Sales Q1 2012 2013 VA Vdef

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GAZETKA PROMOCYJNA Oferta Promocyjna Ważna W Okresie14-30.11.2019 Lub Do Wyczerpania Zapasów I Jeśli Nie Wystąpił Błąd W Druku

GAZETKA PROMOCYJNA Oferta promocyjna ważna w okresie14-30.11.2019 lub do wyczerpania zapasów i jeśli nie wystąpił błąd w druku. Informacja handlowa dla przedsiębiorstw posiadających ważne zezwolenie na sprzedaż wyrobów alkoholowych. 17,89 netto 39,25 37,49 34,79 netto netto netto 22,75 31,19 22,75 31,19 netto netto netto netto 54,99 netto 54,99 54,99 82,59 139,99 netto netto netto netto 97 90 29 79 3 netto 3 netto 3 netto 2 netto 80 15 58 04 7 netto 7 netto 6 netto 6 netto 25 60 51 16netto 15netto 15netto 1,0 l 31,03 netto 0,1 l 0,2 l 0,5 l 0,7 l 0,2 l 0,5 l 0,7 l 3,90 6,82 14,65 21,59 7,80 17,31 24,38 netto netto netto netto netto netto netto 46,10 50,99 netto netto WHISKY 2799 6199 6859 6859 3599 3599 9900 500ml 700ml 700ml 700ml 700ml 700ml 700ml 3599 700ml 4599 1000ml BALLANTINE’S BALLANTINE’S BALLANTINE’S BALLANTINE’S 12YO BALLANTINE’S BALLANTINE’S ABERLOUR FINEST 12YO 12YO + KARTONIK + SZKLANKI BRASIL PASSION 12YO 49 79 68 74 7479 84 59 99 59 54 700ml 700ml 70 97 30 700ml 700ml 700ml 700ml 700ml CHIVAS CHIVAS REGAL CHIVAS REGAL CHIVAS REGAL THE GLENLIVET THE GLENLIVET PASSPORT REGAL 12YO 12YO + KARTONIK 12YO + SZKLANKI EXTRA + KARTONIK FOUNTER’S 12 YO RESERVE WHISKEY RUM LIKIER 3684 5309 cena 4249 4249 6159 2951 500ml 700ml u PH 700ml 700ml 700ml 500ml JAMESON JAMESON ORIGINAL JAMESON CRESTED HAVANA HAVANA CLUB HAVANA MALIBU ORIGINAL + MINIATURKI + KARTONIK CLUB 3YO ESPECIAL CLUB 7YO 94 59 31 42 ARARAT 500ml 700ml 4249 Pełna życia, dynamiczna 700ml brandy ARARAT „Three Stars” wniesie słonecz- ne ciepło do spotkania przy stole i umili każdą chwilę spędzoną z ro- dziną i przyjaciółmi na świeżym powietrzu, w podróży czy w domu. -

Marriot Menu-Cristal Bar-03.13.18

Breakfast Menu Great Room Menu Apricot French toast ..................................................................................................................................... 2000 Creamy Bircher muesli ................................................................................................................................. 1300 Breakfast burritos ........................................................................................................................................... 2200 Fried or scrambled eggs with bacon wrapped sausage .............................................................. 3000 Ham and cheese croissant .......................................................................................................................... 2600 Bacon and egg croissant ............................................................................................................................. 2600 Scrambled eggs with Basturma in a croissant ................................................................................. 2600 Egg benedict ..................................................................................................................................................... 2600 Granola, yogurt, mix berry compote .................................................................................................... 1300 Fruit salad ........................................................................................................................................................... 1800 Croissant, -

