The Dow Theory and the Management of Investments

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Stairstops Using Magee’S Basing Points to Ratchet Stops in Trends

StairStops Using Magee’s Basing Points to Ratchet Stops in Trends This may be the most important book on stops of this decade for the general investor. Professor Henry Pruden, PhD. Golden Gate University W.H.C. Bassetti Coauthor/Editor Edwards & Magee’s Technical Analysis of Stock Trends, 9th Edition This book contains information obtained from authentic and highly regarded sources. Reprinted material is quoted with permission, and sources are indicated. A wide variety of references are listed. Reasonable efforts have been made to publish reliable date and information, but the author and the publisher cannot assume responsibility for the validity of all materials or for the consequences of their use. Neither this book nor any part may be reproduced or transmitted in any form by any means, electronic or mechanical, including photocopying, microfilming, and recording, or by any information storage or retrieval system, without prior permission in writing from the publisher. The consent of MaoMao Press LLC does not extend to copying for general distribution, for promotion, for creating new works, or for resale. Specific permission must be obtained in writing from MaoMao Press LLC for such copying. Direct all inquiries to MaoMao Press LLC, POB 88, San Geronimo, CA 94963-0088 Trademark Notice: Product or corporate names may be trademarks or registered trademarks, and are used only for identification and explanation, without intent to infringe. Dow–JonesSM, The DowSM, Dow–Jones Industrial AverageSM, and DJIASM are service marks of Dow– Jones & Company, Inc., and have been licensed for use for certain purposes by the Board of Trade of the City of Chicago (CBOT®). -

Dow Theory for the 21St Century Schannep Timing Indicator COMPOSITE Indicator

st April 1 , 2015 Dow Theory for the 21st Century Schannep Timing Indicator COMPOSITE Indicator Charting a Course of Caution Dow Jones: 17,776.12 S&P 500: 2,067.88 OVERVIEW: There are many stock market and economic indicators ‘out NYSE: 11,062.79 there’, and we can’t follow them all. But every so often we see something that causes us to take a look. Recently a couple of lesser known, or followed, indicators have given us pause in our bullishness. A MarketWatch column by Mark Hulbert about an indicator described by Norman Fosback in his 1976 ‘classic’ Stock Market Logic is intriguing. In years prior to those shown in the chart below, Fosback states that from 1942 to 1975, the "tops of 1946, '56, '59, '61, '66, '68, and '73 were all accompanied or preceded by turns in margin debt". All but 1959 were major bull market tops, as you can see at the Historic Record on our website. The concept illustrated is that ‘sophisticated’ investors aggressively use margin in bull markets, but pull in their horns when stocks start going down. Fosback further stated that when the trend is down, there is a 59% chance a bear market is in progress (41% a bull market is in progress) - not good odds. That implies the bull market topped out earlier this last month on March 2nd at 18,288.63! How’s that for a cloudy outlook? On the other hand, when margin debt is rising there is an 85% probability that a bull market is in progress – as has been the case since 2011, until now. -

Investing with Volume Analysis

Praise for Investing with Volume Analysis “Investing with Volume Analysis is a compelling read on the critical role that changing volume patterns play on predicting stock price movement. As buyers and sellers vie for dominance over price, volume analysis is a divining rod of profitable insight, helping to focus the serious investor on where profit can be realized and risk avoided.” —Walter A. Row, III, CFA, Vice President, Portfolio Manager, Eaton Vance Management “In Investing with Volume Analysis, Buff builds a strong case for giving more attention to volume. This book gives a broad overview of volume diagnostic measures and includes several references to academic studies underpinning the importance of volume analysis. Maybe most importantly, it gives insight into the Volume Price Confirmation Indicator (VPCI), an indicator Buff developed to more accurately gauge investor participation when moving averages reveal price trends. The reader will find out how to calculate the VPCI and how to use it to evaluate the health of existing trends.” —Dr. John Zietlow, D.B.A., CTP, Professor of Finance, Malone University (Canton, OH) “In Investing with Volume Analysis, the reader … should be prepared to discover a trove of new ground-breaking innovations and ideas for revolutionizing volume analysis. Whether it is his new Capital Weighted Volume, Trend Trust Indicator, or Anti-Volume Stop Loss method, Buff offers the reader new ideas and tools unavailable anywhere else.” —From the Foreword by Jerry E. Blythe, Market Analyst, President of Winthrop Associates, and Founder of Blythe Investment Counsel “Over the years, with all the advancements in computing power and analysis tools, one of the most important tools of analysis, volume, has been sadly neglected. -

