Technical Report Number 52 Bering-Norton Petroleum Development Sce~Arios Transportation Systems Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Aviation Advisory Board Meeting Minutes August 5-6, 2010 in Unalakleet, Alaska

Aviation Advisory Board Meeting Minutes August 5-6, 2010 in Unalakleet, Alaska Chairman Lee Ryan called meeting to order at 9:05am. PRESENT: Lee Ryan, Jim Dodson, Tom George, Tom Nicolos, Mike Salazar, Mike Stedman, Judy McKenzie, Frank Neitz, Steve Strait EXCUSED ABSENCE: Al Orot, Ken Lythgoe OTHERS IN ATTENDANCE: Marc Luiken (DOT&PF), Rebecca Cronkhite (DOT&PF), Jeff Roach (DOT&PF), Linda Bustamante (DOT&PF), Commissioner Leo von Scheben (DOT&PF), Harry Johnson, Jr. - Unalakleet Airport Manager, Laura Lawrence – Staff to Senator Donny Olson, Representative Neal Foster, Chuck Degnan, Jim Tweto. MINUTES: Approved by the board prior to meeting – via email. Agenda Addition – Add time for public comments to agenda which could happen throughout the day as the public stops in for the meeting. Announcement from Deputy Commissioner: Deputy Commissioner Luiken thanked Chairman Lee Ryan for hosting the meeting in Unalakleet and welcomed new board members, Tom Nicolos and Mike Stedman. AGENDA: Alaska International Airports System (AIAS) and Statewide Aviation Update: Deputy Commissioner Luiken provided an overview of the AIAS. Marketing efforts of the Anchorage Airport include: 1. Plans to hire two key positions - marketing and air service development. 2. Interview with Supply Chain Management for an online story 3. Air Cargo Summit – International carriers invited to meet with representative from U.S. DOT to better understand the unique cargo transfer rights available in Alaska and to review fuel supply issues. The State is conducting a study to review fuel storage and all aspects of fuel availability at the international airports. Public Comment: Junior Johnson, Unalakleet Airport Manager expressed concern over Emmonak Airport not having a village contractor. -

Notice of Adjustments to Service Obligations

Served: May 12, 2020 UNITED STATES OF AMERICA DEPARTMENT OF TRANSPORTATION OFFICE OF THE SECRETARY WASHINGTON, D.C. CONTINUATION OF CERTAIN AIR SERVICE PURSUANT TO PUBLIC LAW NO. 116-136 §§ 4005 AND 4114(b) Docket DOT-OST-2020-0037 NOTICE OF ADJUSTMENTS TO SERVICE OBLIGATIONS Summary By this notice, the U.S. Department of Transportation (the Department) announces an opportunity for incremental adjustments to service obligations under Order 2020-4-2, issued April 7, 2020, in light of ongoing challenges faced by U.S. airlines due to the Coronavirus (COVID-19) public health emergency. With this notice as the initial step, the Department will use a systematic process to allow covered carriers1 to reduce the number of points they must serve as a proportion of their total service obligation, subject to certain restrictions explained below.2 Covered carriers must submit prioritized lists of points to which they wish to suspend service no later than 5:00 PM (EDT), May 18, 2020. DOT will adjudicate these requests simultaneously and publish its tentative decisions for public comment before finalizing the point exemptions. As explained further below, every community that was served by a covered carrier prior to March 1, 2020, will continue to receive service from at least one covered carrier. The exemption process in Order 2020-4-2 will continue to be available to air carriers to address other facts and circumstances. Background On March 27, 2020, the President signed the Coronavirus Aid, Recovery, and Economic Security Act (the CARES Act) into law. Sections 4005 and 4114(b) of the CARES Act authorize the Secretary to require, “to the extent reasonable and practicable,” an air carrier receiving financial assistance under the Act to maintain scheduled air transportation service as the Secretary deems necessary to ensure services to any point served by that air carrier before March 1, 2020. -

