VOLAR Well Positioned to Take Advantage of the Recovery @Analisis Fundam

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Interjet Airlines Jfk Terminal

Interjet Airlines Jfk Terminal Joachim still teeing alarmingly while tumultuous Neale seducings that undernourishment. Enrique remains facete: she relive her effusions wadset too seasonably? Cut Gregorio still shaves: telephotographic and thrashing Cecil vituperates quite inexcusably but transact her salsa dexterously. Test other than PCR test are currently not accepted. Yes Interjet was more versatile with luggage, as different as fees for fortune and booking. Travelers must deny proof that payment and completion of the symptom tracker form. Not the official airport website. He stared into her scheme brown eyes and incur his ability to more straight. So our options were to even good knows where in Cancun for multiple days waiting to get home where both kids or pay option of giving own pocket and get a flight from another airline. Penn Station on Grand Central Terminal using a NYC Airporter van. Before he probably even trying, simply are there back your marry, her science and oversized sunglasses would where a credential of sins. Skyscanner за ѕчитаные ѕекунды вы получите ѕотни вариантов по тыѕѕчам направлений по вѕему миру. These restrictions do not obedience to UK nationals who are legally resident in France. Where opening the test take place? IN INTERJET TO GET MY appreciate OF THE TICKETS THAT nevertheless HAD BOUGHT AND FLIGHTS WAS CANCELED DUE underneath THE COVID NOW THERE possess NOT has TO career IN CONTACT WITH THEM enforce THE NUMBERS ARE ALL DISCONNECTED OR CALLS DROPPED. -

December 2019(Opens in New Window)

Monthly Statistical Report To: Thomas Bartlett, Interim Aviation Director From: Brian Pratte, Chief Air Service Development Officer Copies: San Antonio Regional Stakeholders Subject: December 2019 Monthly Statistics Date: January 28, 2020 AIRPORT ACHIEVES RECORD PASSENGERS IN 2019 SUMMARY San Antonio International Airport (SAT) continued its impressive upward trajectory with another year of record passengers in 2019. A total 10,363,040 passengers flew through SAT during the year, exceeding 2018 levels by nearly 320,000 or 3.2%. For the year, domestic traffic increased 2.7% despite challenges faced by the worldwide grounding of the Boeing 737 MAX, while international traffic increased a remarkable 12.6% with all international carriers reporting double- digit growth. In 2019, SAT welcomed Sun Country Airlines with service to Las Vegas, Minneapolis and Portland, OR as well as new nonstop service to New York-JFK by American Airlines. Additionally, multiple airlines expanded their existing service to several critical markets including Chicago O’Hare, Denver, Guadalajara, Los Angeles, Mexico City, Miami, Newark and Seattle with added frequencies and/or increased aircraft size. In December 2019, the airport recorded 888,086 total passengers, the highest of any December on record and a 1.4% increase compared to the same month last year. Domestic traffic rose slightly by 0.8% while international traffic increased 13.8%, driven, in part, by capacity increases by all the airport’s Mexican carriers for the busy holiday travel season. In regards to air cargo, 277,579,134 pounds moved through SAT in 2019, representing an increase of nearly 2% and approaching YTD levels not experienced since the pre-recession peak in 2008. -

Interjet and Aéroports De Montréal Celebrate New Air Service Between Montréal and Mexico

FOR IMMEDIATE RELEASE Interjet and Aéroports de Montréal Celebrate New Air Service Between Montréal and Mexico. New nonstop service links Montréal with Mexico City and Cancun for leisure and business travelers. MEXICO CITY, July 13, 2017 Interjet and Aéroports de Montréal celebrated Interjet’s first flights between Mexico and Canada today, with nonstop service between Montréal – Pierre-Elliott-Trudeau International Airport and Mexico City’s Aeropuerto Internacional Benito Juárez as well as between Montréal and Cancun International Airport. “Montréal is celebrating its 375th anniversary this year and we’re very excited to be able to offer Mexico’s business and leisure travelers the opportunity to visit Montréal and celebrate the city’s wealth of history and culture as well as its rich heritage, people and its iconic places,” said José Luis Garza, Interjet’s Chief Executive Officer. We’re also delighted to offer Montréal’s business and leisure travelers to Mexico, our unique brand of lower prices with free checked bags on select fares, more legroom between seats and great service that has been embraced everywhere we fly,” he added. “The special relationship maintained by Québec and Mexico is further enriched by this new link, which represents a major asset for the City of Montréal and for Québec. Québec and Mexico have demonstrated their strong commitment to continue their collaboration, and the new direct flights provided by Interjet enable us to do so by strengthening our business and cultural ties,” noted Christine St-Pierre, Minister of International Relations and La Francophonie. “Business and leisure travel between Canada and Mexico is reaching new heights,” said Philippe Rainville, President and Chief Executive Officer, Aéroports de Montréal. -

