CHAPTER 16 Cost Concepts and Cost Allocation

REVIEWING THE CHAPTER Objective 1: Describe how managers use information about costs. 1. Because costs affect profitability, having accurate and up-to-date cost information is important to managers in all types of for-profit organizations. Managers in manufacturing, retail, and service businesses use information about operating costs to plan, perform, evaluate, and communicate the results of operating activities. a. In the planning stage, managers develop budgets and estimate selling prices for goods or services based on estimates of operating costs. b. In performing operating activities, managers use cost information in several ways, including estimating the profitability of a product or service, deciding whether to drop a product line or service, and determining selling prices. c. When managers evaluate performance, they want to know about significant variances between estimated costs and actual costs. Such variances help them ascertain the reasons for cost overruns, which may enable them to avoid such problems in the future. d. In external reports, managers expect income statements that communicate the actual cost of operating activities and balance sheets that show the value of inventory. They expect internal reports that summarize their plans, summarize performance outcomes, and evaluate variances. Objective 2: Explain how managers classify costs and how they use these cost classifications. 2. A single cost can be classified in several ways: by cost traceability, by cost behavior, by whether it is value-adding or nonvalue-adding, and by whether it is a product cost or a period cost. 3. By tracing costs to cost objects, such as products or services, managers can obtain a fairly accurate cost measurement on which to base decisions about pricing and about reallocating resources to other cost objects. a. Direct costs are costs that can be conveniently or economically traced to a specific cost object. The wages of production workers, which can be directly traced to an individual product, are an example. b. Indirect costs are costs that cannot be conveniently or economically traced to a cost object. Rivets used in the production of airplanes and glue used in the production of furniture are examples. Although difficult to trace, indirect costs must be included in the cost of a product or service; to do so, managers use a formula to assign them to a cost object. 4. Cost behavior is the way costs respond (or do not respond) to changes in volume or activity. A cost that changes in direct proportion to a change in productive output (or to any other measure of volume) is a variable cost. A fixed cost is one that remains constant within a defined range of activity or time period. By analyzing cost behavior, managers can calculate the number of units that must be sold to obtain a certain level of profit. 5. A value-adding cost is the cost of an activity that increases the market value of a product or service—that is, the value as perceived by the customer. For example, if customers are willing to pay more for a product made of a better material, the company’s cost of using that material in its product is a value-adding cost. A nonvalue-adding cost is the cost of an activity that adds cost to a product or service but does not increase its market value. Such a cost may, however, be necessary. For example, the accounting department is necessary for the operation of a business, but it does not add value to a business’s product or service. By classifying costs as adding value or not adding value, managers can eliminate the costs of nonvalue-adding activities that are not essential to the business and try to reduce the costs of those that are essential. 6. For financial reporting purposes, managers classify costs as product costs or period costs. a. Product costs (also known as inventoriable costs) are costs assigned to inventory. They include the three elements of manufacturing cost: direct materials, direct labor, and overhead. Product costs appear on the income statement as cost of goods sold and on the balance sheet as finished goods inventory. b. Period costs (also called noninventoriable costs) are the costs of resources used during the accounting period and not assigned to products. They appear as operating expenses on income statement. Period costs appear as expenses on the income statement in the period in which they are incurred—for example, selling, administrative, and general expenses. Objective 3: Compare how service, retail, and manufacturing organizations report costs on their financial statements and how they account for inventories. 