Bottled Beer Desserts Non Alcoholic Drinks Alcoholic

DESSERTS LVIV STYLE COFFEE ALCOHOLIC DRINKS WINE LIST SPARKLING WINES 150 ml 1пл Seasonal roulade 70 BITTERS 50 ml MADE IN A CEZVE, A TRADITIONAL GALICIAN METHOD Lambrusco dell'Emilia 420 Tiramisu 65 Kavivka (coee infused liquor) Italy, sweet / dry Lviv style coee / served with home-made liquor and lemon 65 28 Lviv cheese cake 60 Classic / Cream Lviv rainy day coee / with home-made 90 TM «SHABO» 370 Three chocolate cake 60 spirit and whipped cream semisweet, white Becherovka 65 Napoleon cake 72 Yuiry Kulchytskyy’s / with ginger, mint and citrus liqueur 70 TM «SHABO» 370 Becherovka Lemond 65 brut, white Ice cream with walnuts 60 Paradise delight / coee with coconut liqueur 85 and ice-cream Jägermeister 85 Drunk cherry cake 59 WHITE WINES Lviv style cappuccino 55 Xenta Absenta 90 Brownie with ice cream 75 Riesling Trocken.Dr.Loosen 98 490 EARL LYUBOMYRSKY'S COFFEE / coee with 75 Riga Black Cherry 80 Germany, dry Honey cake 59 rum liqueur Eastern style / coee with anise liqueur 70 VODKA 50 ml Tokaji Muskotaly.Chateau Dereszla 84 420 Hungary, semisweet Nemiro Original 37 FRESHLY HARVESTED COFFEE Nemiro De Luxe 43 ROSE WINES Nemiro Honey Pepper De Luxe 45 Rose d'Anjou 92 460 NONALCOHOLIC DRINKS Finlandia Vodka 57 France, semisweet Banderivska / with sweetened milk 45 Finlandia Cranberry 57 Morning coee / very strong black coee 42 RED WINES Ginger pomegranate tea 300 45 After meals coee / with brandy 60 WHISKEY 50 ml Chianti. Runo 100 500 Tea mint / berries / cranberry 300 45 Italy, dry Evening coee / with caramel and milk 52 Johnnie Walker Red Label 94 84 420 Tea black / green 300 Shiraz-Malbec. -

Ararat Brandy

ArArAt Brandy: Transforming a Legend into a Modern Icon 08/2014-5660 This case was written by Amitava Chattopadhyay, the GlaxoSmithKline Chaired Professor of Corporate Innovation at INSEAD and Fellow of the Institute on Asian Consumer Insight, and Vadim Grigorian, Marketing Director of Creativity and Luxury, Pernod Ricard. It is intended to be used as a basis for class discussion rather than to illustrate either effective or ineffective handling of an administrative situation. Additional material about INSEAD case studies (e.g., videos, spreadsheets, links) can be accessed at cases.insead.edu. Copyright © 2014 INSEAD COPIES MAY NOT BE MADE WITHOUT PERMISSION. NO PART OF THIS PUBLICATION MAY BE COPIED, STORED, TRANSMITTED, REPRODUCED OR DISTRIBUTED IN ANY FORM OR MEDIUM WHATSOEVER WITHOUT THE PERMISSION OF THE COPYRIGHT OWNER. Vadim Grigorian, Marketing Director for Pernod-Ricard Russia, was lost in thought in his office as a wintry sun failed to warm passers-by in the snow-covered Moscow streets below. He had a lot on his mind. What could he do to move the ArArAt brand to the next level? Currently the largest brand of brandy in Russia, with an enviable 32% market share and a long history, ArArAt was one of the jewels in Pernod Ricard Russia’s alcoholic beverage portfolio. After a recent product update, five key questions remained: 1. Which consumer segment(s) should ArArAt be targeted at? 2. What should be the ArArAt brand platform? 3. Which of the five advertising options before him (recent agency pitches for the ArArAt account) should he choose? 4. Should all seven sub-brands in the ArArAt portfolio feature in the campaign, or only some of them? If the latter, which ones should he select? 5. -