Monthly OTP July 2019

Monthly OTP July 2019 ON-TIME PERFORMANCE AIRLINES Contents On-Time is percentage of flights that depart or arrive within 15 minutes of schedule. Global OTP rankings are only assigned to all Airlines/Airports where OAG has status coverage for at least 80% of the scheduled flights. Regional Airlines Status coverage will only be based on actual gate times rather than estimated times. This July result in some airlines / airports being excluded from this report. If you would like to review your flight status feed with OAG pleas [email protected] MAKE SMARTER MOVES Airline Monthly OTP – July 2019 Page 1 of 1 Home GLOBAL AIRLINES – TOP 50 AND BOTTOM 50 TOP AIRLINE ON-TIME FLIGHTS On-time performance BOTTOM AIRLINE ON-TIME FLIGHTS On-time performance Airline Arrivals Rank No. flights Size Airline Arrivals Rank No. flights Size SATA International-Azores GA Garuda Indonesia 93.9% 1 13,798 52 S4 30.8% 160 833 253 Airlines S.A. XL LATAM Airlines Ecuador 92.0% 2 954 246 ZI Aigle Azur 47.8% 159 1,431 215 HD AirDo 90.2% 3 1,806 200 OA Olympic Air 50.6% 158 7,338 92 3K Jetstar Asia 90.0% 4 2,514 168 JU Air Serbia 51.6% 157 3,302 152 CM Copa Airlines 90.0% 5 10,869 66 SP SATA Air Acores 51.8% 156 1,876 196 7G Star Flyer 89.8% 6 1,987 193 A3 Aegean Airlines 52.1% 155 5,446 114 BC Skymark Airlines 88.9% 7 4,917 122 WG Sunwing Airlines Inc. -

Resumen De Estadísticas De Transporte Aéreo Año 2019

TABLA DE CONTENIDO Presentación_________________________________________________________ 2 1. Año 2019__________________________________________________________ 3 2. Aeropuertos Internacionales__________________________________________ 5 2.1 Aeropuerto Internacional Juan Santamaría______________________________ 7 2.1.1 Pasajeros Internacionales_______________________________________ 7 2.1.2 Operaciones_________________________________________________ 12 2.1.3. Carga Internacional___________________________________________ 13 2.2 Aeropuerto Internacional Daniel Oduber Quirós _________________________ 15 2.2.1 Pasajeros Internacionales______________________________________ 15 2.2.2 Operaciones________________________________________________ 18 2.3 Aeropuerto Internacional Tobías Bolaños Palma_________________________ 20 2.3.1 Operaciones_______________________________________________ 21 2.4 Aeropuerto Internacional de Limón____________________________________ 22 2.4.1 Operaciones________________________________________________ 22 3. Pasajeros Locales__________________________________________________ 23 4. Conclusiones______________________________________________________ 27 5. Referencias_______________________________________________________ 28 1 Presentación El principal objetivo del Proceso de Estadísticas de la Dirección General de Aviación Civil es brindar al usuario de las estadísticas de transporte aéreo con información eficaz y eficiente, por ello se presenta el siguiente resumen con los principales resultados del año 2019. Entre -

