Biopartnering Executive Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uniqure N.V. Paasheuvelweg 25A 1105BP Amsterdam the Netherlands +1-339-970-7000

uniQure N.V. Paasheuvelweg 25a 1105BP Amsterdam The Netherlands +1-339-970-7000 NOTICE OF EXTRAORDINARY GENERAL MEETING OF SHAREHOLDERS To be held on September 14, 2017 To the Shareholders of uniQure N.V.: Notice is hereby given that an Extraordinary General Meeting of Shareholders (the “Extraordinary Meeting”) of uniQure N.V., a public company with limited liability ( naamloze vennootschap ) under the laws of the Netherlands (the “Company,” “uniQure,” and “we”), will be held on September 14, 2017, at 9:30 a.m., Central European Summer Time, at the Company’s principal executive offices located at Paasheuvelweg 25a, 1105BP Amsterdam, the Netherlands, for the following purposes: I. Opening and announcements; II. Appointment of Jeremy P. Springhorn, Ph.D. as a non-executive director (voting proposal no. 1); III. Appointment of Madhavan Balachandran as a non-executive director (voting proposal no. 2); IV Any other business that may properly come before the meeting or any adjournment of the meeting; and V. Closing of the meeting. Each person authorized to attend the Extraordinary Meeting may inspect the Agenda at the office of uniQure. Our Board of Directors (our “Board”) recommends that you vote “FOR” each of the voting proposals noted above. The record date is set at the close of business on August 17, 2017 EST and, therefore, only the Company’s shareholders of record at the close of business on August 17, 2017 EST are entitled to receive this notice (this “Notice”) and to vote at the Extraordinary Meeting and any adjournment thereof. Only shareholders who have given notice in writing to the Company by September 12, 2017 of their intention to attend the Extraordinary Meeting in person are entitled to attend the Extraordinary Meeting in person. -

CB2013 Committee and Board Disclosureauditlist 9.10.13

2013-2014 Conflict of Interest Disclosure AST Activity Participant First Name Participant Last Name Degree DisclosureDate Disclsoure Item Committee Member Reza Abdi MD 4/22/2013 No Relevant Financial Relationships Committee Member Sameh R. Abul-Ezz MD, PhD 4/16/2013 No Relevant Financial Relationships Committee Member Deborah B. Adey MD 4/15/2013 No Relevant Financial Relationships Committee Member Enver Akalin MD 4/16/2013 Consultant relationship with Pfizer Fellows 2013 Maria-Luisa Alegre MD, PhD 7/12/2013 No Relevant Financial Relationships Committee Member Alessandrini Alessandro PhD 4/29/2013 No Relevant Financial Relationships Board Member James S. Allan MD 5/3/2013 Committee Member No Relevant Financial Relationships Rita R. Alloway PharmD, FCCP Grant Support relationship with Astellas Grant Support relationship with BMS Grant Support relationship with Novartis Grant Support relationship with Lifecycle Grant Support relationship with Millenium Grant Support relationship with Pfizer (previously Wyeth) Grant Support relationship with Genentech (previously Roche) Board Member Grant Support relationship with Viropharma Committee Member Grant Support relationship with Alexion Fellows 2013 7/18/2013 Grant Support relationship with Sanofi (previously Genzyme, previously Sangstat) Committee Member Sandra Amaral MD, MHS 6/18/2013 Other relationship with Bristol Myers-Squibb Hatem Amer MD 5/6/2013 Grant Support relationship with Abbott Laborartories. Committee Member Other relationship with Massacheussetts Medical Society. Committee Member William Applegate No Relevant Financial Relationships Committee Member Alexander Aussi BSN, RN, MBA 4/22/2013 Consultant relationship with Total Transplant Advantage, LLC Committee Member Jamil Azzi MD 4/30/2013 No Relevant Financial Relationships Committee Member Fellows 2013 Mark L. -

