Investor Kit 1H 2016 COMPANY STRUCTURE a Focused Vehicle for AGI’S Property Interests

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos. (02) 8 376-4039, (02) 8 376-4072, (02) 8 376-4044, (02) 8 332-2353, (02) 8 332-2341, (02) 8 376-5430 Locals 115, 116, 117 and look for Ms. Julie Ann G. Blanquisco or Ms. Marivic A. Dela Torre-Santos E-mail: [email protected] | [email protected] Website: http://llda.gov.ph List of APPROVED DISCHARGE PERMITS as of September 03, 2021 Establishment Address Permit No. Approve Date 11 FTC Enterprises, Inc. 236 P. Dela Cruz San Bartolome Quezon City MM DP-25b-2021-03532 August 18, 2021 189 Realty Corp. (CI Market) Qurino Highway Santa Monica, Novaliches Quezon City MM DP-25b-2021-03744 August 20, 2021 189 Realty Corporation - 2nd (CI Market/Commercial Complex) Quirino Highway, Sta. Monica Novaliches Quezon City MM DP-25b-2021-03743 August 20, 2021 21st Century Mouldings Corporation 18 F. Carlos St. cor. Howmart Road Apolonio Samson Quezon City MM DP-25b-2021-03541 August 23, 2021 24K Property Ventures, Inc. (20 Lansbergh Place Condominium) 170 T. Morato Ave. cor. Sct. Castor Sacred Heart Quezon City MM DP-25b-2021-02819 July 15, 2021 3J Foods Corp. Sta. Ana San Pablo City Laguna DP-16d-2021-03174 August 06, 2021 8 Gilmore Place Condominium 8 Gilmore Ave. cor. 1st St. Valencia New Manila Quezon City MM DP-25b-2021-03829 August 27, 2021 AC Technical Services, Inc. 5 RMT Ind`l. Complex Tunasan Muntinlupa City MM DP-23a-2021-01804 May 12, 2021 Ace Roller Manufacturing, Inc. -

Caltex Stations As of 23 June 2020

CHEVRON (CALTEX) STATIONS IMPLEMENTING THE 10% TARIFF Estimated Address Estimated No. Retailer Name Date * Source Depot Tariff Province City/Municipality Diesel 1 RDL FUEL POINT INC. Valenzuela North Expressway, Malinta, Valenzuela 24-Jun-20 Batangas P1.71/liter 2 NORTH WEST STAR GAS CORP.-WILSON San Juan Ortigas Ave / Wilson St., San Juan 24-Jun-20 Batangas P1.71/liter 3 ACHIEVERS MCKINLEY San Juan Ortigas Ave/McKinley, San Juan 24-Jun-20 Batangas P1.71/liter 4 STAREV MOTORIST SERVICE CENTER Mandaluyong EDSA / Boni Ave, Mandaluyong City 24-Jun-20 Batangas P1.71/liter 5 RDL FUEL POINT INC. Makati EDSA/Harvard, Makati City 24-Jun-20 Batangas P1.71/liter 6 DON DEXTER- SLEX Laguna San Antonio, San Pedro, Laguna 24-Jun-20 Batangas P1.71/liter 7 NORTHERN STAR ENERGY AND FUEL Pasig Pioneer/Shaw Blvd, Pasig City 24-Jun-20 Batangas P1.71/liter 8 RDL FUEL POINT INC. Pampanga San Fernando, Pampanga 24-Jun-20 Mariveles P1.71/liter Mcarthur Highway, Barrio Dolores, San Fernando, 9 RDL FUEL POINT DISTRIBUTION Pampanga 24-Jun-20 Mariveles P1.71/liter Pampanga 10 MARIA MAY ORINO LEE Bicol Goa, Camarines Sur 24-Jun-20 Batangas P1.71/liter Ochoa St. Cor. L. Jaena St.,Butuan City, Agusan 11 GARDENSTATE ENTERPRISES INC. Agusan 24-Jun-20 Cabadbaran P1.71/liter Norte 12 IRON CITY STATION Surigao Claver, Surigao del Norte 24-Jun-20 Cabadbaran P1.71/liter 13 ANELYN DAUBNEY Zamboanga Tampilisan, Zamboanga Del Norte 24-Jun-20 Jimenez P1.71/liter National Highway, Tiniguiban, Puerto Princesa, 14 WILLIAM TAN ENT. -

REGIONAL REPORT on the APPROVED CONSTRUCTION SAFETY & HEALTH PROGRAM (CSHP) DOLE-National Capital Region

