Capital Markets Day 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Times Are Good for KONE, Neste Oil and Wärtsilä

Nov 01, 2013 10:39 UTC Times Are Good for KONE, Neste Oil and Wärtsilä M-Index, M-Brain’s quarterly look into the media coverage of 15 large Finnish stock-listed companies revealed that in July-September, KONE, Neste Oil and Wärtsilä were the companies most often at the receiving end of positive publicity. Nokia reached a larger audience than the combined audience of all the other companies surveyed. Positive media coverage – three companies stand out Slightly more than half of KONE’s publicity in the surveyed web publications of Helsingin Sanomat, Kauppalehti and Taloussanomat was positive by tone, an excellent result and a further improvement to the company’s early-year performance. Examples of favourable coverage included positive profit warning and improved stock exchange performance that followed, Forbes placing KONE as an even more innovative company than Google, and reports of large orders that the company won in China. For Neste Oil, almost four tenths of publicity was positive. The company continued its good performance, improving from the last quarter’s one fourth share of positive attention. Most of the favourable coverage was connected with financials. Media reported of Neste Oil’s profit warning and the role of renewables in the improved Q2 result. Wärtsilä was the third company to stand out in terms of the share of favourable publicity. Comparisons to earlier M-Index analyses show that the company has considerably improved its performance in the surveyed media, compared to the last year. More than a third of Wärtsilä’s publicity in Q3 was positive by tone. -

Corporate Governance Statement

KESKO ANNUAL REPORT CORPORATE GOVERNANCE STATEMENT Introduction 3 Other information to be provided in the CG statement 18 CORPORATE Descriptions concerning Corporate Governance 4 Internal audit 18 GOVERNANCE Kesko Group’s corporate governance system 4 Related party transactions 18 Board of Directors 5 Main procedures relating to insider administration 19 STATEMENT Managing Director (President and CEO) and his duties 12 Auditing 19 Group Management Board 12 Descriptions of internal control procedures and the main features of risk management systems 13 The Group’s financial reporting 13 Internal control 15 Risk management 16 KESKO'S YEAR 2019 2 Introduction This Corporate Governance Statement has been CORPORATE GOVERNANCE CODES KESKO COMPLIES WITH AND DEPARTURES FROM THEM reviewed at the meeting of the Audit Committee of Kesko Corporate Governance Code The Corporate Governance Code effective as of 1 January 2020 Corporation’s Board of Directors on 3 February 2020. the Company complies with (“Corporate Governance Code”) This is the Corporate Governance Statement in accordance Website where the Corporate cgfinland.fi/en/corporate-governance-code/ Governance Code is publicly available with the Finnish Corporate Governance Code issued by the Securities Market Association and effective as of 1 January Corporate Governance Code Recommendation 6 (Term of Office of the Board of Directors) 2020. Kesko Corporation issues the statement separately recommendations from which the Recommendation 10 (Independence of Directors) company departs from the Report by the Board of Directors. This statement and the other information to be disclosed in accordance Explanation of and grounds for The term of office of Kesko's Board of Directors departs from the one-year term pursuant to with the Corporate Governance Code, and the Company’s the departure Recommendation 6 (Term of Office of the Board of Directors) of the Corporate Governance • grounds for the departure Code. -

Annual Report 2001 Information for Shareholders

Annual Report 2001 Information for Shareholders ANNUAL GENERAL MEETING Letters authorizing a proxy to exer- INTERIM REPORTS 2002 The Annual General Meeting of cise a shareholder’s voting right at Wärtsilä Corporation will publish Wärtsilä Corporation will take place the AGM should be sent to the Interim Reports on its financial in the Congress Wing of the Helsinki Company before the notification performance during 2002 as follows: Fair Centre on Tuesday 12 March period expires. 2002, beginning at 4 p.m. January-March: 3 May 2002 Shareholders who have registered PAYMENT OF DIVIDEND January-June: 1 August 2002 themselves no later than 1 March The Board of Directors will propose January-September: 30 October 2002 in the Company’s shareholder to the Annual General Meeting that 2002. register maintained by the Finnish a normal dividend of EUR 0.50 and Central Securities Depository Ltd an extra dividend of EUR 3.50 or These Interim Reports are published may attend the AGM. altogether EUR 4.00 per share to be in English, Finnish and Swedish Shareholders whose shares have paid on the 2001 financial period. on Wärtsilä’s Internet site. Interim not been transferred to the book- The record date for dividend Reports will be sent by post on entry securities system may also payment is 15 March 2002, and the request. Interim Report orders: attend the AGM on condition that dividend payment date is 22 March tel. +358 10 709 0000 or such shareholders were registered in 2002, should the Board’s proposal be Internet: www.wartsila.com the Company’s shareholder register approved. -

