Between Microfinance and Small and Medium-Sized Enterprise Finance in South Asia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jftlvªh Laö Mhö ,Yö&33004@99 Vlk/Kj.K Hkkx II

jftLVªh laö Mhö ,yö&33004@99 REGD. NO. D. L.-33004/99 vlk/kj.k EXTRAORDINARY Hkkx II—[k.M 3 —mi&[k.M (ii) PART II—Section 3—Sub-section (ii) izkf/dkj ls izdkf'kr PUBLISHED BY AUTHORITY la- 363 ] ubZ fnYyh] lkseokj] tuojh 28] 2019@ek?k 8] 1940 No. 363] NEW DELHI, MONDAY, JANUARY 28, 2019/MAGHA 8, 1940 िवē मंJालय (((िवēीय सेवाएं िवभाग ))) अिधसूचना नई Ƙदली , 28 जनवरी, 2019 काकाका.का ...आआआआ.... 476476((((अअअअ))))....—कĞLीय सरकार का राƎीय कृिष और =ामीण िवकास बġक (नाबाडϕ), तिमल नाडु सरकार और इंिडयन बġक तथा इिडयन ओवरसीज़ बġक जो , पलवन =ामा बġक और पांिडयन =ामा बġक के Oायोजक बġक हġ, से परामशϕ करने के प चात यह िवचार है Ƙक जनिहत और उपयुϕŎ Oादेिशक =ामीण बġकĪ ůारा िजन ϓेJĪ मĞ सेवा दी जा रही है, उन ϓेJĪ के िवकास के िहत मĞ तथा वयं उŎ Oादेिशक =ामीण बġकĪ के िहत मĞ यह आवयक है Ƙक उŎ Oादेिशक =ामीण बġकĪ को एकल Oादेिशक =ामीण बġक मĞ समामेिलत Ƙकया जाना चािहए ; अत:, कĞLीय सरकार अब Oादेिशक =ामीण बġक अिधिनयम , 1976 (1976 का 21) (िजसे इसमĞ इसके पƇात 'अिधिनयम' कहा गया है) कƙ धारा 23 क कƙ उपधारा (1) ůारा Oदē शिŎयĪ का Oयोग करते ćए उŎ Oादेिशक =ामीण बġकĪ को एकल Oादेिशक =ामीण बġक मĞ समामेिलत करने का उपबंध करती है जो ऐसे गठन, संपिē , शिŎ , अिधकार, िहतĪ , OािधकारĪ और िवशेषािधकारĪ ; तथा ऐसी देयताĸ , कतϕƆĪ और दाियवĪ जो नीचे िविनƠदƍ हġ, के साथ अOैल , 2019 का पहला Ƙदन से Oभावी होगा (िजसे इसमĞ इसके पƇात 'समामेलन कƙ Oभावी तारीख़’ कहा गया है):- 1. -

India Financial Checks

INDIAN FINANCIAL CHECKLIST Student name Date of Birth Agent (Agency) Business Name You should provide evidence of funds as outlined below. This checklist will assist you to calculate required funds. For information on the financial capacity requirement see http://www.border.gov.au/Trav/Stud/More/Student-Visa-Living-Costs- and-Evidence-of-Funds. Instructions: Please complete this checklist and return it together with your financial documents requested to [email protected] All documents must be certified by the Financial Institution, Bank, a Notary Public or your Education Agent. If you are providing bank statements, they must be for the last 6 months ONLY and should be a summary. No more than 10 pages will be accepted. Expenses Required funds (AUD) Funds available (Please specify in AUD) Funds required for your 12 months’ tuition and living costs AUD $55,000 Add for accompanying dependants Spouse or partner Please add $7,362 Children Please add $3,152 per child TOTAL (AUD) Evidence of Financial Capacity – You must provide one of the following Sufficient funds to cover your travel costs and 12 months of living and tuition fees for you (as above AUD $55,000) plusplusplus accompanying and your family members and school costs for any school aged dependents . Source of funds Acceptable evidence includes: • Your bank statements or deposit certificates from a recognised financial institution • A signed undertaking from a private sponsor that includes an explanation of the relationship between the applicant and sponsor and evidence of financial capacity as above (maximum of 2 sponsors). Note: For married couples, if main applicant is male, funds must be from male side of the family. -

