Vornado Realty Lp

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vornado Realty Trust

SECURITIES AND EXCHANGE COMMISSION FORM 8-K Current report filing Filing Date: 2017-06-05 | Period of Report: 2017-06-05 SEC Accession No. 0001104659-17-037358 (HTML Version on secdatabase.com) FILER VORNADO REALTY TRUST Mailing Address Business Address 888 SEVENTH AVE 888 SEVENTH AVE CIK:899689| IRS No.: 221657560 | State of Incorp.:MD | Fiscal Year End: 0317 NEW YORK NY 10019 NEW YORK NY 10019 Type: 8-K | Act: 34 | File No.: 001-11954 | Film No.: 17889956 212-894-7000 SIC: 6798 Real estate investment trusts VORNADO REALTY LP Mailing Address Business Address 888 SEVENTH AVE 210 ROUTE 4 EAST CIK:1040765| IRS No.: 133925979 | State of Incorp.:DE | Fiscal Year End: 1231 NEW YORK NY 10019 PARAMUS NJ 07652 Type: 8-K | Act: 34 | File No.: 001-34482 | Film No.: 17889957 212-894-7000 SIC: 6798 Real estate investment trusts Copyright © 2017 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported): June 5, 2017 VORNADO REALTY TRUST (Exact Name of Registrant as Specified in Charter) Maryland No. 001-11954 No. 22-1657560 (State or Other (Commission (IRS Employer Jurisdiction of File Number) Identification No.) Incorporation) VORNADO REALTY L.P. (Exact Name of Registrant as Specified in Charter) Delaware No. 001-34482 No. 13-3925979 (State or Other (Commission (IRS Employer Jurisdiction of -

Amazon's Document

REQUEST FOR INFORMATION Project Clancy TALENT A. Big Questions and Big Ideas 1. Population Changes and Key Drivers. a. Population level - Specify the changes in total population in your community and state over the last five years and the major reasons for these changes. Please also identify the majority source of inbound migration. Ne Yok Cit’s populatio ge fo . illio to . illio oe the last fie eas ad is projected to surpass 9 million by 2030.1 New York City continues to attract a dynamic and diverse population of professionals, students, and families of all backgrounds, mainly from Latin America (including the Caribbean, Central America, and South America), China, and Eastern Europe.2 Estiate of Ne York City’s Populatio Year Population 2011 8,244,910 2012 8,336,697 2013 8,405,837 2014 8,491,079 2015 8,550,405 2016 8,537,673 Source: American Community Survey 1-Year Estimates Cumulative Estimates of the Components of Population Change for New York City and Counties Time period: April 1, 2010 - July 1, 2016 Total Natural Net Net Net Geographic Area Population Increase Migration: Migration: Migration: Change (Births-Deaths) Total Domestic International New York City Total 362,540 401,943 -24,467 -524,013 499,546 Bronx 70,612 75,607 -3,358 -103,923 100,565 Brooklyn 124,450 160,580 -32,277 -169,064 136,787 Manhattan 57,861 54,522 7,189 -91,811 99,000 1 New York City Population Projections by Age/Sex & Borough, 2010-2040 2 Place of Birth for the Foreign-Born Population in 2012-2016, American Community Survey PROJECT CLANCY PROPRIETARY AND CONFIDENTIAL 4840-0257-2381.3 1 Queens 102,332 99,703 7,203 -148,045 155,248 Staten Island 7,285 11,531 -3,224 -11,170 7,946 Source: Population Division, U.S. -