7. A manufacturer prepares a statement of cost of goods manufactured so that the cost of goods sold can be summarized in the income statement. The example that follows illustrates the three steps involved in preparing a statement of cost of goods manufactured. a. First, the cost of direct materials used must be found. Beginning balance, materials inventory $100 Add direct materials purchased (net) 350 Cost of direct materials available for use $450 Less ending balance, materials inventory 200 Cost of direct materials used $250 (1) b. Second, total manufacturing costs must be computed. Cost of direct materials used (computed in section a) $ 250 (1) Add direct labor costs 900 Add total overhead costs 750 Total manufacturing costs $1,900 (2) c. Third, the cost of goods manufactured must be computed. Total manufacturing costs (computed in section b) $1,900 (2) Add beginning balance, work in process inventory 400 Total cost of work in process during the period $2,300 Less ending balance, work in process inventory 700 Cost of goods manufactured $1,600 (3) 8. When the figure for the cost of goods manufactured has been computed, it can be transferred to the cost of goods sold section of the income statement, as follows: Beginning balance, finished goods inventory $1,250 Add cost of goods manufactured (computed in section c) 1,600 (3) Total cost of finished goods available for sale $2,850 Less ending balance, finished goods inventory 300 Cost of goods sold $2,550 9. Because the operations of service, retail, and manufacturing organizations differ, their financial statements differ as well. Because a service organization sells services, not products, it has no inventory account on its balance sheet. The cost of sales on its income statement reflects the net cost of the services sold. A retail organization, which purchases products ready for resale, maintains only one inventory account on its balance sheet. Called the Merchandise Inventory account, it reflects the costs of goods held for resale. The cost of goods sold on a retail organization’s income statement is simply the difference between the cost of goods available for sale and the ending merchandise inventory. A manufacturing organization, because it creates a product, maintains three inventory accounts on its balance sheet: Materials Inventory, Work in Process Inventory, and Finished Goods Inventory. Its cost of goods sold equals the cost of goods available for sale minus ending finished goods inventory. Objective 4: Describe the flow of costs through a manufacturer’s inventory accounts. 10. A manufacturer maintains a Materials Inventory account, a Work in Process Inventory account, and a Finished Goods Inventory account. The balance in the Materials Inventory account shows the cost of goods purchased but unused. The balance in the Work in Process Inventory account shows the costs assigned to partially completed products. The balance in the Finished Goods Inventory account shows the costs of products completed but not yet sold. 11. Accountants track manufacturing costs and make changes in account balances by referring to the source documents that accompany the flow of costs through the production process. a. The purchasing process begins with a purchase request for materials. If the materials are not on hand, the purchasing department sends a purchase order to a supplier. A receiving report documents the arrival of the materials. The company then receives a vendor’s invoice for payment for the materials. The costs of these materials increase the balance in the Materials Inventory account. b. As production begins, the storeroom clerk receives an authorized materials request form specifying which materials are to be sent to the production area. The cost of the direct materials transferred to production increases the balance of the Work in Process Inventory account, and the cost of the indirect materials transferred increases the balance of the Overhead account. The costs of both types of materials decrease the balance of the Materials Inventory account. Time cards are used to record production employees’ hours; the cost of their labor increases the Work in Process Inventory account. A job order cost card records all costs incurred as the products move through production. c. The cost of completed products decreases the balance of the Work in Process Inventory account and increases the balance of the Finished Goods Inventory account. When a product is sold, a clerk prepares a sales invoice. A shipping document shows the quantity of goods shipped and gives a description of them. As products are sold, the balance in the Finished Goods Inventory account decreases, and the balance in the Cost of Goods Sold account increases. 