Indian Overseas Bank Minutes of the 149Th Meetings of SLBC Held on 23.03.2017

State Level Bankers’ Committee, Tamil Nadu Convenor: Indian Overseas Bank Minutes of the 149th Meetings of SLBC Held on 23.03.2017 The 149th meeting of SLBC, Tamil Nadu was held at Chennai on 23rd March, 2017. List of participants is furnished in the Annexure. The meeting was chaired by Shri.R.Subramania Kumar, ED with Addl. Charge MD & CEO, Indian Overseas Bank. Welcome Address:- Shri.M.M.Sarangi, General Manager, Indian Overseas Bank and Convenor, SLBC, Tamil Nadu, welcomed the participants to the 149th meeting of SLBC, Tamil Nadu. He has highlighted the various special SLBC meetings and Sub committee meetings organised by SLBC after the 148th meeting. He briefed the forum about the various measures taken for providing relief to the farmers affected by drought in terms of RBI’s Master Circular. He informed that SLBC has conducted special meeting to discuss the various relief measures to be provided in the drought affected areas. He advised the banks to instruct their branches in the state to ensure that necessary relief is provided to all the eligible accounts within the stipulated time of 3 months as per RBI guidelines. He informed the forum that Government of Tamil Nadu has issued necessary notification of area / crops for Rabi season 2016. He informed that the notification has already been circulated to all the member banks. He appealed to the member banks to advise all their branches in the State to ensure that all loans extended for cultivation of the notified crops in the notified areas are covered under PMFBY. Convenor, SLBC advised Public sector Banks to advise their branches to participate actively in disbursement of MUDRA loans and achieve the annual target given to each bank under the three MUDRA schemes namely “Shishu, Kishore, and Tarun”. -

List of Banks for the Purpose of Proof of Address and Photo Identity for Passport Application

ANNEXURE List of Banks for the purpose of proof of Address and Photo identity for Passport Application A. PUBLIC SECTOR BANKS 1. AIlahabad Bank 31. Gramin Bank of Aryavart 2. Andhra Bank 32. Assam Gramin Vikash Bank 3. Bank of Baroda 33. Bangiya Gramin Vikash Bank 4. Bank of India 34. Baroda Gujarat Gramin Bank 5. Bank of Maharashtra 35. Baroda Rajasthan Kshetriya Gramin 6. Canara Bank Bank 7. Central Bank of India 36. Baroda. U P Gramin Bank 8. Corporation Bank 37. Bihar Gramin Bank 9. Dena Bank 38. Central Madhya Pradesh Gramin 10. Indian Bank Bank 11. Indian Overseas Bank 39. Chaitanya Godavari Grameena Bank 12. Oriental Bank of Commerce 40. Chhattisgarh Rajya Gramin Bank 13. Punjab National Bank 41. Deccan Grameena Bank 14. Punjab & Sind Bank 42. Dena Gujarat Gramin Bank 15. Syndicate Bank 43. Ellaquai Dehati Bank 16. Union Bank of India 44. Himachal Pradesh Gramin Bank 17. United Bank of India 45. Jharkhand Gramin Bank 18. UCO Bank 46. Jammu And Kashmir Gramin Bank 19. Vijaya Bank 47. Karnataka Vikas Grameena Bank 20. IDBI Bank Ltd 48. Kashi Gomti Samyut Gramin Bank 21. State Bank of India 49. Kaveri Grameena Bank 22. State Bank of Bikaner & Jaipur 50. Kerala Gramin Bank 23. State Bank of Patiala 51. Langpi Dehangi Rural Bank 24. State Bank of Hyderabad 52. Madhyanchal Gramin Bank 25. State Bank of Mysore 53. Maharashtra Gramin Bank 26. State Bank of Travancore 54. Malwa Gramin Bank 55. Manipur Rural Bank B. LIST OF REGIONAL RURAL BANKS 56. Marudhara Rajasthan Gramin Bank 57. Meghalaya Rural Bank 27. -