REGIONAL REPORT ON THE APPROVED CONSTRUCTION SAFETY & HEALTH PROGRAM (CSHP) DOLE-National Capital Region April 2017 No. Company Name and Address Project Name Date Approved Jesreel Alday/ Ametricia Trading Demolition of Bungalow 1 3-Apr-2017 1345 Joasmerreay Subd., Putatan, Muntinlupa City L1 B3 Bruger St., Bruger Subd., Putatan, Muntinlupa City Windy G. Gomez Renovation of Residential/ Roofing 2 3-Apr-2017 Mercury St., Bel-Air Village, Makati City #316 C Sto. Rosario St., Brgy. Plainview, Mandaluyong City Jocelyn Delgado Proposed Two (2) Storey Duplex 3 B1 Lot 27 Vatican St., Annex 43 BLS, Brgy. Don Bosco, B1 Lot 47 Vatican St., Annex 43 BLS, Brgy. Don Bosco, 3-Apr-2017 Paranaque City Paranaque City Manuel Co/ Magic World Development Corp. Demolition of Two (2) Storey Residential 4 3-Apr-2017 321 Dasmarinas St., Binondo, Manila 22 Jefferson St., Green Hills West, San Juan City Julieta Dizon Proposed Two(2) Storey Residence 5 3-Apr-2017 M. Dela Cruz St., Pasay City M. Dela Cruz St., Pasay City Alfonso Javier Two (2) Storey Residential 6 #29 Tagbilaran St., Alabang Hills Village, Cupang, Muntinlupa 3-Apr-2017 #29 Tagbilaran St., Alabang Hills Village, Cupang, Muntinlupa City City Residential House Construction Mr. & Mrs. Archie S. Mendoza 7 5 San Miguel Bay Drive, South Bay Gardens Subd., Villongco 3-Apr-2017 33 Syndey St., BF Paranaque PH. VI, Las Pinas City Road, Sucat, Paranaque City Proposed Two (2) Storey, Six (6) Units Residential Bldg., with Euland & Dayan Castillo Roofdeck 8 3-Apr-2017 St. James St., San Agustin, Moonwalk, Paranaque City Lot 13-E PSD 13-00316 Sta.Clara St., Daang Batang, Brgy. -

Metro Manila Market Update Q4 2018

RESEARCH METRO MANILA MARKET UPDATE Q4 2018 METRO MANILA REAL ESTATE SECTOR REVIEW FDI RISES AS NEIGHBORING COUNTRIES CONTINUE TO BET ON “ASIA’S RISING TIGER” COVER | The Philippines remains a popular investment destination for Asian investors FIGURE 1 Net Foreign Direct Investment Level By Country of Origin (in USD Mn) 905.65 SNAPSHOTS 900 750 2017 2018 Economic Indicators 600 450 384.25 263.97 300 189.33 183.51 64.4 150 13.25 8.56 6.1% 0 GDP SINGAPORE HONGKONG CHINA JAPAN Q4 2018 Source: Bangko Sentral ng Pilipinas The Philippines continues to attract Foreign Direct Investments (FDI) as formulates policies that will limit the economy carries on constraints in doing business in the experiencing growth of above 6% 6.1% country. On October 2018, the 11th Inflation Rate for the past 7 consecutive years. Regular Foreign Investment December 2018 The growth was mainly brought Negative List was amended to about by the increase in include five areas that will allow government spending from the 100% foreign investment present administration’s “Build, participation. The list includes Build, Build” infrastructure program. internet businesses (as excluded from mass media), teaching at 3.1% At the end of 2017, the Philippines higher education levels provided the OFW Remittances posted the highest rise in Foreign subject being taught is not a November 2018 Direct Investments (FDI) among professional subject (i.e., included in a government board or bar ASEAN countries. FDI remains examination), training centers that robust as investments increased by are engaged in short-term high- 42% in the first half of 2018. -

