Client Satisfaction with Health Insurance in Uganda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nakaseke Constituency: 109 Nakaseke South County

Printed on: Monday, January 18, 2021 16:36:23 PM PRESIDENTIAL ELECTIONS, (Presidential Elections Act, 2005, Section 48) RESULTS TALLY SHEET DISTRICT: 069 NAKASEKE CONSTITUENCY: 109 NAKASEKE SOUTH COUNTY Parish Station Reg. AMURIAT KABULETA KALEMBE KATUMBA KYAGULA MAO MAYAMBA MUGISHA MWESIGYE TUMUKUN YOWERI Valid Invalid Total Voters OBOI KIIZA NANCY JOHN NYI NORBERT LA WILLY MUNTU FRED DE HENRY MUSEVENI Votes Votes Votes PATRICK JOSEPH LINDA SSENTAMU GREGG KAKURUG TIBUHABU ROBERT U RWA KAGUTA Sub-county: 001 KAASANGOMBE 014 BUKUUKU 01 TIMUNA/KAFENE 716 1 0 1 0 278 2 0 1 0 1 140 424 43 467 0.24% 0.00% 0.24% 0.00% 65.57% 0.47% 0.00% 0.24% 0.00% 0.24% 33.02% 9.21% 65.22% 02 LUKYAMU PR. SCHOOL 778 2 2 0 1 348 2 2 0 1 0 110 468 24 492 0.43% 0.43% 0.00% 0.21% 74.36% 0.43% 0.43% 0.00% 0.21% 0.00% 23.50% 4.88% 63.24% 03 BUKUUKU PRI. SCHOOL 529 0 0 1 1 188 0 1 0 0 0 74 265 3 268 0.00% 0.00% 0.38% 0.38% 70.94% 0.00% 0.38% 0.00% 0.00% 0.00% 27.92% 1.12% 50.66% Parish Total 2023 3 2 2 2 814 4 3 1 1 1 324 1157 70 1227 0.26% 0.17% 0.17% 0.17% 70.35% 0.35% 0.26% 0.09% 0.09% 0.09% 28.00% 5.70% 60.65% 015 BULYAKE 01 NJAGALABWAMI COMM. -

Nakaseke Makes Model Town Plan

40 The New Vision, FrIday, June 4, 2010 NAKASEKE DISTRICT REVIEW SUPPLEMENT Farmers benefit from Caritas support JOHN KASOZI By John Kasozi education, in August 1993 increased, I got married truck. Next year, he plans he moved to Kampala to the following year.” to buy a plot in Kampala ILSON Nsobya find employment. He initial- Nsobya now has 15 and build a commercial could not ly wanted to work as a acres of land under structure in future. believe, when vehicle mechanic, but he pineapples. He pays school fees Wa lady she met ended up as a cleaner. He notes that on for his four children and six in the bank paid sh24,000 “I decided to go back average an acre of others. as school fees for her home after working for one pineapple brings in about Joyce Kizito, the kindergarten child. That and half years,” says sh5m per year. But with Kamukamu community was in 1993 when his Nsobya. intensive farming, a farmer resource person from monthly pay was One morning in 1994, can garner about sh10m, Kawula, Luweero who sh20,000. Nsobya decided to pack his he says. is also a CARITAS “From that day, I became four-inch mattress, The cost of one pineapple beneficiary says before restless. I wondered how Panasonic radio, a basin ranges between sh600 to they started getting I would pay fees for my and utensils. He used his sh1, 000, Nsobya says support from from the children, rent, feed the savings of sh3,000 for adding that his clientele is organisation in 2002, their family, settle medical transport. -

Typhoid Over Diagnosis in Nakaseke District, June 2016

Public Health Fellowship Program – Field Epidemiology Track Typhoid Over diagnosis in Nakaseke District, June 2016 Dr. Kusiima Joy, MBChB-MHSR Fellow,2016 Typhoid Alert May June 2016 2016 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Notification Data Audit ,12 health Reviewed HMIS data facilities Nakaseke 84 cases/ 50,000 by FFETP(wk 15-21) Typhoid Outbreak verification exercise 323 Typhoid cases reported 2 Typhoid verification in Nakaseke District Objectives . Verify the existence of an outbreak . Verify reported diagnosis using standard case definition . Recommend public health action 3 Typhoid verification in Nakaseke District District location 4 Typhoid verification in Nakaseke District Facilities selected . Private hospital - Kiwoko . Government hospital - Nakaseke . Health center IV - Semuto . Health center III - Kapeeka 5 Typhoid verification in Nakaseke District Data collection . Extracted records from registers (1st/12/ 2015 to 14th/06/2016) . Discussed with clinicians & lab personnel . Took clinical history &examined typhoid suspects 6 Typhoid verification in Nakaseke District Standard case definition . Suspected case: Onset of fever ≥3days,negative malaria test, resident of Nakaseke district Plus any of following: chills, malaise, headache, sore throat, cough, abdominal pain, constipation, diarrhea . Probable case: Suspected case plus positive antigen test (Widal) . Confirmed case: Suspected case plus salmonella typhi (+) blood or stool by culture 7 Typhoid verification in Nakaseke District Data quality assessment . Reviewed laboratory -