Default Entities-28092015.Xlsx

List of intermediaries yet to submit the Grievance Policy under non-Government Sector SL Name of Intermediary Type 1 National Aluminium Company Limited Direct Corporate 2 Assam Electricity Grid Corporation Limited Direct Corporate 3 Assam Power Generation Corporation Limited Direct Corporate 4 Assam Power Distribution Company Limited Direct Corporate 5 Chattisgarh State Power Transmission Company Limited Direct Corporate 6 Chhattisgarh State Power Distribution Company Limited Direct Corporate 7 Chhattisgarh State Power Generation Company Limited Direct Corporate 8 Konkan Railway Corporation Limited Direct Corporate 9 Doamodar Valley Corporation Direct Corporate 10LIC Pension Fund Limited PFM 11 SBI Pension Funds Pvt. Ltd PFM 12UTI Retirement Solutions Ltd PFM 13SHCIL Custodian 14 Life Insurance Corporation of India ASP 15 SBI Life Insurance Co. Ltd. ASP 16 ICICI Prudential Life Insurance Co. Ltd. ASP 17 HDFC Standard Life Insurance Co Ltd ASP 18 Bajaj Allianz Life Insurance Co. Ltd. ASP 19 Reliance Life Insurance Co. Ltd. ASP 20 Allahabad Bank POP 21 Andhra Bank POP 22 Bank of Baroda POP 23 Bank of Maharashtra POP 24 Central Bank of India POP 25 Corporation Bank POP 26 Dena Bank POP 27 India Infoline Finance Ltd POP 28 India Post NPS Nodal Office POP 29 Indian Bank POP 30 Indian Overseas Bank POP 31 Karvy Financial Services Limited POP 32 Muthoot Finance Limited POP 33 Punjab and Sind Bank POP 34 Punjab National Bank POP 35 Reliance Capital Limited POP 36 State Bank of Bikaner & Jaipur POP 37 State Bank of India POP 38 State Bank of Mysore POP 39 State Bank of Patiala POP 40 State Bank of Travancore POP 41Union Bank Of India POP 42 United Bank of India POP 43 UTI Asset Management Company Limited POP 44 UTI Infrastructure Technology And Services Limited POP 45 Ventura Securities Ltd. -

Regional Rural Banks Allahabad up Gramin Bank Andhra Pradesh

Regional Rural Banks Allahabad UP Gramin Bank Andhra Pradesh Grameena Vikas Bank Andhra Pragathi Grameena Bank Arunachal Pradesh Rural Bank Aryavart Gramin Bank Assam Gramin Vikash Bank Baitarani Gramya Bank Ballia –Etawah Gramin Bank Bangiya Gramin Vikash Bank Baroda Gujarat Gramin Bank Baroda Rajasthan Gramin Bank Baroda Uttar Pradesh Gramin Bank Bihar Kshetriya Gramin Bank Cauvery Kalpatharu Grameena Bank Chaitanya Godavari Grameena Bank Chhattisgarh Gramin Bank Chikmagalur-Kodagu Grameena Bank Deccan Grameena Bank Dena Gujarat Gramin Bank Durg-Rajnandgaon Gramin Bank Ellaquai Dehati Bank Gurgaon Gramin Bank Hadoti Kshetriya Gramin Bank Haryana Gramin Bank Himachal Gramin Bank Jaipur Thar Gramin Bank Jhabua Dhar Kshetriya Gramin Bank Jharkhand Gramin Bank Kalinga Gramya Bank Karnataka Vikas Grameena Bank Kashi Gomti Samyut Gramin Bank Kerala Gramin Bank Krishna Grameena Bank Kshetriya Kisan Gramin Bank Langpi Dehangi Rural Bank Madhumalti Building Gupte Marg Madhya Bharat Gramin Bank Madhya Bihar Gramin Bank Mahakaushal Kshetriya Gramin Bank Maharashtra Gramin Bank Malwa Gramin Bank Manipur Rural Bank Marwar Ganganagar Bikaner Gramin Bank Meghalaya Rural Bank Mewar Anchalik Gramin Bank Mizoram Rural Bank Nagaland Rural Bank Uttrakhand Gramin Bank[1] Narmada Malwa Gramin Bank Neelachal Gramya Bank Pallavan Grama Bank Pandyan Grama Bank Parvatiya Gramin Bank Paschim Banga Gramin Bank Pragathi Gramin Bank Prathama Bank Puduvai Bharathiar Grama Bank Pune District Central Cooperative Bank Ltd. Punjab Gramin Bank Purvanchal Gramin Bank Rajasthan Gramin Bank Rewa-Sidhi Gramin Bank Rushikulya Gramya Bank Samastipur Kshetriya Gramin Bank Saptagiri Grameena Bank Sarva UP Gramin Bank Satpura Narmada Kshetriya Saurashtra Gramin Bank Sharda Gramin Bank Shreyas Gramin Bank Surguja Kshetriya Gramin Bank Sutlej Kshetriya Gramin Bank Tripura Gramin Bank Utkal Gramya Bank Uttar Banga Kshetriya Gramin Bank Uttar Bihar Gramin Bank Vananchal Gramin Bank Vidharbha Kshetriya Gramin Bank Visveshvaraya Grameena Bank Wainganga Krishna Gramin Bank. -