REAL ESTATE MARKET INSIGHTS August 2018 Executive Summary

REAL ESTATE MARKET INSIGHTS August 2018 Executive Summary • Philippine office supply is forecasted to grow by 46% in the next 6 years adding 5.28 million to the current supply of 11.58 million. • 688,474 square meters of the 2018 office supply are already either leased or pre- committed. This makes our forecasted FY 2018 take-up of 937,000 square meters achievable. • The IT-BPM industry, which includes shared services, took up 46% of FY 2017 demand, while Offshore/Online Gaming took up 30%. The IT-BPM industry is expected to rebound while the Offshore/Online Gaming is expected to grow this 2018. • Rents and land values remain at all-time high across most districts. • China has become a significant investor in economies all over the world. • AI will benefit diverse industries primarily healthcare/medical sciences, agriculture, environment, banking and finance. • Tourism has the potential to be one of the biggest drivers of the Philippine economy. • Developers, investors, and stakeholders must all partake in credible, sensible, and sustainable Masterplanning. 2 METRO MANILA OFFICE MARKET Metro Manila Cityscapes • Most of these districts will be fully developed by 2018. • There will be little land left for development. • The most important districts moving forward will be Bonifacio Global City, Bay Area, Filinvest City, Evia and Arca South. Quezon City 3 MAJOR CBDs MAKATI MAKATI CBD. CENTURY CITY. ROCKWELL CENTER. CIRCUIT MAKATI. San Juan Manila ORTIGAS ORTIGAS CBD. ROCKWELL BUSINESS CENTER. ARCOVIA CITY. SILVER CITY. CAPITOL COMMONS. Manda- luyong Ortigas/ BGC BONIFACIO GLOBAL CITY. MCKINLEY WEST. MCKINLEY HILL. Pasig UPTOWN. VERITOWN. Makati Bay/ Pasay BGC / Taguig 46 BUSINESS PARKS QUEZON CITY. -

Project Brief

GEM RESIDENCES Every single day, SM touches the lives of millions of people through its stores, malls, banks, hotels and leisure facilities. PROJECTAnd nowBRIEFFilipinos can live in style comfort and convenience at SM Development Corporation (SMDC). SMDC commits itself to provide access to luxuriousurban living throughvertical villages perfectly integrated with a commercial retail environment,giving its resident’s atruly cosmopolitanlifestyle. SMDC Developments are strategicallysituated in key areas across Metro Manila specifically the Central Business Districts of Mall of Asia Complex, Makati, Ortigas, Taguig, Quezon City,Manila, Pasay, Parañaque and Las Piñas. “For training purposes only. This material may be subject to change and not for reproduction and distribution without prior consent of the developer.” Value Proposition Gem Residences is a precious find, a home with a strategic albeit off CBD location that shows immediate accessibility to work, all the while providing its residents the luxury of having a psychological headspace from the busy professional’s work environment. Gem Residences features thoughtfully designed facilities and amenities to promote a sense of balance, connectivity and productivity, addressing the various demands of the multi-faceted lives of GEMtoday’s youngRESIDENCES urban professional. PROJECTBRIEF A home to be treasured that allows residents to blissfully move between different facets of one’s life, be it work or play in seamless harmony. “For training purposes only. This material may be subject to change and not for reproduction and distribution without prior consent of the developer.” Metro Manila’s Rising Ecopolis Located at Metro Manila’s smart city with a green heart, and has been honored as one of the Most Liveable Cities in the world in 2013 by LivCom Awards and the 2018 Planet City Challenge winner of World Wild Life Funds’s Planet City Challenge. -

Caltex Stations As of 21 July 2020

List of Liquid Fuel Retail Stations or LPG Dealers Implementing the 10% Tariff (EO 113) Company: CHEVRON As of: July 21, 2020 Note: Passing on of additional import duties to retailers for diesel has ceased on July 9, 2020. This submission may change should there be local purchases that have levied the additional duties. Address Implementation Tariff Rate No. Retailer Name Source Depot Province City/Municipality Date (PhP) 1 RDL FUEL POINT INC. Valenzuela North Expressway, MalInta, Valenzuela 1.62 Batangas 2 NORTH WEST STAR GAS CORP.-WILSON San Juan OrtIgas Ave / WIlson St., San Juan 1.62 Batangas 3 ACHIEVERS MCKINLEY San Juan OrtIgas Ave/McKInley, San Juan 1.62 Batangas 4 STAREV MOTORIST SERVICE CENTER Mandaluyong EDSA / BonI Ave, Mandaluyong CIty 1.62 Batangas 5 RDL FUEL POINT INC. MakatI EDSA/Harvard, MakatI CIty 1.62 Batangas 6 DON DEXTER- SLEX Laguna San AntonIo, San Pedro, Laguna 1.62 Batangas 7 NORTHERN STAR ENERGY AND FUEL PasIg Pioneer/Shaw Blvd, PasIg CIty 1.62 Batangas 8 RDL FUEL POINT INC. Pampanga San Fernando, Pampanga 1.62 MarIveles 9 RDL FUEL POINT DISTRIBUTION Pampanga Mcarthur HIghway, BarrIo Dolores, San Fernando, Pampanga 1.62 MarIveles 10 MARIA MAY ORINO LEE Bicol Goa, CamarInes Sur 1.62 Batangas 11 GARDENSTATE ENTERPRISES INC. Agusan Ochoa St. Cor. L. Jaena St.,Butuan CIty, Agusan Norte 1.62 Cabadbaran 12 IRON CITY STATION SurIgao Claver, SurIgao del Norte 1.62 Cabadbaran 13 ANELYN DAUBNEY Zamboanga TampIlIsan, Zamboanga Del Norte 1.62 Jimenez 14 WILLIAM TAN ENT. INC. (TINIGUIBAN) Palawan NatIonal HIghway, TInIguIban, Puerto PrIncesa, Palawan 1.62 Batangas 15 WILLIAM TAN ENT. -

