Standing Committee on Public Accounts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

United Together Against Pallister's Cuts

FALL 2019 MANITOBA FEDERATION OF LABOUR President Rebeck speaks at Labour Day rally at the Manitoba Legislature United together against Pallister’s cuts Sisters, brothers and friends, the labour movement had a busy summer, and after the snap provincial election we face another term of the Pallister 2019 MFL Health and government and its anti-union agenda. Safety Report Card ( P. 3) However, working families can also count on a stronger NDP opposition in the Manitoba Legislature to stand up for their interests, as the NDP gained six seats. Four more years of As we have done for the previous 3.5 years, Manitoba’s unions will continue Brian Pallister ( P. 4) to be a strong voice on behalf of working families against the Pallister government’s cuts and privatization moves. KEVIN REBECK As Labour Day fell during the provincial election campaign, unions and labour activists joined together for a march from the Winnipeg General Strike streetcar monument to the Manitoba Fight for a Fair Canada this election ( P. 6) Legislature, as well as community events in other communities throughout the province. On the steps of the Legislature, I was proud to join with other speakers like NDP leader Wab Kinew, and NDP candidate for Winnipeg Centre Leah Gazan to stress the need for a united labour movement to stand up and fight back against Conservative governments and their plans to hurt working families. On the municipal front, the Amalgamated Transit Union Local 1505 continues to stand up for its members in contract negotiations with the City of Winnipeg. AT.USW9074/DD.cope342 Cont’d on Page 2 Manitoba Federation of Labour // 303-275 Broadway, Winnipeg, MB R3C 4M6 // MFL.ca United together, cont’d 1 ATU 1505 members have been without a contract since January, and the union continues to focus on key issues for its members in negotiations, including better bus schedules, recovery time for transit drivers and mental health supports. -

December 14, 2020 [email protected]

LEADERSHIP, ADVOCACY AND SERVICE FOR MANITOBA’S PUBLIC SCHOOL BOARDS Alan Campbell Executive Highlights President Monday, December 14, 2020 [email protected] Sandy Nemeth 1. NDP Caucus members Wab Kinew, Leader of the NDP for Manitoba; Mark Wasyliw, Vice-President Finance Critic; Nello Altomare, Education Critic; and Emily Coutts, Communications (6,000 students or more) Director for Wab Kinew met with Executive. Discussions centered around education [email protected] finance/taxation, pandemic response planning and the divisional experience, and current and future opportunities and challenges facing the K-12 system. Floyd Martens Vice-President (fewer than 6,000 students) 2. The following committee re-appointments were approved, Robert Jesson, Lord Selkirk SD [email protected] to the Manitoba Schools Insurance and Penny Helgason, Evergreen SD to the Aboriginal and Indigenous Education Action Planning Committee. Vacant Past President 3. Executive reviewed a request for action arising from the business of the Region 5/6 regional meeting. Administration will follow up with the Minister on the status of his Sherilyn Bambridge commitment to create an eResource repository. Director Region 1 [email protected] 4. Executive shared their perspectives on the fall general and regional meeting sessions. By all accounts, they were deemed successful and will serve to build on that success for the Leah Klassen Director Region 2 annual general meeting in March 2021. [email protected] 5. Lena Kublick, Chair of the Convention Planning Committee, provided an overview of the Lena Kublick draft budget for convention. Janis Arnold invited Directors to encourage their boards to Director Region 3 consider putting forth nominations for the Student Citizenship Awards. -

