Brexit process and the UK leaving the EU in 2019. -

City Council Meeting Inquiry of the Co-Ordinating O&S Committee

City Council Meeting Inquiry of the Co-ordinating O&S Committee 1 Purpose 1.1 One of the recommendations in the Review of Scrutiny, agreed by City Council in March 2018, was that an inquiry into the role and purpose of the full City Council meeting was held. The Co- ordinating agreed to undertake this inquiry at its last meeting and to review the arrangements for City Council meetings. 1.2 A draft terms of reference are appended for the Committee to agree (Appendix 1), which have several lines of enquiry: Understand the statutory requirements and responsibilities of full Council and its role in decision-making in the council; Review Standing Orders to ensure they are fit for purpose; Consider whether the agenda items properly reflect the responsibilities of the council at all levels – from regional to local level; Review the operation of the meetings – the timings, the formalities and use of technology – to ensure it is fit for purpose; Explore the role of Council Business Management Committee (CBM) in supporting Council in non-Executive functions; Explore the role City Council plays in local democracy and public engagement. 1.3 This note sets out some background information and key questions for each area. 2 Previous Reviews of the City Council Process 2.1 The note below includes some findings from previous inquiries and from a recent officer review of the processes associated with the City Council meeting. 2.2 In 2005, the Co-ordinating O&S Committee conducted a review of the Role of Members and the Full Council. The report can be found at: https://www.birmingham.gov.uk/downloads/file/507/role_of_members_at_full_council_scrutiny _report_april_2005pdf .