OECD Russia Corporate Governance Roundtable

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Biggest, the Grandest, Luxurious & the Most Epic

WELCOME The Biggest, The Grandest, Luxurious & The Most Epic Bus Journey’s in The World Introduction An all-encompassing journey of magnificent menus, outstanding scenery and incredible cultural heritage, this itinerary brings you face-to-face with Europe’s & Asia’s finest attractions. Celebrate Catalonia with a small-group pintxo (tapas) tasting, enjoy a tasting of robust Tuscan reds and ascend to the top of Europe on Mount Stanserhorn to learn about regional fauna and flora from a Swiss Ranger. You will meet passionate locals along the way who will share insider knowledge and enrich your experience. See all the 'stans (well, most of them) on this comprehensive Bus tour through Central Asia. Explore natural landscapes like Kaindy Lake's sunken forest and witness the hustle and bustle of capital cities and their bazaars, cathedrals, and historical sites. Along the way, you'll Eat like the locals and Sleep in Yurts / Hotels to get even closer to this underexplored destination. Start in Volgograd and end in Moscow! With the Historical tour Remarkable Russia, you have a Epic Road tour taking you through Volgograd, Russia and Moscow, Remarkable Russia includes accommodation in a hotel as well as an expert guide, meals, transport and more. Treat yourself with the epic Himalayan panorama before enjoying a roller- coaster ride to vibrant Kathmandu. The thrilling Tibet Nepal tours are expertly crafted to fulfill your ultimate fantasy to delve into two of the most fascinating Himalayan Kingdoms across the Mighty Himalayas. we promise you quality one-stop service for the entire journey, with safety guaranteed. -

Worldwide Hotel Portfolio

2020 WORLDWIDE HOTEL PORTFOLIO ® As a lifelong traveller, I have stayed in hotels all over the world, and I know that where you unwind at the end of the day truly makes a difference. A well-chosen hotel acts as an extension of your destination, furthering your sense of place while offering the conveniences and hospitality that make you feel at home. Whether you are visiting Botswana or Beijing, it is a hotel’s true local character and superior service that make it an integral part of your journey. The hotels, camps and lodges in this Worldwide Hotel Portfolio are chosen by A&K experts because they embody these essential qualities, effortlessly combining first-rate comfort with a keen eye toward their locale. As you begin to imagine your own A&K adventure, refer to this book with the knowledge that no matter which property you choose, your stay will meet our award-winning standards of comfort, service and authenticity. Geoffrey Kent Founder, Chairman & CEO | Abercrombie & Kent Follow @geoffrey_kent on Instagram 1 Worldwide Hotel Portfolio | 2020 2020 Worldwide Hotel Portfolio 4 AFRICA 42 ASIA, INDIA & THE PACIFIC 86 EUROPE 112 EGYPT, MOROCCO & BEYOND 132 THE AMERICAS 152 A&K VILLAS 800 323 7308 | abercrombiekent.com 1 The Right Hotels for Every Journey You can spend endless hours reading hotel reviews online — or you can leave it to the experts in A&K’s local offices, who know the most authentic and luxurious properties in every locale we visit. 2 Worldwide Hotel Portfolio | 2020 Handpicked Accommodations to Accompany Your Private Journey Luxury Tailor Made Travel means seeing the world exactly your way — while staying at hotels selected with you in mind — on an itinerary designed by the foremost experts. -

Russian and Cypriot Opportunities in an Ever Evolving Tax Environment

www.pwc.com.cy Russian and Cypriot opportunities in an ever evolving tax environment 18 May Lotte Hotel Moscow 8 Bld.2, Novinskiy Blvd., Conference Crystal 2 The Republic of Cyprus is a traditional partner of Russian business, as significant investments into Russian economy are structured through Cypriot companies. We are pleased to invite you to a seminar, which will focus on the recent trends in the Russian tax legislation and how these impact Cypriot structures. Our specialists will comment on how the new approach of Russian tax authorities towards international tax planning as a whole may change business models of operations, for the Groups with presence in Cyprus. We are also pleased to present the view of the Cypriot tax authorities and the Cypriot financial regulator on the most interesting areas for cooperation between our countries. www.pwc.com.cy Russian and Cypriot opportunities in an ever evolving tax environment Time Program 9.00 – 9.30 Registration and coffee Introduction 9.30 – 9.45 Costas Mavrocordatos, Partner, Head of Tax & Legal, PwC Cyprus David John, Tax and Legal Practice Leader, PwC Russia 9.45 – 10.00 Bank of Cyprus Group Louis Pochanis, Senior Manager, International Banking Services, Bank of Cyprus The evolving Russian tax scene: does it have an impact on the Cypriot structures 10.00 – 10.30 Ekaterina Lazorina, Partner, Financial Services, PwC Russia Natalia Kuznetsova, Partner, International Taxation, PwC Russia 10.30 – 11.00 Russian transfer pricing: new rules for international operations Svetlana Stroykova, -