Population by Parish

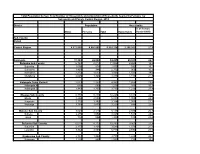

Total Population by Sex, Total Number of Households and proportion of Households headed by Females by Subcounty and Parish, Central Region, 2014 District Population Households % of Female Males Females Total Households Headed HHS Sub-County Parish Central Region 4,672,658 4,856,580 9,529,238 2,298,942 27.5 Kalangala 31,349 22,944 54,293 20,041 22.7 Bujumba Sub County 6,743 4,813 11,556 4,453 19.3 Bujumba 1,096 874 1,970 592 19.1 Bunyama 1,428 944 2,372 962 16.2 Bwendero 2,214 1,627 3,841 1,586 19.0 Mulabana 2,005 1,368 3,373 1,313 21.9 Kalangala Town Council 2,623 2,357 4,980 1,604 29.4 Kalangala A 680 590 1,270 385 35.8 Kalangala B 1,943 1,767 3,710 1,219 27.4 Mugoye Sub County 6,777 5,447 12,224 3,811 23.9 Bbeta 3,246 2,585 5,831 1,909 24.9 Kagulube 1,772 1,392 3,164 1,003 23.3 Kayunga 1,759 1,470 3,229 899 22.6 Bubeke Sub County 3,023 2,110 5,133 2,036 26.7 Bubeke 2,275 1,554 3,829 1,518 28.0 Jaana 748 556 1,304 518 23.0 Bufumira Sub County 6,019 4,273 10,292 3,967 22.8 Bufumira 2,177 1,404 3,581 1,373 21.4 Lulamba 3,842 2,869 6,711 2,594 23.5 Kyamuswa Sub County 2,733 1,998 4,731 1,820 20.3 Buwanga 1,226 865 2,091 770 19.5 Buzingo 1,507 1,133 2,640 1,050 20.9 Maziga Sub County 3,431 1,946 5,377 2,350 20.8 Buggala 2,190 1,228 3,418 1,484 21.4 Butulume 1,241 718 1,959 866 19.9 Kampala District 712,762 794,318 1,507,080 414,406 30.3 Central Division 37,435 37,733 75,168 23,142 32.7 Bukesa 4,326 4,711 9,037 2,809 37.0 Civic Centre 224 151 375 161 14.9 Industrial Area 383 262 645 259 13.9 Kagugube 2,983 3,246 6,229 2,608 42.7 Kamwokya -

Planned Shutdown Web October 2020.Indd

PLANNED SHUTDOWN FOR SEPTEMBER 2020 SYSTEM IMPROVEMENT AND ROUTINE MAINTENANCE REGION DAY DATE SUBSTATION FEEDER/PLANT PLANNED WORK DISTRICT AREAS & CUSTOMERS TO BE AFFECTED Kampala West Saturday 3rd October 2020 Mutundwe Kampala South 1 33kV Replacement of rotten vertical section at SAFARI gardens Najja Najja Non and completion of flying angle at MUKUTANO mutundwe. North Eastern Saturday 3rd October 2020 Tororo Main Mbale 1 33kV Create Two Tee-offs at Namicero Village MBALE Bubulo T/C, Bududa Tc Bulukyeke, Naisu, Bukigayi, Kufu, Bugobero, Bupoto Namisindwa, Magale, Namutembi Kampala West Sunday 4th October 2020 Kampala North 132/33kV 32/40MVA TX2 Routine Maintenance of 132/33kV 32/40MVA TX 2 Wandegeya Hilton Hotel, Nsooda Atc Mast, Kawempe Hariss International, Kawempe Town, Spencon,Kyadondo, Tula Rd, Ngondwe Feeds, Jinja Kawempe, Maganjo, Kagoma, Kidokolo, Kawempe Mbogo, Kalerwe, Elisa Zone, Kanyanya, Bahai, Kitala Taso, Kilokole, Namere, Lusanjja, Kitezi, Katalemwa Estates, Komamboga, Mambule Rd, Bwaise Tc, Kazo, Nabweru Rd, Lugoba Kazinga, Mawanda Rd, East Nsooba, Kyebando, Tilupati Industrial Park, Mulago Hill, Turfnel Drive, Tagole Cresent, Kamwokya, Kubiri Gayaza Rd, Katanga, Wandegeya Byashara Street, Wandegaya Tc, Bombo Rd, Makerere University, Veterans Mkt, Mulago Hospital, Makerere Kavule, Makerere Kikumikikumi, Makerere Kikoni, Mulago, Nalweuba Zone Kampala East Sunday 4th October 2020 Jinja Industrial Walukuba 11kV Feeder Jinja Industrial 11kV feeders upgrade JINJA Walukuba Village Area, Masese, National Water Kampala East -

