The Coca-Cola Company 2002 Anuual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Coca-Cola Enterprises, Inc

A Progressive Digital Media business COMPANY PROFILE Coca-Cola Enterprises, Inc. REFERENCE CODE: 0117F870-5021-4FB1-837B-245E6CC5A3A9 PUBLICATION DATE: 11 Dec 2015 www.marketline.com COPYRIGHT MARKETLINE. THIS CONTENT IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED OR DISTRIBUTED Coca-Cola Enterprises, Inc. TABLE OF CONTENTS TABLE OF CONTENTS Company Overview ........................................................................................................3 Key Facts.........................................................................................................................3 Business Description .....................................................................................................4 History .............................................................................................................................5 Key Employees ...............................................................................................................8 Key Employee Biographies .........................................................................................10 Major Products & Services ..........................................................................................18 Revenue Analysis .........................................................................................................20 SWOT Analysis .............................................................................................................21 Top Competitors ...........................................................................................................25 -

Coca-Cola HBC Strengthens Its Coffee Portfolio with Minority Stake in Casa Del Caffè Vergnano and Exclusive, Long-Term Distribution Agreement

Coca-Cola HBC strengthens its coffee portfolio with minority stake in Casa del Caffè Vergnano and exclusive, long-term distribution agreement Zug, Switzerland, 28 June 2021. Coca-Cola HBC AG (“Coca-Cola HBC”) is pleased to announce that on 25 June 2021, its wholly-owned subsidiary CC Beverages Holdings II B.V. (“CCH Holdings”), reached an agreement to acquire a 30% equity shareholding in Casa Del Caffè Vergnano S.p.A. (“Caffè Vergnano”), a premium Italian coffee company. Completion of the acquisition is expected in the second half of 2021 and is subject to customary closing conditions and regulatory approvals. Furthermore, Coca-Cola HBC and Caffè Vergnano will enter into an exclusive distribution agreement for Caffè Vergnano’s products in Coca-Cola HBC’s territories outside of Italy (together, the “Proposed Transaction”). CCH Holdings will be represented on the Board of Directors of Caffè Vergnano and have customary minority decision-making and governance rights. The parties have agreed not to disclose financial details of the Proposed Transaction. Caffè Vergnano is a family-owned Italian coffee company headquartered in Santena, Italy. It is one of the oldest coffee roasters in Italy with roots dating back to 1882. Its product offering consists of truly premium, high-quality coffee that represents Italian heritage and authenticity at its best. Caffè Vergnano’s portfolio includes traditional espresso in various blends, packages and formats such as beans, roast and ground coffee and single portioned pods. In 2020, the company sold approx. 7,000 tons of coffee in more than 90 countries worldwide. The Proposed Transaction represents an important milestone in Coca-Cola HBC’s vision of being the leading 24/7 beverage partner across its markets. -

Thirst for Innovation

QUENCH YOUR THIRST FOR INNOVATION In a market like this, you need to operate at peak performance. Beverage processors need every advantage they can get. Today, your biggest opportunity lies in innovation. At the Worldwide Food Expo, you’ll see how new technologies can address today’s hot topics — from trends and ingredients to food safety, sustainability and how to “green” your operations and packaging. This is the one event that encompasses the entire dairy, food and beverage production process from beginning to end. So go ahead, quench your thirst and better your bottomline. WHERE THE DAIRY AND FOOD INDUSTRY COME TOGETHER OCTOBER 28–31, 2009 CHICAGO, ILLINOIS McCORMICK PLACE WWW.WORLDWIDEFOOD.COM MOVING AT THE SPEED OF INNOVATION REGISTER TODAY! USE PRIORITY CODE ASD08 Soft Drinks Internationa l – October 2009 ConTEnTS 1 news Europe 4 Africa 6 Middle East 8 The leading English language magazine published in Europe, devoted exclusively to the Asia Pacific 10 manufacture, distribution and marketing of soft drinks, fruit juices and bottled water. Americas 12 Ingredients 14 features Juices & Juice Drinks 18 Energy & Sports 20 Drinks With Attitude 26 The energy drinks caTegory conTinues Waters & Water Plus Drinks 22 To grow and boosTed by The inTroduc - Carbonates 23 Tion of innovaTion such as The energy shoT. Rob Walker gives his analysis. Building A Green Employment Brand 36 Packaging 46 User Friendly Fortification RecruiTing and reTaining like-minded Environment 48 employees can pay dividends, reporTs 28 MargueriTe GranaT. People On-Trend, producT innovaTion has 50 been made easier, according To Events 51 Glanbia NuTriTionals. Sincerity 38 Jo Jacobius Takes a look aT boTTled Bubbling Up 53 waTer producers who Truly Take Meeting The Challenge 30 environmenTal and susTainabiliTy Choosing The righT sweeTener sysTem issues To hearT. -