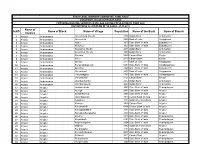

S.NO Name of District Name of Block Name of Village Population Name

STATE LEVEL BANKERS' COMMITTEE, TAMIL NADU CONVENOR: INDIAN OVERSEAS BANK PROVIDING BANKING SERVICES IN VILLAGE HAVING POPULATION OF OVER 2000 DISTRICTWISE ALLOCATION OF VILLAGES -01.11.2011 Name of S.NO Name of Block Name of Village Population Name of the Bank Name of Branch District 1 Ariyalur Andiamadam Anikudichan (South) 2730 Indian Bank Andimadam 2 Ariyalur Andiamadam Athukurichi 5540 Bank of India Alagapuram 3 Ariyalur Andiamadam Ayyur 3619 State Bank of India Edayakurichi 4 Ariyalur Andiamadam Kodukkur 3023 State Bank of India Edayakurichi 5 Ariyalur Andiamadam Koovathur (North) 2491 Indian Bank Andimadam 6 Ariyalur Andiamadam Koovathur (South) 3909 Indian Bank Andimadam 7 Ariyalur Andiamadam Marudur 5520 Canara Bank Elaiyur 8 Ariyalur Andiamadam Melur 2318 Canara Bank Elaiyur 9 Ariyalur Andiamadam Olaiyur 2717 Bank of India Alagapuram 10 Ariyalur Andiamadam Periakrishnapuram 5053 State Bank of India Varadarajanpet 11 Ariyalur Andiamadam Silumbur 2660 State Bank of India Edayakurichi 12 Ariyalur Andiamadam Siluvaicheri 2277 Bank of India Alagapuram 13 Ariyalur Andiamadam Thirukalappur 4785 State Bank of India Varadarajanpet 14 Ariyalur Andiamadam Variyankaval 4125 Canara Bank Elaiyur 15 Ariyalur Andiamadam Vilandai (North) 2012 Indian Bank Andimadam 16 Ariyalur Andiamadam Vilandai (South) 9663 Indian Bank Andimadam 17 Ariyalur Ariyalur Andipattakadu 3083 State Bank of India Reddipalayam 18 Ariyalur Ariyalur Arungal 2868 State Bank of India Ariyalur 19 Ariyalur Ariyalur Edayathankudi 2008 State Bank of India Ariyalur 20 Ariyalur -

REGIONAL RURAL BANKS Staff-In-Charge: Dr.R.Mahara Jothi Priya Associate Professor and Head REGIONAL RURAL BANKS UNIT - 1

DEPARTMENT OF B.COM BANKING & INSURANCE SUBJECT: INDIAN BANKING SYSTEM TOPIC: UNIT 1: REGIONAL RURAL BANKS Staff-in-charge: Dr.R.Mahara Jothi Priya Associate Professor and Head REGIONAL RURAL BANKS UNIT - 1 MEANING • Regional Rural Banks(RRBs) are Indian ScheduledCommercialBanks (Government Ba nks) operating at regional level in different States of India. They have been created with a view of serving primarily the rural areas of India with basic banking and financial services. • Providing banking facilities to rural and semi- urban areas. FUNCTIONS • Carrying out government operations like disbursement of wages of MGNREGA workers, distribution of pensions etc. • Providing Para-Banking facilities like locker facilities, debit and credit cards,mobile banking,internet banking,UPI etc. • Small financial banks. CONCEPTS OF RRB • Regional Rural Banks were established under the provisions of an Ordinance passed on 26th September,1975 and the RRB Act 1976 to provide sufficient banking and credit facility for agriculture and other rural sectors • As a result Five Regional Rural Banks were set up on 2nd October,1975,Gandhi Jayanti • The Regional Rural Banks were owned by the Central Government, the State Government and the Sponsor Bank (Any commercial bank can sponsor the regional rural banks) who held shares in the ratios as follows Central Government – 50%, State Government – 15% and Sponsor Banks – 35%. ORGANISATION STRUCTURE • The organizational structure for RRB's varies from branch to branch and depends upon the nature and size of business done by the branch. The Head Office of an RRB normally had three to nine departments. • The following is the decision making hierarchy of officials in a Regional Rural Bank. -