Chapter 8 Stock Price Behavior and Market Efficiency Questions and Problems

CHAPTER 8 Stock Price Behavior and Market Efficiency “One of the funny things about the stock market is that every time one man buys, another sells, and both think they are astute.” William Feather “There are two times in a man’s life when he shouldn’t speculate: When he can’t afford it, and when he can.” Mark Twain Our discussion of investments in this chapter ranges from the most controversial issues, to the most intriguing, to the most baffling. We begin with bull markets, bear markets, and market psychology. We then move into the question of whether you, or indeed anyone, can consistently “beat the market.” Finally, we close the chapter by describing market phenomena that sound more like carnival side shows, such as “the amazing January effect.” (marg. def. technical analysis Techniques for predicting market direction based on (1) historical price and volume behavior, and (2) investor sentiment.) 8.1 Technical Analysis In our previous two chapters, we discussed fundamental analysis. We saw that fundamental analysis focuses mostly on company financial information. There is a completely different, and controversial, approach to stock market analysis called technical analysis. Technical analysis boils down to an attempt to predict the direction of future stock price movements based on two major types of information: (1) historical price and volume behavior and (2) investor sentiment. 2 Chapter 8 Technical analysis techniques are centuries old, and their number is enormous. Many, many books on the subject have been written. For this reason, we will only touch on the subject and introduce some of its key ideas in the next few sections. -

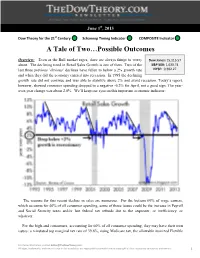

Dow Theory for the 21St Century Schannep Timing Indicator COMPOSITE Indicator a Tale of Two…Possible Outcomes

st June 1 , 2013 Dow Theory for the 21st Century Schannep Timing Indicator COMPOSITE Indicator A Tale of Two…Possible Outcomes Overview: Even as the Bull market rages, there are always things to worry Dow Jones: 15,115.57 about. The declining trend in Retail Sales Growth is one of them. Two of the S&P 500: 1,630.74 last three previous ‘obvious’ declines have fallen to below a 2% growth rate NYSE: 9,302.27 and when they did the economy entered into recession. In 1995 the declining growth rate did not continue and was able to stabilize above 2% and avoid recession. Today’s report, however, showed consumer spending dropped to a negative -0.2% for April, not a good sign. The year- over-year change was about 2.8%. We’ll keep our eyes on this important economic indicator: The reasons for this recent decline in sales are numerous. For the bottom 60% of wage earners, which accounts for 40% of all consumer spending, some of those issues could be the increase in Payroll and Social Security taxes and/or late federal tax refunds due to the sequester, or inefficiency, or whatever. For the high-end consumers, accounting for 60% of all consumer spending, they may have their own issues: a reinstated top marginal tax rate of 39.6%, rising Medicare tax, the allowable itemized Flexible For more information, contact [email protected]. All logos, trademarks, and content used in this newsletter are registered trademarks and/or copyright of their respective companies and owners. 1 st June 1 , 2013 spending health-care accounts reduced by half, and the top rate on long-term capital gains and dividends rose from 15% to 20%. -

Bear Market Investing Strategies WILEY TRADING SERIES

Y L F M A E T Team-Fly® Bear Market Investing Strategies WILEY TRADING SERIES The Psychology of Finance, revised edition Lars Tvede The Elliott Wave Principle: Key to Market Behavior Robert R. Prechter International Commodity Trading Ephraim Clark, Jean-Baptiste Lesourd and Rene´Thie´blemont Dynamic Technical Analysis Philippe Cahen Encyclopedia of Chart Patterns Thomas N. Bulkowski Integrated Technical Analysis Ian Copsey Financial Markets Tick by Tick: Insights in Financial Markets Microstructure Pierre Lequeux Technical Market Indicators: Analysis and Performance Richard J. Bauer and Julie R. Dahlquist Trading to Win: The Psychology of Mastering the Markets Ari Kiev Pricing Convertible Bonds Kevin Connolly At the Crest of the Tidal Wave: A Forecast for the Great Bear Market Robert R. Prechter BEAR MARKET INVESTING STRATEGIES Harry D. Schultz Copyright # 2002 by John Wiley & Sons Ltd Baffins Lane, Chichester, West Sussex PO19 1UD, England National 01243 779777 International (þ44) 1243 779777 e-mail (for orders and customer service enquiries): [email protected] Visit our Home Page on http://www.wiley.co.uk or http://www.wiley.com All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency, 90 Tottenham Court Road, London W1P 9HE, UK without -