12. Manufacturing cost flow is the flow of manufacturing costs (direct materials, direct labor, and overhead) through the Materials Inventory, Work in Process Inventory, and Finished Goods Inventory accounts into the Cost of Goods Sold account. Manufacturing costs flow first into the Materials Inventory account, which is used to record the costs of materials when they are received and again when they are issued for use in production. As the production process begins, all manufacturing-related costs (direct materials, direct labor, and overhead) are recorded in the Work in Process Inventory account. The total costs of direct materials, direct labor, and overhead incurred and transferred to Work in Process Inventory during an accounting period are called total manufacturing costs. When products are completed, their costs move from the Work in Process Inventory account to the Finished Goods Inventory account. The cost of goods manufactured is the cost of all units completed and moved to finished goods storage. Costs remain in the Finished Goods Inventory account until the products are sold. They are then transferred to the Cost of Goods Sold account. Objective 5: Define product or service cost and compute the unit cost of a product or service. 13. The three elements of product cost are the costs of direct materials, direct labor, and overhead (which are indirect costs). Direct materials costs are costs that can be conveniently and economically traced to specific products, such as the cost of the wood used in making a desk. Direct labor costs are the costs of the labor needed to make a product that can be conveniently and economically traced to specific units of the product (e.g., the wages of production workers). Overhead costs (also called service overhead, factory overhead, factory burden, manufacturing overhead, or indirect manufacturing costs) are costs of production that cannot be practically or conveniently traced directly to an end product. They include the costs of indirect materials and indirect labor. a. Indirect materials costs are costs that are too insignificant to assign to direct materials—for example, the costs of nails, rivets, lubricants, and small tools. b. Indirect labor costs are labor costs for production-related activities that cannot be conveniently traced to a product, such as the costs of maintenance, inspection, engineering design, supervision, and materials handling. c. Other indirect manufacturing costs include the costs of building maintenance, property taxes, property insurance, rent, utilities, and depreciation on plant and equipment. 14. Prime costs are the primary costs of production; they are the sum of a product’s direct materials costs and direct labor costs. Conversion costs are the costs of converting raw materials into finished goods; they are the sum of the direct labor and overhead costs incurred in turning direct materials into a finished product. 15. Product unit cost is the cost of manufacturing a single unit of product. It is computed either by dividing the total cost of direct materials, direct labor, and overhead by the total number of units produced, or by determining the cost per unit for each element of the product cost and adding those per-unit costs. Product unit cost can be calculated by using the actual, normal, or standard costing methods. a. Actual costing uses the costs of direct materials, direct labor, and overhead at the end of the accounting period, or when actual costs are known, to calculate the product unit cost. b. Normal costing combines the actual direct materials and direct labor costs with estimated overhead costs to determine a product unit cost. It can be used when the actual overhead costs are not yet known. c. Standard costing allows managers to use estimates (standards) of direct materials, direct labor, and overhead costs to determine the product unit cost. Managers use standard costs as a benchmark for pricing decisions and for controlling product costs. Objective 6: Define cost allocation and explain how cost objects, cost pools, and cost drivers are used to assign overhead costs. 16. Overhead costs are indirect costs that must be collected and allocated in some manner. Cost allocation is the process of assigning a collection of indirect costs to a specific cost object, such as a product or service, using an allocation base known as a cost driver. A cost driver might be direct labor hours, direct labor costs, units produced, or another activity base that has a cause-and-effect relationship with the cost. As a cost driver increases in volume, it causes the cost pool—the collection of indirect costs assigned to a cost object—to increase in amount. 17. Allocating overhead costs is a four-step process that corresponds to the four stages of the management process. In the first step (planning), managers estimate overhead costs and calculate a predetermined overhead rate (in traditional settings) by dividing the cost pool of total estimated overhead costs by the total estimated cost driver level, or an activity pool rate (in activity-based costing settings) at which they will assign overhead costs to products or services. In the second step (performing), the estimated overhead costs are applied to the product or service as overhead costs are incurred and recorded during production. In the third step (evaluating), actual overhead costs are recorded as they are incurred, and managers calculate the difference between the estimated or (applied) and actual costs. In the fourth step (communicating), managers report on this difference. 