Overview of Corporate Financial Reporting CHAPTER 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dynamic Power Canadian Growth Fund

SUMMARY OF INVESTMENT PORTFOLIO As at March 31, 2021 The Summary of Investment Portfolio may change due to ongoing portfolio transactions. Updates are available quarterly on our website at www.dynamic.ca 60 days after quarter end, except for June 30, which is the fiscal year end, when they are available after 90 days. The total net asset value of the Fund as at March 31, 2021 was $646,062,000. Percentage of net Percentage of net By Asset Type asset value † Top 25 Holdings asset value † Equities 97.2 Intact Financial Corporation 5.6 Cash and Short Term Instruments (Bank Overdraft) 2.9 Canadian National Railway Company 5.4 Other Net Assets (Liabilities) -0.1 West Fraser Timber Co. Ltd. 5.0 Facebook, Inc., Class "A" 4.2 Microsoft Corporation 4.2 Percentage of net Canadian Pacific Railway Limited 4.1 By Country / Region (1) asset value † Alphabet Inc., Class "C" 4.0 Canada 57.2 National Bank of Canada 4.0 United States 40.0 Amazon.com, Inc. 3.7 Cash and Short Term Instruments (Bank Overdraft) 2.9 Trisura Group Ltd. 3.6 NVIDIA Corporation 3.5 Percentage of net Toronto-Dominion Bank (The) 3.1 By Industry (1)(2) asset value † Brookfield Asset Management Inc., Class "A" 3.1 Financials 26.4 Sherwin-Williams Company (The) 3.0 Information Technology 17.7 Apple Inc. 3.0 Consumer Discretionary 14.6 Visa Inc., Class "A" 2.9 Industrials 14.1 Cash and Short Term Instruments (Bank Overdraft) 2.9 Communication Services 8.2 Royal Bank of Canada 2.9 Materials 7.3 Nuvei Corporation, Subordinated Voting 2.5 Health Care 4.1 Danaher Corporation 2.4 Consumer Staples 3.9 CCL Industries Inc., Class "B" 2.3 Cash and Short Term Instruments (Bank Overdraft) 2.9 CGI Inc. -

Canadian Focus List

RBC Dominion Securities Inc. Canadian Focus List March 1, 2017 | Quarterly Report Portfolio Advisory Group – Equities What’s inside 3 Portfolio positions Waiting for the baton to be passed 4 Sector commentary The Canadian Focus List delivered a solid return amid a search for clarity on U.S. policy direction. 8 Alimentation Couche-Tard Inc. Portfolio increase 9 Canadian National Railway Improved global economic data helped Markets were surprisingly calm during Portfolio increase set the market on an upward trajectory the Portfolio’s winter 2017 quarter with 10 Canadian Pacific Railway Ltd. in early 2016. Despite initial trepidation, volatility holding at historically low the election of a U.S. president set on levels. We believe it is reasonable to Portfolio decrease slashing tax rates, increasing fiscal expect moments of market anxiety in 11 Cott Corporation spending, and cutting regulatory red the months to come as policy-related Portfolio removal tape stoked investor enthusiasm for headlines influence expectations for 12 Dollarama Inc. higher potential corporate earnings future tax rates, fiscal spending levels, and set the stage for the market’s next and regulatory oversight. In such an Portfolio increase leg higher late last year. We have now environment, we believe clients are well 13 Imperial Oil Ltd. entered a period where investors are served by the Focus List’s prudent mix Portfolio removal looking for signs that the baton is in of economically sensitive and defensive 14 Magna International Inc. the process of being passed from policy positions in addition to adherence to Portfolio increase rhetoric to tangible action. the Portfolio’s core tenet of emphasizing high-quality, well-managed businesses. -

Gildan Activewear Nominates Four New Directors to Board

Gildan Activewear Nominates Four New Directors to Board Montreal, Thursday, March 29, 2018 - Gildan Activewear Inc. (GIL: TSX and NYSE) today announced that its Board of Directors has nominated Maryse Bertrand, Marc Caira, Charles M. Herington and Craig Leavitt as Director nominees to be voted on by the Company’s shareholders at its upcoming Annual Meeting of Shareholders to be held on May 3, 2018 in Montreal, Quebec. “The competitive dynamics in the apparel industry continue to evolve and these proposed director candidates are highly accomplished individuals who will bring a wealth of experience to the Board as the Company continues to grow” said Gildan’s Chairman Bill Anderson. Maryse Bertrand has had a career in law and business spanning over 35 years. Ms. Bertrand is currently an advisor in corporate governance and risk management and is a member of the Boards of Directors of National Bank of Canada, Canada’s sixth largest retail and commercial bank, and Metro Inc., a leader in the grocery and pharmaceutical distribution sectors in Canada. From 2016 to 2017, she was Strategic Advisor and Counsel to Borden Ladner Gervais LLP, and, prior to that she was Vice-President, Real Estate Services, Legal Services and General Counsel at CBC/Radio-Canada, Canada’s public broadcaster. Prior to 2009, Ms. Bertrand was a partner at Davies Ward Phillips and Vineberg LLP, where she specialized in M&A and corporate finance, and served on the firm’s National Management Committee. She was named as Advocatus emeritus (Ad. E.) in 2007 by the Quebec Bar in recognition of her exceptional contribution to the legal profession. -