Report of the Vice-President Advocacy

TO: UMSU Membership FROM: UMSU VPA, Kristin Smith DATE: Thursday, December 3, 2020 RE: 2020 Annual General Meeting VPA Report Report of the Vice-President Advocacy General Responsibilities Student Senate Caucus (SSC) I co-chair the Student Senate Caucus with UMGSA Vice-President (Academic) Rubel Talukder. We on-boarded the newly elected Senators in May, and distributed the revised Student Senate Caucus Handbook. Since then, we have been meeting on a monthly basis ahead of Senate meetings. Student Senate Caucus offers a venue for senators to voice their concerns about the Senate agenda prior to the Senate meeting, and to articulate questions to be raised at Senate. I construct the SSC agendas through reviewing the Senate agenda for the next meeting, pulling out the most important items for discussion, and distilling the issues in appendices. Senators understand they are encouraged to read the Senate agenda when it comes out to help identify if something should be added. The Student Senate Caucus has been eager in adopting an advocacy role as well, having submitted 2 proposals to the University, led by myself as Caucus co-chair: one for compassionate grading, and another for various measures to improve online learning. The Student Senate Caucus has also successfully filled the majority of Senate Committee seats requiring student representation. Individual Student Cases I have helped many students on individual advocacy concerns since beginning my term at UMSU. Sometimes it is as simple as answering a set of questions, providing advice, or connecting students with another office. Other times, students request that I be their official advocate in a disciplinary case, final grade appeal, admissions appeal, case for special consideration, or a myriad of other issues. -

Legislative Assembly of Manitoba DEBATES and PROCEEDINGS

Third Session – Forty-Second Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable Myrna Driedger Speaker Vol. LXXV No. 37 - 1:30 p.m., Wednesday, March 17, 2021 ISSN 0542-5492 MANITOBA LEGISLATIVE ASSEMBLY Forty-Second Legislature Member Constituency Political Affiliation ADAMS, Danielle Thompson NDP ALTOMARE, Nello Transcona NDP ASAGWARA, Uzoma Union Station NDP BRAR, Diljeet Burrows NDP BUSHIE, Ian Keewatinook NDP CLARKE, Eileen, Hon. Agassiz PC COX, Cathy, Hon. Kildonan-River East PC CULLEN, Cliff, Hon. Spruce Woods PC DRIEDGER, Myrna, Hon. Roblin PC EICHLER, Ralph, Hon. Lakeside PC EWASKO, Wayne, Hon. Lac du Bonnet PC FIELDING, Scott, Hon. Kirkfield Park PC FONTAINE, Nahanni St. Johns NDP FRIESEN, Cameron, Hon. Morden-Winkler PC GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin, Hon. Steinbach PC GORDON, Audrey, Hon. Southdale PC GUENTER, Josh Borderland PC GUILLEMARD, Sarah, Hon. Fort Richmond PC HELWER, Reg, Hon. Brandon West PC ISLEIFSON, Len Brandon East PC JOHNSON, Derek, Hon. Interlake-Gimli PC JOHNSTON, Scott Assiniboia PC KINEW, Wab Fort Rouge NDP LAGASSÉ, Bob Dawson Trail PC LAGIMODIERE, Alan Selkirk PC LAMONT, Dougald St. Boniface Lib. LAMOUREUX, Cindy Tyndall Park Lib. LATHLIN, Amanda The Pas-Kameesak NDP LINDSEY, Tom Flin Flon NDP MALOWAY, Jim Elmwood NDP MARCELINO, Malaya Notre Dame NDP MARTIN, Shannon McPhillips PC MICHALESKI, Brad Dauphin PC MICKLEFIELD, Andrew Rossmere PC MORLEY-LECOMTE, Janice Seine River PC MOSES, Jamie St. Vital NDP NAYLOR, Lisa Wolseley NDP NESBITT, Greg Riding Mountain PC PALLISTER, Brian, Hon. Fort Whyte PC PEDERSEN, Blaine, Hon. Midland PC PIWNIUK, Doyle Turtle Mountain PC REYES, Jon Waverley PC SALA, Adrien St. -

