Investor Presentation CSB Bank Q4 FY20

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

111Th SLBC Meeting

राज्य स्तरीय बℂक셍स 셍मिती,गोवा राज्य State Level Bankers’ Committee, Goa State Agenda & Background Papers of __________________________________ 111th SLBC Meeting WEB MEETING THROUGH MICROSOFT TEAMS th Date : 24 NOVEMBER 2020 Time : 11.30 AM 셍ंयोजकConvener भारतीयस्टेटबℂक State Bank of India िागसदर्शी बℂक मवभाग, SLBC Department थानीय प्रधान कायासलय, Local Head Office, बांद्रा-कुलास 셍ंकुल, Bandra Kurla Complex, िुंबई – ४०००५१, Mumbai – 400051, INDEX Agenda Particulars Page No. Point No. 1 Confirmation of Minutes of 110th SLBC Meeting dated 21.09.2020 2 - 7 2 Position in respect of Action Points of last meeting 8 Review of Financial Inclusion Initiatives, expansion of banking network and 3 Financial Literacy a. Banking scenario of the State 9 b. Details of Business Correspondents / Customer Service Point (BC/CSP) 9 c. List of Unbanked villages 10 d. Review of Financial literacy initiatives by banks (particularly digital 11 financial literacy). e. Status of Financial Inclusion (PMJDY). 11-12 f. Govt Security Schemes (PMSBY PMJJBY and APY) 13-14 4. Expanding and Deepening of Digital Payments Ecosystem 15-17 Review of Credit disbursement by banks 5 a. Review of Performance under ACP 18-23 b. Review of Priority Sector Lending. 24-27 6 Launching of ACP for the year 2021 -22 28 7 Pradhan Mantri MUDRA Yojana (PMMY) 29 a. Progress in Lending for last four quarters b. Position of NPA in Mudra Accounts as on 30.09.2020 8. Doubling farmers’ income by 2022 a. Measures 30 b. Present Position of Lending to Farmers 31 Government Sponsored Schemes 9 a) Review of Government Sponsored Schemes as on 30.09.2020 32 b) Schematic lending, Certificate Cases and Recovery of NPAs 10 The quarterly meetings of Steering Sub Group of SLBC Goa for Sept 2020 33 11 Timely submission of data by Bank, adhering to the schedule of SLBC meeting. -

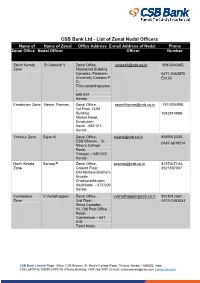

CSB Bank Ltd - List of Zonal Nodal Officers Name of Name of Zonal Office Address E-Mail Address of Nodal Phone Zonal Office Nodal Officer Officer Number

CSB Bank Ltd - List of Zonal Nodal Officers Name of Name of Zonal Office Address E-mail Address of Nodal Phone Zonal Office Nodal Officer Officer Number South Kerala Sri Aneesh V Zonal Office, [email protected] 8943344365, Zone Malankara Building Complex, Palayam, 0471-2463570 University Campus P Ext.33 O, Thiruvananthapuram - 695 034 Kerala Ernakulam Zone Newin Thomas Zonal Office, [email protected] 7510304998, 1st Floor, DJM Building, 7042814998 Market Road, Ernakulam, Kochi - 682 011 Kerala Thrissur Zone Sajan K Zonal Office, [email protected] 8589072330, CSB Bhavan, St 0487-6619214 Mary’s College Road, Thrissur – 680 020 Kerala North Kerala Sanooj P Zonal Office, [email protected] 8157047144, Zone Ground Floor, 8921897007 CM Mathew Brothers Arcade, Chakkorathkulam, Kozhikode – 673 006 Kerala Coimbatore V Varadhappan Zonal Office, [email protected] 9578012367, Zone 2nd Floor, 0422-2383053 Shiva Complex, 54, Old Post Office Road, Coimbatore – 641 018 Tamil Nadu CSB Bank Limited Regd. Office: CSB Bhavan, St. Mary's College Road, Thrissur, Kerala – 680020, India. CIN: L65191KL1920PLC000175 | Phone Banking :1800 266 9090 | E-mail: [email protected] | www.csb.co.in Chennai Zone Saranya R Zonal Office, [email protected] 9942063813 603, Rani Seethai Hall, 044-28294078 Anna Salai, Extn: 22 Chennai – 600 006 Tamil Nadu Western Zone Shoby John Zonal Office, [email protected] 9222104047, Jolly Maker Chambers - 022-22821636 II, 4th Floor, Vinay K Shah Marg, Nariman Point, Mumbai - 400 021 Maharashtra Northern Zone Jagdeep Sharma Zonal Office, [email protected] 9871892299, G- 36, Mezzanine Floor, 011-23733543 Connaught Place, New Delhi -110 001 Deccan Zone Namitha Ponnanna CSB Bank Ltd., Zonal [email protected] 8277093654 Office Unit No. -

