Annual Report 2001 Serving 500 Million People in 26 Countries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cook County Health Media Compilation

Cook County Health Media Compilation Cook County Health News Media Dashboard and Media Compilation The Cook County Health News Media Dashboard: COVID-19 Edition is a visual summary of COVID-19-related news stories that feature Cook County Health experts and leaders from January 21, 2020 through April 28, 2020. January 21 marks the first interview with a Cook County Health expert regarding COVID-19. 1 The following media compilation includes the full text of key news stories mentioning the health system. The first section includes stories about COVID-19, published since January 21. The second section includes stories on other topics published since the previous board meeting on February 28. Part 1: COVID-19 Media Stories Pages 3-267 Part 2: Other Media Stories Pages 268-286 2 Nurses are trying to save us from the virus, and from ourselves April 28, 2020 – Washington Post First, arrive at work before dawn. Then put on a head cover, foot covers, surgical scrubs, and a yellow plastic gown. Next, if one is available, the N95 mask. Fitting it to your face will be the most important 10 seconds of your day. It will protect you, and it will make your head throb. Then, a surgical mask over the N95. A face shield and gloves. Cocooned, you’ll taste your own recycled breath and hear your own heartbeat; you’ll sweat along every slope and crevice of your body. Now, the hard part. Maintain your empathy, efficiency and expertise for 12 or 18 hours, while going thirsty and never sitting down, in an environment that is under-resourced and overworked, because your latest duty — in a profession with limitless duties — is confronting the most frightening pandemic in 100 years while holding people’s hands through it, through two pairs of gloves and a feeling that tomorrow could be worse. -

Kids Parties

HOT DRINKS SHAKES R T SUPER LATTES 39 S R T VANILLA 33 44 COFFEE MADE WITH ALMOND CREAMERY NUT MILK* (OR SOYA MILK IF YOU PREFER) AMERICANO 23 26 29 WHITE CHOCOLATE 33 44 MATCHA PLAIN CHOCOLATE 33 44 CAPPUCCINO 26 29 32 Contains beneficial antioxidant catechins. Coconut sugar & LATTE 26 29 32 oil, organic matcha tea powder, wheatgrass, ground COFFEE 33 44 peppermint leaf & Himalayan crystal salt. FLAT WHITE 28 WILD BERRY 33 44 GOLDEN MILK TUMERIC SF CHAI 33 44 MOCHA DARK CHOC 31 35 39 Powerful anti-inflammatory effects & a strong anitoxidant. MOCHA WHITE CHOC 32 36 40 Coconut sugar & oil, organic ground tumeric, cinnamon, ginger, black pepper, cardamom, nutmeg, Himalayan crystal *Sugar free also available salt & cayenne pepper. ICED FRAPPES 40 RED VELVET BEETROOT ICY FROZEN & SLUSHY LATTES SHORTS S D Contains immune boosting vitamin c, Manganese & CLOSED SANDWICHES COFFEE FREEZO SF 20 23 B vitamin folate. Coconut sugar & oil, ground beetroot, ESPRESSO organic cocoa, ginger, cinnamon and Himalayan crystal salt. ROOIBOS WHITE CHOCOLATE SF CLASSIC CHICKEN MAYONAISE 49 MACCHIATO 23 26 On a ciabatta roll with lettuce, cucumber pickle & tomato. ACTIVE CHARCOAL CHAI LATTE SF CORTADO 23 26 Assists in cleansing toxins & impurities. Made with activated charcoal. CARAMEL CLASSIC CHICKEN MAYONNAISE & AVO 59 WHITE CHOCOLATE SF On a ciabatta roll with lettuce, cucumber pickle, avo & LATTES S R T SF tomato. ROOIBOS 29 34 39 SF PLAIN CHOCOLATE WE USE ALMOND CREAMERY ORIGINAL *Sugar free also available CHAI 29 34 39 SF ALMOND MILK MADE BY SOAKING, TOMATO, MOZZARELLA & BASIL 66 CARAMEL 28 32 36 BLENDING AND STRAINING ALMONDS AND On a ciabatta roll with rocket, walnut pesto & fresh basil. -