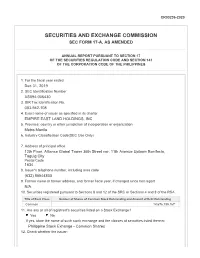

Securities and Exchange Commission Sec Form 17-A, As Amended

CR03236-2020 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended Dec 31, 2019 2. SEC Identification Number AS094-006430 3. BIR Tax Identification No. 003-942-108 4. Exact name of issuer as specified in its charter EMPIRE EAST LAND HOLDINGS, INC. 5. Province, country or other jurisdiction of incorporation or organization Metro Manila 6. Industry Classification Code(SEC Use Only) 7. Address of principal office 12th Floor, Alliance Global Tower 36th Street cor. 11th Avenue Uptown Bonifacio, Taguig City Postal Code 1634 8. Issuer's telephone number, including area code (632) 85544800 9. Former name or former address, and former fiscal year, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 14,676,199,167 11. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exhange - Common Shares 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports) Yes No (b) has been subject to such filing requirements for the past ninety (90) days Yes No 13. -

Project Brief

1st Philippine Conglomerate to breach PHP 1 Trillion in Market Capitalization RETAIL BANKS PROPERTY BANKING RETAIL PROPERTY OTHER INVESTMENTS GROUP COMPANY RANKINGS SMIC, SM Prime, and BDO comprise 30% of the value of the Philippine Index Philippine Conglomerates Philippine Retailers Philippine Banks Property Developers Market Cap (USD bn) FY 2018 Total Sales (USD mn) Total Resources (USD bn) Market Cap (USD bn) SMIC 24.5 SM Retail 6,145 BDO 59.6 SMPH 22.2 JG Summit 10.8 Puregold 2,675 Metrobank 45.0 Ayala Land 14.1 Ayala Corp 10.6 Robinsons 2,519 BPI 41.7 Megaworld 3.1 SMC 7.8 Landbank 35.8 Robinsons Land 2.6 Aboitiz Equity 6.2 PNB 21.2 Vistaland 1.9 GT Capital 3.8 Philippine Retailers China Bank 17.8 Double Dragon 0.9 Metro Pacific 3.0 FY 2018 Store Count Security Bank 15.3 Filinvest 0.8 LT Group 2.8 SM Retail 2,328 UBP 13.7 Alliance Global 2.2 Puregold 409 RCBC 13.3 DMCI 2.1 Robinsons 1,910 DBP 13.2 Source: Bloomberg; Source: Company Information end-2018 Source: Consolidated statements of Source: Bloomberg; Figures as of October 31, 2019 condition (SOC), 1H 2019 Figures as of October 31, 2019 1st Philippine Property Company to breach PHP 1 Trillion in Market Capitalization One E-com (2008) Sea Residences (2008) Two E-com Conrad Manila (2012) Shell Residences SM Arena (2016) (2011) (2012) Five E-com Shore SMX (2015) Residences Mall of Asia Convention (2017) (2006) Center, Manila (2007) EXPANDS TO CHINA EXPANDS TO CHINA SM Development Corporation commits itself to provide access to luxurious urban living through its vertical villages and gated horizontal communities, designed with thoughtful features and generous resort-like amenities, all perfectly integrated with a commercial retail environment, thus giving its residents access to a truly cosmopolitan lifestyle. -