18. At the end of the accounting period, the difference between the applied overhead and actual overhead costs is calculated and reconciled. The Cost of Goods Sold account is corrected if the amount of overapplied overhead costs or underapplied overhead costs is immaterial. If the amount is material, adjustments are made not only to the Cost of Goods Sold account, but also to the Work in Process Inventory and Finished Goods Inventory accounts. 19. Because managers use predetermined overhead rates to make pricing decisions and to control costs, the rates should be calculated as accurately as possible. The successful allocation of overhead costs depends on two factors: a careful estimate of the total overhead costs and a good forecast of the cost driver activity level used to allocate overhead. Objective 7: Using the traditional method of allocating overhead costs, calculate product or service unit cost. 20. The traditional approach to applying overhead costs is to use a single predetermined overhead rate. The total overhead costs constitute one cost pool, and a traditional activity base, such as direct labor hours, direct labor costs, or machine hours, is the cost driver. 21. The first step in calculating product or service unit cost when using the traditional method is to compute a predetermined overhead rate. The second step is to apply overhead costs to the products by multiplying the predetermined rate by the actual cost driver level. For example, assume that total estimated overhead is $100,000 and that the cost driver (direct labor hours) is estimated at 5,000 hours. Actual direct labor hours total 4,500. Of the 4,500 hours, 2,000 were spent on the production of 6,000 units of Product A, and 2,500 were spent on the production of 7,000 units of Product B. The predetermined overhead rate would be calculated as follows: $100,000 = $20 per Direct Labor Hour 5,000 Overhead would then be applied to both products as follows: A: 2,000 D.L. Hours × $20 Rate = $40,000 B: 2,500 D.L. Hours × $20 Rate = 50,000 Total Applied $90,000 Thus, the overhead cost per unit is $40,000 Applied A. = $6.67 per Unit 6,000 Units $50,000 Applied B. = $7.14 per Unit 7,000 Units

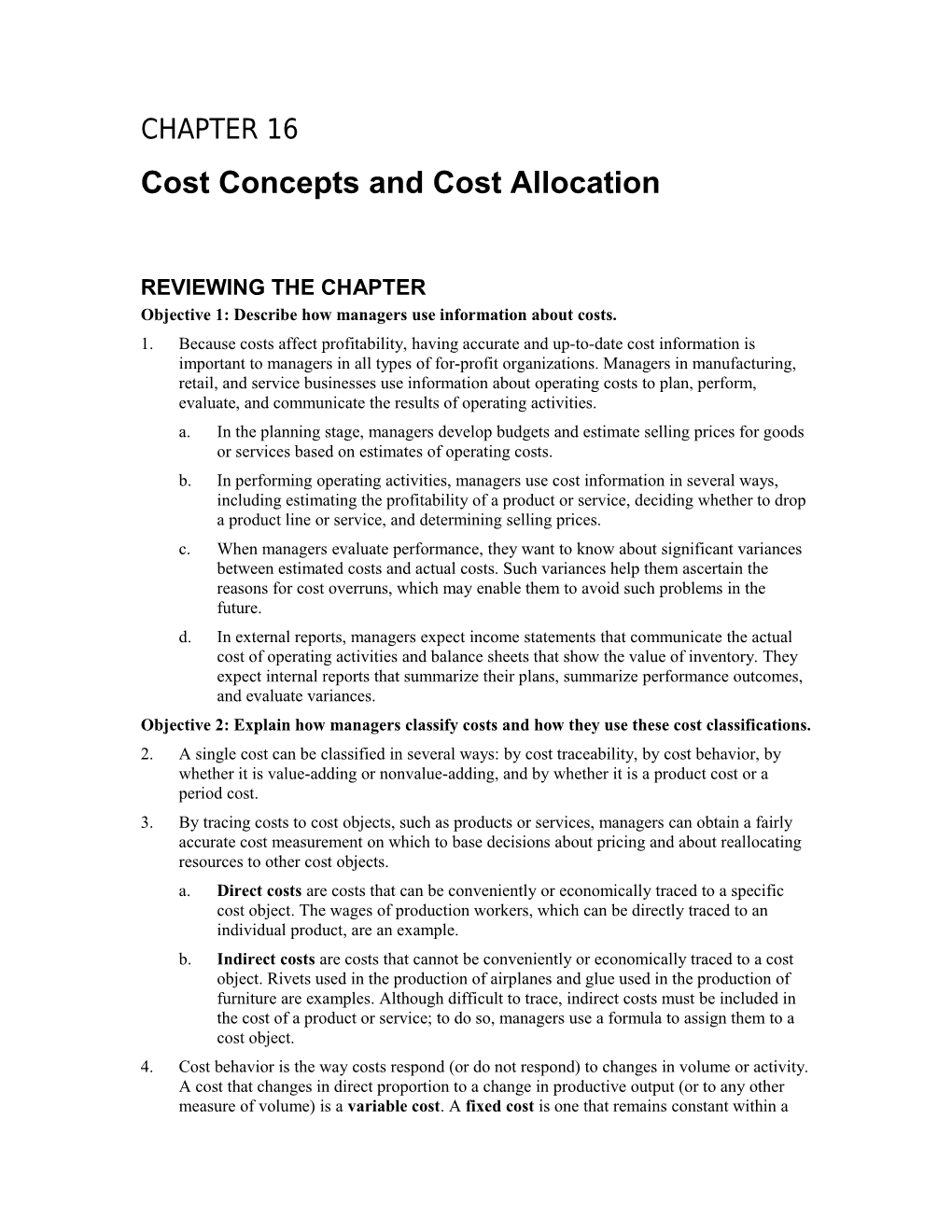

Objective 8: Using activity-based costing to assign overhead costs, calculate product or service unit cost. 22. Activity-based costing (ABC) is a more accurate method of assigning overhead costs to products and services than the traditional method. It categorizes all indirect costs by activity, traces the indirect costs to those activities, and assigns activity costs to products or services using a cost driver related to the cause of the cost. 23. The first step in calculating product unit cost when using activity-based costing is to estimate the total overhead costs and then group these costs into appropriate activity pools related to specific activities. After identifying the appropriate number of activity pools and a cost driver, estimated activity pool amounts and estimated cost driver levels must be determined. The next step is to calculate a predetermined activity cost rate for each activity pool, as shown in Table 1. The cost pool rate is the estimated activity pool amount divided by the estimated cost driver level. As shown in Table 2 (below), overhead costs are then applied to the products or services by using the cost driver levels for each cost driver multiplied by the appropriate rate. Table 1 Activity Estimated Total Estimated Total Cost Predetermined Pool Activity Pool Costs Cost Driver Driver Level Activity Cost Rate Setup $10,000 Number of setups 100 setups $100 per setup Inspection 8,000 Number of inspections 400 inspections $20 per inspection Building 7,000 Machine hours 3,500 machine hours $2 per machine hour Packaging 5,000 Packaging hours 1,000 packaging hours $5 per packaging hour $30,000

24. The example in Table 2 shows that Product B’s overhead cost was lower than Product A’s. The primary reason for this difference is that Product A requires more setups and inspections than Product B. The information about production requirements and the accuracy of the product unit cost that the ABC costing method yields provide managers with valuable insights. Table 2 Product A Product B Actual Activit Cost y Cost Driver Cost Activity Pool Rate Level Applied Actual Cost Driver Level Cost Applied Setup $100 70 $ 7,000 30 $ 3,000 Inspection 20 250 5,000 150 3,000 Building 2 1,500 3,000 2,000 4,000 Packaging 5 300 1,500 700 3,500 Total $16,500 $13,500 ÷ by Number of units 1,000 2,000 = Overhead cost per unit $16.50 $6.75