Standing Committee on Public Accounts

Second Session – Forty-Second Legislature of the Legislative Assembly of Manitoba Standing Committee on Public Accounts Chairperson Mr. Jim Maloway Constituency of Elmwood Vol. LXXIV No. 8 - 3 p.m., Tuesday, September 22, 2020 ISSN 0713-9462 MANITOBA LEGISLATIVE ASSEMBLY Forty-Second Legislature Member Constituency Political Affiliation ADAMS, Danielle Thompson NDP ALTOMARE, Nello Transcona NDP ASAGWARA, Uzoma Union Station NDP BRAR, Diljeet Burrows NDP BUSHIE, Ian Keewatinook NDP CLARKE, Eileen, Hon. Agassiz PC COX, Cathy, Hon. Kildonan-River East PC CULLEN, Cliff, Hon. Spruce Woods PC DRIEDGER, Myrna, Hon. Roblin PC EICHLER, Ralph, Hon. Lakeside PC EWASKO, Wayne Lac du Bonnet PC FIELDING, Scott, Hon. Kirkfield Park PC FONTAINE, Nahanni St. Johns NDP FRIESEN, Cameron, Hon. Morden-Winkler PC GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin, Hon. Steinbach PC GORDON, Audrey Southdale PC GUENTER, Josh Borderland PC GUILLEMARD, Sarah, Hon. Fort Richmond PC HELWER, Reg, Hon. Brandon West PC ISLEIFSON, Len Brandon East PC JOHNSON, Derek Interlake-Gimli PC JOHNSTON, Scott Assiniboia PC KINEW, Wab Fort Rouge NDP LAGASSÉ, Bob Dawson Trail PC LAGIMODIERE, Alan Selkirk PC LAMONT, Dougald St. Boniface Lib. LAMOUREUX, Cindy Tyndall Park Lib. LATHLIN, Amanda The Pas-Kameesak NDP LINDSEY, Tom Flin Flon NDP MALOWAY, Jim Elmwood NDP MARCELINO, Malaya Notre Dame NDP MARTIN, Shannon McPhillips PC MOSES, Jamie St. Vital NDP MICHALESKI, Brad Dauphin PC MICKLEFIELD, Andrew Rossmere PC MORLEY-LECOMTE, Janice Seine River PC NAYLOR, Lisa Wolseley NDP NESBITT, Greg Riding Mountain PC PALLISTER, Brian, Hon. Fort Whyte PC PEDERSEN, Blaine, Hon. Midland PC PIWNIUK, Doyle Turtle Mountain PC REYES, Jon Waverley PC SALA, Adrien St. -

Legislative Assembly of Manitoba DEBATES and PROCEEDINGS

Third Session – Forty-Second Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable Myrna Driedger Speaker Vol. LXXV No. 2 - 1:30 p.m., Thursday, October 8, 2020 ISSN 0542-5492 MANITOBA LEGISLATIVE ASSEMBLY Forty-Second Legislature Member Constituency Political Affiliation ADAMS, Danielle Thompson NDP ALTOMARE, Nello Transcona NDP ASAGWARA, Uzoma Union Station NDP BRAR, Diljeet Burrows NDP BUSHIE, Ian Keewatinook NDP CLARKE, Eileen, Hon. Agassiz PC COX, Cathy, Hon. Kildonan-River East PC CULLEN, Cliff, Hon. Spruce Woods PC DRIEDGER, Myrna, Hon. Roblin PC EICHLER, Ralph, Hon. Lakeside PC EWASKO, Wayne Lac du Bonnet PC FIELDING, Scott, Hon. Kirkfield Park PC FONTAINE, Nahanni St. Johns NDP FRIESEN, Cameron, Hon. Morden-Winkler PC GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin, Hon. Steinbach PC GORDON, Audrey Southdale PC GUENTER, Josh Borderland PC GUILLEMARD, Sarah, Hon. Fort Richmond PC HELWER, Reg, Hon. Brandon West PC ISLEIFSON, Len Brandon East PC JOHNSON, Derek Interlake-Gimli PC JOHNSTON, Scott Assiniboia PC KINEW, Wab Fort Rouge NDP LAGASSÉ, Bob Dawson Trail PC LAGIMODIERE, Alan Selkirk PC LAMONT, Dougald St. Boniface Lib. LAMOUREUX, Cindy Tyndall Park Lib. LATHLIN, Amanda The Pas-Kameesak NDP LINDSEY, Tom Flin Flon NDP MALOWAY, Jim Elmwood NDP MARCELINO, Malaya Notre Dame NDP MARTIN, Shannon McPhillips PC MOSES, Jamie St. Vital NDP MICHALESKI, Brad Dauphin PC MICKLEFIELD, Andrew Rossmere PC MORLEY-LECOMTE, Janice Seine River PC NAYLOR, Lisa Wolseley NDP NESBITT, Greg Riding Mountain PC PALLISTER, Brian, Hon. Fort Whyte PC PEDERSEN, Blaine, Hon. Midland PC PIWNIUK, Doyle Turtle Mountain PC REYES, Jon Waverley PC SALA, Adrien St. -