September 2015 the Dow Jones Industrial Average (DJIA), S&P 500

On Our Radar – September 2015 The Dow Jones Industrial Average (DJIA), S&P 500 and NASDAQ Composite fell 6.56 percent, 6.25 percent, and 6.85 percent, respectively, in August, which was highlighted by a dramatic 1089.42 point decline in the DJIA in the first ten minutes of trading on Monday August 24, 2015. That extreme selloff was shortly followed by a two-day rally of 988.33 points, the largest in history. Although last month we stated that trading in August “can subject the markets to large swings,” and that “it is not unusual for periods of low volatility to be followed by periods of high volatility,” we did not anticipate a decline of 1692.28 DJIA points in four days. The catalyst for the decline seems to have been a combination of factors including the devaluation of the Chinese renminbi (yuan), which surprised the markets. On or about August 11, 2015, the International Monetary Fund (IMF) decided that the yuan would not be part of a reserve currency basket, at least for another year. Soon thereafter, China officially devalued their currency. As the U.S. plays a dominant role in the IMF, China’s response may have been a way to retaliate against the U.S. In addition, a deceleration in China’s economic growth along with a strong U.S. dollar have caused a massive bear market in commodities, led by the near 60 percent decline in the price of oil. This is putting further economic pressure on oil producing countries including Russia and Saudi Arabia. -

A Technical Analysis-Based Method for Share Price Forecasting

A TECHNICAL ANALYSIS-BASED METHOD FOR SHARE PRICE FORECASTING C.A. Mahesh Kumar1, S.Naseeruddin2, B.Narendra3, A.Venugopal Reddy4 1Assistant Professor, 2,3,4P.G Student, Department of Management Studies, Gates Institute of Technology, Gooty, A.P (India) ABSTRACT Technical analysis attempts to explain and forecast changes in security prices by studying only the market data. In other words a study of past share prices behavior to predict the future trend is termed as technical analysis. The main objective of this paper is to identify or predict the share price in stock market by using Dow theory, moving average method(MAM), relative strength index(RSI). Dow Theory, moving average method and relative strength index these are all tools of technical analysis. Dow theory is a market indicator and MAM,RSI are market and individual stock indicators. Here we find out primary movements , secondary reactions and minor movements and also to know the bullish trend and bearish trend. Keywords: Technical analysis, Dow theory, Moving average method(MAM),Bullish & Bearish trend and also Relative strength index(RSI). I. INTRODUCTION The methods used to analyze securities and make investment decisions fall into two very broad categories: fundamental analysis and technical analysis. Fundamental analysis involves analyzing the characteristics of a company in order to estimate its value. Technical analysis takes a completely different approach; it doesn't care one bit about the "value" of a company or a commodity. Technicians (sometimes called chartists) are only interested in the price movements inthemarket. Despite all the fancy and exotic tools it employs, technical analysis really just studies supply and demand in a market in an attempt to determine what direction, or trend, will continue in the future. -

Technical Analysis in the Foreign Exchange Market

Research Division Federal Reserve Bank of St. Louis Working Paper Series Technical Analysis in the Foreign Exchange Market Christopher J. Neely and Paul A. Weller Working Paper 2011-001B http://research.stlouisfed.org/wp/2011/2011-001.pdf January 2011 Revised July 2011 FEDERAL RESERVE BANK OF ST. LOUIS Research Division P.O. Box 442 St. Louis, MO 63166 ______________________________________________________________________________________ The views expressed are those of the individual authors and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis, the Federal Reserve System, or the Board of Governors. Federal Reserve Bank of St. Louis Working Papers are preliminary materials circulated to stimulate discussion and critical comment. References in publications to Federal Reserve Bank of St. Louis Working Papers (other than an acknowledgment that the writer has had access to unpublished material) should be cleared with the author or authors. Prepared for Wiley’s Handbook of Exchange Rates Technical Analysis in the Foreign Exchange Market Christopher J. Neely* Paul A. Weller July 24, 2011 Abstract: This article introduces the subject of technical analysis in the foreign exchange market, with emphasis on its importance for questions of market efficiency. “Technicians” view their craft, the study of price patterns, as exploiting traders’ psychological regularities. The literature on technical analysis has established that simple technical trading rules on dollar exchange rates provided 15 years of positive, risk-adjusted returns during the 1970s and 80s before those returns were extinguished. More recently, more complex and less studied rules have produced more modest returns for a similar length of time. Conventional explanations that rely on risk adjustment and/or central bank intervention do not plausibly justify the observed excess returns from following simple technical trading rules. -