Croc's July 1.Indd

CLASSIFIED ADVERTS NEW VISION, Monday, July 1, 2013 57 BUSINESS INFORMATION MAYUGE SUGAR INDUSTRIES LTD. SERVICE Material Testing EMERGENCY VACANCIES POLICE AND FIRE BRIGADE: Ring: 999 or 342222/3. One of the fastest developing and THE ONLY 6. BOILER ATTENDANT - 3 Posts Africa Air Rescue (AAR) 258527, MANUFACTURER OF SULPHURLESS SUGAR IN Boiler Attendant Certificate Holders with 3-5 258564, 258409. EAST AFRICA based in Uganda. The organization yrs working experience preferred (Thermo ELECTRICAL FAILURE: Ring is engaged in the manufacturing of “Nile Sugar” fluid handling) UMEME on185. and soon starting the manufacturing of Extra 7. SR. ELECTRICAL & INSTRUMENTATION ENGR. MATERIAL TESTING AND SURVEY EQUIPMENT Water: Ring National Water and Neutral Alcohol Invites applications for below - 1Post Sewerage Corporation on 256761/3, 242171, 232658. Telephone inquiry: posts; B.E.(electrical & instrumentation) or equallent Material Testing UTL-900, Celtel 112, MTN-999, 112 1. SHIFT CHEMIST FOR DISTILLATION - 3 Posts with experience of 15 years FUNERAL SERVICES Must have 3-5 years of experience in PLC/ 8. ELECTRICAL ENGR - 1 Post Aggregates impact Value Kampala Funeral Directors, SKADA system independent operation . Diploma in Electrical Engr.or equallent with Apparatus Bukoto-Ntinda Road. P.O. Box 9670, Qualification :-B.SC.Alco,Tech or Diploma in exp of 5 yrs Flakiness Gauge&Flakiness Chem Eng. 9. INSTRUMENTATION ENGR. - 1 Post Kampala. Tel: 0717 533533, 0312 Sleves 533533. 2. LABORATORY CHEMIST SHIFT - 3 Posts Diploma in Instrumentation or equallent with Los Angeles Abrasion Machine Uganda Funeral Services For Mol Analysis /Spirit Analysis /Q.C exp of 5 yrs H/Q 80A Old Kira Road, Bukoto Checking/Spent wash loss checking etc 10. -

Legend " Wanseko " 159 !