Russian Restaurant & Vodka Lounge M O SC O W

Moscow on the hill Russian Restaurant & Vodka Lounge V o d k a Russians do not consider their meal complete without vodka. It is never sipped: it should be swallowed in one gulp. The custom of drinking neat in cold countries was probably designed for this purpose for it not only thaws out those who travelled through the snow, but breaks the social ice. House Infusions 5.00 * Referent Horseradish * Chateau Marusya (cherry) * Tiramisu * Caramel * Garlic & Dill * Pepper * Coffee * Cinnamon * * Listed Prices per shot *Russia* * USA * *Poland* Stoli Elit 10.00 Hangar One CA (assorted flavors) 8.00 Ultimat (assorted flavors) 8.00 Jewel of Russia 8.00 Skyy 90˚ CA 8.00 Alchemia (Ginger) 7.00 Imperia 8.00 Opulent MN 7.00 Alchemia (Wild Cherry, Chocolate) 7.00 Youri Dolgoruki 8.00 Yazi OR (Ginger) 7.00 Chopin (Potato) 6.00 Stoli Gold 7.00 Shakers MN 6.00 Belvedere (assorted flavors) 6.00 Cristall 7.00 Roth CA 6.00 Sobieski 6.00 Russian Standard Platinum 7.00 Square 1 Cucumber ID (Rye) 6.00 Zubrowka (Bison Grass) 5.00 Russian Standard 6.00 45th Parallel WI (Corn) 6.00 Luksusowa (Potato) 5.00 White Gold 6.00 Jeremiah Weed Sweet Tea 5.00 Pravda 5.00 Stolichnaya (assorted flavors) 5.00 Rain (Organic) 5.00 Old Krupnik (Honey) 5.00 Ruskova 5.00 Tito TX 5.00 *Ukraine Tovarich 5.00 Teton Glacier ID (Potato) 5.00 Nemiroff 5.00 Blue Ice ID (Potato) 5.00 *Armenia* 3 Vodka FL (Soy) 5.00 *Estonia* Armyanskaya 6.00 Skyy CA 5.00 Tall Blonde 6.00 *England* Smirnoff 5.00 *France* Three Olives (assorted flavors) 5.00 *Holland* XO 9.00 Blavod 5.00 Vox (assorted flavors) -

Cafeteria Ice Cream Drinks and Soft Drinks

Cafeteria Espresso 1200 AMD Armenian coffee 1400 AMD Cappuccino 2000 AMD American coffee 1200 AMD Decaffeinated 1600 AMD Althaus Tea selection 1500 AMD Althaus Herbal Tea 2200 AMD Organic Armenia Tea 2000 AMD Ice coffee 1200 AMD Hot Chocolate 2000 AMD Latte Macchiato (milk with a dash of coffee) 1800 AMD Hot Milk 1200 AMD Ice Cream Cafè Glacè with ice cream 2500 AMD Vanilla, Chocolate, Nuts 600 AMD per scoop Fruit flavor 600 AMD per scoop Drinks and soft drinks S. Pellegrino Sparkling Water 75cl 2200 AMD Panna Still Water 75cl 2000 AMD Noy Still water 50cl 1000 AMD Bjni Sparkling water 50cl 1000 AMD Coca cola 1000 AMD Coca cola light 1000 AMD Sprite 1000 AMD Fanta 1000 AMD Althaus Ice tea 1500 AMD Red bull 3000 AMD Tonic water 1500 AMD Bottle of Juice 1200 AMD Fresh fruit juices Orange 2600 AMD Grapefruit 2600 AMD Blended Fruit and Vegetables Apple, ginger, carrot and lime 2600 AMD Kiwi and apple 2600 AMD Apple, Grapefruit and Carrot 2600 AMD Beers Kotayk 33cl 1400 AMD Alexandrapol 33cl 1900 AMD Gyumri 33cl 1400 AMD Kilikia 33cl 1400 AMD Heineken 33cl 3000 AMD Draft Beer 33cl 1200 AMD Draft Beer 50cl 1500 AMD Wines Glasses Takar white wine 3000AMD Karas red wine 3500AMD Takar red wine 3500AMD Takar Sparkling Brut 3500AMD Armenian brandy Ararat 5 years 3000 AMD Ararat Akhtamar 10 years 4500 AMD Ararat Nairi 20 years 9000 AMD Noy 10 years 3500 AMD Grappe Poli Aromatic 4000AMD Poli Dry 4000AMD International brandy Martell V.S. 4500 AMD Martell V.S.O.P. -