The Dow Theory in Technical Analysis

The Dow Theory in Technical Analysis CharlesDow is the father of the modern technical analysis in theWest. He developed a theory, later called Dow Theory, whichexpresses his ideas on price actions in the stock market. www.ifcmarkets.com CharlesDow is the father of the modern technical analysis in theWest. He developed a theory, later called Dow Theory, whichexpresses his Theideas Dow on Theoryprice in Technicalactions Analysisin the stock market. INTRODUCTION oday Foreign Exchange Market is one of the popular segments of the glob- al financial market. FOREX is the largest and the most liquid financial market in the world. The daily turnover of the market reaches up to $5 Ttrillion. That’s really an enormous number! Day by day more and more people get interested in Forex and try to make money by trading. The reason why Foreign Exchange Market is so attractive is due to the following characteristic features: • high liquidity • variety of trading instruments • availability of the market, that is to say the market is active 24 hours a day, except for weekends Being that much attractive, Foreign Exchange Market is also very unpredictable, and you should be very careful while trading and use some methods of analysis and tools that will help you somehow to forecast the behavior of the market. The two most well-known methods of analysis for predicting the market are tech- nical analysis and fundamental analysis, which are considered to be the insepa- rable part of trading. In this article we are going to speak about technical analysis trying to observe its role in financial markets. -

Study Book for Successful Foreign Exchange Dealing

ROYALFOREX FFOORREEXX STUDY BOOK FOR SUCCESSFUL FOREIGN EXCHANGE DEALING Los Angeles, California 2001 Contents 1.Common knowledge about the trading on Forex 1.1. Forex as a aart af the global financial market Brief data about the Forex rise and development. The factors caused Foreign Exchange Volume Growth on Forex (Exchange Rate Volatility, Business Internationalization, Increasing of Traders’ Sophistication, Developments in Telecommunications, Computer And Programming Development). The role of the U.S. Federal Reserve System and central banks of other G-7 countries on Forex. 1.2. Risks by the trading on Forex 1.3. Forex sectors Spot Market Forward Market Futures Market Currency Options 2. Major currencies and trade systems 2.1. Major currencies The U.S. Dollar The Euro The Japanese Yen The British Pound The Swiss Franc 2.2. Trade systems on Forex Trading with brokers Direct dealing 3. Fundamental analysis by trading on Forex 3.1 Theories of exchange rate determination Purchasing Power Parity Theory of Elasticities Modern monetary theories on exchange rate volatility 3.2. Indicators for the fundamental analysis Economic indicators The Gross National Product The Gross Domestic Product Consumption Spending Investment Spending Government Spending Net Trading Industrial sector indicators 2001 by Royal Forex. All right reserved. www.royalforex.com 2 Industrial Production Capacity Utilization Factory Orders Durable Goods Orders Business Inventories Construction Data Inflation Indicators Producer Price Index Consumer Price Index Gross National Product Implicit Deflator Gross Domestic Product Implicit Deflator Commodity Research Bureau’s Futures Index The Journal of Commerce Industrial Price Balance of Payments Merchandise Trade Balance The U.S. – Japan Merchandise Trade Balance Employment Indicators Employment Cost Index Consumer Spending Indicators Retail Sales Consumer Sentiment Auto Sales Leading Indicators Personal Income 3.3. -

A Technical Analysis-Based Method for Share Price Forecasting

A TECHNICAL ANALYSIS-BASED METHOD FOR SHARE PRICE FORECASTING C.A. Mahesh Kumar1, S.Naseeruddin2, B.Narendra3, A.Venugopal Reddy4 1Assistant Professor, 2,3,4P.G Student, Department of Management Studies, Gates Institute of Technology, Gooty, A.P (India) ABSTRACT Technical analysis attempts to explain and forecast changes in security prices by studying only the market data. In other words a study of past share prices behavior to predict the future trend is termed as technical analysis. The main objective of this paper is to identify or predict the share price in stock market by using Dow theory, moving average method(MAM), relative strength index(RSI). Dow Theory, moving average method and relative strength index these are all tools of technical analysis. Dow theory is a market indicator and MAM,RSI are market and individual stock indicators. Here we find out primary movements , secondary reactions and minor movements and also to know the bullish trend and bearish trend. Keywords: Technical analysis, Dow theory, Moving average method(MAM),Bullish & Bearish trend and also Relative strength index(RSI). I. INTRODUCTION The methods used to analyze securities and make investment decisions fall into two very broad categories: fundamental analysis and technical analysis. Fundamental analysis involves analyzing the characteristics of a company in order to estimate its value. Technical analysis takes a completely different approach; it doesn't care one bit about the "value" of a company or a commodity. Technicians (sometimes called chartists) are only interested in the price movements inthemarket. Despite all the fancy and exotic tools it employs, technical analysis really just studies supply and demand in a market in an attempt to determine what direction, or trend, will continue in the future.