Manulife Fidelity True North Fund

CANADIAN LARGE CAP EQUITY Code 7143 Volatility meter Low High Manulife Fidelity True North Fund Fund (6) Benchmark (9) Based on 3 year standard deviation How the underlying fund is invested UNDERLYING FUND -> Fidelity True North Fund - O Objective The Fund aims to achieve long term capital growth by investing primarily in Canadian Composition equity securities. Canadian Equity 78.50% United States Equity 9.08% Managed by FIAM LLC Cash & Equivalents 8.47% Fund managers Maxime Lemieux Foreign Equity 2.88% Other 1.07% Inception date February 2001 Manulife inception date January 2009 Total assets $5,079.1 million Underlying fund operating expense (2015) in IMF Equity Industry Financials 17.69% Energy 16.87% Consumer Staples 10.82% Consumer Discretionary 9.79% Industrials 9.30% Information Technology 8.17% Materials 6.24% Other 21.12% Overall past performance This graph shows how a $10,000 investment in this fund would have changed in value over time, Geographic split based on gross returns. Gross rates of return are shown before investment management Canada 78.56% fees have been deducted. The shaded returns represent the underlying fund returns prior to the United States 9.04% Manulife Fund’s inception date. United Kingdom 0.77% Israel 0.55% Japan 0.51% Manulife Fidelity True North Fund - ($18,950) Ireland 0.51% S&P/TSX Composite Cap TR - ($14,386) Bermuda 0.45% Fidelity True North Fund Series O Other 9.61% Top holdings within the underlying fund (As at June 30, 2016) 15,000 Toronto-Dominion Bank 7.41% Loblaw Companies -

Stock-Table-Canada-Newsletter.Pdf

The table below displays stock information as of February 1, 2021. Stock information for March will be available by March 5, 2021. EDWARD JONES STOCKS § Ticker Symbol Ticker Current Opinion Price Recent Forward Est. on Based P/E Forward Est. L-T EPS Growth Estimate PEGY DividendsAnnual Dividend Yield L-T Dividend Growth Estimate DividendsCash Since Invested $10,000 10 Years Ago CategoryInvestment Important Disclosures (High – Low) EPS AS OF 02/01/21 Range Price 52-week S&P / TSX Composite 17692.45 18058.61 - 11172.73 1215.59 14.6 6 1.6 538.38 3.04 12,902 COMMUNICATION SERVICES (8%) Alphabet - US GOOGL BUY 1893.07 1932.08 - 1008.87 61.74 30.7 15 2.0 0.00 0.0 NA 61,902 G AT&T - US T BUY 28.65 38.82 - 26.08 3.33 8.6 3 0.8 2.08 7.3 0 1984 17,934 G/I 12 BCE - Canada BCE.T BUY 54.51 65.28 - 46.03 3.43 15.9 4 1.6 3.33 6.1 4 1881 25,056 G/I Omnicom Group - US OMC BUY 62.86 80.25 - 44.50 5.96 10.5 7 1.0 2.60 4.1 5 1986 18,340 G Rogers Communications - Canada RCI.B.T HOLD 58.05 66.87 - 46.81 3.74 15.5 4 2.1 2.00 3.4 0 2003 23,801 G/I Shaw Communications - Canada SJR.B.T BUY 22.17 26.64 - 17.77 1.47 15.1 4 1.6 1.19 5.4 0 1982 16,259 G/I TELUS - Canada T.T BUY 26.54 27.74 - 18.55 1.30 20.4 5 2.1 1.24 4.7 5 1993 32,613 G/I Verizon Communications - US VZ BUY 54.28 61.95 - 48.84 4.93 11.0 4 1.3 2.51 4.6 2 1984 23,620 G/I CONSUMER DISCRETIONARY (8%) Amazon - US AMZN BUY 3342.88 3552.25 - 1626.03 45.00 74.3 30 2.5 0.00 0.0 NA 194,229 G Canadian Tire - Canada CTC.A.T HOLD 171.48 181.57 - 67.15 12.00 14.3 8 1.3 4.70 2.7 10 1996 33,245 G/I Dollarama - Canada -