UPM the Biofore Company

UPM The Biofore Company Investor Presentation December 2018 Competitive businesses with strong market positions UPM UPM UPM UPM UPM UPM BIOCHEMICALS BIOREFINING ENERGY RAFLATAC SPECIALTY COMMUNICA- PLYWOOD BIOCOMPOSITES PAPERS TION PAPERS Pulp Electricity Label Label papers, Magazine Plywood WOOD SOURCING Biofuels generation materials for release liners, papers, and veneer AND FORESTRY Timber and trading product and office papers newsprint and products information and flexible fine papers labelling packaging 2 | © UPM – The Biofore Company Global businesses – local presence UPM’s sales by market 2017 EUR 10,010 million 12,000 customers in 120 countries 54 62% production plants 13% Europe 20% in 12 countries 90,000 North America Asia shareholders in 35 countries 19,100 25,000 employees b-to-b suppliers 5% in 46 countries in 75 countries Rest of the world 3 | © UPM – The Biofore Company Operating on healthily growing markets UPM PLYWOOD Comparable EBIT by Plywood, veneer ~3% business area 2017 EUR 1,292m UPM COMMUNICATION PAPERS Graphic papers ~ –4% UPM BIOREFINING Pulp ~3% Biofuels strong UPM SPECIALTY PAPERS Timber ~2% Label papers ~4% High-end office papers ~4% UPM RAFLATAC Self-adhesive labels ~4% UPM ENERGY Demand trend growth, % pa 4 | © UPM – The Biofore Company Electricity ~1% Sustainable and safe products ELECTRICITY for everyday use everywhere PULP-BASED MATERIALS for packaging, transport, LABEL MATERIALS storage and hygiene products for food packaging, drinks bottles and for communicating PUBLICATION information PAPERS for reading -

Economic Commission for Europe

1 ECONOMIC COMMISSION FOR EUROPE Timber Committee October 2020 FINLAND MARKET STATEMENT 1 GENERAL ECONOMIC TRENDS In 2019, the Finnish economy grew by 1.1 percent year-over-year. At the end of the year, however, Finland's economic growth turned negative. In the first quarter of this year, the economy contracted further by 1.9 percent and in the second quarter by 4.5 percent from previous quarters. Compared to quarters a year ago, the corresponding percentages were -1.3 and -6.4, respectively. Technically, this means that Finland has been in recession throughout the first half of 2020. The corona-related restrictions on assembly and movement imposed in the spring affected particularly the service and transport sectors in Finland. Although the rapid rise in unemployment could be avoided through part-time work, lay-offs and other arrangements, the general increase in uncertainty and restrictive measures quickly dampened private consumption. The first wave of the pandemic in Finland was curbed fairly quickly, and the lifting of restrictions at the beginning of June quickly revived consumption and economic activity. However, significant growth in private consumption will be limited by rising unemployment towards the end of this year. In Finland, construction contracted even before corona, but the pandemic even had a stimulating effect on housing renovation, as the renovation of detached houses and summer cottages increased during the spring and summer due to remote work and mobility restrictions. Investments in machinery and equipment, on the other hand, will shrink this year as a result of uncertainty and weakening new orders. With the stimulus packages, public consumption will increase. -