An Dem Ort Der Kapitulation Im Museum “Berlin-Karlshorst” Hat Die Dauerausstellung Neu Eröffnet

Nr. 9 (352) Mai 2013 www.mdz-moskau.eu UNABHÄNGIGE ZEITUNG FÜR POLITIK, WIRTSCHAFT UND KULTUR • GEGRÜNDET 1870 WEST-PAKETE OST-RAKETE возможен ли Der Handel im Internet Kai Bagus wagt die lange диалог? wächst einfach unwidersteh- Reise von Freiburg nach В последние месяцы lich. Jetzt haben sich auch Wladiwostok – mit einem отношения Германии Amazon und Ebay DDR-Mofa und с Россией обострились. in Russland verliebt. 05 HIV im Blut. 10 III StichWORTE RIA Novosti Im vollen Bewusstsein Der emanzipierte Protest meiner Verantwortung sage Gegen die Verhaftungen auf dem Bolotnaja Platz ich, dass es in Tschetschenien sicherer ist als in England! Herzlich willkommen. vor einem Jahr gehen tausende Russen auf die Straße Tschetscheniens Präsident Ramsan Kadyrow in Reaktion auf die Rei- sewarnung, die Großbritannien Anfang Mai ausgegeben hat, für Tschetschenien, Dagestan, Teile des Stawropoler Kreises und Inguscheti- en wegen Terrorgefahr. Ich bin viel zu ominös für diese schöne, neue Welt. Wladislaw Surkow, langjähriger Chef der Präsidialverwaltung, Gestalter der politischen Landschaft unter Putin und Medwedew, zuletzt Vize-Premier. Anfang Mai war auf „eigenes Gesuch“ zurückgetreten. Das vakante Mandat des Ein Jahr ist es her, dass Wladimir Putin in dritter Amtszeit Präsident wurde – nach vier Abgeordneten Ramsan Jahren als Ministerpräsident und einer Rochade mit Dmitrij Medwedew, der seitdem Abdulatipow in der Idioten-Duma aus dem höchsten Amt im Staat wieder selbst als Premier der Regierungsmannschaft geht an ein Mitglied von Einiges vorsteht. Gejährt haben sich auch die Proteste auf dem Bolotnaja Platz vom 6. Mai. Russland. Eine Bilanz des Protest- und Regierungsjahres. Seiten 1, 2 und 4 Dieser Versprecher ist Maria Mor- gun unterlaufen, Nachrichtenspre- cherin beim Fernsehsender „Rossija Von Mandy Ganske-Zapf / einen Wendepunkt: Zum einen für gerrechte einschränken. -