DIGITAL PAYMENTS BOOK Part1

DIGITAL PAYMENTS Trends, Issues And Opportunities July 2018 FOREWORD A Committee on Digital Payments was growth figures for both volume and value. constituted by Department of Economic Notwithstanding this the analysis finds that Affairs, Ministry of Finance in August 2016 both the data are relevant and equally under my Chairmanship to inter-alia important. They are complementary. In recommend medium term measures of addition to this the underlying growth trends promotion of Digital Payments Ecosystem in Digital Payments over the last seven in the country. The Committee submitted its years are also covered in this booklet. final report to Hon’ble Finance Minister in December 2016. One of the key This booklet has some new chapters which recommendations of the Committee related cover the areas of policy developments, to development of a metric for Digital global trends and opportunities in Digital Payments. As a follow-up on this a group of Payments. In the policy space the important Stakeholders from Different Departments of developments with respect to the Government of India and RBI was amendment of the Payment and Settlement constituted in NITI Aayog under my Act 2007 are covered. chairmanship to facilitate the work relating I am grateful to Governor, RBI, Secretary to development of the metric. This group MeitY and CEO, NPCI for their support in prepared a document on the measurement preparing this booklet. Shri. B.N. Satpathy, issues of Digital Payments. Accordingly, a Senior Consultant, EAC-PM and Shri. booklet titled “Digital Payments: Trends, Suneet Mohan, Young Professional, NITI Issues and Challenges” was prepared in Aayog have played a key role in compiling May 2017 and was released by me in July this booklet. -

46 Indian Bank Investor Services Cell FAX� : 28134075 254-260, Avvai Shanmugam Salai PHONE : 28134076 Royapettah E-Mail : [email protected] Chennai 600 014

ei. Corporate Office 46 Indian Bank Investor Services Cell FAX : 28134075 254-260, Avvai Shanmugam Salai PHONE : 28134076 Royapettah E-mail : [email protected] Chennai 600 014 Ref : ISC /(©7/ 2019-20 06.06.2019 The Vice President The Manager National Stock Exchange of India B S E Limited Limited Phiroze Jeejibhai Towers "Exchange Plaza", Bandra Kuria Dalai Street Complex, Bandra East Mumbai - 400 001. Mumbai - 400 051. Scrip Code : 532814 NSE Symbol: INDIANB Dear Sir, Sub : Annual Report of the Bank for the year 2018-19. In compliance to Regulation 34(1) of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, we are herewith submitting the Annual Report of the Bank for the year 2018-19. We request you to take the same on record. Yours faithfully. (Bimal ti.bh) Company Secretary & Compliance Officer funs'kd eaMy BOARD OF DIRECTORS in~etk pqUMw: çcaèk funs'kd ,oa eq[; dk;Zikyd vfèkdkjh PADMAJA CHUNDURU MANAGING DIRECTOR & CEO ,e- ds- HkV~Vkpk;Z 'ks.kkW; fo'oukFk oh dk;Zikyd funs'kd dk;Zikyd funs'kd M K BHATTACHARYA SHENOY VISHWANATH V EXECUTIVE DIRECTOR EXECUTIVE DIRECTOR vfer vxzoky ,l ds ikf.kxzgh fot; dqekj xks;y AMIT AGRAWAL S K PANIGRAHY VIJAY KUMAR GOEL Lkyhy dqekj >k fouksn dqekj ukxj Hkjr Ñ".k 'kadj SALIL KUMAR JHA VINOD KUMAR NAGAR BHARATH KRISHNA SANKAR eq[; lrdZrk vf/kdkjh / CHIEF VIGILANCE OFFICER lq/kkdj vkj v;~;j / Sudhakar R Iyer egkizca/kdx.k / GENERAL MANAGERS mn; HkkLdj jsìh ds ukxjktu ,e psfG;u ,l y{ehifr jsìh th Udaya Bhaskara Reddy K Nagarajan M Chezhian S Lakshmipathy Reddy G xksiky -

Sl.No. Salutation Name Designation Organisation / Department I CHAIRMAN Executive Director with Addl