Sustainable Valueco2 Creation by Pulp & Paper Companies

Sustainable ValueCO2 Creation by Pulp & Paper Companies www.SustainableValue.com Authors Ralf Barkemeyer, Frank Figge, Tobias Hahn, Andrea Liesen and Frank Müller This present survey was funded by the Swedish MISTRA foundation under the umbrella of the research projeĐƚ ͞^ƵƐƚĂŝŶĂďůĞ /ŶǀĞƐƚŵĞŶƚ ZĞƐĞĂƌĐŚ WůĂƚĨŽƌŵ͟ ;^/ZWͿ͕ ƐƵďƉƌŽũĞĐƚ ͞sĂůƵĞ-based ĞŶǀŝƌŽŶŵĞŶƚĂůƐƵƐƚĂŝŶĂďŝůŝƚLJĂŶĂůLJƐŝƐŽĨEŽƌĚŝĐĐŽŵƉĂŶŝĞƐ͟. The study was authored by resear- chers of the following institutions: University of Leeds Euromed Management IZT ʹ Institute for Futures Marseille Studies and Technology Sustainability Research Assessment Institute, School of Earth & Domaine de Luminy - Environment BP 921 Schopenhauerstr. 26 13 288 Marseille cedex 9 14129 Berlin Leeds, LS2 9JT France Germany United Kingdom Contact: [email protected] We suggest to cite this report as follows: Barkemeyer, R.; Figge, F.; Hahn, T.; Liesen, A.; & Müller, F. (2011). Sustainable ValueCO2 Creation by Pulp & Paper Companies. Sustainable Value Research: Leeds, Marseille and Berlin. © Leeds, Marseille and Berlin 2011. All rights reserved. Dissemination of this document is free as long as full reference to the authors is made. Title art work: aboutpixel.de / Lesestoff © Rainer Sturm Sustainable ValueCO2 Creation by Pulp & Paper Companies Table of Contents Table of Contents Table of Contents.............................................................................................................. 1 List of Figures and Tables ................................................................................................. -

Warranttien Pörssitiedote 31.8.2006

Nordea Bank ABP laskee liikkeeseen 143 uutta warranttisarjaa 5.12.2018 (sarjat 2018: C10 FI ja 2018: P10 FI) Nordea Bank ABP laskee warranttiohjelmansa puitteissa liikkeeseen 143 uutta warranttisarjaa 5.12.2018. Warranttien kohde-etuutena on Nokian Renkaat Oyj, Sampo Oyj, Stora Enso Oyj, UPM-Kymmene Oyj, Kone Oyj, Metso Oyj, Nokia Oyj, Neste Oyj, Fortum Oyj ja Wärtsilä Oyj. Warrantit ovat osto- tai myyntiwarrantteja. Warranttien lunastustapa on käteissuoritus. Warrantin erääntyessä haltijalle tilitetään mahdollinen positiivinen nettoarvo käteisenä. Warranttikohtaiset ehdot Kaikki warrantit lasketaan liikkeeseen osana Nordea Bank AB (publ):n warranttiohjelmaa, joka muodostuu 14.6.2018 julkaistusta ohjelmaesitteestä ja mahdollisista täydentävistä ohjelmaesitteistä. Warranttiohjelmaa koskevat ohjelmaesitteet ja kaikkiin liikkeeseenlaskettaviin warrantteihin sovellettavat lopulliset ehdot ovat saatavilla liikkeeseenlaskijan kotisivuilta: http://www.nordea.fi/warrantit/. Tässä esitettävät tiedot ovat ainoastaan tiivistelmä lopullisissa ehdoissa ja ohjelmaesitteessä esitetyistä tiedoista. Liikkeeseenlaskija Nordea Bank ABP Sijoitusinstrumentti Warrantti (osto ja myynti) Warranttien kohde- Nokian Renkaat Oyj, Sampo Oyj, Stora Enso Oyj, UPM-Kymmene etuus Oyj, Kone Oyj, Metso Oyj, Nokia Oyj, Neste Oyj, Fortum Oyj ja Wärtsilä Oyj. Käteissuorituksen Ostowarrantti: määrä (Loppukurssi – Lunastushinta) x Kerroin Jos Loppukurssi on alhaisempi tai sama kuin Lunastushinta, käteissuoritusta ei makseta. Myyntiwarrantti: (Lunastushinta – Loppukurssi) x Kerroin -