Lotte Hotel Moscow

LOTTE HOTEL MOSCOW A NEW DIMENSION OF LUXURY THE LOTTE HOTELS & RESORTS CHAIN CURRENTLY INCLUDES 32 DELUXE HOTELS IN SOUTH KOREA, RUSSIA, VIETNAM, UZBEKISTAN, MYANMAR, JAPAN, AND THE USA. LOTTE HOTEL MOSCOW (RUSSIA) LOTTE HOTEL ST PETERSBURG (RUSSIA) LOTTE HOTEL JEJU (SOUTH KOREA) L7 MYENGDONG (SOUTH KOREA) LOTTE NEW YORK PALACE (USA) LOTTE HOTEL WORLD (SOUTH KOREA) LOTTE LEGEND HOTEL SAIGON (VIETNAM) SIGNIEL SEOUL (SOUTH KOREA) LOTTE RESORT SOKCHO (SOUTH KOREA) LOTTE GLOBALLY The LOTTE Group takes its name from Charlotte, the protagonist of Goethe’s masterpiece, “The Sorrows of Young Werther.” Charlotte is a character beloved by readers all over the world. Inspired by her, The LOTTE Group has developed into a leading Korean enterprise with a dream of filling the world with love, liberty, and life. It is now expanding further to become a company beloved by people throughout the world. ORIGIN OF THE NAME Lotte Hotel Moscow is strategically located in the centre of Moscow. Offering easy access to business, shopping and entertainment facilities, Tverskaya ul. Lotte Hotel Moscow is only a few kilometres from main railway stations and a comfortable drive from the Moscow International Airports. BOLSHOI THEATRE Bolshaya Nikitskaya ul. Nikitskiy Blvd TRANSPORT ACCESSIBILITY THE HOUSE OF THE GOVERNMENT OF THE RUSSIAN FEDERATION Povarskaya ul. Krasnopresnenskaya nab. MOSCOWCITY Airports Trubnikovskiy per. NOVINSKIY BULEVARD М Vystavochnaya • Sheremetyevo (SVO) – 26 km/45 min by car Borisoglebskiy per. Vozdvizhenka ul. Konyushkovskaya ul. NEW ARBAT ST. Arbatskiy per. М Arbatskaya • Domodedovo (DME) – 42 km/1 hour by car Serebryanyy per. М М Smolenskaya nab. Kompozitorskaya ul. • Vnukovo (VKO) - 25 km/45 min by car Trubnikovskiy per. -

Minutes of 2019 Extraordinary Council Meeting On

Minutes WT Extraordinary Council Meeting Crystal Ball Room, Lotte Hotel Moscow | Moscow, Russia 10h00-18h00 | December 5, 2019 AGENDA 1. Establish Quorum: Call Meeting to Order 2. President Report 3. Approval of the Minutes - Approval of the Minutes of the Council Meeting held in Manchester, UK on May 13, 2019 4. Amendments a. Statues b. Ethics Code c. Finance Rules d. Event Operation Rules e. Standing Procedures for Taekwondo Competitions at Olympic Games f. Medical Code g. Anti-Doping Rules h. Standing Procedures for Para Taekwondo at the Paralympic Games i. Ranking Bylaw 5. Enactment a. Para Taekwondo Ranking Bylaw 6. Approval a. 2020 Strategic Planning | Budget b. 2020 WT Development Guidelines c. Anti-Discrimination Policy 7. Reports a. Test Events for Tokyo 2020 Olympic Games and Paralympic Games b. Athlete Uniform for Tokyo 2020 Olympic Games c. Result of E-Votes i) Bylaws of WT Hall of Fame ii) Regulations on the Administration of WT Educators iii) Regulations on the Administration of WT International Coaches iv) Disciplinary Actions and Appeals Code d. Membership i) Approval of new membership – Faroe Islands ii) Membership Category e. Online Education System f. GMS Update g. Committee Reports i) MRD Commission ii) Education Committee iii) Development Committee iv) Taekwondo for All Committee Meeting Minutes | World Taekwondo Extraordinary Council Meeting | December 5, 2019 | Moscow, Russia Page 1 / 20 v) Para Taekwondo Committee 8. Other Matters a. 20th Commemoration of Olympic Games b. 2023 World Taekwondo Festival c. Grand Prix Challenge d. Guidelines on usage of WT IP by members e. Other Items 9. Selection of the Host Cities a. -

Draft Agenda

AGENDA THE 2019 MOSCOW NONPROLIFERATION CONFERENCE November 7–9, 2019 DAY 1: Thursday, November 7, 2019 19.00–21.00. Reception House of the Ministry of Foreign Affairs (Spiridonovka Street, 17) RECEPTION FOR SPEAKERS, AMBASSADORS AND OUT-OF-MOSCOW PARTICIPANTS DAY 2: Friday, November 8, 2019 07.45–08.45. Lotte Hotel Moscow, Crystal Ballroom Foyer (Novinsky blvd., 8, bldg. 2) REGISTRATION. WELCOME COFFEE 08.45–09.00. Crystal Ballroom OPENING REMARKS Anton KHLOPKOV, Director, Center for Energy and Security Studies (CENESS); Chair, The 2019 Moscow Nonproliferation Conference, Russian Federation 09.00–10.30. Crystal Ballroom PLENARY SESSION I: What is the Future of the Nonproliferation Regime and Arms Control? Sergey RYABKOV, Deputy Minister of Foreign Affairs, Russian Federation FU Cong, Director General, Department of Arms Control and Disarmament, Ministry of Foreign Affairs, China Izumi NAKAMITSU, Under-Secretary-General, High Representative for Disarmament Affairs, United Nations Chair (for all plenary sessions): Anton KHLOPKOV, Director, Center for Energy and Security Studies (CENESS); Chair, The 2019 Moscow Nonproliferation Conference, Russian Federation 10.30–11.00. COFFEE BREAK 11.00–12.00. Crystal Ballroom KEYNOTE ADDRESS. The Priorities of Russia’s Policy in the Field of Arms Control and Nonproliferation at a Time of Changes in the Global Security Architecture Sergey LAVROV, Minister of Foreign Affairs, Russian Federation 12.00–12.15. TECHNICAL BREAK 1 12.15–13.30. Crystal Ballroom PLENARY SESSION II. The 1995 NPT Review and -