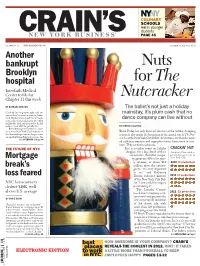

Nuts for the Nutcracker

CULINARY SCHOOLS reel in younger students CRAIN’S® PAGE 45 NEW YORK BUSINESS VOL. XXVIII, NO. 49 WWW.CRAINSNEWYORK.COM DECEMBER 3-9, 2012 PRICE: $3.00 Another bankrupt Nuts Brooklyn hospital for The Interfaith Medical Center to file for Nutcracker Chapter 11 this week BY BARBARA BENSON The ballet’s not just a holiday Crushed by long-term debt and ex- mainstay, it’s plum cash that no penses that far outstrip revenue, Inter- faith Medical Center will file for bank- dance company can live without ruptcy this week,making the Brooklyn facility the 11th city hospital or health system since 2005 to go belly up. BY THERESA AGOVINO Behind that grim statistic is a com- mon story:New York City hospitals on Black Friday not only kicks off the start of the holiday shopping the financial ropes can no longer count season, it also marks the beginning of the annual run of The Nut- on a bailout from Albany.For years,the See INTERFAITH on Page 44 crackerat the New York City Ballet.And it turns out that discount- ed cashmere sweaters and sugarplum fairies have much in com- mon: They are both cash cows. THE FUTURE OF NYC Just as retailers count on holiday CRACKIN’ NUT shoppers for a big chunk of their Number of Nutcracker annual sales, the ballet compa- productions per year in Mortgage ny generates 45% of its year- New York City ly revenue, or about $12 2010 14 productions break’s million, from the extrava- ganza. “It is very important to us,” said Katherine loss feared Brown, executive director 2011 17 productions of the New York City Bal- NYC homeowners let. -

Chapter 9: Urban Design and Visual Resources A. INTRODUCTION

Chapter 9: Urban Design and Visual Resources A. INTRODUCTION This chapter considers the potential effects of the proposed project on urban design and visual resources. It is expected that the Farley Complex, an important visual resource, would be altered by the insertion of a new intermodal hall between West 31st and 33rd Streets that would be enclosed with a glass skylight, as envisioned in the preliminary design that was previously considered in 1999. Further, since Phase II of the proposed project could include construction of a structure of up to 1 million zoning square feet either above the Western Annex or on the Development Transfer Site at Eighth Avenue between West 34th and West 33rd Streets, it could create a more visible alteration to the urban design character of the study area. As recommended by the CEQR Technical Manual, the study area is, therefore, defined as the area within approximately 400 feet of the project site—an area bounded by West 30th and 34th Streets, the west side of Ninth Avenue and the east side of Eighth Avenue (see Figure 9-1). This chapter has been prepared in accordance with the State Environmental Quality Review Act (SEQRA), which requires that State agencies consider the effects of their actions on urban design and visual resources. The technical analysis follows the guidance of the CEQR Technical Manual. As defined in the manual, urban design components and visual resources determine the “look” of a neighborhood—its physical appearance, including the street pattern, the size and shape of buildings, their arrangement on blocks, streetscape features, natural features, and noteworthy views that may give an area a distinctive character. -

Penn Station, NY

Station Directory njtransit.com Penn Station, NY VENDOR INFORMATION Upper Level RAIL INFORMATION FOOD CONCOURSE LEVEL Auntie Anne’s (3 locations) ................ Amtrak/NJ TRANSIT Upper (2 locations) .................................. Exit Concourse/LIRR Lower NJ TRANSIT Au Bon Pain....................................... LIRR Lower Caruso Pizza ...................................... LIRR Lower Montclair-Boonton Line Carvel................................................ LIRR Lower Trains travel between Penn Station New York Central Market ................................... LIRR Lower and Montclair with connecting service to Chickpea (1 location) ......................... Amtrak/NJ TRANSIT Upper Hackettstown. 34th Street Down to (1 location)................................... LIRR Lower Down to LIRR Subway Down to Down to Morris & Essex Lines Cinnabon ........................................... LIRR Lower Subway To Subway Port Authority ONE PENN PLAZA ENTRANCE CocoMoko Cafe .................................. Amtrak/NJ TRANSIT Upper Bus Terminal, EXIT Down to Trains travel between Penn Station New York 8th Ave & 41st St Down to Subway Colombo Yogurt ................................. LIRR Lower (6 blocks) Lower Level to Summit and Dover or Gladstone. Cookie Cafe........................................ Exit Concourse Lower One Penn Plaza Down to Don Pepi Deli..................................... Amtrak/NJ TRANSIT Upper Lower Level Northeast Corridor Don Pepi Express (cart) ...................... LIRR Lower Trains travel between Penn Station -