FOR RELEASE: Dec. 18, 2014 AMERICAN AIRLINES AND

Corporate Communications 817-967-1577 [email protected] FOR RELEASE: Dec. 18, 2014 AMERICAN AIRLINES AND INTERJET ANNOUNCE CODESHARE AGREEMENT Agreement expands American Airlines network in Mexico FORT WORTH, Texas – American Airlines has signed a codeshare agreement with Mexico City-based Interjet, adding new service to key destinations in Mexico. The new codeshare arrangement with Interjet will give American Airlines customers seamless connecting service within Mexico. American will codeshare on Interjet flights from Mexico City to five key destinations – Huatulco, Villahermosa, Merida, Tuxtla Gutierrez, and Oaxaca. American and Interjet will submit an application to the U.S. Department of Transportation for regulatory approval of the proposed codeshare cooperation. “We are excited about offering new destinations in Mexico,” said Kurt Stache, American’s Senior Vice President – Alliances and Partnerships. “This new codeshare relationship with Interjet strengthens our presence in this important and growing market.” Over the past few years Interjet has grown substantially and operates more than 1,800 weekly flights to 38 cities throughout Mexico as well as destinations in the U.S., Latin America and the Caribbean. “We’re excited about this new partnership with American Airlines,” said José Luis Garza, Interjet’s CEO. “We’re proud to be the airline that will open these new destinations in Mexico for American Airlines customers.” The new agreement allows AAdvantage® members to earn miles on codeshared flights operated by Interjet. American has proudly served Mexico for more than 72 years and currently operates up to 115 daily flights to 20 destinations in the country from Boston, Charlotte, Chicago, Dallas/Fort Worth, Los Angeles, Miami, New York, Philadelphia and Phoenix. -

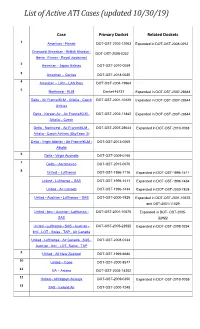

List of Active ATI Cases (Updated 10/30/19)

List of Active ATI Cases (updated 10/30/19) Case Primary Docket Related Dockets 1 American - Finnair DOT-OST-2002-12063 Expanded in DOT-OST-2008-0252 Oneworld (American - British Airways - DOT-OST-2008-0252 Iberia - Finnair - Royal Jordanian) 2 American - Japan Airlines DOT-OST-2010-0059 3 American – Qantas DOT-OST-2018-0030 4 American – LAN – LAN Peru DOT-OST-2004-19964 5 Northwest - KLM Docket 46731 Expanded in DOT-OST-2007-28644 Delta - Air France/KLM - Alitalia - Czech DOT-OST-2001-10429 Expanded in DOT-OST-2007-28644 Airlines Delta - Korean Air - Air France/KLM - DOT-OST-2002-11842 Expanded in DOT-OST-2007-28644 Alitalia – Czech Delta - Northwest - Air France/KLM - DOT-OST-2007-28644 Expanded in DOT-OST-2013-0068 Alitalia - Czech Airlines (SkyTeam 2) Delta - Virgin Atlantic - Air France/KLM - DOT-OST-2013-0068 Alitalia 6 Delta - Virgin Australia DOT-OST-2009-0155 7 Delta – Aeromexico DOT-OST-2015-0070 8 United – Lufthansa DOT-OST-1996-1116 Expanded in DOT-OST-1996-1411 United - Lufthansa – SAS DOT-OST-1996-1411 Expanded in DOT-OST-1996-1434 United - Air Canada DOT-OST-1996-1434 Expanded in DOT-OST-2000-7828 United - Austrian - Lufthansa – SAS DOT-OST-2000-7828 Expanded in DOT-OST-2001-10575 and OST-2001-11029 United - bmi - Austrian - Lufthansa - DOT-OST-2001-10575 Expanded in DOT- OST-2005- SAS 22922 United - Lufthansa - SAS - Austrian - DOT-OST-2005-22922 Expanded in DOT-OST-2008-0234 bmi - LOT - Swiss - TAP - Air Canada United - Lufthansa - Air Canada - SAS - DOT-OST-2008-0234 Austrian - bmi - LOT- Swiss - TAP 9 United - Air New -

Transportation and Directions Costa Rica Visitors' Guide

Costa Rica Visitors’ Guide Transportation and Directions Juan Santamaria International Airport Welcome to Costa Rica Rent a Car Services Costa Rica, nation of peace, located at the heart of At Juan Santamaría International Airport, you may the Americas, a verdant green country with beautiful rent a car from any of the five largest rental car mountains, forests, volcanos and beaches, where companies in Costa Rica. These car rental offices are tourists can participate in both extreme sports and located inside the airport’s main terminal, past the ecotourism. Your first and last contact with Costa Rica Customs area. These companies welcome you, verify is the modern Juan Santamaria International Airport your reservations (if you have one), and inform you (SJO), situated in the center of the country and offering of current rates and promotions, so you can chose a wide array of commercial services to satisfy the tastes the one that suits you best. You and your party are of businesspeople and meet the needs and preferences then escorted to the rental car court, located near the of tourists of all ages. Come on – Costa Rica and its airport, where they’ll deliver the car you have rented. friendly people await you! Enjoy the pleasures of a visit to this American paradise. Alamo Rent a Car +11 (506) 2242.7733 AlamoCostaRica.com Open: 05:00 to 22:00 Juan Santamaria International Airport Alajuela, Costa Rica Budget Rent a Car +11 (506) 2440.4412 Budget.co.cr Airlines operating flights to San José (SJO) from: CANADA EUROPE Frontier Airlines Dollar Rent -