Coca-Cola Enterprises, Inc

A Progressive Digital Media business COMPANY PROFILE Coca-Cola Enterprises, Inc. REFERENCE CODE: 0117F870-5021-4FB1-837B-245E6CC5A3A9 PUBLICATION DATE: 11 Dec 2015 www.marketline.com COPYRIGHT MARKETLINE. THIS CONTENT IS A LICENSED PRODUCT AND IS NOT TO BE PHOTOCOPIED OR DISTRIBUTED Coca-Cola Enterprises, Inc. TABLE OF CONTENTS TABLE OF CONTENTS Company Overview ........................................................................................................3 Key Facts.........................................................................................................................3 Business Description .....................................................................................................4 History .............................................................................................................................5 Key Employees ...............................................................................................................8 Key Employee Biographies .........................................................................................10 Major Products & Services ..........................................................................................18 Revenue Analysis .........................................................................................................20 SWOT Analysis .............................................................................................................21 Top Competitors ...........................................................................................................25 -

“Craft” Beer's Competitiveness in Bulgaria

IZVESTIYA 2016 Vol. 60 Journal of Varna University of Economics №1 PRICE ASPECTS OF “CRAFT” BEER’S COMPETITIVENESS IN BULGARIA Yordan IVANOV1 JEL M30, M39 Abstract “Craft” beer is a special part of the “Wine production” class which attracts even more consumers in the last couple of years. The oppor- tunity for an informed choice of a product or service that satisfies specific needs of consumers shifts the focus from the low price to the product of high value for which it must be paid. The goal of this article is to empirically develop the determinants that influence the choice of “Craft” beer based on theoretically proven determinants of competitiveness of price. The scientific tasks can be summarized as: developing the determinants that form the value accepted and theoreti- cal motivation of its relation with price flexibility; theoretical motiva- tion of the relation between price flexibility and price competitive- Keywords: ness; empirical development of the key determinants of price competi- prices, value, rela- tiveness of the “Craft” beer in Bulgaria. In this paper there are used tionships, clients, the methods of analysis and synthesis, surveys through questionnaires, competitiveness. statistical methods, market research and others. Introduction At the onset of the second decade of XXI C there started a wave of developing new “micro” and “small” enterprises in class C.11.05 “Beer production”. Despite the competitive pressure from leaders in the branch they adapt successfully and establish themselves on the market by managing to attract more real clients. While looking for advantages, they are forced to offer their clients a unique product through which to justify its higher price. -

Coca-Cola HBC Strengthens Its Coffee Portfolio with Minority Stake in Casa Del Caffè Vergnano and Exclusive, Long-Term Distribution Agreement

Coca-Cola HBC strengthens its coffee portfolio with minority stake in Casa del Caffè Vergnano and exclusive, long-term distribution agreement Zug, Switzerland, 28 June 2021. Coca-Cola HBC AG (“Coca-Cola HBC”) is pleased to announce that on 25 June 2021, its wholly-owned subsidiary CC Beverages Holdings II B.V. (“CCH Holdings”), reached an agreement to acquire a 30% equity shareholding in Casa Del Caffè Vergnano S.p.A. (“Caffè Vergnano”), a premium Italian coffee company. Completion of the acquisition is expected in the second half of 2021 and is subject to customary closing conditions and regulatory approvals. Furthermore, Coca-Cola HBC and Caffè Vergnano will enter into an exclusive distribution agreement for Caffè Vergnano’s products in Coca-Cola HBC’s territories outside of Italy (together, the “Proposed Transaction”). CCH Holdings will be represented on the Board of Directors of Caffè Vergnano and have customary minority decision-making and governance rights. The parties have agreed not to disclose financial details of the Proposed Transaction. Caffè Vergnano is a family-owned Italian coffee company headquartered in Santena, Italy. It is one of the oldest coffee roasters in Italy with roots dating back to 1882. Its product offering consists of truly premium, high-quality coffee that represents Italian heritage and authenticity at its best. Caffè Vergnano’s portfolio includes traditional espresso in various blends, packages and formats such as beans, roast and ground coffee and single portioned pods. In 2020, the company sold approx. 7,000 tons of coffee in more than 90 countries worldwide. The Proposed Transaction represents an important milestone in Coca-Cola HBC’s vision of being the leading 24/7 beverage partner across its markets. -