Leverage Our Unique 24/7 Portfolio

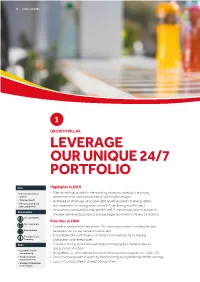

26 COCA-COLA HBC 1 GROWTH PILLAR LEVERAGE OUR UNIQUE 24/7 PORTFOLIO KPIs Highlights in 2019 • FX-neutral revenue • Maintained high growth in the sparkling category, aided by the strong growth performance of sophisticated adult sparkling beverages • Volume growth • Achieved another year of double-digit revenue growth in energy drinks • FX-neutral revenue per case growth and expanded the energy portfolio with Coke Energy and Predator • Innovations supported overall growth, with 4.2pp of total volume growth in Stakeholders the year delivered by products and packages launched in the last 12 months Our consumers Priorities in 2020 Our customers • Continue expanding to become a 24/7 beverage partner, creating shared Shareholders value with our consumers and customers The Coca-Cola • Consolidate the performance of product innovations by increasing Company distribution and repeat sales Risks • Continue driving growth in sparkling by leveraging light variants, flavour and pack architecture • Consumer health and wellbeing • Bring ready-to-drink tea back to growth through a strong plan for FUZETEA • Geopolitical and • Drive revenue growth in water by implementing our hydration portfolio strategy macroeconomic • Launch Costa Coffee in at least 10 countries • Strategic stakeholder relationships INTEGRATED ANNUAL REPORT 2019 27 SR CG FS SSR SI Introduction As lifestyles and consumer habits change, Percentage the motivations and occasions driving of Coca-Cola beverage consumption are also evolving. HBC revenue Our category strategy We are unlocking growth potential in segments beyond our core sparkling portfolio, offering a wider choice of drinks to meet consumer needs at any time of the day. In line with growing societal concerns around environmental issues, consumers are looking for sustainably-sourced ingredients and responsible packaging. -

March / April 1993

The Ecologist Vol 23 No 2 March/April 1993 C * £3 (US $6) My Enemy's Enemies A "Model" Indian Coal Mine Women Evade WID Diversity's Decline •The Great Snail Disaster ISSN D5L1-3131 03 > The Flag of Convenience Multinationals and Maastricht i "770261H313003 Subscribe to Bioscience The biologist's monthly magazine "Editorial standards are excellent, guaranteeing that the papers can be understood by all biologists. As I have traveled worldwide, I hear Bioscience strongly praised by all biologists!" —David Pimentel, Department of Entomology, Cornell University "Bioscience brings to biological scientists the important issues of Whence Bat Fii#»t? the day that affect future directions of research."—Paul Stumpf, Department of Biochemistry and Biophysics, University of California at Davis Join AIBS and start your subscription today! 1993 Rates (per year): Individual @ $49.50 Name Family @ $68.50 Address Sustaining @ $73.00 Emeritus @ $31.50 Charge my: Mastercard _ VISA _ Exp. (These include $30.25 per year for Bioscience) Acct. # Student @ $27.50 Signature (This includes $17.00 per year for Bioscience) Please make check payable to AIBS. Remit US dollars only. Mail to: AIBS, P.O. Box 27417, Central Station, Washington, DC 20077-0038. AMERICAN INSTITUTE OF BIOLOGICAL SCIENCES The Ecologist is published by Ecosystems Ltd. Editorial Office: Agriculture House, Bath Road, Sturminster Newton, Dorset, DT10 1DU, United Kingdom Tel: (0258) 73476 Fax: (0258) 73748 E-Mail [email protected] Subscriptions: RED Computing, 29A High Street, New Maiden, Surrey, KT3 4BY, United Kingdom Tel: (0403) 782644 Fax: (081) 942 9385 Books and Back Issues: WEC Books, Worthyvale Manor, Camelford, Cornwall, PL32 9TT, United Kingdom Tel: (0840) 212711 Fax: (0840) 212808 Annual Subscription Rates Advertising Contributions The editors welcome contributions, which £18 (US$32) for individuals and schools; Display Rates: should be typed, double-spaced, on one Full Colour Outside Back Cover £950 £45 (US$70) for institutions; side of the paper only. -