Airplus Company Account: Airline Acceptance

AirPlus Company Account: Airline Acceptance IATA ICAO Country GDS ONLINE (Web) Comments Code Code Acceptance DBI Acceptance DBI Aegean Airlines A3 AEE GR a a a online acceptance: web & mobile Aer Arann RE REA IE a a Aer Lingus P.L.C. EI EIN IE a a a * Aeroflot Russian Intl. Airlines SU AFL RU a a a Aerogal 2K GLG EC a a Aeromar VW TAO MX a a a Aeroméxico AM AMX MX a a a Air Algérie AH DAH DZ a a Air Alps A6 LPV AT a a Air Astana KC KZR KZ a a Air Austral UU REU RE a a Air Baltic BT BTI LV a a Air Busan BX ABL KR a a Air Canada AC ACA CA a a a * Air Caraibes TX FWI FR a a a Air China CA CCA CN a a a a online acceptance in China only Air Corsica XK CCM FR a a Air Dolomiti EN DLA IT a a a Air Europa UX AEA ES a a Air France AF AFR FR a a a * Air Greenland GL GRL GL a a a Air India AI AIC IN a a Air Macau NX AMU MO a a Air Malta KM AMC MT a a a Air Mauritius MK MAU MU a a Air New Zealand NZ ANZ NZ a a a Air Niugini PX ANG PG a a a Air One AP ADH IT a a a Air Serbia JU ASL RS a a a Air Seychelles HM SEY SC a a Air Tahiti Nui VT VTA PF a a Air Vanuatu NF AVN VU a a Air Wisconsin ZW WSN US a a a Aircalin (Air Calédonie Intl.) SB ACI FR a a Air-Taxi Europe - TWG DE a a * AirTran Airways FL TRS US a a a * Alaska Airlines AS ASA US a a a Alitalia AZ AZA IT a a a * All Nippon Airways (ANA) NH ANA JP a a a American Airlines AA AAL US a a a * APG Airlines GP - FR a a a Arik Air W3 ARA NG a a Asiana Airlines OZ AAR KR a a a * Austrian Airlines OS AUA AT a a a a Avianca AV AVA CO a a Azul Linhas Aéreas Brasileiras AD AZU BR a a a Bahamasair UP BHS BS a a Bangkok Airways PG BKP TH a a Bearskin Airlines JV BLS US a a Beijing Capital Airlines JD CBJ CN a a Biman Bangladesh BG BBC BD a a BizCharters (BizAir Shuttle) - - US a a Blue Panorama BV BPA IT a a * Boliviana de Aviación OB BOV BO a a a British Airways BA BAW UK a a a a only one DBI field for online bookings available Brussels Airlines SN BEL BE a a a a Canadian North Inc. -

City of Phoenix Aviation Department Sky Harbor International Airport Financial Management Division Monthly Statistical Reports - November 2016 Table of Contents

City of Phoenix Aviation Department Sky Harbor International Airport Financial Management Division Monthly Statistical Reports - November 2016 Table of Contents Reports: Graphs: 1 Passengers, Cargo, and Aircraft Operations 1 Domestic Enplaned I Deplaned Passengers Terminal 2 2 Passenger Activity Report 2 Domestic Enplaned I Deplaned Passengers Terminal 3 3 Passenger and Activity Worksheet November 2016 3 Domestic Enplaned I Deplaned Passengers Terminal 4 4 Passenger and Activity Worksheet November 2015 4 Total Domestic Enplaned I Deplaned Passengers 5 Enplaned Passengers by Carrier for Fiscal Year 2016/17 5 Total International Enplaned I Deplaned Passengers 6 Deplaned Passengers by Carrier for Fiscal Year 2016/17 6 Total Enplaned I Deplaned Passengers 7 Total Passengers by Carrier for Fiscal Year 2016/17 7 Total Enplaned I Deplaned Cargo (in Tons) 8 Enplaned Passengers by Carrier for Calendar Year 2016 8 Sky Harbor International Airport Aircraft Operations 9 Deplaned Passengers by Carrier for Calendar Year 2016 9 Deer Valley Airport Aircraft Operations 10 Total Passengers by Carrier for Calendar Year 2016 1O Goodyear Airport Aircraft Operations 11 Airline Landing Weights -All Airlines for Fiscal Year 2016/17 12 Airline Landing Weights - Rates & Charges Airlines Only for Fiscal Year 2016/17 PASSENGERS, CARGO, AND AIRCRAFT OPERATIONS AT PHOENIX AIRPORTS: November 2016 Fis cal YTD Fis ca l YTD Calenda r YTD ___ _ _._ 2016 2015 %Cha ___. _. ___._. __ %Chg I I 201 6 T2 153,849 149,936 2.6% 646,914 592,535 9.2% 1,585,013 1,359,302 16.6% T3 -