Banks Doing Salary Transactions Through Wage

BANKS DOING SALARY TRANSACTIONS THROUGH WAGE PROTECTION SYSTEM Sl No Name of Bank Rating . 1 For WPS Queries Related to State Bank of India : 8921303221 (Jithin),9496096832(Anju Mohan) 2 For WPS Queries Related to Union Bank Pls Contact : 9495590075 (Nidhin) 3 For WPS Queries Related to Federal Bank: 0484-2412125,9746094636(Sita S) 4 For WPS Queries Related to South Indian Bank Pls Contact : 8547389016 (Deepthi),9446373267(Premjith) 5 For WPS Queries Related to ICICI Bank: 9846339935 (Renjith Das) 6 For WPS Queries Related to Canara Bank Pls Contact :8281991598,0471-2471222(Shini) 7 For WPS Queries Related to Dhanlaxmi Bank: 09539003879 ,0487 6617207/211 (Gireesh Nair P) 8 For WPS Queries Related to IDBI Bank: 9047080044,0471-2321168,69 (Manoj A) 8 For WPS Queries Related to Punjab National Bank: 8882345254, 0484-2384625 (Anish) 10 For WPS Queries Related to Andhra Bank: 9912659777(Ashish), 9700835875(Rakesh) 11 For WPS Queries Related to AXIS Bank: 8589008686(Dhanya R); 9847998098(Vivek Sarathy) 12 For WPS Queries Related to CSB Bank: 9620237305,0487-6619283 (Sanilkumar) 13 For WPS Queries Related to HDFC Bank Pls Contact : 9388 302 673 (Sandeepkumar) 14 For WPS Queries Related to Indian Bank Pls Contact : 9446534258 (Ramesh) 15 For WPS Queries Related to Central Bank of India: 4712471294 16 For WPS Queries Related to Bank of India Pls Contact : 8891003310 (Gayathri.J.) 17 For WPS Queries Related to UCO Bank Pls Contact : 0484 2788608 (Unnikrishnan, Manager) 18 For WPS Queries Related to Corporation Bank Pls Contact : 0471-2338260,9446451958(Juny Sam) 19 20 For WPS Queries Related to Indian Overseas Bank Pls Contact : 0471-2461397(Nithin) 21 For WPS Queries Related to IndusInd Bank Pls Contact :9840871992(Mathavan C) 22 23 Note:- *Support Person details of some banks are not included in this document as that are not provided by the bank. -