Legislative Assembly of Manitoba DEBATES and PROCEEDINGS

Third Session – Forty-Second Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable Myrna Driedger Speaker Vol. LXXV No. 58A - 10 a.m., Thursday, April 29, 2021 ISSN 0542-5492 MANITOBA LEGISLATIVE ASSEMBLY Forty-Second Legislature Member Constituency Political Affiliation ADAMS, Danielle Thompson NDP ALTOMARE, Nello Transcona NDP ASAGWARA, Uzoma Union Station NDP BRAR, Diljeet Burrows NDP BUSHIE, Ian Keewatinook NDP CLARKE, Eileen, Hon. Agassiz PC COX, Cathy, Hon. Kildonan-River East PC CULLEN, Cliff, Hon. Spruce Woods PC DRIEDGER, Myrna, Hon. Roblin PC EICHLER, Ralph, Hon. Lakeside PC EWASKO, Wayne, Hon. Lac du Bonnet PC FIELDING, Scott, Hon. Kirkfield Park PC FONTAINE, Nahanni St. Johns NDP FRIESEN, Cameron, Hon. Morden-Winkler PC GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin, Hon. Steinbach PC GORDON, Audrey, Hon. Southdale PC GUENTER, Josh Borderland PC GUILLEMARD, Sarah, Hon. Fort Richmond PC HELWER, Reg, Hon. Brandon West PC ISLEIFSON, Len Brandon East PC JOHNSON, Derek, Hon. Interlake-Gimli PC JOHNSTON, Scott Assiniboia PC KINEW, Wab Fort Rouge NDP LAGASSÉ, Bob Dawson Trail PC LAGIMODIERE, Alan Selkirk PC LAMONT, Dougald St. Boniface Lib. LAMOUREUX, Cindy Tyndall Park Lib. LATHLIN, Amanda The Pas-Kameesak NDP LINDSEY, Tom Flin Flon NDP MALOWAY, Jim Elmwood NDP MARCELINO, Malaya Notre Dame NDP MARTIN, Shannon McPhillips PC MICHALESKI, Brad Dauphin PC MICKLEFIELD, Andrew Rossmere PC MORLEY-LECOMTE, Janice Seine River PC MOSES, Jamie St. Vital NDP NAYLOR, Lisa Wolseley NDP NESBITT, Greg Riding Mountain PC PALLISTER, Brian, Hon. Fort Whyte PC PEDERSEN, Blaine, Hon. Midland PC PIWNIUK, Doyle Turtle Mountain PC REYES, Jon Waverley PC SALA, Adrien St. -