Lighting Designed

DESIGNEDARCHITECTURAL LIGHTING Major Commercial Projects The Point, Paddington, London Citibank, Canary Wharf Thomas Tallis School, Kidbrook, London The Shard, London New Street Square, London Standard Life, London DMS Watson Building, University London Bridge Tower Broadgate Development, City of Lazards Bank, London College London 1, Threadneedle Street, City of London London Bank of England, City of London University of Westminster, Wells Street Campus, London. 23, Bloomsbury Square, London Little Britain, City of London BZW, Canary Wharf Senate House, University of London 25, Cannon Street, City of London Thames Court, City of London Bank of England Settlement’s Office, Paternoster Square, City of London City of London The Cloisters, University College 3-10, Finsbury Square, City of London London Cazenove, City of London Lloyds Registry, London Gazprom, 33, Kingsway, London University College London Library J Sainsbury Headquarters, London Bank of England Guilt’s Office, City of 5, Golden Square, London King Solomon Academy, London Deloitte Touche, City of London London 6, Bevis Marks, City of London Queen Mary University, London Mid City Place, London Bank of England Conference Rooms, 62, Buckingham Gate, London City of London Imperial College London Blossom Inn, London Abbot House, Reading GNI Bank, London Anatomy Building, University College Tower A, Baku, Azerbaijan Glaxo Smithkline European London Headquarters, London Kleinwort Benson, London Tower B, Baku, Azerbaijan Chelsea College of Art and Design, Orange Headquarters, London -

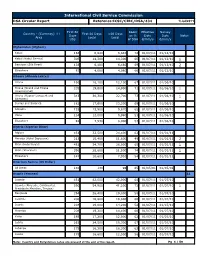

International Civil Service Commission DSA Circular Report Reference:ICSC/CIRC/DSA/442 1/Mar/2012