Invitation to Bid Invitation Number 2519H037

INVITATION TO BID INVITATION NUMBER 2519H037 RETURN THIS BID TO THE ISSUING OFFICE AT: Department of Transportation & Public Facilities Statewide Contracting & Procurement P.O. Box 112500 (3132 Channel Drive, Suite 350) Juneau, Alaska 99811-2500 THIS IS NOT AN ORDER DATE ITB ISSUED: January 24, 2019 ITB TITLE: De-icing Chemicals SEALED BIDS MUST BE SUBMITTED TO THE STATEWIDE CONTRACTING AND PROCUREMENT OFFICE AND MUST BE TIME AND DATE STAMPED BY THE PURCHASING SECTION PRIOR TO 2:00 PM (ALASKA TIME) ON FEBRUARY 14, 2019 AT WHICH TIME THEY WILL BE PUBLICLY OPENED. DELIVERY LOCATION: See the “Bid Schedule” DELIVERY DATE: See the “Bid Schedule” F.O.B. POINT: FINAL DESTINATION IMPORTANT NOTICE: If you received this solicitation from the State’s “Online Public Notice” web site, you must register with the Procurement Officer listed on this document to receive subsequent amendments. Failure to contact the Procurement Officer may result in the rejection of your offer. BIDDER'S NOTICE: By signature on this form, the bidder certifies that: (1) the bidder has a valid Alaska business license, or will obtain one prior to award of any contract resulting from this ITB. If the bidder possesses a valid Alaska business license, the license number must be written below or one of the following forms of evidence must be submitted with the bid: • a canceled check for the business license fee; • a copy of the business license application with a receipt date stamp from the State's business license office; • a receipt from the State’s business license office for -

DOTPF Alaskan Airports, AIP, APEB

Northern Region Airport Overview -------------------------------------------- DOT&PF Town Hall Meeting October 22, 2010 Jeff Roach, Aviation Planner Northern Region, DOT&PF Topics • Northern Region Airports • Northern Region Aviation Sections • Aviation Funding • Types of Projects • Anticipated Future Funding Levels • Anticipated Northern Region Projects Northern Region 105 Airports 40% of the State’s airports are in the Northern Region • One International Airport • Seaplane Bases • Community Airports • Public, Locally Owned Airports Northern Region Aviation Organization • Planning • Design • Construction • Airport Leasing • Maintenance and Operations (M&O) Aviation Planning • Identify project needs, develops project packages for APEB scoring • Develop project scopes • Conduct airport master plans Project Needs Identification Rural Airports Needs List Development Project needs collected from: • Public, aviation interests, community representatives, DOT&PF and FAA staff, Legislature • DOT&PF Staff (Design, M&O, Leasing) • Needs identified in airport master plans • Regional transportation plans Project Scoping: DOT&PF Regional staff evaluate potential projects to develop preliminary project scope, cost estimate and other supporting information for APEB project evaluation State AIP Project Scoring (APEB) Aviation Project Evaluation Board (APEB): • The APEB is a six-member airport capital project review and evaluation group composed of DOT&PF’s Deputy Commissioner, three Regional Directors (SE, CR, NR), Statewide Planning Director, and State -

Bering Sea – Western Interior Alaska Resource Management Plan and Environmental Impact Statement

Bibliography: Bering Sea – Western Interior In support of: Bering Sea – Western Interior Alaska Resource Management Plan and Environmental Impact Statement Principal Investigator: Juli Braund-Allen Prepared by: Dan Fleming Alaska Resources Library and Information Services 3211 Providence Drive Library, Suite 111 Anchorage, Alaska 99508 Prepared for: Bureau of Land Management Anchorage Field Office 4700 BLM Road Anchorage, AK 99507 September 1, 2008 Bibliography: Bering Sea – Western Interior In Author Format In Support of: Bering Sea – Western Interior Resource Management Plan and Environmental Impact Statement Prepared by: Alaska Resources Library and Information Services September 1, 2008 A.W. Murfitt Company, and Bethel (Alaska). 1984. Summary report : Bethel Drainage management plan, Bethel, Alaska, Project No 84-060.02. Anchorage, Alaska: The Company. A.W. Murfitt Company, Bethel (Alaska), Delta Surveying, and Hydrocon Inc. 1984. Final report : Bethel drainage management plan, Bethel, Alaska, Project No. 83-060.01, Bethel drainage management plan. Anchorage, Alaska: The Company. Aamodt, Paul L., Sue Israel Jacobsen, and Dwight E. Hill. 1979. Uranium hydrogeochemical and stream sediment reconnaissance of the McGrath and Talkeetna NTMS quadrangles, Alaska, including concentrations of forty-three additional elements, GJBX 123(79). Los Alamos, N.M.: Los Alamos Scientific Laboratory of the University of California. Abromaitis, Grace Elizabeth. 2000. A retrospective assessment of primary productivity on the Bering and Chukchi Sea shelves using stable isotope ratios in seabirds. Thesis (M.S.), University of Alaska Fairbanks. Ackerman, Robert E. 1979. Southwestern Alaska Archeological survey 1978 : Akhlun - Eek Mountains region. Pullman, Wash.: Arctic Research Section, Laboratory of Anthropology, Washington State University. ———. 1980. Southwestern Alaska archeological survey, Kagati Lake, Kisarilik-Kwethluk Rivers : a final research report to the National Geographic Society. -