GARNISHES DESSERTS PIES SOUPS SAUCES 50 G on the PAN

SHARING STARTERS STARTERS PICKLES 100 g Lavash 2 pcs / 100 ₽ Ajapsandal with lavash 180/60 g / 390 ₽ Pickled cabbage / 180 ₽ Vegetables and herbs 300/50 g / 470 ₽ Lobio with lavash 220/60 g / 330 ₽ Gurian cabbage / 180 ₽ 150 g / ₽ Eggplant rolls 150/30 g / 390 ₽ Hummus 270 Salted tomatoes / light-salted / 180 ₽ Dolma with Beyond Meat 250/50 g / 590 ₽ Adyghe cheese, tomatoes Salted cucumbers / light-salted / 180 ₽ Dolma with lamb 200/100 g / 470 ₽ and tarragon sauce 190 g / 440 ₽ Pickled bamboo / 230 ₽ Caucasian style Lightly salted trout 100 g / 590 ₽ eggplant сarpaccio 200 g / 450 ₽ Mushrooms and herbs with oil / Local cheese 250 g / 490 ₽ sour cream / 250 ₽ Rapana with cream sauce 250 g / 610 ₽ Smalets with horseradish 200 g / 380 ₽ Herring with potatoes 200/150 g / 410 ₽ Hot pickled peppers / 220 ₽ Assorted lard 180/50 g / 450 ₽ Forshmak with toast Marinated garlic / 250 ₽ (salted, smoked, with layers of meat, mustard /horseradish) of Borodino bread 240 g / 350 ₽ Meat delicacy 150 g / 550 ₽ Satsivi with chicken 200 g / 370 ₽ (tongue, sujuk, basturma) Chicken liver pate SALADS with tangerines 140/100 g / 370 ₽ SOUPS Veal tail jelly 250 g / 390 ₽ Vinaigrette with khamsa 200 g / 310 ₽ Kharcho 350 g / 390 ₽ Assorted phali 120 g / 390 ₽ «Yalta» salad with tomatoes & cheese 240 g / 380 ₽ Borsch with garlic bun Dressed herring 230 g / 350 ₽ and sour cream 350/50 g / 380 ₽ The Black Sea fish soup 300 g / 390 ₽ Russian salad with veal tongue 200 g / 370 ₽ KHINKALI Homemade noodles soup 300 g / 330 ₽ Salad with persimmon and shrimp 250 g / 510 -

Liköre Vermouth

COCKTAIL SIGNATURE COCKTAILS GIRLS VIKTRING GIRL 8,5 Absolut Vodka, Campari, Zitrone, Erdbeeren, Chilli Agave, Palmzucker PASSION APEROL 8,5 Absolut Vodka, Aperol, Passionsfrucht, Prosecco RASPBERRY FIZZ 8,5 Absolut Vodka, Limettensaft, Himbeeren, Zucker, Soda, weisse Schokolade ROSATO MUSA 7 Ramazzotti Rosato, Vanillesirup, Apfelsaft PINKY BRAIN 8 Lillet Rosé, Absolut Vodka, Grapfruitsaft, Limettensaft, Bitter Lemon SIGNATURE COCKTAILS CLASSIC VESPER 8 Blue Gin, Absolut Vodka, Lillet rosé FIZZY TOUCH 14 Blue Gin, Zitrone, Hollunder, Orange Bitter, Perrier Jouet Champagner NEGRONI 8 Blue Gin, Antica Formula, Campari OLD FASHION 9 Four Roses Small Batch, Zuckerwürfel, Angostura Bitter MARTINI 9 Blue Gin /Absolut Elyx, Noilly Prat, Orange Bitter MOJITO 9 Havana 3y, Zucker, Limettensaft, Minze, Soda CAIPIRINHA 8,5 Janeiro Cachaca, Zucker, Limette JULEPS 9 Four Roses / Havana 3y / Ararat WeinbrandSpirituose, Minze, Zucker MOSCOW MULE 8,5 Absolut Vodka/London Buck (Gin)/Dark & Stormy (Jamaika Rum) Spirituose, Limettensaft, Ginger Beer, Gurke SIGNATURE COCKTAILS GENTLEMAN MARTINEZ 8 Gin oder Genever, Antica Formula, Marachino, Angostura Bitter EL PRESIDENTE 9 Havana 7y, trockener Vermouth, Orange Curacao, Grenadine 151TH SMOKEY 12 Chivas Regal, Lagavulin, Lagavulin spraye, Zitrone, Zucker, Eiweiss LE GURK 9 Absolut Elyx, Zitrone, Hollunder, Apfelsaft, Gurke MELON TANGO 8 Absolut Vodka, Melonenlikör, Grapefruitsaft, Gurke, Zitrone SOFT SPICY BERRY 6 frische Beeren, Agavennektar, Ingwerlimonade, Limettensaft SANTINO (ALKOHOLFREI) 6 Bitter Limonade, -