International Civil Service Commission DSA Circular Report Reference:ICSC/CIRC/DSA/442 1/Mar/2012 Chairman Kingston P. Rhodes ,,QWURGXFWLRQ ,,QWURGXFWLRQ ,,'HVFULSWLRQRI'6$GDWDIRUPDW ,,'HVFULSWLRQGHVGRQQpHVUHODWLYHVjO LQGHPQLWpMRXUQDOLqUHGHVXEVLVWDQFH ,,1752'8&7,21 $FRQVROLGDWHGOLVWRI'DLO\6XEVLVWHQFH$OORZDQFH '6$ UDWHVLVSURPXOJDWHGRQDPRQWKO\EDVLVE\WKH&KDLUPDQRI WKH,QWHUQDWLRQDO&LYLO6HUYLFH&RPPLVVLRQ ,&6& 7KLVLVDQDOORZDQFHZKLFKLVLQWHQGHGWRDFFRXQWIRUORGJLQJ PHDOVJUDWXLWLHVDQGRWKHUH[SHQVHVRI8QLWHG1DWLRQVWUDYHOOHUV 7KH'6$UDWHVDUHHVWDEOLVKHGRQWKHEDVLVRIGDWDVXSSOLHGE\GHVLJQDWHGDJHQFLHVIRUGXW\VWDWLRQVDURXQGWKH ZRUOG7KHUDWHVDUHLQWHQGHGWRUHODWHWRJRRGFRPPHUFLDOKRWHOVDQGUHVWDXUDQWV$QDGGLWLRQDODPRXQWRISHU FHQW RIWKHDYHUDJHKRWHODQGPHDOFRVW LVLQFOXGHGLQWKH'6$UDWHWRDFFRXQWIRULQFLGHQWDOH[SHQVHV WLSV ODXQGU\WRLOHWULHVHWF '6$UDWHVJHQHUDOO\UHODWHWRVSHFLILFORFDWLRQV SULPDULO\FLWLHV ZLWKLQDFRXQWU\$Q HOVHZKHUHUDWHLVDOVRJHQHUDOO\SURYLGHGWRHQFRPSDVVDOOUHPDLQLQJDUHDVRIDFRXQWU\7KHVWDQGDUG'6$UDWHV DUHGHVLJQHGIRUVWDIILQOHYHOV3DQGEHORZ2IILFLDOVLQOHYHOV'DQGDERYHUHFHLYHHLWKHUDRUSHUFHQW VXSSOHPHQW GHSHQGLQJRQOHYHO WRWKHVWDQGDUG'6$UDWH ,,'(6&5,37,212)'6$'$7$)250$7 1DPHRIFRXQWU\RUDUHDDQGFXUUHQF\ &ROXPQ 1DPHRIFRXQWU\RUDUHDDQGWKHFXUUHQF\XVHGDSSHDULQWKLVFROXPQ '6$UDWHIRUWKHILUVWGD\VLQ8QLWHG6WDWHVGROODUV &ROXPQ 7KH'6$UDWHSHUGD\LQ8QLWHG6WDWHVGROODUVLVOLVWHGLQWKLVFROXPQ '6$UDWHIRUWKHILUVWGD\VLQORFDOFXUUHQF\ &ROXPQ 7KH'6$UDWHSHUGD\LQORFDOFXUUHQF\LVOLVWHGLQWKLVFROXPQ '6$UDWHSD\DEOHDIWHUGD\VLQORFDOFXUUHQF\ &ROXPQ 7KH'6$UDWHSHUGD\LQWKLVFROXPQUHSUHVHQWVWKHUDWHSDLGIRUDVWD\LQWKHFLW\RUDUHDEH\RQGGD\V -

International Civil Service Commission DSA Circular Report Reference:ICSC/CIRC/DSA/434 1/Jul/2011

International Civil Service Commission DSA Circular Report Reference:ICSC/CIRC/DSA/434 1/Jul/2011 First 60 Room Effective Survey Country - (Currency) First 60 Days >60 Days Days as % Date Date Notes Area Local Local US$ of DSA d/mm/y d/mm/y Afghanistan (Afghani) Kabul 184 8,640 8,640 74 01/07/11 01/12/10 Kabul (Kabul Serena) 305 14,300 14,300 65 01/07/11 01/12/10 1 Bamiyan (Silk Road) 138 6,480 6,480 69 01/07/11 01/12/10 2 Elsewhere 87 4,080 4,080 66 01/07/11 01/12/10 Albania (Albania Lek(e)) Tirana 166 16,100 12,100 67 01/07/11 01/06/10 Tirana (Grand and Tirana 205 19,800 14,900 71 01/07/11 01/06/10 1 International) Tirana (Rogner Europark and 313 30,300 22,700 73 01/07/11 01/06/10 1 Sheraton) Durres and Saranda 182 17,600 13,200 69 01/07/11 01/06/10 Shkodra 133 12,900 9,670 62 01/07/11 01/06/10 Vlore 124 12,000 8,990 53 01/07/11 01/06/10 Elsewhere 82 7,930 6,000 53 01/07/11 01/06/10 Algeria (Algerian Dinar) Algiers 451 32,500 24,400 62 01/07/11 01/01/11 Annaba (Hotel Seybouse) 213 15,400 11,600 49 01/07/11 01/01/11 2 Oran (Hotel Royal) 481 34,700 26,000 65 01/07/11 01/01/11 1 Oran (Sheraton) 396 28,600 21,500 74 01/07/11 01/01/11 1 Elsewhere 147 10,600 7,950 54 01/07/11 01/01/11 American Samoa (US Dollar) All Areas 130 130 98 65 01/05/01 01/05/01 Angola (Kwanza) 11 Luanda 451 42,000 42,000 68 01/07/11 01/07/10 Luanda (Alvalade, Continental, 590 54,900 41,200 72 01/07/11 01/07/10 1 Presidente Meridien, Tropico) Benguela 284 26,400 19,800 58 01/07/11 01/07/10 Cabinda 200 18,600 18,600 60 01/07/11 01/07/10 Dundu 204 19,000 14,200 52 01/07/11 01/07/10 Huambo 206 19,200 14,400 60 01/07/11 01/07/10 Kuito 185 17,200 12,900 62 01/07/11 01/07/10 Lobito 263 24,500 18,300 67 01/07/11 01/07/10 Lubango 175 16,300 16,300 63 01/07/11 01/07/10 Luena 178 16,600 12,500 56 01/07/11 01/07/10 Note: Country and Dutystation notes are present at the end of the report. -