List-Of-Public-Sector-Banks-In-India

1 List of Public Sector Banks in India Anchor Bank Merged Bank Established Headquarter Vijaya Bank Bank of Baroda 1908 Vadodara, Gujarat Dena Bank Bank of India 1906 Mumbai, Maharashtra Bank of Maharashtra 1935 Pune Maharashtra Canara Bank Syndicate Bank 1906 Bengaluru, Karnataka Central Bank of India 1911 Mumbai, Maharashtra Indian Bank Allahabad Bank 1907 Chennai, Tamil Nadu Indian Overseas Bank 1937 Chennai, Tamil Nadu Punjab & Sind Bank 1908 New Delhi, Delhi Oriental Bank of Commerce Punjab National Bank 1894 New Delhi, Delhi United Bank of India State Bank of Bikaner & Jaipur State Bank of Hyderabad State Bank of Indore State Bank of India 1955 Mumbai, Maharashtra State Bank of Mysore State Bank of Patiala State Bank of Travancore Bhartiya Mahila Bank UCO Bank 1943 Kolkata, West Bengal Andhra Bank Union Bank of India 1919 Mumbai, Maharashtra Corporation Bank List of Private Sector Banks in India Bank Name Established Headquarters HDFC Bank 1994 Mumbai, Maharashtra Axis Bank 1993 Mumbai, Maharashtra Bandhan Bank 2015 Kolkata, West Bengal CSB Bank 1920 Thrissur, Kerala City Union Bank 1904 Thanjavur, Tamil Nadu DCB Bank 1930 Mumbai, Maharashtra Dhanlaxmi Bank 1927 Thrissur, Kerala Federal Bank 1931 Aluva, Kerala 2 Bank Name Established Headquarters ICICI Bank 1994 Mumbai, Maharashtra IDBI Bank 1964 Mumbai, Maharashtra IDFC First Bank 2015 Mumbai, Maharashtra IndusInd Bank 1994 Mumbai, Maharashtra Jammu & Kashmir Bank 1938 Srinagar, Jammu and Kashmir Karnataka Bank 1924 Mangaluru, Karnataka Karur Vysya Bank 1916 Karur, Tamil Nadu Kotak -

Banking Annual DATABASE

bank-datatable-2021-revised.qxd 29/01/2021 07:00 PM Page 2 Banking Annual DATABASE (In ~ crore) FY 2019 FY 2020 % chg (In ~ crore) FY 2019 FY 2020 % chg PRIVATE BANKS FOREIGN BANKS City Union Bank 32,673 33,927 3.8 J P Morgan Chase 13,800 14,683 6.4 CSB Bank 10,615 11,366 7.1 Societe Generale 1,495 1,574 5.3 DCB Bank 23,568 25,345 7.5 Standard Chartered Bank 66,838 76,214 14.0 Dhanlaxmi Bank 6,289 6,496 3.3 Sumitomo Mitsui 6,920 10,920 57.8 Federal Bank 1,10,223 122,268 10.9 HDFC Bank 8,19,401 993,703 21.3 ICICI Bank 5,86,647 645,290 10.0 GROWTH: DEPOSITS IDBI Bank 1,46,790 129,842 -11.5 IDFC First Bank 86,302 85,595 -0.8 PUBLIC SECTOR BANKS IndusInd Bank 1,86,394 206,783 10.9 Bank of Baroda 9,15,159 9,45,984 3.4 Jammu and Kashmir Bank 66,272 64,399 -2.8 Bank of India 5,20,862 5,55,505 6.7 Karnataka Bank 54,828 56,964 3.9 Bank of Maharashtra 1,40,650 1,50,066 6.7 Karur Vysya Bank 48,581 46,098 -5.1 Canara Bank 5,99,033 6,25,351 4.4 Kotak Mahindra Bank 2,05,695 219,748 6.8 Central Bank of India 2,99,855 3,13,763 4.6 Nainital Bank 3,516 3,829 8.9 Indian Bank 2,42,076 2,60,226 7.5 RBL Bank 54,308 58,019 6.8 Indian Overseas Bank 2,22,534 2,22,952 0.2 South Indian Bank 62,694 64,439 2.8 Punjab & Sind Bank 98,558 89,668 -9.0 Tamilnad Mercantile Bank 26,488 27,716 4.6 Punjab National Bank 6,76,030 7,03,846 4.1 Yes Bank 2,41,500 171,443 -29.0 State Bank of India 29,11,386 32,41,621 11.3 UCO Bank 1,97,907 1,93,203 -2.4 SMALL FINANCE BANKS Union Bank of India 4,15,915 4,50,668 8.4 AU Small Finance Bank 22,819 26,992 18.3 Equitas Small Finance Bank -