Automated Cleaning-In-Place Crucial for Beverage Plant Operation Coca-Cola Beverages, Czech Republic Case Story

Automated Cleaning-in-Place crucial for beverage plant operation Coca-Cola Beverages, Czech Republic Case story Being a clear leader in the Czech soft drink market, Coca-Cola has a long history in the region. The first bottles of Coke arrived to the country in 1945 along with U.S. allied troops liberating the western part of Bohemia from the Nazi rule. More than two decades later, the famous drink has been produced here for the first time in the state-owned enterprise in Brno in 1968. Today, Coca-Cola Beverages Czech Republic (CCB), member of Coca-Cola HBC Group is a sole Coca-Cola franchise operator for the Czech market. It is a total beverage company, producing, distributing and selling all categories of non-alcohol drinks. The wide range of its products includes Coca-Cola, Coca-Cola Light, Cherry Coke, Fanta flavours, Sprite, Kinley Tonic Water, Lift flavours, various Cappy flavours, including Cappy Ice Fruit nectars, Bonaqua bottled water (including flavoured versions), Powerade sports drink, Burn energy drink, Nestea Ice Tea, Nescafé and Nescafé Xpress. In the Czech Republic, CCB operates one production facility in Kyje and 10 sales and administration centres around the country. The production, distribution and sales of its beverages directly gives an employment to almost 1300 people. The heart of the Coca-Cola Beverages Czech Republic production is located in Prague’s Kyje district, where the company operates its bottling plant. Efficient cleaning of the piping systems, tanks and filling machines is crucial both for the famed product quality and for keeping up with the high production volumes. -

Salads & Sandwiches Speciality Entrées Starters & Shareables Legendary® Steak Burgers

CLASSIC NACHOS EATS ORIGINAL LEGENDARY® BURGER STARTERS & SHAREABLES CLASSIC NACHOS Crisp tortilla chips layered with ranch-style beans and a four-cheese sauce blend, topped with fresh pico de gallo, spicy jalapeños, pickled red onions, melted Cheddar and Monterey Jack cheese, and green onions, served with sour cream on the side. €13.75 Add Guacamole €4.25 or Grilled Chicken €4.25 or Sirloin Steak* €7.25 ONE NIGHT IN BANGKOK SPICY SHRIMP™ WINGS 227g of crispy shrimp, tossed in a creamy, spicy sauce, topped with green Our signature slow-roasted wings tossed with classic Buffalo or onions, served on a bed of creamy coleslaw. €15.25 barbecue sauce, served with celery and blue cheese dressing. €11.75 ONION RING TOWER ALL-AMERICAN SLIDERS Our signature crispy onion rings perfectly seasoned and served with Three grass-fed mini-burgers with melted American cheese, crispy barbecue and ranch sauce. €6.75 onion ring and creamy coleslaw on a toasted brioche bun.* €15.50 LEGENDARY® STEAK BURGERS All Legendary® Steak Burgers are served with fresh toasted buns and seasoned fries. Upgrade your fries to loaded cheese fries for €1.75 more. ORIGINAL LEGENDARY® BURGER SURF & TURF BURGER The burger that started it all! Black Angus steak burger**, with Our signature steak burger** topped with One Night in Bangkok Spicy smoked bacon, Cheddar cheese, crispy onion ring, leaf lettuce and Shrimp™ on a bed of spicy slaw.* €20.45 vine-ripened tomato.* €16.95 BBQ BACON CHEESEBURGER THE BIG CHEESEBURGER Black Angus steak burger**, seasoned and seared with a signature -