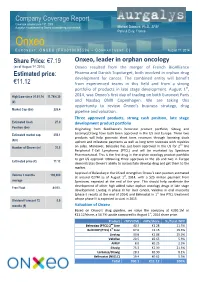

Company Coverage Report

Company Coverage Report th Coverage initiated June 19 , 2009 Aurgalys is contracted by Onxeo to provide equity research Mickael Dubourd, Ph.D., SFAF Paris & Evry, France Onxeo E URONEXT : ONXEO [FR0010095596 – C OMPARTMENT C] August 1st, 2014 Share Price: €7.19 Onxeo, leader in orphan oncology (as of August 1st, 2014) Onxeo resulted from the merger of French BioAlliance Estimated price: Pharma and Danish Topotarget, both involved in orphan drug development for cancer. The combined entity will benefit €11.12 from experienced teams in this field and from a strong portfolio of products in late stage development. August 1st, High/Low since 01.01.14 11.74/4.30 2014, was Onxeo’s first day of trading on both Euronext Paris (€) and Nasdaq OMX Copenhagen. We are taking this opportunity to review Onxeo’s business strategy, drug Market Cap (€m) 226.4 pipeline and valuation. Three approved products, strong cash position, late stage Estimated Cash 27.0 development product portfolio Position (€m) Originating from BioAlliance's historical product portfolio, Sitavig and Estimated market cap. 350.1 Loramyc/Oravig have both been approved in the US and Europe. These two products will help generate short term revenues through licensing deals (€m) upfront and milestone payments as well as long term revenues with royalties nd Number of Shares (m) 31.5 on sales. Moreover, Beleodaq has just been approved in the US for 2 line Peripheral T-Cell Lymphoma (PTCL) and will be marketed by Spectrum Pharmaceutical. This is the first drug in the orphan oncology product portfolio to get US approval. -

Biotechnology Worldwide

Biotechnology Worldwide There are several countries that are making special efforts to both develop and capitalise on Biotechnology. Chief amongst them is America, though cutting edge work is also going on in the UK, Ireland, Germany, Korea, Singapore, China and Japan. • America is the world leader in biotechnology, it has 1,379 biotechnology companies and employs 174,000 people. It spends £9 billion on research into biotechnology. • The European market for goods and services dependent on biotechnology is currently estimated at £30 billion and is forecast to exceed £100 billion by the year 2005 • The UK leads Europe in biotechnology and employs 19,000 people • The UK has 300 dedicated biotechnology companies and a further 250-300 involved in broader bioscience related activities • The industrial sectors which stand to benefit from biotechnology are pharmaceutical, agriculture, food and drink, chemicals and environmental technologies • Germany is the second strongest country in Europe, with 332 companies but fewer products in development than the UK. UK The UK biotechnology industry is regarded as second only to the huge effort taking place in the States. UK biotechnology companies generate over a billion pounds in revenue; half of this is pumped back into research and development. The industry has particular strengths, for example: • Britain was a key player in the world wide project of sequencing the 30,000 genes of the human genome. The announcement of the first working draft of the human genome marks a significant step forward in our understanding of the way in which we understand and develop treatments for incurable genetic conditions. -