Fund Profile

Manulife Fidelity True North GIF Select GIF SELECT InvestmentPlus (F-Class) · Performance as at August 31, 2021 · Holdings as at July 31, 2021 GROWTH OF $10,000 ± INVESTMENT OBJECTIVE The Fund aims to achieve long-term capital growth. It invests primarily in equity securities of Canadian companies. CALENDAR RETURNS % 2012 2013 2014 2015 2016 2017 2018 2019 2020 8.75 22.79 13.77 -1.64 10.32 5.26 -4.68 17.68 10.45 COMPOUND RETURNS % 1 mth 3 mths 6 mths YTD 1 yr 3 yrs 5 yrs 10 yrs Incept. 2.57 7.23 16.72 19.94 29.16 12.86 9.80 9.50 8.96 ASSET ALLOCATION % GEOGRAPHIC ALLOCATION % SECTOR ALLOCATION % OVERVIEW Inception Date: October 18, 2010 Asset Class: Canadian Equity Net Assets: $261.5 million Risk: Medium Legend Weight % Name Legend Weight % Name Legend Weight % Name Low High 97.70 Equities 92.36 Canada 31.22 Financials Fund Status: Open * 2.95 Cash and equivalents 5.96 United States 15.47 Industrials 0.01 Fixed income 1.03 Bermuda 13.35 Information tech. Management Fee: 1.45% 0.22 Israel 9.13 Materials Management Expense Ratio1: 2.05% 0.16 Australia 7.70 Cons. discrectionary 0.15 United Kingdom 7.19 Energy AWARDS 0.08 Singapore 5.52 Consumer staples 0.04 Germany 3.86 Communication serv. 3.25 Utilities 1.71 Real Estate 1.59 Health care UNDERLYING FUND INFORMATION TOP 10 HOLDINGS % ® Name: Fidelity True North Fund Royal Bank of Canada 8.36 Underlying Fund Manager: Toronto-Dominion Bank Com New 4.59 Fidelity Investments Canada ULC Shopify Inc. -

Annual Information Form

ANNUAL INFORMATION FORM FISCAL YEAR ENDED FEBRUARY 2, 2020 April 29, 2020 TABLE OF CONTENTS 1 Explanatory Notes ........................................................................................ 1 2 Corporate Structure ...................................................................................... 3 3 General Development of the Business ....................................................... 4 4 Business of the Corporation ....................................................................... 8 5 Risk Factors ................................................................................................ 20 6 Description of Capital Structure ................................................................ 32 7 Dividends ..................................................................................................... 34 8 Description of Material Indebtedness ....................................................... 34 9 Ratings ......................................................................................................... 37 10 Market for Securities .................................................................................. 40 11 Directors and Officers ................................................................................ 40 12 Audit Committee Information .................................................................... 43 13 Legal Proceedings and Regulatory Actions ............................................ 45 14 Interest of Management and Others in Material Transactions .............. -

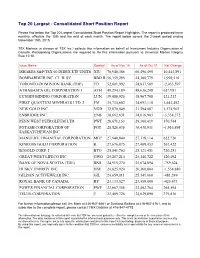

Top 20 Largest - Consolidated Short Position Report

Top 20 Largest - Consolidated Short Position Report Please find below the Top 20 Largest Consolidated Short Position Report Highlights. The report is produced twice monthly, effective the 15th and the end of each month. The report below covers the 2-week period ending November 15th, 2015. TSX Markets (a division of TSX Inc.) collects this information on behalf of Investment Industry Organization of Canada. Participating Organizations are required to file this information pursuant to Universal Market Integrity Rule 10.10. Issue Name Symbol As of Nov 15 As of Oct 31 Net Change ISHARES S&P/TSX 60 INDEX ETF UNITS XIU 70,940,386 60,496,495 10,443,891 BOMBARDIER INC. CL 'B' SV BBD.B 56,359,295 54,360,779 1,998,516 TORONTO-DOMINION BANK (THE) TD 52,801,992 54,837,589 -2,035,597 ATHABASCA OIL CORPORATION J ATH 49,294,189 48,636,208 657,981 LUNDIN MINING CORPORATION LUN 39,088,920 38,967,708 121,212 FIRST QUANTUM MINERALS LTD. J FM 35,734,602 34,091,110 1,643,492 NEW GOLD INC. NGD 32,870,049 31,294,087 1,575,962 ENBRIDGE INC. ENB 30,662,631 34,016,903 -3,354,272 PENN WEST PETROLEUM LTD. PWT 28,671,163 28,300,419 370,744 POTASH CORPORATION OF POT 28,520,036 30,436,931 -1,916,895 SASKATCHEWAN INC. MANULIFE FINANCIAL CORPORATION MFC 27,940,840 27,318,114 622,726 KINROSS GOLD CORPORATION K 27,676,875 27,409,453 267,422 B2GOLD CORP. -