SKRZ/LD/SARFAESI/ / 2021 Zonal Office, Thiruvananthapuram AUCTION SALE NOTICE Auction Sale Notice for Sale of Immovable

SKRZ/LD/SARFAESI/ / 2021 Zonal Office, Thiruvananthapuram AUCTION SALE NOTICE Auction Sale Notice for sale of immovable Assets under the Securitisation and Reconstruction of Financial Assets and Enforcement of security Interest Act, 2002 read with proviso to Rule 8 (6) of the Security Interest (Enforcement) Rules 2002. Notice is given to the public in general and in particular to the Borrower and guarantors that the below described immovable property mortgaged/charged to the Secured Creditor, the physical possession of which has been taken by the Authorised Officer of CSB Bank Ltd,(Formerly The Catholic Syrian Bank Ltd), Secured Creditor, will be sold on “As is where is” “As is what is” and “Whatever there is” on 24.03.2021 for recovery of Rs.6,96,64,070/34(Rupees Six Crores Ninety Six Lakhs Sixty Four Thousand and Seventy and Paisa Thirty Four Only) as on 31-01.2021 with further interest and cost in M/s Narayana Cashew and Rs.11,46,82,407/44 (Rupees Eleven Crores Fourty Six Lakhs Eighty Two Thousand Four Hundred and Seven and Paisa Fourty Four Only) as on 31.01.2021 with further interest and cost in M/s Ohm Namasivaya Cashew due to CSB Bank Ltd, Secured Creditor, from borrower,1.M/s Narayana Cashew,(Prop.Mr Sasidharan Pillai),2.Mr Sasidharan Pillai,Prop.M/s Narayana Cashew, Guarantors: (1) Sri. Hareesh Kumar, (2) Smt. Lalithamma, W/o Sasidharan Pillai, (3) Smt. Lakshmikutty, W/o Kunjukrishna Pillai, All Residing at: Lakshmi Bhavanam, Puthenchantha, Vallikunnam P.O., Alappuzha-690501., And (1) M/s. -

Live Banks in API E-Mandate

Bank status in API E-Mandate Sponsor Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK BANK LTD Live Live 2YESB YES BANK Live Live 3 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 4 INDB INDUSIND BANK Live Live 5 ICIC ICICI BANK LTD Live Live 6 IDFB IDFC FIRST BANK LTD Live Live 7 HDFC HDFC BANK LTD Live Live 8 ESFB EQUITAS SMALL FINANCE BANK LTD Live Live 9 DEUT DEUTSCHE BANK AG Live Live 10FDRL FEDERAL BANK Live Live 11 SBIN STATE BANK OF INDIA Live Live 12CITI CITI BANK Live Live 13UTIB AXIS BANK Live Live 14 PYTM PAYTM PAYMENTS BANK LTD Live Live 15 SIBL SOUTH INDIAN BANK Live Live 16 KARB KARNATAKA BANK LTD Live Live 17 RATN RBL BANK LIMITED Live Live 18 JSFB JANA SMALL FINANCE BANK LTD Live Live 19 CHAS J P MORGAN CHASE BANK NA Live Live 20 JIOP JIO PAYMENTS BANK LTD Live Live 21 SCBL STANDARD CHARTERED BANK Live Live 22 DBSS DBS BANK INDIA LTD Live Live 23 MAHB BANK OF MAHARASHTRA Live Live 24CSBK CSB BANK LTD Live Live 25BARB BANK OF BARODA Live Live 26IBKL IDBI BANK Live X 27KVBL KARUR VYSA BANK Live X 28 HSBC THE HONGKONG AND SHANGHAI BANKING CORPORATION LTD Live X 29BDBL BANDHAN BANK LTD Live X 30 CBIN CENTRAL BANK OF INDIA Live X 31 IOBA INDIAN OVERSEAS BANK Live X 32 PUNB PUNJAB NATIONAL BANK Live X 33 TMBL TAMILNAD MERCANTILE BANK LTD Live X 34 AUBL AU SMALL FINANCE BANK LTD X Live Destination Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK MAHINDRA BANK LTD Live Live 2YESB YES BANK Live Live 3 IDFB IDFC FIRST BANK LTD Live Live 4 PUNB PUNJAB NATIONAL BANK Live Live 5 INDB INDUSIND BANK Live Live 6 USFB -