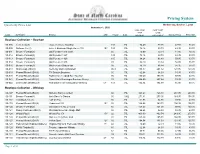

Pricing System

Pricing System Quarterly Price List Wednesday, October 7, 2020 November 1, 2020 CASE COST CASE COST LESS WITH MXB COST CODE SUPPLIER BRAND AGE PROOF SIZE BAILMENT SURCHARGE RETAIL PRICE Boutique Collection – Bourbon 00-005 Hello Cello(3) Hookers House Bourbon 100 .75L 74.40 77.05 47.65 51.40 00-009 Sazerac Co.(3) John J. Bowman Single Barrel 10Y 10Y 100 .75L 78.14 80.79 49.95 53.70 00-011 Brown - Forman(3) Old Forester 1870 Craft 90 .75L 70.09 72.74 44.95 48.70 00-012 Brown - Forman(3) Old Forester 1897 100 .75L 78.14 80.79 49.95 53.70 00-013 Brown - Forman(3) Old Forester 1920 115 .75L 94.24 96.89 59.95 63.70 00-014 Brown - Forman(3) Old Forester 1910 93 .75L 86.19 88.84 54.95 58.70 00-016 Brown - Forman(3) Old Forester Statesman 95 .75L 86.19 88.84 54.95 58.70 00-018 Stoli Group USA(3) Kentucky Owl Confiscated 96.4 .75L 198.87 201.52 124.95 128.70 00-019 Pernod Ricard USA(3) TX Straight Bourbon 90 .75L 62.04 64.69 39.95 43.70 00-020 Pernod Ricard USA(6) Rabbit Hole Heigold Rye Bourbon 95 .75L 190.60 193.25 59.95 63.70 00-021 Pernod Ricard USA(6) Rabbit Hole Dareringer Bourbon Sherry 93 .75L 254.99 257.64 79.95 83.70 00-022 Seven Jars Distillery(3) Ava Gardner Select Bourbon Whiskey 5Y 101 .75L 102.34 104.99 65.00 68.75 Boutique Collection – Whiskey 00-107 Pernod Ricard USA(3) Midleton Barry Crockett 92 .75L 424.23 426.88 264.95 268.70 00-111 Brown - Forman(3) Jack Daniel's Sinatra 90 1.00L 271.31 273.96 169.95 174.95 00-112 Hotaling & Co.(3) LOT 40 Rye 86 .75L 61.95 64.60 39.90 43.65 00-119 Pernod Ricard USA(3) Redbreast 15Y 15Y 92 .75L 166.68 169.33 104.95 108.70 00-120 Brown - Forman(3) Jack Daniel's No. -