SOFT DRINKS COGNAC, BRANDY Whisky Sandwitches with SPARKLING WINE, CHAMPAGNE

SPARKLING WINE, CHAMPAGNE 1 dl 0,75 l KREINBACHER BIRTOK, Somló Extra dry ..............................1120 Ft ........ 6580 Ft VILLA SANDI, Veneto (Italy) Dolce Sandi white, sweet www.operacafe.hu sparkling wine ..................114 0 F t ........6580 Ft POL ROGER erkel theatre Brut Réserve ...........................................21 980 Ft e Wine s w e t & Savory 1,5 dl 0,75 l KREINBACHER BIRTOK, Somló Ischler .................................................................570 Ft White: Nagy-Somlói cuvée ..990 Ft .... 4420 Ft Linzer ........................................................ 570 Ft Rozé ..............................................990 Ft .... 4420 Ft “Opera” cake ............................................ 720 Ft Red: Birtokvörös ......................990 Ft .... 4420 Ft Eszterházy cake ..................................... 820 Ft Sacher cake ............................................. 820 Ft Scone with Gouda cheese ................... 470 Ft PELLE PINCE, Tokaj ................................... 0,8 dl Sweet: Tokaj ...............................................1980 Ft Pretzel ....................................................... 720 Ft Almond/pistachio/salted peanuts ....... 590 Ft Cheesecake ............................................. 820 Ft Salted caramel ........................................ 820 Ft COGNAC, BRANDY 4 cl Russian Standard vodka ...................... 1480 Ft Grey Goose vodka ................................. 1880 Ft Bombay Sapphire gin ........................... 1580 Ft sandwitches with -

Scotch Whisky, They Often Refer to A

Catalogue Family Overview Styles About the Font LL Catalogue is a contemporary a rising demand for novels and ‘news’, update of a 19th century serif font of these fonts emerged as symptom of Catalogue Light Scottish origin. Initially copied from a new culture of mass education and an old edition of Gulliver’s Travels by entertainment. designers M/M (Paris) in 2002, and In our digital age, the particularities Catalogue Light Italic first used for their redesign of French of such historical letterforms appear Vogue, it has since been redrawn both odd and unusually beautiful. To from scratch and expanded, following capture the original matrices, we had Catalogue Regular research into its origins and history. new hot metal types moulded, and The typeface originated from our resultant prints provided the basis Alexander Phemister’s 1858 de- for a digital redrawing that honoured Catalogue Italic sign for renowned foundry Miller & the imperfections and oddities of the Richard, with offices in Edinburgh and metal original. London. The technical possibilities We also added small caps, a Catalogue Bold and restrictions of the time deter- generous selection of special glyphs mined the conspicuously upright and, finally, a bold and a light cut to and bold verticals of the letters as the family, to make it more versatile. Catalogue Bold Italic well as their almost clunky serifs. Like its historical predecessors, LL The extremely straight and robust Catalogue is a jobbing font for large typeface allowed for an accelerated amounts of text. It is ideally suited for printing process, more economical uses between 8 and 16 pt, provid- production, and more efficient mass ing both excellent readability and a distribution in the age of Manchester distinctive character. -

Annual Report 2001 Serving 500 Million People in 26 Countries

Annual Report 2001 Serving 500 million people in 26 countries Armenia Latvia Chairman’s statement 1 Austria Lithuania Operating review 2 Belarus Moldova Financial review 14 Corporate governance 19 Bosnia & Herzegovina Nigeria Directors, company advisers and other information 22 Bulgaria Northern Ireland Directors’ biographies 23 Croatia Poland Report of the auditors 25 Czech Republic Republic of Ireland Basis of preparation and accounting policies 26 Estonia Romania Consolidated income statement 30 Federal Republic of Yugoslavia Russia Consolidated balance sheet 31 Consolidated cash flow 32 FYROM Slovak Republic Consolidated changes in equity in the year 33 Greece Slovenia Notes to the financial statements 34 Hungary Switzerland Glossary of terms 61 Italy – north and central Ukraine Chairman’s statement A year of great progress In reviewing 2001 performance, I am pleased to report that all of the goals we set for ourselves at the time of the merger with CCB have been achieved. The first full year of the newly enlarged group has seen a continued improvement in performance – volume +8%, underlying EBITDA +18% and operating profit +56%. The strategy of delivering profitable volume growth, which is a balance of price realisation, product/package mix management and cost management is strongly reflected in our results. Within our diverse and balanced portfolio of countries I should make specific reference to Nigeria, Russia and Ukraine where the benefits of the strategies outlined above are reflected in very strong results. I would also like to refer to the acquisitions of those parts of Russia which we did not previously own and the Baltic states of Estonia, Latvia and Lithuania, that were completed on 23 November 2001 and on 2 January 2002 respectively. -