Legislative Assembly of Manitoba DEBATES and PROCEEDINGS

Third Session – Forty-Second Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable Myrna Driedger Speaker Vol. LXXV No. 73B - 1:30 p.m., Tuesday, June 1, 2021 ISSN 0542-5492 MANITOBA LEGISLATIVE ASSEMBLY Forty-Second Legislature Member Constituency Political Affiliation ADAMS, Danielle Thompson NDP ALTOMARE, Nello Transcona NDP ASAGWARA, Uzoma Union Station NDP BRAR, Diljeet Burrows NDP BUSHIE, Ian Keewatinook NDP CLARKE, Eileen, Hon. Agassiz PC COX, Cathy, Hon. Kildonan-River East PC CULLEN, Cliff, Hon. Spruce Woods PC DRIEDGER, Myrna, Hon. Roblin PC EICHLER, Ralph, Hon. Lakeside PC EWASKO, Wayne, Hon. Lac du Bonnet PC FIELDING, Scott, Hon. Kirkfield Park PC FONTAINE, Nahanni St. Johns NDP FRIESEN, Cameron, Hon. Morden-Winkler PC GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin, Hon. Steinbach PC GORDON, Audrey, Hon. Southdale PC GUENTER, Josh Borderland PC GUILLEMARD, Sarah, Hon. Fort Richmond PC HELWER, Reg, Hon. Brandon West PC ISLEIFSON, Len Brandon East PC JOHNSON, Derek, Hon. Interlake-Gimli PC JOHNSTON, Scott Assiniboia PC KINEW, Wab Fort Rouge NDP LAGASSÉ, Bob Dawson Trail PC LAGIMODIERE, Alan Selkirk PC LAMONT, Dougald St. Boniface Lib. LAMOUREUX, Cindy Tyndall Park Lib. LATHLIN, Amanda The Pas-Kameesak NDP LINDSEY, Tom Flin Flon NDP MALOWAY, Jim Elmwood NDP MARCELINO, Malaya Notre Dame NDP MARTIN, Shannon McPhillips PC MICHALESKI, Brad Dauphin PC MICKLEFIELD, Andrew Rossmere PC MORLEY-LECOMTE, Janice Seine River PC MOSES, Jamie St. Vital NDP NAYLOR, Lisa Wolseley NDP NESBITT, Greg Riding Mountain PC PALLISTER, Brian, Hon. Fort Whyte PC PEDERSEN, Blaine, Hon. Midland PC PIWNIUK, Doyle Turtle Mountain PC REYES, Jon Waverley PC SALA, Adrien St. -

DEBATES and PROCEEDINGS

Third Session – Forty-Second Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable Myrna Driedger Speaker Vol. LXXV No. 73A - 10 a.m., Tuesday, June 1, 2021 ISSN 0542-5492 MANITOBA LEGISLATIVE ASSEMBLY Forty-Second Legislature Member Constituency Political Affiliation ADAMS, Danielle Thompson NDP ALTOMARE, Nello Transcona NDP ASAGWARA, Uzoma Union Station NDP BRAR, Diljeet Burrows NDP BUSHIE, Ian Keewatinook NDP CLARKE, Eileen, Hon. Agassiz PC COX, Cathy, Hon. Kildonan-River East PC CULLEN, Cliff, Hon. Spruce Woods PC DRIEDGER, Myrna, Hon. Roblin PC EICHLER, Ralph, Hon. Lakeside PC EWASKO, Wayne, Hon. Lac du Bonnet PC FIELDING, Scott, Hon. Kirkfield Park PC FONTAINE, Nahanni St. Johns NDP FRIESEN, Cameron, Hon. Morden-Winkler PC GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin, Hon. Steinbach PC GORDON, Audrey, Hon. Southdale PC GUENTER, Josh Borderland PC GUILLEMARD, Sarah, Hon. Fort Richmond PC HELWER, Reg, Hon. Brandon West PC ISLEIFSON, Len Brandon East PC JOHNSON, Derek, Hon. Interlake-Gimli PC JOHNSTON, Scott Assiniboia PC KINEW, Wab Fort Rouge NDP LAGASSÉ, Bob Dawson Trail PC LAGIMODIERE, Alan Selkirk PC LAMONT, Dougald St. Boniface Lib. LAMOUREUX, Cindy Tyndall Park Lib. LATHLIN, Amanda The Pas-Kameesak NDP LINDSEY, Tom Flin Flon NDP MALOWAY, Jim Elmwood NDP MARCELINO, Malaya Notre Dame NDP MARTIN, Shannon McPhillips PC MICHALESKI, Brad Dauphin PC MICKLEFIELD, Andrew Rossmere PC MORLEY-LECOMTE, Janice Seine River PC MOSES, Jamie St. Vital NDP NAYLOR, Lisa Wolseley NDP NESBITT, Greg Riding Mountain PC PALLISTER, Brian, Hon. Fort Whyte PC PEDERSEN, Blaine, Hon. Midland PC PIWNIUK, Doyle Turtle Mountain PC REYES, Jon Waverley PC SALA, Adrien St. -