European Fruit Juice Association

17-18 October 2018 The must attend event for fruit juice executives www.juicesummit.org AIJN European Fruit Juice Association 2018 Liquid Fruit Market Report AIJN2018_Cover.indd 3 02/08/2018 13:49 AIJN2018_Contents.indd 2 02/08/2018 13:28 Contents COUNTRY PROFILES Austria ........................................................................... 18 Belgium ......................................................................... 19 Bulgaria ......................................................................... 28 Croatia ........................................................................... 28 Cyprus ........................................................................... 28 Czech Republic ................................................................ 30 5 Introduction: Denmark ........................................................................ 30 AIJN President José Jordão Estonia .......................................................................... 30 Finland .......................................................................... 32 6 The Fruit Juice Industry: France ........................................................................... 20 Germany ........................................................................ 21 Overall Fruit Juice and Nectars Consumption Greece ........................................................................... 32 Hungary ......................................................................... 32 7 European Industry Trends and Segmentation Ireland .......................................................................... -

Case Studies in Strategy, Marketing and Innovation

Kids Nutrition Report Issue 60 2017 Kids Nutrition Report Case Studies in strategy, marketing and innovation Published by ISSN 1744-5450 IssUE 60 2017 © New Nutrition Business 2017 1 www.new-nutrition.com Kids Nutrition Report Issue 60 2017 Published by New Nutrition Business The Centre for Food & Health Studies Crown House 72 Hammersmith Road London W14 8TH UK Telephone +44 207 617 7032 Fax +44 207 900 1937 www.new-nutrition.com Asia-Pacific Office: PO Box 21675 Henderson Auckland 0650 New Zealand This edition printed June 2017 © The Centre for Food & Health Studies Limited 2017 Trademark notice: Product or corporate names may be trademarks or registered trademarks and are used only for identification and explanation, without intent to infringe. British ibrary Cataloguing in ublication ata. catalogue record for this case study is available from the British ibrary. ISBN: 978-1-906297-58-9 All enquiries: Miranda Mills Editor Crown House, 72 Hammersmith Road Julian Mellentin New Nutrition Business uses every possible care in London W14 8TH, UK [email protected] compiling, preparing and issuing the information Phone: +44 (0)20 7617 7032 herein given but can accept no liability whatsoever in Fax: +44(0)20 7900 1937 connection with it. [email protected] Dale Buss, New Nutrition Business, 6390 Cherry Tree Ct, Payment by Mastercard, American Express and Visa Rochester Hills, MI 48306, USA. © 2017 The Centre for Food & Health Studies Ltd. Tel: 248-953-2701 accepted. Conditions of sale: All rights reserved; no part of this [email protected] publication may be reproduced, stored in a retrieval For 1 year at $1,175/€895/£745/¥ 95,000/ system, or transmitted in any form by any means, A$1,330/NZ$1,550/C$1,175 (4 issues). -