CONSTITUENT MAP FOR UGANDA_ELECTORAL AREAS 2016 CONSTITUENT MAP FOR UGANDA GAZETTED ELECTORAL AREAS FOR 2016 GENERAL ELECTIONS CODE CONSTITUENCY CODE CONSTITUENCY CODE CONSTITUENCY CODE CONSTITUENCY 266 LAMWO CTY 51 TOROMA CTY 101 BULAMOGI CTY 154 ERUTR CTY NORTH 165 KOBOKO MC 52 KABERAMAIDO CTY 102 KIGULU CTY SOUTH 155 DOKOLO SOUTH CTY Pirre 1 BUSIRO CTY EST 53 SERERE CTY 103 KIGULU CTY NORTH 156 DOKOLO NORTH CTY !. Agoro 2 BUSIRO CTY NORTH 54 KASILO CTY 104 IGANGA MC 157 MOROTO CTY !. 58 3 BUSIRO CTY SOUTH 55 KACHUMBALU CTY 105 BUGWERI CTY 158 AJURI CTY SOUTH SUDAN Morungole 4 KYADDONDO CTY EST 56 BUKEDEA CTY 106 BUNYA CTY EST 159 KOLE SOUTH CTY Metuli Lotuturu !. !. Kimion 5 KYADDONDO CTY NORTH 57 DODOTH WEST CTY 107 BUNYA CTY SOUTH 160 KOLE NORTH CTY !. "57 !. 6 KIIRA MC 58 DODOTH EST CTY 108 BUNYA CTY WEST 161 OYAM CTY SOUTH Apok !. 7 EBB MC 59 TEPETH CTY 109 BUNGOKHO CTY SOUTH 162 OYAM CTY NORTH 8 MUKONO CTY SOUTH 60 MOROTO MC 110 BUNGOKHO CTY NORTH 163 KOBOKO MC 173 " 9 MUKONO CTY NORTH 61 MATHENUKO CTY 111 MBALE MC 164 VURA CTY 180 Madi Opei Loitanit Midigo Kaabong 10 NAKIFUMA CTY 62 PIAN CTY 112 KABALE MC 165 UPPER MADI CTY NIMULE Lokung Paloga !. !. µ !. "!. 11 BUIKWE CTY WEST 63 CHEKWIL CTY 113 MITYANA CTY SOUTH 166 TEREGO EST CTY Dufile "!. !. LAMWO !. KAABONG 177 YUMBE Nimule " Akilok 12 BUIKWE CTY SOUTH 64 BAMBA CTY 114 MITYANA CTY NORTH 168 ARUA MC Rumogi MOYO !. !. Oraba Ludara !. " Karenga 13 BUIKWE CTY NORTH 65 BUGHENDERA CTY 115 BUSUJJU 169 LOWER MADI CTY !. -

NAKASEKE DLG Q4 REPORT.Pdf

Local Government Quarterly Performance Report Vote: 569 Nakaseke District 2016/17 Quarter 4 Structure of Quarterly Performance Report Summary Quarterly Department Workplan Performance Cumulative Department Workplan Performance Location of Transfers to Lower Local Services and Capital Investments Submission checklist I hereby submit _________________________________________________________________________. This is in accordance with Paragraph 8 of the letter appointing me as an Accounting Officer for Vote:569 Nakaseke District for FY 2016/17. I confirm that the information provided in this report represents the actual performance achieved by the Local Government for the period under review. Name and Signature: Chief Administrative Officer, Nakaseke District Date: 8/23/2017 cc. The LCV Chairperson (District)/ The Mayor (Municipality) Page 1 Local Government Quarterly Performance Report Vote: 569 Nakaseke District 2016/17 Quarter 4 Summary: Overview of Revenues and Expenditures Overall Revenue Performance Cumulative Receipts Performance Approved Budget Cumulative % UShs 000's Receipts Budget Received 1. Locally Raised Revenues 1,338,786 1,704,820 127% 2a. Discretionary Government Transfers 3,314,474 3,260,284 98% 2b. Conditional Government Transfers 16,270,489 15,459,486 95% 2c. Other Government Transfers 948,643 966,847 102% 4. Donor Funding 22,900 Total Revenues 21,872,393 21,414,338 98% Overall Expenditure Performance Cumulative Releases and Expenditure Perfromance Approved Budget Cumulative Cumulative % % % UShs 000's Releases Expenditure -