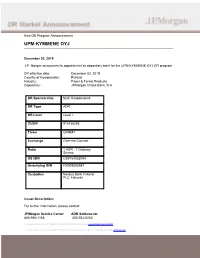

Upm-Kymmene Oyj ______

New DR Program Announcement UPM-KYMMENE OYJ __________________________________________________________________________________ December 03, 2019 J.P. Morgan announces its appointment as depositary bank for the UPM-KYMMENE OYJ DR program. DR effective date:December 03, 2019 Country of incorporation:Finland Industry:Paper & Forest Products Depositary:JPMorgan Chase Bank, N.A DR Sponsorship Multi Unsponsored DR Type ADR DR Level Level I CUSIP 915436208 Ticker UPMMY Exchange Over-the-Counter Ratio 1 ADR : 1 Ordinary Shares US ISIN US9154362084 Underlying ISIN FI0009005987 Custodian Nordea Bank Finland PLC, Helsinki Issuer Description: For further information, please contact: JPMorgan Service Center ADR Settlements 800-990-1135 302-552-0230 For more information on J.P. Morgan’s Depositary Receipt services, go to www.jpmorgan.com/visit/adr. For market information on Depositary Receipts and international equities, go to J.P. Morgan’s Web site www.adr.com. Disclosures J.P. Morgan collects fees from holders of depositary receipts. JPMorgan may (i) reimburse the issuer for certain expenses incurred by the issuer in connection with the depositary receipts program or (ii) share with the issuer revenue derived by JPMorgan from the program. JPMorgan may use brokers, dealers or other service providers that are affiliates or other divisions of JPMorgan and may earn or share fees and commissions. From time to time, J.P. Morgan may pay a rebate to brokers in connection with the deposit of shares for the issuance of unsponsored depositary receipts. J.P. Morgan disclaims all liability arising out of, or relating to, such rebates. In particular, J.P. Morgan disclaims all responsibility regarding whether such broker passes all or a portion of such rebate to beneficial holders of such depositary receipts. -

Upm Biorefinery

Fuels of the future - from wood-based raw materials IEA Bioenergy Conference 13-15.11.2012 UPM Biofuels Sari Mannonen, [email protected] UPM today – The Biofore Company UPM leads the integration of bio and forest industries into a new, sustainable and innovation-driven future • 24,000 employees • Sales exceed 10 billion euros in 2011 - Production in 16 countries, world-wide sales network - Listed in the NASDAQ OMX Helsinki stock exchange Energy and pulp Paper Engineered materials 4,200 employees 14,000 employees 5,200 employees Business areas Paper grades Business areas • Energy • Magazine papers • Label • Pulp including • Fine papers • Plywood Plantation operations • Newsprint • UPM ProFi composite • Biofuels • Selected speciality • Timber papers • Forestry and Wood sourcing 2 | © UPM Megatrends and regulations as the basis for the biofuels market Megatrends... ...drive public policy... ... and Biofuels market Energy security EU-27 biodiesel demand • Political, Current regulation favourable geographical • Blending mandates and targets (Mtons) and price risks (EU: Renewable energy and 50 fuel quality directives. US: Climate change Renewable fuel standard) 40 +7% • Financial subsidies, mainly tax advantages 30 • EU as 22 forerunner Major short-term regulation 20 changes unlikely 11 Rural development • Biofuels needed to fight the 10 15 megatrends • Employment • Stable regulatory environment 0 in rural areas required to drive investments 2010 2015 2020 • Land use UPM's plan 0.13 0.7 Long-term, biofuels are likely to (Mtons) Energy prices -