A New Packaging for Zagorka

Press release A new packaging for Zagorka Heineken entrusts P.E.T. Engineering the development of the new packaging for its Zagorka, the only "special" beer of Bulgaria. San Vendemiano, 07th May 2015 – Zagorka, part of the Heineken Group, is the heir of centuries of devotion to excellence of the big brewers, excellence to which was added a touch of originality that has enabled it to become the only "special "beer in Bulgaria. Zagorka is the beer of a less ordinary taste characterized by a distinctive bitterness and a rich aroma, the result of the perfect balance of two different types of hops: these characteristics make it particularly appreciated by young people between 20 and 30 years who love to experience all that life can offer. The brand therefore needed to associate a less ordinary taste to an equally distinctive packaging that would strengthen the shelf impact and allow to visually align the PET packaging of 1 and 2 liters to the smaller sizes of glass and aluminium. The new design of Zagorka, developed by the Design Center of P.E.T. Engineering, gives the brand a more distinctly masculine connotation through a robust shape and the inclusion of two majestic lions on the body of the bottle, a metaphor for the pride of the Bulgarian people and a reference to the nation in which this special beer is brewed. The labels located in the upper part of the container allow immediate recognition within a range of bottles that show large labels in the central part or thin ones in the lower one. -

Thirst for Innovation

QUENCH YOUR THIRST FOR INNOVATION In a market like this, you need to operate at peak performance. Beverage processors need every advantage they can get. Today, your biggest opportunity lies in innovation. At the Worldwide Food Expo, you’ll see how new technologies can address today’s hot topics — from trends and ingredients to food safety, sustainability and how to “green” your operations and packaging. This is the one event that encompasses the entire dairy, food and beverage production process from beginning to end. So go ahead, quench your thirst and better your bottomline. WHERE THE DAIRY AND FOOD INDUSTRY COME TOGETHER OCTOBER 28–31, 2009 CHICAGO, ILLINOIS McCORMICK PLACE WWW.WORLDWIDEFOOD.COM MOVING AT THE SPEED OF INNOVATION REGISTER TODAY! USE PRIORITY CODE ASD08 Soft Drinks Internationa l – October 2009 ConTEnTS 1 news Europe 4 Africa 6 Middle East 8 The leading English language magazine published in Europe, devoted exclusively to the Asia Pacific 10 manufacture, distribution and marketing of soft drinks, fruit juices and bottled water. Americas 12 Ingredients 14 features Juices & Juice Drinks 18 Energy & Sports 20 Drinks With Attitude 26 The energy drinks caTegory conTinues Waters & Water Plus Drinks 22 To grow and boosTed by The inTroduc - Carbonates 23 Tion of innovaTion such as The energy shoT. Rob Walker gives his analysis. Building A Green Employment Brand 36 Packaging 46 User Friendly Fortification RecruiTing and reTaining like-minded Environment 48 employees can pay dividends, reporTs 28 MargueriTe GranaT. People On-Trend, producT innovaTion has 50 been made easier, according To Events 51 Glanbia NuTriTionals. Sincerity 38 Jo Jacobius Takes a look aT boTTled Bubbling Up 53 waTer producers who Truly Take Meeting The Challenge 30 environmenTal and susTainabiliTy Choosing The righT sweeTener sysTem issues To hearT. -

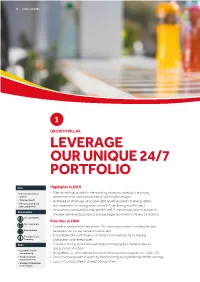

Leverage Our Unique 24/7 Portfolio

26 COCA-COLA HBC 1 GROWTH PILLAR LEVERAGE OUR UNIQUE 24/7 PORTFOLIO KPIs Highlights in 2019 • FX-neutral revenue • Maintained high growth in the sparkling category, aided by the strong growth performance of sophisticated adult sparkling beverages • Volume growth • Achieved another year of double-digit revenue growth in energy drinks • FX-neutral revenue per case growth and expanded the energy portfolio with Coke Energy and Predator • Innovations supported overall growth, with 4.2pp of total volume growth in Stakeholders the year delivered by products and packages launched in the last 12 months Our consumers Priorities in 2020 Our customers • Continue expanding to become a 24/7 beverage partner, creating shared Shareholders value with our consumers and customers The Coca-Cola • Consolidate the performance of product innovations by increasing Company distribution and repeat sales Risks • Continue driving growth in sparkling by leveraging light variants, flavour and pack architecture • Consumer health and wellbeing • Bring ready-to-drink tea back to growth through a strong plan for FUZETEA • Geopolitical and • Drive revenue growth in water by implementing our hydration portfolio strategy macroeconomic • Launch Costa Coffee in at least 10 countries • Strategic stakeholder relationships INTEGRATED ANNUAL REPORT 2019 27 SR CG FS SSR SI Introduction As lifestyles and consumer habits change, Percentage the motivations and occasions driving of Coca-Cola beverage consumption are also evolving. HBC revenue Our category strategy We are unlocking growth potential in segments beyond our core sparkling portfolio, offering a wider choice of drinks to meet consumer needs at any time of the day. In line with growing societal concerns around environmental issues, consumers are looking for sustainably-sourced ingredients and responsible packaging. -