2005 Manhattan Hotel Market Overview Page 1 of 22

HVS International : 2005 Manhattan Hotel Market Overview Page 1 of 22 Manhattan Hotel Market Overview HVS International, in cooperation with New York University’s Preston Robert Tisch Center for Hospitality, Tourism, and Sports Management, is pleased to present the eighth annual Manhattan Hotel Market Overview. In 2004, the Manhattan lodging market experienced an impressive recovery, with a RevPAR increase of 22% compared to 2003. From March through December of 2004, the market recorded double-digit growth in RevPAR each month, ranging from a high of 41% in April to a low of roundly 17% in October. At 83.2%, overall occupancy reached close to the historical peak achieved in 2000 (at 83.7%) while marketwide average rate was less than 10% below the 2000 level. Occupancy and average rate in 2005 should surpass 2000 levels. Due to limited new supply and increased compression resulting from near-maximum-capacity occupancy levels, overall RevPAR will experience double-digit growth for the next few years. Based on an overall improved economic climate, strong barriers to entry, limited new supply, and increased compression, we forecast the Manhattan lodging market to achieve a robust ±17% RevPAR growth in 2005. HVS International HVS International is a global consulting and services organization focused on the hotel, restaurant, timeshare, gaming, and leisure industries. Its clients rely on the firm’s specialized industry knowledge and expertise for advice and services geared to enhance economic returns and asset value. Through a network of 23 offices staffed by more than 200 seasoned industry professionals, HVS offers a wide scope of services that track the development/ownership process. -

Advisory Board Calendar

ADVISORY BOARD CALENDAR May 20, 2009 Calendar # Submission # Applicant Name andAddress Type of Request Installation Location Status Fee 49327CO 09A0114CO Essential Electric Corp. Requested approval for the electric service Approved $0.00 32 East 31st Street, 8th Floor equipment proposed to be installed 630 East 104th Street New York NY 10016 Brooklyn NY Carry over from March 18, 2009 meeting. Add note to drawing indicating that no life safety ATS is located in the service room. 49329CO 09A0116cO Crana Electric Inc. Requested approval for the electric service Approved $0.00 600A East 132nd Street equipment proposed to be installed 131 8th Avenue Bronx NY 10454 New York NY Carry over from March 18, 2009 meeting. 1) Verify that service entrance conductors are Con-ED. 2) All switchboards must pick up the grounding electrode conductor. Job finalized 07/9/09. 49349CO3 09A0136CO3 Michael Mazzeo Electric Corp. Requested approval for the electric service Verizon Hold $0.00 41-24 24th Street equipment proposed to be installed 240 East 38th Street Long Island City NY 11101 New York NY Carry over from April 15, 2009 meeting. 1) Load shedding sequence not provided. 2) Provide ground fault protection or all non-life safety loads. 3) The emergency loads must comply with the current codes. 49387CO 09A0146CO JMC Electric Corp. Requested approval for the electric service Approved $0.00 172-02 39th Avenue equipment proposed to be installed 10 Monroe Street Flushing NY 11358 New York NY Carry over from April 15, 2009 meeting. 49405CO 09A0164CO Linco Electrical Contracting, Inc. Requested approval for the electric service NY Aquarium Hold $0.00 5442 Arthur Kill Road equipment proposed to be installed 502 Surf Avenue Staten Island NY 10307 Brooklyn NY Carry over from April 15, 2009 meeting. -

Roger Brown (1941 – 1997)