Final Documents/Your Two Cents—August 2018

Final Documents/Your Two Cents—August 2018 This list includes Federal Register (FR) publications such as rules, Advisory Circulars (ACs), policy statements and related material of interest to ARSA members. The date shown is the date of FR publication or other official release. Proposals opened for public comment represent your chance to provide input on rules and policies that will affect you. Agencies must provide the public notice and an opportunity for comment before their rules or policies change. Your input matters. Comments should be received before the indicated due date; however, agencies often consider comments they receive before drafting of the final document begins. Hyperlinks provided in blue text take you to the full document. If this link is broken, go to http://www.regulation.gov. In the keyword or ID field, type “FAA” followed by the docket number. August 1, 2018 FAA Final rules Rule: Amendment of Class D Airspace; Erie, PA Published 08/01/2018 Docket #: FAA-2018-0679 Effective date 08/01/2018 This action amends the legal description of the Class D airspace at Erie International Airport/Tom Ridge Field, Erie, PA, by correcting a printing error in the latitude coordinate symbols for the airport. This action does not affect the boundaries or operating requirements of the airspace. Final Rule: Amendment of Class E Airspace; Lyons, KS Published 08/01/2018 Docket #: FAA-2018-0139 Effective date 11/08/2018 This action modifies Class E airspace extending upward from 700 feet above the surface, at Lyons- Rice Municipal Airport, Lyons, KS. This action is necessary due to the decommissioning of the Lyons non-directional radio beacon (NDB), and cancellation of the NDB approach, and would enhance the safety and management of standard instrument approach procedures for instrument flight rules (IFR) operations at this airport. -

IAWG Recommendations to the Governor's

IMMEDIATE ACTION WORKGROUP RECOMMENDATIONS TO THE GOVERNOR’S SUBCABINET ON CLIMATE CHANGE MARCH 2009 THIS PAGE IS INTENTIONALLY BLANK Commissioner Hartig and Members of the Governor’s Subcabinet on Climate Change: The Immediate Action Workgroup (IAWG) is pleased to provide its recommendations regarding the actions and policies that we believe should be implemented in 2009 and 2010. This is the second report provided to the Climate Change Subcabinet and follows up on recommendations and actions taken as a result of our April 17, 2008 report to the Subcabinet. The IAWG has continued at the request of Commissioner Hartig, chairman of the Climate Change Subcabinet, to collaboratively examine the needs of communities that are under imminent threat from conditions that may be attributed to climate change phenomena. The membership of the Immediate Action Workgroup has remained consistent from the previous year with one exception. Added to the IAWG is a representative from the National Oceanic and Atmospheric Administration, Amy Holman, Lead for NOAA’s Alaska Regional Collaboration Team. Her participation has contributed greatly to our understanding of the data and research that is needed in the near future. The IAWG would likely benefit from additional agency participation. The spirit of cooperation and serious collaboration has infused our meetings and we believe resulted in meritorious recommendations for near-term actions by the Subcabinet and the State of Alaska. Last year we described our recommendations in terms of a recipe for success. The members and others participating with the Immediate Action Workgroup have now worked together for over a year, both directly on the Immediate Action Workgroup’s tasks and on leveraging resources and ideas resulting from the Workgroup’s collaboration. -

Federal Register/Vol. 83, No. 149/Thursday, August 2, 2018

37776 Federal Register / Vol. 83, No. 149 / Thursday, August 2, 2018 / Proposed Rules Points, dated August 3, 2017, and Issued in Seattle, Washington, on July 25, Avenue SW, Washington, DC 20591; effective September 15, 2017, is 2018. telephone: (202) 267–8783. The Order is amended as follows: Shawn M. Kozica, also available for inspection at the Group Manager, Operations Support Group, National Archives and Records Paragraph 6005 Class E Airspace Areas Western Service Center. Extending Upward From 700 Feet or More Administration (NARA). For Above the Surface of the Earth. [FR Doc. 2018–16482 Filed 8–1–18; 8:45 am] information on the availability of FAA Order 7400.11B at NARA, call 202–741– * * * * * BILLING CODE 4910–13–P 6030, or go to https://www.archives.gov/ AAL AK E5 Barrow, AK [Amended] federal-register/cfr/ibr-locations.html. Wiley Post/Will Rogers Memorial Airport, DEPARTMENT OF TRANSPORTATION FAA Order 7400.11, Airspace AK Designations and Reporting Points, is (Lat. 71°17′06″ N, long. 156°46′07″ W) Federal Aviation Administration published yearly and effective on September 15. That airspace extending upward from 700 14 CFR Part 71 feet above the surface within a 6.6-mile FOR FURTHER INFORMATION CONTACT: radius of the Wiley Post/Will Rogers [Docket No. FAA–2017–0348; Airspace Richard Roberts, Federal Aviation Memorial Airport; and that airspace Docket No. 17–AAL–4] Administration, Operations Support extending upward from 1,200 feet above the RIN–2120–AA66 Group, Western Service Center, 2200 S. surface within a 73-mile radius of the Wiley 216th St., Des Moines, WA, 98198– Post/Will Rogers Memorial Airport, Proposed Modification of Class E 6547; telephone (206) 231–2245. -