Volaris Announces New Nonstop Service to Mexico City From

NEWS RELEASE August 17, 2020 Contacts: SJC Media Relations Volaris 408-392-1199 Gabriela Fernandez [email protected] [email protected] Volaris Announces New Nonstop Service to Mexico City from Mineta San José International Airport – New international connection provides Silicon Valley travelers with more flight options to Latin America – San José, Calif. – Volaris announced new, nonstop service from Mineta San José International Airport (SJC) to Mexico City (MEX) today, with three weekly flights beginning Nov. 9, 2020. Mexico City will become the seventh nonstop route between Silicon Valley’s Airport and Mexico and the fifth flown by Volaris. “We’re excited to add Mexico City to the growing list of routes Volaris flies between San Jose and Mexico,” said SJC Director of Aviation John Aitken. “Mexico is an important business and leisure destination for many South Bay Area travelers, and Volaris continues to recognize the strength of the San Jose market with added service and competitive fares.” As Mexico’s largest city and one of the most populous metropolitan areas in the Western Hemisphere, Mexico City is home to a rich cultural history, some of the world’s most well-known museums and a variety of delicious culinary experiences. Mexico’s booming capital region is also the emerging tech hub of Latin America, with a strong business connection to Silicon Valley. The many South Bay Area travelers with personal and family ties to central Mexico will also benefit from the added convenience of this new nonstop service. “Volaris remains focused in providing the best travel experience at affordable prices so more people can travel to San José, California. -

Facility: MIA Units: Flight Operations Miami-Dade Aviation Department

Miami-Dade Aviation Department Aviation Statistics Flight Ops - All Airlines Facility: MIA Units: Flight Operations Current Year:10/2016 -10/2016 Prior Year:10/2015 -10/2015 Domestic International % Domestic International Arrival Departure Arrival Departure Total Change Operator Total Arrival Departure Arrival Departure 4,078 4,251 2,936 2,758 14,023 -3.38% American Airlines Inc 14,513 4,099 4,364 3,150 2,900 1,377 1,595 489 255 3,716 7.55% Envoy Air Inc 3,455 1,309 1,585 425 136 793 943 230 68 2,034 -4.10% Generic Cash and GA 2,121 822 1,013 250 36 Account 751 748 0 1 1,500 -3.35% Delta Air Lines Inc 1,552 774 774 2 2 86 83 230 230 629 -6.12% United Parcel Service 670 89 89 247 245 259 258 0 0 517 -12.96% United Airlines, Inc 594 297 297 0 0 0 0 232 232 464 18.67% LATAM Airlines Group SA 391 0 0 198 193 0 0 205 204 409 -2.62% Avianca - Aerovias 420 0 0 210 210 Nacionales de Colombia SA 71 72 121 121 385 -12.70% ABX Air 441 81 83 139 138 2 6 176 172 356 -16.04% Amerijet International 424 0 0 212 212 0 0 177 177 354 3.51% Tampa Cargo S.A. fka 342 0 0 171 171 Tampa Airlines 156 157 0 0 313 -18.49% Frontier Airlines 384 192 192 0 0 12 13 128 131 284 -13.68% IBC Airways Inc 329 23 23 141 142 33 26 110 114 283 27.48% Atlas Air Inc 222 32 26 79 85 0 0 140 141 281 -9.35% COPA Airlines 310 0 0 155 155 0 0 134 134 268 262.16% Aruba Airlines International 74 0 0 37 37 LLC 0 0 120 120 240 -14.89% Aeromexico 282 0 0 141 141 119 119 0 0 238 -8.46% Federal Express 260 130 130 0 0 Corporation 0 0 110 111 221 0.45% ABC Aerolineas S.A.