AMGEN INC. V. SANOFI

Case: 20-1074 Document: 159 Page: 1 Filed: 06/21/2021 NOTE: This order is nonprecedential. United States Court of Appeals for the Federal Circuit ______________________ AMGEN INC., AMGEN MANUFACTURING, LIMITED, AMGEN USA, INC., Plaintiffs-Appellants v. SANOFI, AVENTISUB LLC, FKA AVENTIS PHARMACEUTICALS INC., REGENERON PHARMACEUTICALS INC., SANOFI-AVENTIS U.S. LLC, Defendants-Appellees ______________________ 2020-1074 ______________________ Appeal from the United States District Court for the District of Delaware in Nos. 1:14-cv-01317-RGA, 1:14-cv- 01349-RGA, 1:14-cv-01393-RGA, 1:14-cv-01414-RGA, Judge Richard G. Andrews. ______________________ JEFFREY A. LAMKEN, MoloLamken LLP, Washington, DC, filed a petition for rehearing en banc for plaintiffs-ap- pellants. Also represented by SARAH JUSTINE NEWMAN, MICHAEL GREGORY PATTILLO, JR.; SARA MARGOLIS, New York, NY; EMILY JOHNSON, ERICA S. OLSON, STEVEN TANG, STUART WATT, WENDY A. WHITEFORD, Amgen Inc., Thou- sand Oaks, CA; KEITH HUMMEL, Cravath Swaine & Moore LLP, New York, NY; WILLIAM G. GAEDE, III, McDermott Case: 20-1074 Document: 159 Page: 2 Filed: 06/21/2021 2 AMGEN INC. v. SANOFI Will & Emery LLP, Menlo Park, CA; CHRISTOPHER B. MEAD, Schertler Onorato Mead & Sears LLP, Washington, DC; JAMES L. HIGGINS, MELANIE K. SHARP, Young, Cona- way, Stargatt & Taylor, LLP, Wilmington, DE. Plaintiff- appellant Amgen Inc. also represented by SARAH CHAPIN COLUMBIA, McDermott, Will & Emery LLP, Boston, MA; LAUREN MARTIN, Quinn Emanuel Urquhart & Sullivan LLP, Boston, MA. MATTHEW WOLF, Arnold & Porter Kaye Scholer LLP, Washington, DC, filed a response for defendants-appellees. Also represented by VICTORIA REINES; DAVID K. BARR, DANIEL REISNER, New York, NY; DEBORAH E. -

Surescripts, Llc As Amicus Curiae in Support of Petitioners in No

Nos. 19-508 and 19-825 In the Supreme Court of the United States ———————————— AMG CAPITAL MANAGEMENT, LLC, ET AL., Petitioners, v. FEDERAL TRADE COMMISSION, Respondent. ———————————— FEDERAL TRADE COMMISSION, Petitioner, v. CREDIT BUREAU CENTER, LLC, ET AL., Respondents. ———————————— ON WRITS OF CERTIORARI TO THE UNITED STATES COURTS OF APPEALS FOR THE SEVENTH AND NINTH CIRCUITS ———————————— BRIEF OF SURESCRIPTS, LLC AS AMICUS CURIAE IN SUPPORT OF PETITIONERS IN NO. 19-508 AND RESPONDENTS IN NO. 19-825 ———————————— ALFRED C. PFEIFFER, JR. ROMAN MARTINEZ LATHAM & WATKINS LLP Counsel of Record 505 Montgomery Street AMANDA P. REEVES Suite 2000 ALLYSON M. MALTAS San Francisco, CA 94111 DOUGLAS C. TIFFT BLAKE E. STAFFORD JAMES A. TOMBERLIN* LATHAM & WATKINS LLP 555 Eleventh Street, NW Suite 1000 Washington, DC 20004 (202) 637-2200 [email protected] Counsel for Amicus Curiae Surescripts, LLC TABLE OF CONTENTS Page TABLE OF AUTHORITIES ...................................... ii INTEREST OF AMICUS CURIAE ............................1 SUMMARY OF ARGUMENT .....................................3 ARGUMENT ...............................................................5 I. The FTC Has Increasingly Wielded Section 13(b) To Obtain Monetary Relief In Antitrust Cases ................................................5 II. The FTC’s Antitrust Authority Confirms That Section 13(b) Does Not Authorize Monetary Relief ..................................................22 CONCLUSION ..........................................................32 ii TABLE OF AUTHORITIES Page(s) CASES Apple Inc. v. Pepper, 139 S. Ct. 1514 (2019) .......................................... 13 Armstrong v. Exceptional Child Center, Inc., 575 U.S. 320 (2015) .............................................. 23 Bell Atlantic Corp. v. Twombly, 550 U.S. 544 (2007) .............................................. 26 In re Cardinal Health, Inc., No. 101-0006, 2015 WL 1849040 (F.T.C. Apr. 17, 2015) ........................ 19, 20, 28, 30 Credit Suisse Securities (USA) LLC v. Billing, 551 U.S. -