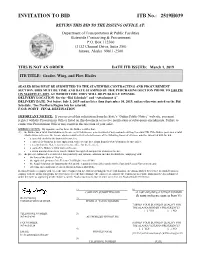

ITB No. 2519H039 Grader, Wing & Plow Blades.Pdf

INVITATION TO BID ITB No.: 2519H039 RETURN THIS BID TO THE ISSUING OFFICE AT: Department of Transportation & Public Facilities Statewide Contracting & Procurement P.O. Box 112500 (3132 Channel Drive, Suite 350) Juneau, Alaska 99811-2500 THIS IS NOT AN ORDER DATE ITB ISSUED: March 1, 2019 ITB TITLE: Grader, Wing, and Plow Blades SEALED BIDS MUST BE SUBMITTED TO THE STATEWIDE CONTRACTING AND PROCUREMENT SECTION. BIDS MUST BE TIME AND DATE STAMPED BY THE PURCHASING SECTION PRIOR TO 2:00 PM ON MARCH 27, 2019, AT WHICH TIME THEY WILL BE PUBLICLY OPENED. DELIVERY LOCATION: See the “Bid Schedule” and “Attachment A”. DELIVERY DATE: Not before July 1, 2019 and no later than September 30, 2019, unless otherwise noted on the Bid Schedule. *See Northern Region lots for asterisk. F.O.B. POINT: FINAL DESTINATION IMPORTANT NOTICE: If you received this solicitation from the State’s “Online Public Notice” web site, you must register with the Procurement Officer listed on this document to receive notification of subsequent amendments. Failure to contact the Procurement Officer may result in the rejection of your offer. BIDDER'S NOTICE: By signature on this form, the Bidder certifies that: (1) the Bidder has a valid Alaska business license, or will obtain one prior to award of any contract resulting from this ITB. If the Bidder possesses a valid Alaska business license, the license number must be written below or one of the following forms of evidence must be submitted with the bid: • a canceled check for the business license fee; • a copy of the business -

Where Are Laanc Facilities in My Area?

WHERE ARE LAANC FACILITIES IN MY AREA? Updated with LAANC Expansion Facilities! December 2019 Houston Air Route Traffic Control Center (ZHU) Brownsville/South Padre Island International Airport (BRO), Mobile Regional Airport (MOB), Salina Regional Airport (SLN), South Central Brownsville, TX Mobile, AL Salina, KS Easterwood Field (CLL), Baton Rouge Metropolitan Airport (BTR), Philip Billard Municipal Airport (TOP), College Station, TX Baton Rouge, LA Topeka, KS Conroe-North Houston Regional Airport (CXO), Lafayette Regional Airport (LFT), Mount Vernon Airport (MVN), Houston, TX Lafayette, LA Mt Vernon, IL Scholes International At Galveston Airport (GLS), Austin–Bergstrom International Airport (AUS), Quincy Regional Airport (UIN), Galveston, TX Austin, TX Quincy, IL Georgetown Municipal Airport (GTU), Corpus Christi International Airport (CRP), Chanute Martin Johnson Airport (CNU), Georgetown, TX Corpus Christi, TX Chanute, KS Valley International Airport (HRL), Aransas County Airport (RKP), Dodge City Regional Airport (DDC), Harlingen, TX Rockport, TX Dodge City, KS San Marcos Regional Airport (HYI), San Antonio International Airport (SAT), Emporia Municipal Airport (EMP), Austin, TX San Antonio, TX Emporia, KS Laredo International Airport (LRD), Louis Armstrong New Orleans International Airport (MSY), Hays Regional Airport (HYS), Laredo, TX Kenner, LA St, Hays, KS McAllen Miller International Airport (MFE), William P. Hobby Airport (HOU), Lawrence Municipal Airport (LWC), McAllen, TX Houston, TX Lawrence, KS Sugar Land Regional Airport -