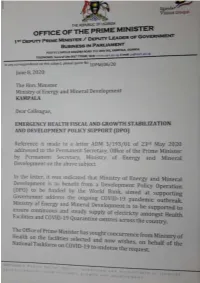

Emergency Health Fiscal and Growth Stabilization and Development

LIST OF COVID-19 QUARANTINE CENTRES IN WATER AND POWER UTILITIES OPERATION AREAS WATER S/N QUARANTINE CENTRE LOCATION POWER UTILITY UTILITY 1 MASAFU GENERAL HOSPITAL BUSIA UWS-E UMEME LTD 2 BUSWALE SECONDARY SCHOOL NAMAYINGO UWS-E UMEME LTD 3 KATAKWI ISOLATION CENTRE KATAKWI UWS-E UMEME LTD 4 BUKWO HC IV BUKWO UWS-E UMEME LTD 5 AMANANG SECONDARY SCHOOL BUKWO UWS-E UMEME LTD 6 BUKIGAI HC III BUDUDA UWS-E UMEME LTD 7 BULUCHEKE SECONDARY SCHOOL BUDUDA UWS-E UMEME LTD 8 KATIKIT P/S-AMUDAT DISTRICT KATIKIT UWS-K UEDCL 9 NAMALU P/S- NAKAPIRIPIRIT DISTRICT NAMALU UWS-K UEDCL 10 ARENGESIEP S.S-NABILATUK DISTRICT ARENGESIEP UWS-K UEDCL 11 ABIM S.S- ABIM DISTRICT ABIM UWS-K UEDCL 12 KARENGA GIRLS P/S-KARENGA DISTRICT KARENGA UWS-K UMEME LTD 13 NAKAPELIMORU P/S- KOTIDO DISTRICT NAKAPELIMORU UWS-K UEDCL KOBULIN VOCATIONAL TRAINING CENTER- 14 NAPAK UWS-K UEDCL NAPAK DISTRICT 15 NADUNGET HCIII -MOROTO DISTRICT NADUNGET UWS-K UEDCL 16 AMOLATAR SS AMOLATAR UWS-N UEDCL 17 OYAM OYAM UWS-N UMEME LTD 18 PADIBE IN LAMWO DISTRICT LAMWO UWS-N UMEME LTD 19 OPIT IN OMORO OMORO UWS-N UMEME LTD 20 PABBO SS IN AMURU AMURU UWS-N UEDCL 21 DOUGLAS VILLA HOSTELS MAKERERE NWSC UMEME LTD 22 OLIMPIA HOSTEL KIKONI NWSC UMEME LTD 23 LUTAYA GEOFREY NAJJANANKUMBI NWSC UMEME LTD 24 SEKYETE SHEM KIKONI NWSC UMEME LTD PLOT 27 BLKS A-F AKII 25 THE EMIN PASHA HOTEL NWSC UMEME LTD BUA RD 26 ARCH APARTMENTS LTD KIWATULE NWSC UMEME LTD 27 ARCH APARTMENTS LTD KIGOWA NTINDA NWSC UMEME LTD 28 MARIUM S SANTA KYEYUNE KIWATULE NWSC UMEME LTD JINJA SCHOOL OF NURSING AND CLIVE ROAD JINJA 29 MIDWIFERY A/C UNDER MIN.OF P.O.BOX 43, JINJA, NWSC UMEME LTD EDUCATION& SPORTS UGANDA BUGONGA ROAD FTI 30 MAAIF(FISHERIES TRAINING INSTITUTE) NWSC UMEME LTD SCHOOL PLOT 4 GOWERS 31 CENTRAL INN LIMITED NWSC UMEME LTD ROAD PLOT 2 GOWERS 32 CENTRAL INN LIMITED NWSC UMEME LTD ROAD PLOT 45/47 CHURCH 33 CENTRAL INN LIMITED NWSC UMEME LTD RD CENTRAL I INSTITUTE OF SURVEY & LAND PLOT B 2-5 STEVEN 34 NWSC 0 MANAGEMENT KABUYE CLOSE 35 SURVEY TRAINING SCHOOL GOWERS PARK NWSC 0 DIVISION B - 36 DR. -

Atomic Energy Council Annual Report 2012/2013

Atomic Energy Council 1 Annual Report 2012/2013 ATOMIC ENERGY COUNCIL ANNUAL REPORT FOR 2012/2013 “To regulate the peaceful applications and management of ionizing radiation for the protection and safety of society and the environment from the dangers resulting from ionizing radiation” Atomic Energy Council 2 Annual Report 2012/2013 FOREWARD The Atomic Energy Council was established by the Atomic Energy Act, 2008, Cap. 143 Laws of Uganda, to regulate the peaceful applications of ionizing radiation in the country. The Council consists of the policy organ with five Council Members headed by the Chairperson appointed by the Minister and the full time Secretariat headed by the Secretary. The Council has extended services to various areas of the Country ranging from registering facilities that use radiation sources, authorization of operators, monitoring occupational workers, carrying out inspections in facilities among others. The Council made achievements which include establishing the Secretariat, gazetting of the Atomic Energy Regulations, 2012, developing safety guides for medical and industrial practices, establishing systems of notifications, authorizations and inspections, establishing national and international collaborations with other regulatory bodies and acquisition of some equipment among others. The Council has had funding as the major constraint to the implementation of the Act and the regulations coupled with inadequate equipment and insufficient administrative and technical staff. The Council will focus on institutional development, establishing partnerships and collaborations and safety and security of radioactive sources. The Council would like to thank the government and in particular the MEMD, the International Atomic Energy Agency, United States Nuclear Regulatory Commission and other organizations and persons who have helped Council in carrying out its mandate. -