The Leaders, Volume 11 Construction and Engineering Items Appearing in This Magazine Is Reserved

SHARING YOUR VISION. BUILDING SUCCESS. Humber River Hospital, Toronto ON 2015 Dan Schwalm/HDR Architecture, Inc. We are Canada’s construction leaders. We look beyond your immediate needs to see the bigger picture, provide solutions, and ensure that we exceed your expectations. PCL is the proud builder of Canada’s landmark projects. Watch us build at PCL.com Message from Vince Versace, National Managing Editor, ConstructConnect 4 East and West connected by rail 6 On the road: the Trans-Canada Highway – Canada’s main street 21 Chinese workers integral in building Canada’s first megaproject 24 Canada’s most transformational project, the building The CN Tower: Canada’s iconic tower 53 of the Canadian Pacific Railway. From the ground up: building Canada’s parliamentary precinct 56 CanaData Canada’s Economy on Mend, but Don’t Uncork the Champagne Just Yet 14 Fighting the Fiction that Prospects are Nothing but Rosy in Western Canada 26 In Eastern Canada, Quebec is Winning the Accolades 60 Canada’s Top 50 Leaders in Construction 5 Leaders in Construction – Western Canada 28 Leaders in Construction – Eastern Canada 62 Advertisers’ Index 90 www.constructconnect.com Publishers of Daily Commercial News and Journal of Commerce Construction Record 101-4299 Canada Way 3760 14th Avenue, 6th Floor Burnaby, British Columbia Markham, Ontario L3R 3T7 V5G 1H3 Phone: (905) 752-5408 Phone: (604) 433-8164 Fax: (905) 752-5450 Fax: (604) 433-9549 www.dailycommercialnews.com www.journalofcommerce.com CanaData www.canadata.com Mark Casaletto, President John Richardson, Vice President of Customer Relations Peter Rigakos, Vice President of Sales Marg Edwards, Vice President of Content Alex Carrick, Chief Economist, CanaData Vince Versace, National Managing Editor Mary Kikic, Lead Designer Erich Falkenberg, National Production Manager Kristin Cooper, Manager, Data Operations Copyright © 2017 ConstructConnect™. -

Canadian General Investments, Limited May 2017 Monthly Factsheet

Canadian General Investments, Limited May 2017 Monthly Factsheet Canadian General Investments, Limited (CGI or the Company) is domiciled in Canada and incorporated under the laws of Ontario, Canada. CGI is a closed-end equity fund focussed on medium- to long-term investments in Canadian corporations. The Company’s common shares are publicly listed and trade on the Toronto Stock Exchange and the London Stock Exchange (symbol CGI). PORTFOLIO ANALYSIS FUND DETAILS Top 10 Holdings Investment Objective Sector % of Portfolio It strives, through prudent security selection, timely recognition of Dollarama Inc. Consumer Discretionary 5.4% capital gains/losses and appropriate income generating Franco-Nevada Corporation Materials 4.1% instruments, to provide better than average returns to investors. NVIDIA Corporation Information Technology 3.8% Bank of Montreal Financials 3.2% Portfolio Manager D. Greg Eckel Open Text Corporation Information Technology 3.2% Morgan Meighen & Associates Canadian Pacific Railway Limited Industrials 3.2% Board of Directors James F. Billett CCL Industries Inc., B NV Materials 3.1% A. Michelle Lally Amazon.com, Inc. Consumer Discretionary 3.1% Jonathan A. Morgan Shopify Inc. Information Technology 3.0% Vanessa L. Morgan Royal Bank of Canada Financials 3.0% R. Neil Raymond 35.1% Michael A. Smedley Richard O'C. Whittall Relative Performance - 5 Years - Total Return, with dividends reinvested Year End December 31 $20,000 Inception 1930 $18,000 TSX and LSE Symbol CGI $16,000 ISIN CA1358251074 $14,000 Benchmark S&P/TSX Composite -