Roger Brown (1941 – 1997) Born, Hamilton, AL Died, Atlanta, GA Education 1970, MFA School of the Art Institute of Chicago 1968, BFA School of the Art Institute of Chicago 1962-1964 attended the American Academy of Art Solo Exhibitions 2015 Roger Brown: Political Paintings, DC Moore Gallery, New York, NY, June 18 – July 31, 2015 Roger Brown: Virtual Still Life, Maccarone Gallery, New York, NY, June 25 – August 7, 2015 2014 Roger Brown: Virtual Still Life, Russell Bowman Art Advisory, September 5 – November 1, 2014 Roger Brown: His American Icons, The Hughes Gallery, Sydney, Australia, March 22 - April 14, 2014 2013 Roger Brown, DC Moore Gallery, New York, NY, January 10 - February 9, 2013 2012 Roger Brown: This Boy’s Own Story, Sullivan Galleries, School of the Art Institute of Chicago, IL, August 24 – November 10, 2012 Dual exhibition, Roger Brown: Major Paintings, Russell Bowman Art Advisory, Chicago, IL and Zolla Lieberman Gallery, Chicago, IL, September 7 - October 27, 2012 Roger Brown: Urban Traumas and Natural Disasters, Springfield Art Museum, Springfield, MO, September 17 – November 13, 2012 2011 Roger Brown: Calif. U.S.A., Hyde Park Art Center, Chicago, IL, June 20 – October 3 roger brown: urban traumas and natural disasters, Springfield Art Museum, Springfield, MO, September 17 - November 13 1 2010 Roger Brown: Calif. U.S.A., curated by Nicholas Lowe, Hyde Park Art Center, Chicago, IL, June 20 – October 3, 2010 2009 Roger Brown: Early Work, Major Paintings and Constructions, 1968-1980, Russell Bowman Art Advisory, Chicago, IL, March 27 – May 16 Roger Brown, Art Works: Chicago A Progressive Corporate Exhibition of Chicago Artists, Metropolitan Capital Bank, Chicago, IL 2008 Roger Brown: The American Landscape, DC Moore Gallery, New York, NY, May 1 – June 13 2007-2009 Roger Brown: Southern Exposure, curated by Sidney Lawrence, The Jule Collins Smith Museum of Fine Art at Auburn University, AL, October 6, 2007 – January 5, 2008. -

Chapter 5: Shadows

Chapter 5: Shadows A. INTRODUCTION This chapter presents the detailed shadow study that was conducted to determine whether the proposed One Vanderbilt development would cast any new shadows on sunlight-sensitive resources. Sunlight-sensitive resources can include parks, playgrounds, residential or office plazas, and other publicly accessible open spaces; sunlight-dependent features of historic resources; and important natural features such as water bodies. Since the preparation of the shadow analysis in the Draft Environmental Impact Statement (DEIS), the height of the proposed One Vanderbilt development was increased. The shadow analysis in this Final Environmental Impact Statement (FEIS) has been revised to reflect this change including Figures 5-1 to 5-22 and 5-27. PRINCIPAL CONCLUSIONS This analysis compared shadows that would be cast by the proposed One Vanderbilt development, which would be built to a floor area ratio (FAR) of 30, with those that would be cast by the 15 FAR building that would be developed absent the proposed actions (the 15 FAR No-Action building). As described below, the analysis concluded that the proposed 30 FAR One Vanderbilt development would cast new shadows on Bryant Park, the west windows of Grand Central Terminal’s main concourse and several other sunlight-sensitive resources. However, the new shadows would be limited in extent, duration and effects and would not result in any significant adverse shadow impacts, as demonstrated in detail below. B. DEFINITIONS AND METHODOLOGY This analysis has been prepared in accordance with CEQR procedures and follows the guidelines of the 2014 City Environmental Quality Review (CEQR) Technical Manual. DEFINITIONS Incremental shadow is the additional, or new, shadow that a structure resulting from a project would cast on a sunlight-sensitive resource. -