Federal Register/Vol. 84, No. 232/Tuesday, December 3, 2019

Federal Register / Vol. 84, No. 232 / Tuesday, December 3, 2019 / Notices 66191 the Assistant Attorney General, patterns, devices, manufacturing filed with and accepted, subject to final developed the HSR Rules and the processes, or customer names. approval, by the Commission, has been corresponding Notification and Report placed on the public record for a period Form. Heather Hippsley, of thirty (30) days. The following On September 11, 2019, the Deputy General Counsel. Analysis to Aid Public Comment Commission sought comment on the [FR Doc. 2019–26075 Filed 12–2–19; 8:45 am] describes the terms of the consent reporting requirements associated with BILLING CODE 6750–01–P agreement and the allegations in the the HSR Rules and corresponding complaint. An electronic copy of the Notification and Report Form. 84 FR full text of the consent agreement 47951. No relevant comments were FEDERAL TRADE COMMISSION package can be obtained from the FTC received. Pursuant to the OMB [File No. 191 0061] Home Page (for November 15, 2019), on regulations, 5 CFR part 1320, that the World Wide Web, at https:// implement the PRA, 44 U.S.C. 3501 et Bristol-Myers Squibb Company and www.ftc.gov/news-events/commission- seq., the FTC is providing this second Celgene Corporation; Analysis of actions. opportunity for public comment while Agreement Containing Consent Orders You can file a comment online or on seeking OMB approval to renew the pre- To Aid Public Comment paper. For the Commission to consider existing clearance for those information your comment, we must receive it on or collection requirements. -

National Cancer Institute Cancer National

DIVISION OF CANCER TREATMENT AND DIAGNOSIS National Cancer Institute Cancer National PROGRAM ACCOMPLISHMENTS 2006 U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES National Institutes of Health TABLE OF CONTENTS Foreword . iii Division of Cancer Treatment and Diagnosis Overview . .1 Major Ongoing Initiatives and Accomplishments . .7 Biometric Research Branch Overview . 11 Partnerships and Collaborations . 12 Scientific Advances . 17 Other Biostatistical Research . 24 Tools, Products, and Resources . 27 Cancer Diagnosis Program Overview . 29 Major Ongoing Initiatives . 30 Current Funding Opportunities . 34 Partnerships and Collaborations . 36 Scientific Advances . 39 Tools, Products, and Resources . 41 Cancer Imaging Program Overview . 45 Major Ongoing Initiatives . 47 Current Funding Opportunities . 54 Partnerships and Collaborations . 57 Scientific Advances . 61 Tools, Products, and Resources . 63 Cancer Therapy Evaluation Program Overview . 65 Major Ongoing Initiatives . 67 Significant Ongoing Clinical Trials . 71 Current Funding Opportunities . 73 Partnerships and Collaborations . 75 Scientific Advances . 79 Tools, Products, and Resources . 92 TABLE OF CONTENTS ■ i Developmental Therapeutics Program Overview . 95 New Initiatives . 97 Major Ongoing Initiatives . .100 Current Funding Opportunities . .104 Tools, Products, and Resources . .105 History-Marking Event . .114 Scientific Advances . .115 Radiation Research Program Overview . .119 Partnerships and Collaborations . .121 Scientific Advances . .127 Tools, Products, and Resources . .129 -

Shire Acquisition of Viropharma - Strategic Move to Strengthen Shire’S Rare Disease Business - Augments Already Strong Growth Prospects