City Union Bankfebruary 13, 2020

City Union Bank (CITUNI) CMP: | 155 Target: | 200 (29%) Target Period: 12 months BUY August 10, 2021 Operational performance steady… City Union Bank is an old private sector bank with focus on MSME Particulars About the stock: and trading loans that form 52% of overall advances. Particulars Amount Market Capitalisation | 11462 crore Strong presence in south India with 630 out of total 702 branches 52 week H/L 200 /116 Update Total 99% of bank’s advances are secured loans Networth (FY21) | 5842 crore Face value | 1 Shareholding pattern Result Q1FY22 Results: PAT was boosted by other income and low credit cost. Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Promoter - - - - - NII up 2.4% YoY, 4.5% QoQ at | 448 crore, NIMs up 14 bps QoQ to 3.86% FII 21.7 18.7 18.7 18.0 17.2 DII 30.1 27.5 37.6 39.1 41.7 Other income up 34.9% QoQ helped by ~3.5x rise in treasury income Others 48.3 53.8 43.8 42.9 41.2 C/I ratio down 991 bps to 40.5%; provisions fell 28.7% QoQ to | 170 crore Price Chart Loan book up 5.4% YoY while deposit growth was at 8.7% YoY 300 18000 16000 GNPA up 48 bps QoQ to 5.59% while restructuring up 46 bps QoQ to 5.45% 250 14000 200 12000 10000 150 8000 100 6000 City Union Bank’s stock price has given over 30% 4000 What should investors do? 50 2000 returns in the past five years. -

South Indian Bank Ltd

South Indian Bank Ltd. Target: Rs. 14 CMP INR. 10.73 (FY24 P/ Adj.Bv 0.6X) BUY Index Details The South Indian Bank Ltd (SIB) based out of Thrissur (Kerala) is one of Sensex 50,651.90 the earliest banks in South India. The bank, after reporting subdued Nifty 15,197.70 numbers in the recent past has now recalibrated its approach with the new management and redefined business strategies. This is evident from its recent performance in which the bank has successfully improved its CASA Industry Banking deposits stood at an all-time high CASA ratio of 29.7% along with simultaneously decreasing its exposure in the Standard Large Corporate Scrip Details Advances (INR 100 Cr and above) from 27% of total advances in FY15 to Mkt Cap (INR Cr) 2,245.51 5% of total advances in FY21. O/S Share (Cr) 209.27 52 Wk H/L (INR) 11.83/4.85 Further, with the bank’s focus on retail banking (Deposits and Advances), growing its low-cost CASA and NRI deposits, coupled with change in Div Yield (%) 2.25 business strategy from branch banking to establishment of verticals for FVPS (INR) 1.00 each segment of retail assets, we expect a turnaround in this stock in the coming period. Shareholding Pattern We initiate coverage on South Indian Bank Ltd with a price target of INR 14.0 per share, which represents a potential upside of 30.8% from the CMP Shareholder % of INR 10.73 (FY24 P/Adj BV 0.75 x) over a period 24 months. -

Comparative Analysis of Public and Private Sector Banks in India

Quest Journals Journal of Research in Business and Management Volume 8 ~ Issue 11 (2020) pp: 61-63 ISSN(Online):2347-3002 www.questjournals.org Comparative Analysis of Public and Private Sector Banks in India Rabindra Kumar Assistant professor, Department of Commerce SPY College, Gaya ABSTRACT: Public Sector Banks (PSBs) are a major type of bank in India, where a majority stake (i.e. more than 50%) is held by the government. The shares of these banks are listed on stock exchanges. The private sector enterprise is an organisation which is owned, managed & controlled by private individuals or a group of individuals or both. This is also engaged in business activity but with the motive of profit maximisation rather than public service like in case of public sector enterprise. The merger of the loss making New Bank of India with the profitable Punjab National Bank was the first instance of merger of two public sector commercial banks. Corporate world have been merging to gain synergies in their operations, derive economies of scale and offer one-stop facilities to more demanding clientele. Hence, the desire to grow quickly through mergers, rather than through the slow path of normal expansion in business it is important to improve the competitiveness and quality of the services sector in order to enhance its efficiency. The present comparative study focuses on the merger of public and private sector banks in India specially merger events relating to Bank of Baroda, Punjab National Bank, HDFC Bank and ICICI Bank. It also examines the only aspect of such merger(s) in terms of valuation of banks before and after merger and find out the result that which sector gained more value through merger in India. -