1.4 Introduction to Coca-Cola

Project Report On “Assessing the service Quality level of Maaza brand with respect to its competitors in Nagpur City” A report submitted towards the partial fulfilment of the requirements of the two years full–time Post Graduate Diploma in Management. Under Guidance of Dr. Vikas Kumar Submitted By: Indrajith H PGDM (GENERAL) Roll No. : 2K11A13 (2011-2013) ASIA PACIFIC INSTITUTE OF MANAGEMENT 3&4 Institutional Area, Jasola, NEW DELHI 110025 1 ACKNOWLEDGEMENT Preparing a project of this nature is an arduous task and I was fortunate enough to get support from a large number of people to whom I shall always remain grateful. I would like to express my gratitude to Superior Drinks Pvt Ltd. for allowing me to undertake this project. I must express my profound gratitude to my project guide Prof. Vikas Kumar and Mr.Atul Kumar Organisation Mentor, who has guided me to completion of this project & he has been a pillar of strength to me and always stood by my side during the project tenure with his innovative ideas and conversation full of force, zest and attitude. I am also grateful to my institute, Asia Pacific Institute of Management and various faculty members who provided me a platform from where the academic awareness can be transformed to realistic applications. Indrajith.H PGDM (General) Asia-Pacific Institute of Management, New Delhi 2 DECLARATION I hereby declare that the project work entitled ―Assessing the service Quality level of Maaza brand with respect to its competitors in Nagpur City‖, submitted to the Asia Pacific Institute of Management, is a record of an original work done by me under the guidance of Prof. -

Appendix Unilever Brands

The Diffusion and Distribution of New Consumer Packaged Foods in Emerging Markets and what it Means for Globalized versus Regional Customized Products - http://globalfoodforums.com/new-food-products-emerging- markets/ - Composed May 2005 APPENDIX I: SELECTED FOOD BRANDS (and Sub-brands) Sample of Unilever Food Brands Source: http://www.unilever.com/brands/food/ Retrieved 2/7/05 Global Food Brand Families Becel, Flora Hellmann's, Amora, Calvé, Wish-Bone Lipton Bertolli Iglo, Birds Eye, Findus Slim-Fast Blue Band, Rama, Country Crock, Doriana Knorr Unilever Foodsolutions Heart Sample of Nestles Food Brands http://www.nestle.com/Our_Brands/Our+Brands.htm and http://www.nestle.co.uk/about/brands/ - Retrieved 2/7/05 Baby Foods: Alete, Beba, Nestle Dairy Products: Nido, Nespray, La Lechera and Carnation, Gloria, Coffee-Mate, Carnation Evaporated Milk, Tip Top, Simply Double, Fussells Breakfast Cereals: Nesquik Cereal, Clusters, Fruitful, Golden Nuggets, Shreddies, Golden Grahams, Cinnamon Grahams, Frosted Shreddies, Fitnesse and Fruit, Shredded Wheat, Cheerios, Force Flake, Cookie Crisp, Fitnesse Notes: Some brands in a joint venture – Cereal Worldwide Partnership, with General Mills Ice Cream: Maxibon, Extreme Chocolate & Confectionery: Crunch, Smarties, KitKat, Caramac, Yorkie, Golden Cup, Rolo, Aero, Walnut Whip, Drifter, Smarties, Milkybar, Toffee Crisp, Willy Wonka's Xploder, Crunch, Maverick, Lion Bar, Munchies Prepared Foods, Soups: Maggi, Buitoni, Stouffer's, Build Up Nutrition Beverages: Nesquik, Milo, Nescau, Nestea, Nescafé, Nestlé's