Annual Report 2003 Confidence in Our Business

Annual Report 2003 Confidence in our business Contents 1 Financial highlights 2 Overview of Coca-Cola HBC 8 Chairman’s letter 9 Managing Director’s overview 10 Strategy and execution 20 Operating performance 25 Financial performance 30 Corporate governance 36 Social responsibility 38 Directors’ biographies 40 Governing bodies 41 Financial statements IFRS 85 Financial statements US GAAP 127 Reconciliation US GAAP/IFRS 129 Convenience translation 130 Forward-looking statements 131 Glossary of terms 132 Shareholder information Financial highlights in millions except per share data and ROIC 2003 2002* % change Volume (unit cases) 1,359 1,268 7 Net sales revenue €4,064 €3,881 5 Gross profit 1,594 1,490 7 Operating profit (EBIT) 258 186 39 Profit before tax 212 128 66 Net profit 115 35 >100 Dividends per share €0.19 €0.18 6 Earnings per share 0.49 0.15 >100 EBITDA €665 €579 15 ROIC 7.0% 5.1% 1.9 points * A new policy for accounting for sales revenue was adopted in 2003. Prior year comparatives have been updated for consistency. Refer to IFRS financial statements. Coca-Cola HBC 2003 Annual Report 1 We are one of the world’s largest bottlers of Coca-Cola products Who we are: We are one of Europe’s leading soft drink bottlers. We are also the second largest Coca-Cola bottler in the world in terms of net sales revenue and market capitalisation. We have access to the world’s major capital markets and an extensive international investor base. We have a sizeable team of over 37,000 dedicated employees. -

The Coca-Cola Company 2002 Anuual Report

t he coca-cola company 2002 annual report 2002 annual company he coca-cola creating new value the coca-cola company 2002 annual report Glossary Bottling Partner or Bottler: businesses that buy concentrates, bever- Market: when used in reference to geographic areas, territory in age bases or syrups from the Company, convert them into finished which the Company and its bottling partners do business, often packaged products and sell them to customers. defined by national boundaries. Carbonated Soft Drink: nonalcoholic carbonated beverage contain- Net Capital: calculated by adding share-owners’ equity to net debt. ing flavorings and sweeteners. Excludes, among others, waters and Net Debt: calculated by subtracting from debt the sum of cash, cash flavored waters, juices and juice drinks, sports drinks, and teas equivalents, and marketable securities, less the amount of cash and coffees. determined to be necessary for operations. The Coca-Cola System: the Company and its bottling partners. Noncarbonated Beverages: nonalcoholic noncarbonated beverages on Lithograph Company: The Coca-Cola Company together with its subsidiaries. including, but not limited to, waters and flavored waters, juices and Concentrate or Beverage Base: material manufactured from juice drinks, sports drinks, and teas and coffees. Anders Company-defined ingredients and sold to bottlers to prepare finished Operating Margin: calculated by dividing operating income by net beverages through the addition of sweeteners and/or water and operating revenues. marketed under trademarks of the Company. Printing: Per Capita Consumption: average number of servings consumed Consumer: person who drinks Company products. per person, per year in a specific market. Per capita consumption of Cost of Capital: after-tax blended cost of equity and borrowed funds Company products is calculated by multiplying our unit case volume used to invest in operating capital required for our business.