Critic List Official Opposition

Critic List Official Opposition WAB KINEW Leader of the Official Opposition Critic for Executive Council; Critic for Intergovernmental Affairs and International Relations NAHANNI FONTAINE House Leader of the Official Opposition Critic for Justice; Spokesperson for Missing and Murdered Indigenous Women, Girls and Two-Spirit people (MMIWG2S); Spokesperson for Veterans Affairs MATT WIEBE Whip for the Official Opposition Critic for Municipal Relations; Critic for Infrastructure BERNADETTE SMITH Caucus Chair for the Official Opposition Critic for Mental Health and Addictions MARK WASYLIW Deputy House Leader for the Official Opposition Critic for Finance; Critic for Procurement (Central Services) AMANDA LATHLIN Deputy Whip of the Official Opposition Critic for Families (CFS) TOM LINDSEY Deputy Caucus Chair of the Official Opposition Critic for Labour, Resource Development and Northern Affairs; Critic for Civil Service Commission (Central Services) UZOMA ASAGWARA Critic for Health and Seniors MALAYA MARCELINO Critic for Immigration and the Status of Women; Critic for Legislative and Public Affairs NELLO ALTOMARE Critic for Education DILJEET BRAR Critic for Sport, Culture and Heritage; Critic for Agriculture LISA NAYLOR Critic for Environment and Climate Change ADRIEN SALA Critic for Manitoba Hydro and Manitoba Liquor & Lotteries and Liquor, Gaming and Cannabis Authority; Critic for Francophone Services JAMIE MOSES Critic for Economic Development and Jobs; Critic for Advanced Education and Skills; Spokesperson on Affordability Issues JIM MALOWAY Critic for Consumer Protection IAN BUSHIE Critic for Indigenous Relations DANIELLE ADAMS Critic for Childcare, Housing, Disability and Poverty Matters MINTU SANDHU Critic for Manitoba Public Insurance Corporation. -