Stoxx® Canada Total Market Mid Index

STOXX® CANADA TOTAL MARKET MID INDEX Components1 Company Supersector Country Weight (%) EMERA Utilities Canada 3.01 BAUSCH HEALTH Health Care Canada 2.71 WSP GLOBAL Construction & Materials Canada 2.59 Teck Resources Ltd. Cl B Basic Resources Canada 2.48 Canadian Tire Corp. Ltd. Cl A Retail Canada 2.36 ALGONQUIN POWER & UTILITIES Utilities Canada 2.34 CAE Industrial Goods & Services Canada 2.27 CCL INDS.'B' Industrial Goods & Services Canada 2.12 CANADIAN APARTMENT PROP REIT Real Estate Canada 2.11 Kinross Gold Corp. Basic Resources Canada 2.11 TFI INTERNATIONAL Industrial Goods & Services Canada 2.04 LIGHTSPEED POS Technology Canada 1.97 AIR CANADA Travel & Leisure Canada 1.95 Cameco Corp. Energy Canada 1.93 INTER PIPELINE Energy Canada 1.83 TOROMONT INDUSTRIES Industrial Goods & Services Canada 1.81 TOURMALINE OIL Energy Canada 1.81 GILDAN ACTIVEWEAR Consumer Products & Services Canada 1.77 Blackberry Ltd Technology Canada 1.72 RITCHIE BROS.AUCTIONEERS (NYS) Consumer Products & Services Canada 1.68 WEST FRASER TIMBER Basic Resources Canada 1.62 FIRSTSERVICE Real Estate Canada 1.62 NORTHLAND POWER Utilities Canada 1.56 PAN AMER.SILV. (NAS) Basic Resources Canada 1.55 LUNDIN MINING Basic Resources Canada 1.53 ALTAGAS Utilities Canada 1.51 KEYERA CORP Energy Canada 1.51 IA FINANCIAL CORP Insurance Canada 1.51 EMPIRE 'A' Personal Care, Drug & Grocery Stores Canada 1.49 DESCARTES SYSTEMS GROUP Technology Canada 1.44 RIOCAN REIT.TST. Real Estate Canada 1.44 ONEX Financial Services Canada 1.44 TMX GROUP Financial Services Canada 1.41 ARC RESOURCES LTD Energy Canada 1.29 Element Fleet Management Corp. -

Manulife Fundamental Balanced Class GIF Select GIF SELECT Investmentplus (F-Class) · Performance As at August 31, 2021 · Holdings As at July 31, 2021

Manulife Fundamental Balanced Class GIF Select GIF SELECT InvestmentPlus (F-Class) · Performance as at August 31, 2021 · Holdings as at July 31, 2021 GROWTH OF $10,000 ± INVESTMENT OBJECTIVE The Manulife Fundamental Balanced Class fund seeks to provide long-term total return by investing primarily in a diversified portfolio of Canadian equity, fixed income and money market securities. CALENDAR RETURNS % 2012 2013 2014 2015 2016 2017 2018 2019 2020 — — — — — — — — — COMPOUND RETURNS % 1 mth 3 mths 6 mths YTD 1 yr 3 yrs 5 yrs 10 yrs Incept. 1.80 5.76 14.30 14.74 19.77 — — — — OVERVIEW ASSET ALLOCATION % GEOGRAPHIC ALLOCATION % SECTOR ALLOCATION % Inception Date: May 4, 2020 Asset Class: Canadian Equity Balanced Net Assets: $1.4 million Risk: Low to Medium Low High Legend Weight % Name Legend Weight % Name Legend Weight % Name Fund Status: Open * 65.03 Equities 71.65 Canada 22.93 Financials 18.95 Cash and equivalents 21.96 United States 16.55 Industrials Management Fee: 1.32% 13.99 Fixed income 2.28 United Kingdom 15.83 Information tech. Management Expense Ratio1: 1.51% 1.94 France 11.91 Health care 1.64 Netherlands 11.17 Cons. discrectionary 0.36 Europe 9.02 Communication serv. UNDERLYING FUND INFORMATION 0.09 Jersey Channel 5.75 Energy Name: Manulife Fundamental Balanced Class Islands 3.16 Consumer staples Underlying Fund Manager: 0.07 Great Britain 2.04 Materials 1.24 Real Estate Manulife Investment Management Limited 0.41 Utilities Portfolio Managers: Patrick Blais, Cavan Yie, FIXED INCOME ALLOCATION % TOP 10 HOLDINGS % Roshan Thiru Canadian provincial bonds 29.55 Gov.