Investor Presentation CSB Bank Q4 FY21

CSB Bank Investor Presentation Q4 FY 21 Company Business Digital Earnings Strategy Overview Overview Penetration Key Information • A century young Total provisions down Well Capitalised by Rs 167Cr (53%) YoY Organisation Growth Asset Improved Cost and & Strong (12M Period) • 514 Branches & 320 Profitability Revenue Momentum Liquidity Quality Position ATMs • 9 Zonal Offices * GNPA came down to • 1.7Mn happy customers *Posted strong NII growth *Advance grew by 27% in 2.68% as against 3.54% *Highest PAT for the 12 *Strong Capital comfort • Presence in 16 states & of 59% YoY FY 21 & 10% QoQ with a CRAR of 21.37% as on 31.03.20- down by 86 months ended 31.03.21 - on 31.03.2021 bps 4 UTs crosses double century *Non interest income up *Deposits grew by 21% in mark in the century year - by 81% –supported by * Net NPA decreased FY 21 & 8% QoQ * Tier I ratio of 19.96% • Total business of at Rs 218 Cr Treasury, PSLC income, PF, from 1.91% as on Banca/BG Commission etc 31.03.2020 to 1.17% as Over Rs 34500 Cr * In terms of overall *Strong liquidity & LCR of on 31.03.2021 business, bank has grown Increase in income out 210% • 6 bancassuance tie ups •PBT up by 118% for FY21 * a fourth of the total *PCR of 85% as on weighed the increase in business it grew in past 99 31.03.2021 with industry leaders. opex on account of years. *comfortable leverage ratio increased AS 15 provisions, 8.11% *Operating Profit surges Opening of 101 branches, *Accelerated *CASA annual growth of Provisioning Policy-25% to Rs 613 Cr with 119% conservative depreciation increase -

Notice and Regulations for CSB Bank Limited (Immediate Joinees Required) (MBA/PGDM) 2021

Notice and Regulations for CSB Bank Limited (Immediate Joinees Required) (MBA/PGDM) 2021 IMPORTANT 1. Interested students are advised to read full notice 2. Registration link: https://virtual-event.convstaging.com/user/signup Company: CSB Bank Eligibility: MBA/PGDM 2021 batch Salary: 2.5 LPA Position: Customer Relationship Officer Last Date To Apply: 24 June before 6 pm Drive Date: will be notified soon. Drive Location: online About the Company: Established in 1920 as The Catholic Syrian Bank Limited, CSB Bank Limited had its modest beginning in November 1920 and is currently the oldest private sector bank in Kerala, celebrating its Centenary Year in 2020. It was in 1969 that the Bank became a Scheduled Bank, as it was included in the Second Schedule of Reserve Bank of India Act. website:www.csb.co.in Job Description: To support branch head in operations ensuring top of the line customer service and customer engagements Customer Service, Acquisition & Ops; customer service and retention: Branch Operation; NTB Sourcing through referrals and outbound activities; Cross Sell. Job Responsibilities: PART A: Branch Service and Operations: A. Assisting the Branch Manager in carrying out day to day activities and all general banking activities of the branch under Core Banking System environment (CBS). B. Assisting the Branch Manager in recovery and monitoring of Non-Performing Assets (NPA) accounts and the process. C. Rendering effective customer service at counter including disbursement of cash. D. Maintaining proper book of accounts E. Performing the duties as an officer in charge of cash, including receipt and payment of cash and giving and signing receipts and giving effectual discharge for money that are paid and received F.