STATE LEVEL BANKERS' COMMITTEE, TAMIL NADU CONVENOR : INDIAN OVERSEAS BANK 148 th STATE LEVEL BANKERS' COMMITTEE HELD ON 16.12.2016 LIST OF PARTICIPANTS Sl.No. Salutation Name Designation Organisation / Department I CHAIRMAN Executive Director with Addl. charge of 1 Mr. R.Subramaniakumar MD & CEO Indian Overseas Bank II GOVERNMENT OF INDIA 2 Mr. A.K.Dogra Deputy Secretary Dept. of Financial Services II GOVERNMENT OF TAMILNADU AND RELATED DEPARTMENTS / AGENCIES 3 Mr. K.Shanmugam, IAS Additional Chief Secretary (Finance) Govt. of Tamil Nadu 4 Mr. Kumar Jayant,IAS Managing Director TAHDCO 5 Ms. Rita Harish Thakkar, IAS Addl.Commissioner Industries & Commerce 6 Ms. Lalitha R, IAS Dy.Secretary Food & Coop Dept 7 Mr. K.S.Santhalingam A.D (FI) MSME Dt 8 Mr. R.Ekambaram Addl Director Industries & Commerce Dept 9 Mr. S.Annamalai JD TNCDW 10 Mr. M.Subburaj Jt. Director of Fisheries Fisheries Dept 11 Ms. G.Jayalakshmi Jt.Director Directorate of Social Welfare 12 Mr. G.Srinivasa Rao Jt.Director (Credit) TNCDW 13 Mr. S.Nagaraj Jt.Director, OSD Handloom & Textiles 14 Mr. M.Narayanasamy DD Agriculture Dept. Directorate of Agriculture 15 Mr. S.Arun kumar Asst Director (Funds) Directorate of Ex.Service Men's welfare 16 Mr. C.Baskar Asst Director KVIC 17 Mr. N.Nagaraj Asst Director 18 Dr. S.Muzamil Rafeek MVSC Asst Director AH Dept 19 Mr. M.Chinna Thambi Asst Director KVIC, Chennai 20 Mr. A.Nagarajan Asst Director of Sericulture Govt. Anna Silk Exchange , Kancheepuram 21 Ms. C.Poongothai ED, TNSFAC Dept of Agri Marketing 22 Mr. B.Lindsy Jesudial Financial Controller Adi Dravida & Tribal Dept 23 Mr. -

Non-Official Directors on the Board of Regional Rural Banks(Rrbs) As on 30.6.2014

Non-Official Directors on the Board of Regional Rural Banks(RRBs) as on 30.6.2014 Sr. Name of Non Official Director Name of RRB on which appointed Date of appointment No. 1 2 3 4 1 Shri C.L. Naidu Andhra Pradesh Grameena Vikas Bank 29.5.2013 2 Shri Surender Reddy Maturu Andhra Pragathi Grameena Bank 29.5.2013 3 Shri Baidya Nath Sharma Uttar Bihar Gramin Bank 29.5.2013 4 Shri Surya Sinhji – Laxman Sinhji Dena Gujarat Gramin Bank 29.5.2013 5 Shri Rapolu Jaya Prakash Chaitanya Godavari Grameena Bank 29.5.2013 6 Shri A Rasool Mohideen Pandyan Grama Bank 29.5.2013 7 Shri S Suresh Pandyan Grama Bank 29.5.2013 8 Shri Ashwani Kumar Batta Malwa Gramin Bank 15.7.2013 9 Shri Jatin Kumar Prem Singh Baroda Gujarat Gramin Bank 22.8.2013 10 Shri Venga Hanumantha Reddy Andhra Pradesh Grameena Vikas Bank, 22.8.2013 Warangal 11 Shri B.S. Slatia J & K Grameen Bank, Jammu 22.8.2013 12 Shri Ambaraya Aashtagi Kaveri Grameena Bank, Mysore 22.8.2013 13 Shri Shashank Bhargava Central Madhya Pradesh Gramin Bank, 22.8.2013 Chhindwara 14 Shri Ritesh Jaiswal Narmada Jhabua Gramin Bank, Indore 22.8.2013 15 Shri Subhankar Mohpatra Odisha Gramya Bank, Bhubaneswar 22.8.2013 16 Shri Pramod Kumar Mishra Utkal Grameen Bank, Bolangir 22.8.2013 17 Ms. Romila Bansal Punjab Gramin Bank, Kapurthala 22.8.2013 18 Shri Jai Parkash Saini Baroda Rajasthan Kshetriya Gramin Bank, 22.8.2013 Ajmer 19 Shri Satyendra Pratap Singh Baroda UP Gramin Bank, Raibareli 22.8.2013 20 Shri Arun Yadav Kashi Gomti Samyut Gramin Bank 22.8.2013 Sr.