For the Decidedly Unordinary ______

For the Decidedly Unordinary ______________ The Leading Hotels of the World is a collection of authentic and uncommon luxury hotels. Comprised of more than 400 hotels in over 80 countries, our hotels embody the very essence of their destinations. Offering varied styles of architecture and design, and immersive cultural experiences delivered by passionate people, our collection is curated for the curious traveler in search of their next discovery. February 2021 AFRICA Tokyo CENTRAL AMERICA The Milestone Hotel & Residences Imperial Hotel, Tokyo Mauritius Costa Rica The Ritz London Palace Hotel Tokyo Manchester Constance Prince Maurice Nayara Tented Camp The Okura Tokyo The Lowry Hotel Maradiva Villas Resort & Spa Panama Royal Palm Beachcomber Luxury Yokohama Estonia The Kahala Hotel & Resort Panama City Morocco Bristol Panama Tallinn La Mamounia Korea Schlössle Hotel Royal Mansour Marrakech Seoul EUROPE Finland Seychelles Signiel Seoul Andorra Helsinki The Shilla Seoul Constance Lémuria Soldeu Hotel Kämp South Africa Malaysia Sport Hotel Hermitage & Spa France Kuala Lumpur Cape Town Austria Beaulieu sur Mer The RuMa Hotel and Residences 12 Apostles Hotel & Spa Kitzbühel La Réserve de Beaulieu, Hôtel & Spa Langkawi Cape Grace Hotel Weisses Roessl Kitzbühel Cannes The Datai Langkawi Durban Salzburg Hôtel Barrière Le Majestic Cannes The Oyster Box Myanmar Hotel Sacher Salzburg Champillon Yangon George Telfs Royal Champagne Hotel & Spa The Strand Yangon The Manor House at Fancourt Interalpen-Hotel Tyrol Cognac Republic of Maldives Johannesburg -

2. Lotte Hotel Seoul ★★★★★

1. LOTTE Group Affiliates Introduction 79 affiliates (sister companies) Petrochemical- Tourism- Foods Distribution Construction- Finance Services 10% 37% Manufacturing 5% 16% 32% 1. LOTTE Group Affiliates Introduction Total sales of Lotte Confectionery’s Xylitol chewing gum since its launch in May 2000 to early May 2011 1,300,000 [unit: million won] Number of domestic Lotteria restaurants as of early May 2011 933 Number of overseas Lotteria restaurants as of early May 2011 112 Number of domestic Angel-in-us coffee shops as of early May 2011 . LOTTE CONFECTIONERY . LOTTE CHILSUNG BEVERAGE 419 . LOTTE LIQUOR BG . LOTTE ASAHI LIQUOR . LOTTE SAMKANG Number of overseas Angel-in-us coffee shops . LOTTERIA / T.G.I. FRIDAY’S / ANGEL-IN-US as of early May 2011 . KRISPY KREME DOUGHNUTS . LOTTE HAM . LOTTE FRESH DELICA 12 . LOTTE BOULANGERIE . LOTTE PHARMACEUTICAL . WELLGA . LOTTE MERCHANDISING SERVICE CENTER 1. LOTTE Group Affiliates Introduction Number of Lotte department stores as of early May 2011 [including 2 overseas stores] 38 Number of Overseas Lotte Mart stores as of early March 2011 105 Number of Lotte Super stores as of early May 2011 306 . LOTTE DEPARTMENT STORE . LOTTE MART Number of Lotte Cinema theaters . LOTTE SUPER as of early May 2011 . LOTTE CINEMA · LOTTE ENTERTAINMENT . LOTTE.COM . LOTTE HOME SHOPPING 75 . KOREA SEVEN . FRL KOREA Number of 7-Eleven stores as of April-end 2011 3,240 1. LOTTE Group Affiliates Introduction Lotte World’s cumulative number of visitors as of early May 2011 120,000,000 Construction cost of the Second Lotte World Project plans to finish construction by 2014 2 trillion won .