Moynihan East&West

A Regional Rail Center: MOYNIHAN EAST&WEST August 2007 • • moynihanstation.org Acknowledgments Regional Plan Association and the Friends of Moyni- han Station extend their deepest gratitude to the Leon Levy Foundation whose generous grant made this report possible. This report was written by Jeffrey Zupan, Senior Fellow for Transportation, and Juliette Michaelson, Senior Planner. Il- lustrations were designed by Jeff Ferzoco, Senior Designer, and layout was arranged by Yonah Freemark, Design Intern. Special thanks to Maura Moynihan for her leadership on this project. Note: the drawings at the top of some of the pages in this report are based on the ornament on the ceiling of the Far- ley Post Office. The Original Pennsylvania Station, New York City’s grand gateway until 1961 A Regional Rail Center: Moynihan East & West Table of Contents Executive Summary 5 Introduction and Purpose 6 The Benefits 8 Transform Penn Station into the Regional Rail Center Create a Great Public Space and a Gateway to NYC Establish a Transit-Oriented District Create a Passenger-Friendly Design Integrate the Station with the Neighborhood Provide More Efficient and Flexible Train Operations The Plans 15 Moynihan West Moynihan East Do the Venture’s Plans Deliver the Benefits? 18 Conclusion 22 RPA | Friends of Moynihan Station Penn Station is the most heavily used train station in the country in spite of itself. A new Moynihan Station would become the region’s pre-eminent transportation center and a catalyst for the nation’s largest transportation- oriented development district, providing New York with enormous new capacity for efficient transportation and compact, energy-efficient, high-density development. -

Against All Odds MIT's Pioneering Women of Landscape Architecture

Against all Odds MIT’s Pioneering Women of Landscape Architecture * Eran Ben-Joseph, Holly D. Ben-Joseph, Anne C. Dodge1 Massachusetts Institute of Technology, School of Architecture and Planning, City Design and Development Group 77 Massachusetts Ave. 10-485 Cambridge, MA 02139 1 November 2006 * Recipient of the 6th Milka Bliznakov Prize Commendation: International Archive of Women in Architecture (IAWA) This research is aimed at exposing the influential, yet little known and short-lived landscape architecture program at the Massachusetts Institute of Technology (MIT) between 1900 and 1909. Not only was it one of only two professional landscape architecture education programs in the United States at the time (the other one at Harvard also started at 1900), but the first and only one to admit both women and men. Women students were attracted to the MIT option because it provided excellent opportunities, which they were denied elsewhere. Harvard, for example did not admit women until 1942 and all-women institutions such as the Cambridge School or the Cornell program were established after the MIT program was terminated. Unlike the other schools of that time, the MIT program did not keep women from the well-known academic leaders and male designers of the time nor from their male counterparts. At MIT, women had the opportunity to study directly with Beaux-Art design pioneers such as Charles S. Sargent, Guy Lowell, Désiré Despradelle, and the revered department head Francis Ward Chandler. Historical accounts acknowledged that a woman could “put herself through a stiff course” at MIT including advance science and structural engineering instruction. -

Making the Most of Our Parks

Making the Most of Our Parks RECREATION EXERCISE RESPITE PLAY ENSURING GREENER, SAFER, CLEANER PARKS, TOGETHER A SUMMARY OF A REPORT BY THE CITIZENS BUDGET COMMISSION AT THE REQUEST OF NEW YORKERS FOR PARKS NEW YORK’S NONPARTISAN VOICE SEPTEMBER 2007 FOR EFFECTIVE GOVERNMENT MAKING THE MOST OF OUR PARKS the challenge to new yorkers Parks play important roles in city life. They are a source of respite from the bustle of the urban environment, a place for active recreation and exercise for adults, and a safe place for children to play outdoors. In addition, parks preserve sensitive environmen- tal areas, and, by making neighborhoods more attractive, enhance property values and the tax base of the city. Given the benefits of urban parks, it should be reassuring to New Yorkers that more than 37,000 acres, or nearly one-fifth the city’s total land area, is parkland. This pro- portion is larger than in most big cities in the United States, suggesting that New Yorkers are well endowed with parks. But New Yorkers face a distinct challenge in enjoying their parks. Their parks must accommodate an unparalleled volume of people. New York has about 217 residents for each acre of parkland, one of the highest ratios in the nation, compared to a national average among large cities of about 55 residents per acre. When the extraordinarily large number of commuters and tourists is added to New York’s resident population, the potential demand on local parks likely is greater than in any other American city. New Yorkers must be especially innovative in order to make the most of their parks.