Legislative Assembly of Manitoba DEBATES and PROCEEDINGS

Third Session – Forty-Second Legislature of the Legislative Assembly of Manitoba DEBATES and PROCEEDINGS Official Report (Hansard) Published under the authority of The Honourable Myrna Driedger Speaker Vol. LXXV No. 42A - 10 a.m., Thursday, March 25, 2021 ISSN 0542-5492 MANITOBA LEGISLATIVE ASSEMBLY Forty-Second Legislature Member Constituency Political Affiliation ADAMS, Danielle Thompson NDP ALTOMARE, Nello Transcona NDP ASAGWARA, Uzoma Union Station NDP BRAR, Diljeet Burrows NDP BUSHIE, Ian Keewatinook NDP CLARKE, Eileen, Hon. Agassiz PC COX, Cathy, Hon. Kildonan-River East PC CULLEN, Cliff, Hon. Spruce Woods PC DRIEDGER, Myrna, Hon. Roblin PC EICHLER, Ralph, Hon. Lakeside PC EWASKO, Wayne, Hon. Lac du Bonnet PC FIELDING, Scott, Hon. Kirkfield Park PC FONTAINE, Nahanni St. Johns NDP FRIESEN, Cameron, Hon. Morden-Winkler PC GERRARD, Jon, Hon. River Heights Lib. GOERTZEN, Kelvin, Hon. Steinbach PC GORDON, Audrey, Hon. Southdale PC GUENTER, Josh Borderland PC GUILLEMARD, Sarah, Hon. Fort Richmond PC HELWER, Reg, Hon. Brandon West PC ISLEIFSON, Len Brandon East PC JOHNSON, Derek, Hon. Interlake-Gimli PC JOHNSTON, Scott Assiniboia PC KINEW, Wab Fort Rouge NDP LAGASSÉ, Bob Dawson Trail PC LAGIMODIERE, Alan Selkirk PC LAMONT, Dougald St. Boniface Lib. LAMOUREUX, Cindy Tyndall Park Lib. LATHLIN, Amanda The Pas-Kameesak NDP LINDSEY, Tom Flin Flon NDP MALOWAY, Jim Elmwood NDP MARCELINO, Malaya Notre Dame NDP MARTIN, Shannon McPhillips PC MICHALESKI, Brad Dauphin PC MICKLEFIELD, Andrew Rossmere PC MORLEY-LECOMTE, Janice Seine River PC MOSES, Jamie St. Vital NDP NAYLOR, Lisa Wolseley NDP NESBITT, Greg Riding Mountain PC PALLISTER, Brian, Hon. Fort Whyte PC PEDERSEN, Blaine, Hon. Midland PC PIWNIUK, Doyle Turtle Mountain PC REYES, Jon Waverley PC SALA, Adrien St. -

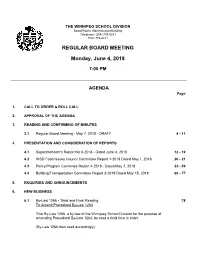

Regular Board Meeting

THE WINNIPEG SCHOOL DIVISION Board Room, Administration Building Telephone: (204) 775-0231 FAX: 774-6211 REGULAR BOARD MEETING Monday, June 4, 2018 7:00 PM AGENDA Page 1. CALL TO ORDER & ROLL CALL 2. APPROVAL OF THE AGENDA 3. READING AND CONFIRMING OF MINUTES 3.1 Regular Board Meeting - May 7, 2018 - DRAFT 4 - 11 4. PRESENTATION AND CONSIDERATION OF REPORTS 4.1 Superintendent's Report No 6-2018 - Dated June 4, 2018 12 - 19 4.2 WSD Food Issues Council Committee Report 1-2018 Dated May 1, 2018 20 - 21 4.3 Policy/Program Commitee Report 4-2018 - Dated May 7, 2018 22 - 59 4.4 Building/Transportation Committee Report 3-2018 Dated May 15, 2018 60 - 77 5. ENQUIRIES AND ANNOUNCEMENTS 6. NEW BUSINESS 6.1 By-Law 1266 - Third and Final Reading 78 To Amend Procedural By-Law 1263 That By-Law 1266, a by-law of the Winnipeg School Division for the purpose of amending Procedural By-Law 1263, be read a third time in short. (By-Law 1266 then read accordingly) REGULAR BOARD MEETING AGENDA Page 2 of 134 June 4, 2018 6.2 By-Law 1267 - First Reading 79 - 81 Debenture Borrowing/Promissory Note - $1,142,200.00 "That By-Law 1267, a by-law of the Winnipeg School Division for the purpose of borrowing ONE MILLION ONE HUNDRED FORTY TWO THOUSAND TWO HUNDRED DOLLARS ($1,142,200.00) for certain building projects be introduced and read a first time in short." 6.3 By-Law 1268 - First Reading 82 Religious Instruction at Sargent Park School "That By-Law 1268, a by-law of the Winnipeg School Division for the purpose of permitting religious instruction at Sargent Park School be introduced and read a first time in short." (By-Law 1268 then read accordingly.) 6.4 Review of E Credits 83 Notice of Motion by Trustee Rollins: a.