Shire acquisition of ViroPharma - Strategic move to strengthen Shire’s Rare Disease business - Augments already strong growth prospects Flemming Ornskov, MD Chief Executive Officer Graham Hetherington Chief Financial Officer Our purpose We enable people with life-altering conditions to lead better lives. CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS Statements included in this communication that are not historical facts are forward-looking statements. Forward-looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialize, results could be materially adversely affected. The risks and uncertainties include, but are not limited to, that: •Shire’s proposed acquisition of ViroPharma may not be consummated due to the occurrence of an event, change or other circumstances that gives rise to the termination of the merger agreement; •a governmental or regulatory approval required for the proposed acquisition of ViroPharma may not be obtained, or may be obtained subject to conditions that are not anticipated, or another condition to the closing of the proposed acquisition may not be satisfied; •ViroPharma may be unable to retain and hire key personnel and/or maintain its relationships with customers, suppliers and other business partners pending the consummation of the proposed acquisition by Shire, or ViroPharma’s business may be disrupted by the proposed acquisition, including increased costs and diversion of management time and resources; •difficulties in integrating ViroPharma into Shire may lead to the combined company not being able to realize the expected operating efficiencies, cost savings, revenue enhancements, synergies or other benefits at the time anticipated or at all; and risks and uncertainties detailed from time to time in Shire’s or ViroPharma’s filings with the U.S. -

Belinostat Phase II Trial Initiated in Platinum-Resistant Ovarian Cancer by the Gynecologic Oncology Group (GOG) Supported by the National Cancer Institute (US)

To NASDAQ OMX Copenhagen A/S TopoTarget A/S Announcement No. 01-10 / Copenhagen, January 6 2010 Symbion Fruebjergvej 3 DK 2100 Copenhagen Denmark Tel: +45 39 17 83 92 Fax: +45 39 17 94 92 CVR-nr: 25695771 www.topotarget.com Belinostat phase II trial initiated in platinum-resistant ovarian cancer by the Gynecologic Oncology Group (GOG) supported by the National Cancer Institute (US) Copenhagen, Denmark – January 6, 2010 – TopoTarget A/S (OMX: TOPO) announced today that GOG (The Gynecologic Oncology Group, US) has initiated a phase II trial evaluating efficacy and safety of belinostat and carboplatin in the treatment of recurrent or persistent platinum-resistant ovarian, fallopian tube or peritoneal cancer. GOG receives support for this trial from the National Cancer Institute (NCI) of the National Institutes of Health (NIH). “Positive efficacy and safety data with belinostat and carboplatin and paclitaxel (BelCaP) in patients with platinum resistant ovarian cancer have previously been announced by TopoTarget. We are very pleased that GOG now initiates this phase II study with belinostat and carboplatin (BelCar) in this difficult to treat patient population. Platin-resistance is a huge unsolved clinical problem in relapsing ovarian cancer and hopefully GOG will be able to show that BelCar, without additional paclitaxel is active in the platinum resistant setting.” said MD., Professor Peter Buhl Jensen, CEO of TopoTarget “ if GOG is able to repeat our initial positive results in platinum resistant patients we hope to advance into pivotal trials.” The study A Phase II evaluation of belinostat and carboplatin in the treatment of recurrent or persistent platinum-resistant ovarian, fallopian tube, or primary peritoneal cancer. -