Press Release

t The Reoublic of LJoanda MINISTRY OF HEALTH Office of the Director General 'Public Relations Unit 256-41 -4231 584 D i rector Gen era l's Off ice : 256- 41 4'340873 Fax : PRESS RELEASE IMPLEMENTATION OF HEPATITIS B CONTROL ACTIVITIES IN I(AMPALA METROPOLITAN AREA Kampala - 19th February 2O2l' The Ministry of Health has embarked on phase 4 of the HePatitis B control activities in 31 districts including Kampala Metropolitan Area.- These activities are expected to run uP to October 2021 in the districts of imPlementation' The hepatitis control activities include; 1. Testing all adolescents and adults born before 2OO2 (19 years and above) 2. Testing and vaccination for those who test negative at all HCIIIs, HCIVs, General Hospitals, Regional Referral Hospitals and outreach posts. 3. Linking those who test positive for Hepatitis B for further evaluation for treatment and monitoring. This is conducted at the levels of HC IV, General Hospitals and Regional Referral Hospitals' The Ministry through National Medical Stores has availed adequate test kits and vaccines to all districts including Kampala City Courrcil' Hepatitis + Under phase 4, ttle following districts will be covered: Central I Regi6n: Kampala Metropolitan Area, Masaka, Rakai, Kyotera, Kalangala, Mpigi, Bffiambala, Gomba, Sembabule, Bukomansimbi, Lwen$o, Kalungu and Lyantonde. South Western region: Kisoro, Kanungu, Rubanda, Rukiga, Rwampara, Rukungiri, Ntungamno, Isingiro, Sheema, Mbarara, Buhweju, Mitooma, Ibanda, Kiruhura , Kazo, Kabale, Rubirizi and Bushenyi. The distribution in Kampala across the five divisions is as follows: Kawempe Division: St. Kizito Bwaise, Bwaise health clinic, Pillars clinic, Kisansa Maternity, Akugoba Maternity, Kyadondo Medical Center, Mbogo Health Clinic, Mbogo Health Clinic, Kawempe Hospital, Kiganda Maternity, Venus med center, Kisaasi COU HC, Komamboga HC, Kawempe Home care, Mariestopes, St. -

![Uganda Health Facilities Survey 2002 [FR140]](https://docslib.b-cdn.net/cover/8904/uganda-health-facilities-survey-2002-fr140-1738904.webp)

Uganda Health Facilities Survey 2002 [FR140]

Uganda Health Facilities Survey 2002 Ministry of Health Kampala, Uganda ORC Macro MEASURE DHS+ Calverton, Maryland, USA John Snow, Inc./DELIVER Arlington, Virginia, USA JSI Research & Training Institute, Inc./ Uganda AIDS/HIV Integrated Model District Programme (AIM) Kampala, Uganda June 2003 Contributors: John Snow, Inc./DELIVER JSI Research and Training Institute, Inc./AIM Dana Aronovich Evas Kansiime Allison Farnum Cochran Maurice Adams Erika Ronnow Ministry of Health ORC Macro F. G. Omaswa Gregory Pappas H. Kyabaggu Eddie Mukooyo Martin O. Oteba This report presents findings from the 2002 Uganda Health Facilities Survey (UHFS 2002) carried out by the Uganda Ministry of Health. ORC Macro (MEASURE DHS+) and John Snow, Inc. (DELIVER) provided technical assistance. Other organizations contributing to the project were the U.S. Centers for Disease Control and Prevention (CDC/Uganda), the U.S. Agency for International Development (USAID/Uganda), and the JSI Research and Training Institute, Inc., AIDS/HIV Integrated Model District Programme (AIM). MEASURE DHS+, a USAID-funded project, assists countries worldwide in the collection and use of data to monitor and evaluate population, health, and nutrition programs. Information about the Uganda Health Facilities Survey or about the MEASURE DHS+ project can be obtained by contacting: MEASURE DHS+, ORC Macro, 11785 Beltsville Drive, Suite 300, Calverton, MD 20705 (Telephone 301-572-0200; Fax 301-572-0999; E-mail [email protected]; Internet: www.measuredhs.com). DELIVER, a worldwide technical assistance support project, is funded by the Commodities Security and Logistics Division (CSL) of the Office of Population and Reproductive Health of the Bureau for Global Health (GH) of the U.S.