Ararat Akhtamar Brandy 10 Years Old

ARARAT AKHTAMAR BRANDY 10 YEARS OLD Yerevan Brandy Company CJSC, Yerevan, Armenia (since 1887) SAQ # 13209882 │ 40.0% alc./vol. │ $50.50 “Deep amber colour. Aromas of roasted nuts, caramel, dried fruits and raisins follow through on a buoyant, slightly tannic entry to a dry-yet-fruity medium body with notes of cocoa and earth. Finishes with a mashed raisin, dried tobacco, and dusty wood spice fade”. (Beverage Testing Institute) Beautiful amber colour with a touch of copper. Lively and elegant aroma. Beeswax, hazelnut and oak bark with traces of vanilla and dried plum dominate the bouquet. Rounded, hidden, sweetish taste unfolds gradually offering you a temptingly long aftertaste. Light dryness in the end is counter-balanced by shades of cinnamon. During his reign in the 10th century, King Gagik I of the Bagratuni dynasty chose to build a luxurious royal residence on Akhtamar Island, situated on Lake Van in the heart of the medieval Duchy of Greater Armenia. The spacious palace was surrounded by gardens and orchards. The name of the island was inspired by the legend of Princess Tamar and her love for a handsome young man who drowned in the harsh waters of Lake Van with the words 'Ah, Tamar'. Process: Wine goes through two distillation phases: primary and secondary, fractional distillation. The first distillation produces 32° alcohol, which is then distilled again. Secondary distillation separates alcohol into three fractions: head, heart and tail. Only the heart, the purest, thinnest and delicate fraction, is used as the basis for ARARAT brandies. Ageing: 10 years in Caucasian oak. -

Prestige Selection 2018 Eng.Pdf

1 By picking up this catalogue, you are entering the sophisticated world of luxury wines and spirits. The exquisite range of products which we offer, each hold their own unique story of craftsmanship, heritage and traditions, spanning many generations. It is a world where success is based on research, expertise and experience handed down from generation to generation. Each brand presented here tells a unique story of flavours, places and people whose visions were ahead of their time and who pursued their dreams with passion. Behind every bottle lies the reputation of authorities such as Master Blender Collin Scott and Sandy Hyslop, as well as Master Distiller Alan Winchester and Master Cellar Didier Mariotti. They continue the legacy of those who have come before them. Always striving to improve, whilst ensuring that they maintain the highest quality possible and remain true to the craftsmanship of their forefathers. Experience unique, luxurious aromas, flavours and textures, by treating yourself to a bottle from this catalogue. By sharing those experiences with your friends and loved ones, you can fully appreciate the masterful craftsmanship of these industry experts. Your experience is also determined by knowledge, which is why we are delighted to give you the opportunity to explore the nuances of Scotch whisky, Irish whiskey, vodkas, liqueurs, rum, wines and champagnes that will please the most sophisticated palates. 2 3 WHISKY IS MORE THAN ALCOHOL. IT’S A WAY OF LIFE. SCOTCH WHISKY Whisky made in Scotland is notable for its wide spectrum of aromas, from intensely peaty and smoky to delicate and fruity to slightly salty, typical of coastal areas. -

Presentation Refers to Organic Growth, Unless Otherwise Stated

2017/18 FULL-YEAR SALES AND RESULTS 29 August 2018 Contents 3 Executive summary 48 Net profit 7 Sales analysis 52 Cash flow and Debt 26 Marketing, innovation and S&R 59 Conclusion and outlook 35 Profit from Recurring Operations 62 Appendices All growth data specified in this presentation refers to organic growth, unless otherwise stated. Data may be subject to rounding. This presentation can be downloaded from our website: www.pernod-ricard.com Audit procedures have been carried out on the full-year financial statements. The Statutory Auditors’ report will be issued following their review of the management report. Executive summary Very strong year Clear Sales acceleration: +6.0% vs. +3.6% in FY17, thanks to +6.0% consistent strategy implementation: • strong diversified growth, with all regions and key brands performing well Organic Sales • improving price / mix Very strong financial delivery • Profit from Recurring Operations (PRO): +6.3%, in line with revised annual guidance +6.3% • PRO margin improvement: +14bps, while increasing investment behind must-win brands/markets to drive future growth Organic PRO • FX mainly impacted by USD, as expected, with -€180m impact on PRO but €91m favourable impact on Net Debt 1 1 • Net Profit : +13% thanks in particular to reduction in financial expenses • very strong Free Cash Flow (+10%) leading to Net debt decrease of c. €0.9bn to €7.0bn +13% and Net debt / EBITDA at 2.6x2 Proposed dividend increased to 41% payout (2.36€/share)3, in line Net profit with new policy of gradually increasing payout to c. 50% by FY204 1 Reported Group share 2 Based on average EUR/USD rates: 1.19 in FY18 vs.