BIOGEN INTERNATIONAL GMBH, Plaintiff-Appellant

Case: 20-1373 Document: 41 Page: 1 Filed: 04/21/2020 United States Court of Appeals for the Federal Circuit ______________________ BIOGEN INTERNATIONAL GMBH, Plaintiff-Appellant v. BANNER LIFE SCIENCES LLC, Defendant-Appellee ______________________ 2020-1373 ______________________ Appeal from the United States District Court for the District of Delaware in No. 1:18-cv-02054-LPS, Chief Judge Leonard P. Stark. ______________________ Decided: April 21, 2020 ______________________ JAMES B. MONROE, Finnegan, Henderson, Farabow, Garrett & Dunner, LLP, Washington, DC, for plaintiff-ap- pellant. Also represented by PAUL WILLIAM BROWNING, J. MICHAEL JAKES, LAURA POLLARD MASUROVSKY, JASON LEE ROMRELL. KYLE MUSGROVE, Parker Poe Adams & Bernstein LLP, Charlotte, NC, for defendant-appellee. Also represented by JOHN WORTHINGTON BATEMAN, ELIZABETH CROMPTON, SCOTT A. CUNNING, II, Washington, DC. ______________________ Case: 20-1373 Document: 41 Page: 2 Filed: 04/21/2020 2 BIOGEN INTERNATIONAL GMBH v. BANNER LIFE SCIENCES LLC Before LOURIE, MOORE, and CHEN, Circuit Judges. LOURIE, Circuit Judge. Biogen International GmbH (“Biogen”) appeals from a judgment of the United States District Court for the Dis- trict of Delaware that Banner Life Sciences LLC (“Banner”) does not infringe the extended portion of U.S. Patent 7,619,001 (the “’001 patent”), extended under the patent term restoration provisions of the Hatch-Waxman Act, Pub. L. No. 98-417, § 201, 98 Stat. 1585, 1598 (as codified at 35 U.S.C. § 156 (2018)). Biogen Int’l GmbH v. Banner Life Scis. LLC, No. 18-2054-LPS, 2020 WL 109499 (D. Del. Jan. 7, 2020) (“Decision”). Because the scope of a patent term extension under 35 U.S.C. -

Etf-Sparpläne

ETF-SPARPLÄNE ISIN NAME IE00B8KGV557 ISHARES EDGE MSCI EM MIN VOL USD (ACC) IE00B86MWN23 ISHARES EDGE MSCI EUROPE MIN VOLATILITY EUR (ACC) IE00B8FHGS14 ISHARES EDGE MSCI WORLD MIN VOLATILITY USD (ACC) IE00B6SPMN59 ISHARES EDGE S&P 500 MIN VOL USD (ACC) IE00B87G8S03 ISHARES GLOBAL AAA-AA GOV BOND USD (DIST) DE0005933931 ISHARES CORE DAX EUR (ACC) IE0032523478 ISHARES CORP BOND LARGE CAP EUR (DIST) IE00B14X4T88 ISHARES ASIA PACIFIC DIVIDEND USD (DIST) IE00B1W57M07 ISHARES BRIC 50 USD (DIST) DE000A0F5UG3 ISHARES DOW JONES EU SUSTAINABLE EUR (DIST) IE00B6R52143 ISHARES AGRIBUSINESS USD (ACC) IE00B0M62Y33 ISHARES AEX EUR (DIST) DE000A0D8Q23 ISHARES ATX EUR (DIST) IE00B1FZSC47 ISHARES USD TIPS USD (ACC) IE00B14X4S71 ISHARES USD TREASURY BOND 1-3Y USD (DIST) IE00B1FZS798 ISHARES USD TREASURY BOND 7-10Y USD (DIST) IE00B1FZSD53 ISHARES GBP INDEX-LINKED GILTS GBP (DIST) IE00B6QGFW01 ISHARES EMERGING ASIA LOCAL GOV BOND USD (DIST) IE00B5M4WH52 ISHARES JPM EM LOCAL GOV BOND USD (DIST) IE00B3DKXQ41 ISHARES EURO AGGREGATE BOND EUR (DIST) IE00B3F81R35 ISHARES CORE EURO CORP BOND EUR (DIST) IE00B4L60045 ISHARES EURO CORP BOND 1-5Y EUR (DIST) IE00B4L5ZG21 ISHARES EURO CORP BOND EX-FIN EUR (DIST) IE00B4L5ZY03 ISHARES EURO CORP BOND EX-FIN 1-5Y EUR (DIST) IE00B6X2VY59 ISHARES EURO CORP BOND INT. RATE HEDGED (DIST) IE00B14X4Q57 ISHARES EURO GOV BOND 1-3Y EUR (DIST) IE00B4WXJH41 ISHARES EURO GOV BOND 10-15Y EUR (DIST) IE00B1FZS913 ISHARES EURO GOV BOND 15-30Y EUR (DIST) IE00B1FZS681 ISHARES EURO GOV BOND 3-5Y EUR (DIST) IE00B4WXJG34 ISHARES EURO GOV BOND