UPM Korkeakoski Sawmill Can Be Sold Either As PEFC™ Or FSC® Certified

UPM Timber in brief UPM Timber is a significant Nordic sawn timber producer. INSTRUCTIONS for visitors Our four sawmills in Finland have annual capacity of 1.5 M cubic meters of redwood and whitewood sawn timber. UPM Timber employs around 410 people and is headquarter in At the site, stay with your host Tampere. WELCOME TO UPM Korkeakoski In our standard and special sawn timber products we use Use protective equipment provided to you certified raw material and latest sawmilling techniques to sawmill produce high quality sawn timber that fulfills customer In an emergency situations follow orders requirements. Our main customer industries are joinery, given by your host packaging, distribution and construction. www.upmtimber.com Permission is needed for photographing Smoking is not allowed Certificates Camera surveillance on the site EN 14081 PEFC/02-34-05 Promoting Sustainable Forest Management www.pefc.org All sawn timber produced by UPM Korkeakoski sawmill can be sold either as PEFC™ or FSC® certified. Korkeakoski mill area UPM Korkeakoski sawmill UPM Koskeakoski sawmill is located in Central Finland Sahantie 10, PO Box 25 wood purchasing area together with UPM Jokilaakso FIN-35501 Korkeakoski, Finland papermills and Jyväskylä plywood mill. The mill site covers in Tel. +358 20 414 149 E-mail: [email protected] total about 33 hectares. Korkeakoski sawmill is in the middle of high quality pine forests in Juupajoki. www.upmtimber.com 07/2016 UPM – The Biofore Company UPM Korkeakoski sawmill Through the renewing of the bio and forest industries, Korkeakoski sawmill produces redwood sawn timber from UPM is building a sustainable future across six business certified Nordic pine. -

Corporate Governance Statement 2019

CORPORATE GOVERNANCE STATEMENT 2019 UPM-KYMMENE CORPORATION CORPORATE GOVERNANCE STATEMENT 2019 UPM-Kymmene Corporation (UPM or the company) follows the Finnish Corporate Governance Code (CG Code) issued by the Securities Market Association which entered into force on 1 January 2020. The CG Code is publicly available on the Securities Market Association’s website at www.cgfinland.fi. UPM complies with all recommendations of the CG Code. UPM’s Corporate Governance Statement (CG UPM uses a one-tier governance model, which, Statement) for the financial year 2019 has been in addition to the general meeting of shareholders, prepared in accordance with the CG Code’s corporate comprises the Board of Directors and the President governance reporting section. UPM presents the and CEO as presented in the illustration below. In the CG Statement as a separate report, distinct from the operative management of the company, the President Report of the Board of Directors. The CG Statement and CEO is assisted by the Group Executive Team, is available on the corporate website’s Investors the Business Area Boards and the Strategy Team. section under Governance (upm.com/governance). The Group Executive Team assists the President The Report of the Board of Directors is presented and CEO in respect of approving and executing group- on pages 120–143 of UPM’s Annual Report 2019, level guidelines and procedures. which is also available on the corporate website. The Business Area Boards assist the President and CEO as regards business-area level decision making UPM’s governance structure in matters pertaining to each business area’s strategy, budget, business performance, operative investments, UPM is a Finnish limited liability company with commercial strategies, business development plans, headquarters in Helsinki, Finland. -

The Finnish Sauna

CHAPTER 10 The Finnish Sauna If sauna, tar, or alcohol doesn’t help, you are sick to die. —Finnish adage Finns are reverential about the sauna.In the glow of the softly lit wood-lined space, they chat jovially or fall into a comfortable silence. The heat makes one welcome a dip in ice-cold water or a roll in the snow, as improbable as that sounds. Food and drink afterward never tasted so delicious. There is etiquette which has to do with practical and safety questions, but generous Finns will walk you through it. As is their method of rearing children, it’s a window to the Finnish psyche. —Anonymous Finn (quoted in Kaiser & Perkins, 2005) inland is located between Sweden and Russia on the Baltic Sea and has a pop- ulation of 5.3 million. There are 15.4 people per square kilometer in compari- Fson to 31.7 in the United States. With 2 million saunas in Finland, the sauna density is clearly greater than that of any other country in the world, even if most of the saunas are in the countryside where 70% of the land surrounding 60,000 lakes is forested.Finland also extends beyond mainland Finland into the Archipelago Sea with its 80,000 islands, which include the self-governing, Swedish-speaking Åland Islands province. Throughout Finland both Finnish and Swedish are official languages. However, most mainland Finnish-speaking Finns, who have taken obligatory Swedish courses in school, have only limited competence in that language. The sauna began in the forests as a hole in the ground with hot stones and evolved into a small log cabin.The sauna metaphor is functionally and symbolically related to local and nature-focused values and customs.