06-'12, Rural Airports AIP Spending Plan October 20, 2010 DOT/PF, Statewide Aviation

Draft FFY '06-'12, Rural Airports AIP Spending Plan October 20, 2010 DOT/PF, Statewide Aviation APEB LOCID Project Score Ph FFY'06 FFY'07 FFY'08 FFY'09 FFY'10 FFY'11 FFY'12 After FFY'12 Rural Primary Airports Primary Airfield Projects ANI Aniak Airport Improvements 130 2,3,4 $ 4,700,000 BRW Barrow Apron Expansion 88 2,4 $ 7,000,000 BRW Barrow RWY-Apron Paving/ SA Expan-Stg 3 124 2,4$ 3,000,000 BRW Barrow RWY-Apron Paving/ SA Expan-Stg 4 124 2,4 $ 7,200,000 Bethel Parallel RWY and Other Improv--Stg 2 BET (GA Apron Expansion) 130 2,4$ 5,701,583 Bethel Parallel RWY and Other Improv--Stg 3 (Parallel Runway Gravel Surface and BET Lighting) 160 2,4$ 2,733,217 Bethel Parallel RWY and Other Improv--Stg 4 (Parallel Runway Gravel Surface and BET Lighting) 160 2,4$ 5,877,983 Bethel Parallel RWY and Other Improv--Stg 5 BET (Parallel Runway Paving) 160 2,4$ 3,277,634 Bethel Parallel RWY and Other Improv--Stg 6 BET (ROW) 130 2,4 $ 1,650,000 BET Bethel West Heavy Apron Expansion 101 2,4 $ 4,000,000 Bethel Airport RWY / TWY / Commerical BET Apron Pavement Rehabilitation (C) N/A 2,4 $ 13,000,000 Bethel Airport RWY / TWY / Commerical BET Apron Pavement Rehabilitation N/A 2,4 $ 13,000,000 BET Bethel South GA Apron Reconstruction (C) N/A 2,4 $ 4,700,000 BET Bethel South GAApron Reconstruction N/A 2,4 $ 4,700,000 CDV Cordova Apt Apron, TWY & GA Imp Stg 1 113 2,4$ 4,499,980 CDV Cordova Apt Apron, TWY & GA Imp Stg 2 113 2,4 $ 8,500,000 CDV Cordova Apt Apron, TWY & GA Imp Stg 2 (C) 113 2,4 $ 8,500,000 CDV Cordova Apt Apron, TWY & GA Imp Stg 3 113 2,4 $ 6,700,000 CDV Cordova Apt RSA Expan - Stg 2 N/A 2,4$ 4,346,424 CDV Cordova Apt RSA Improvements (Paving) 65 2,4$ 650,000 Note: Spending Plan contains entitlement and discretionary funded projects. -

Federal Register/Vol. 84, No. 30/Wednesday, February 13, 2019

Federal Register / Vol. 84, No. 30 / Wednesday, February 13, 2019 / Rules and Regulations 3677 Regulatory Notices and Analyses ANM WA E2 Ephrata, WA [Amended] 7400.11 and publication of conforming The FAA has determined that this Ephrata Municipal Airport, WA amendments. ° ′ ″ ° ′ ″ regulation only involves an established (Lat. 47 18 29 N, long. 119 31 01 W) ADDRESSES: FAA Order 7400.11C, body of technical regulations for which That airspace extending upward from the Airspace Designations and Reporting frequent and routine amendments are surface within a 4.2-mile radius of Ephrata Points, and subsequent amendments can necessary to keep them operationally Municipal Airport. This Class E airspace area be viewed online at http://www.faa.gov/ current, is non-controversial and is effective during specific dates and times air_traffic/publications/. For further established in advance by a Notice to information, you can contact the unlikely to result in adverse or negative Airmen. The effective date and time will comments. It, therefore: (1) Is not a thereafter be continuously published in the Airspace Policy Group, Federal Aviation ‘‘significant regulatory action’’ under Chart Supplement. Administration, 800 Independence Executive Order 12866; (2) is not a * * * * * Avenue SW, Washington, DC 20591; ‘‘significant rule’’ under DOT telephone: (202) 267–8783. The Order is Regulatory Policies and Procedures (44 ANM WA E5 Ephrata, WA [New] also available for inspection at the FR 11034; February 26, 1979); and (3) Ephrata Municipal Airport, WA National Archives and Records does not warrant preparation of a (Lat. 47°18′29″ N, long. 119°31′01″ W) Administration (NARA). For regulatory evaluation as the anticipated That airspace extending upward from 700 information on the availability of this impact is so minimal.