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos. (02) 8 376-4039, (02) 8 376-4072, (02) 8 376-4044, (02) 8 332-2353, (02) 8 332-2341, (02) 8 376-5430 Locals 115, 116, 117 and look for Ms. Julie Ann G. Blanquisco or Ms. Marivic A. Dela Torre-Santos E-mail: [email protected] | [email protected] Website: http://llda.gov.ph List of APPROVED LLDA CLEARANCES as of September 03, 2021 Establishment Address Permit No. Approve Date 3 en 1 Water Refilling Station B7 L71 Laussane St. Malusak (Pob.) Santa Rosa City Laguna LE-20b-2020-00344 March 11, 2020 3MS Enterprises (Total Gas Station) M.H. del Pilar St. San Rafael Rodriguez Rizal PC-01a-2019-00549 January 25, 2021 4S Hiranand Food Corporation (Jollibee Tycoon Pearl Drive) Unit 103 A & B Tycoon Centre Condominium San Antonio Pasig City MM LE-24c-2019-01771 January 28, 2020 7Seven7 Oil & Petroleum Corporation Macabling Santa Rosa City Laguna PC-20b-2021-00658 August 02, 2021 8Alaginto Rice Trading L1 B92 Package 5 Phase 7 Bagong Silang Caloocan City MM LE-25d-2019-01333 January 08, 2020 ACS Manufacturing Corp. 105 Productivity Drive, CIP 1 Canlubang Calamba City Laguna LX-19a-2021-00103 February 17, 2021 Adsia Logistics Inc. 65 Elisco Road Kalawaan Pasig City MM LE-24c-2021-00695 August 20, 2021 AFQ Weldtek, Inc. 9022 F. Reyes St., Purok 6 Balibago Santa Rosa City Laguna PC-20b-2020-00625 October 14, 2020 Alaminos Stone Center Showroom (Trendstone Corporation) Purok 3 San Benito Alaminos Laguna LE-16c-2021-00193 March 08, 2021 Alibudbud Junkshop & Trading Cattleya St., LM Subd. -

Securities and Exchange Commission Sec Form 17-C

C03294-2021 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2(c) THEREUNDER 1. Date of Report (Date of earliest event reported) May 12, 2021 2. SEC Identification Number 167423 3. BIR Tax Identification No. 000-477-103 4. Exact name of issuer as specified in its charter MEGAWORLD CORPORATION 5. Province, country or other jurisdiction of incorporation Metro Manila 6. Industry Classification Code(SEC Use Only) 7. Address of principal office 30th Floor, Alliance Global Tower 36th Street cor. 11th Avenue Uptown Bonifacio, Taguig City Postal Code 1634 8. Issuer's telephone number, including area code (632) 8894-6300/640 9. Former name or former address, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 31,868,244,872 Preferred 6,000,000,000 11. Indicate the item numbers reported herein Item 9(b) The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. Megaworld Corporation MEG PSE Disclosure Form 4-31 - Press Release References: SRC Rule 17 (SEC Form 17-C) Section 4.4 of the Revised Disclosure Rules Subject of the Disclosure Press Release: "MEGAWORLD SETS UP 10 VACCINATION CENTERS IN NCR, LAGUNA" Background/Description of the Disclosure Please see attached Press Release. -

Who You Are Is a Statement. Where You Live Is the Exclamation Point

ACTUAL PHOTO ARCHITECT’S ILLUSTRATION Who you are is a statement. Where you live is the exclamation point. Arcovia Palazzo is a residential address at the heart of Megaworld’s 12.3-hectare ArcoVia City township in Pasig City. It’s an exceptional home—one that makes your everyday life a noteworthy accomplishment. N N TO CALOOCAN Ateneo de Manila LRT University Araneta Center- BLVD. Cubao Station AURORA quezon C-5 Cubao MRT city Araneta Center- Cubao Station TO ANTIPOLO Libis san juan COL. BONNY SERRANO AVE. MRT Santolan- Annapolis The Medical City Station Hospital La Salle Greenhills E D S A ORTIGAS AVENUE LANUZA AVE. LANUZA NUE Valle Valle Verde 5 Verde 4 AVE RIVER JR. NUE SM Center DOÑA JULIA VARGAS AVENUE EAGLE AVE Pasig Valle St. Paul AVENUE LANUZA College Verde 2 MARIKINA CARLOS J. Reedley Shangri-La Toyota CAPARAS International Pasig SHAW BLVD.Plaza AVE. School Valle LEGASPI ST. Verde 3 F. EULOGIO RODRIGUEZ C. SANTOS ST. DR. SIXTO ANTONIO MANDALUYONG Valle AQUA Verde DUCT 1 E D S A pasig city Kapitolyo PASIG MRT Guadalupe RIVER Station KALAYAAN AVE. ArcoVia City, like all Megaworld townships, showcases Uptown Mall a signature live-work-play lifestyle that’s known across C-5 McKinley Hill the country.It’s strategically located along the rizal E. Rodriguez Avenue portion of C-5 Road in Pasig City. TO PASAY taguig city McKinley West Venice Grand Canal Mall ARCHITECT’S ILLUSTRATIONS ACTUAL PHOTO The three towers of ArcoVia Palazzo face the Arco de Emperador, a 62-foot-high arch monument that serves as the centerpiece of ArcoVia City.