Merchant Web Services API Merchant Boarding XML Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

First Washington Associates Washington, D.C. December,,: 198

5 1- BANK JAMAICA/U.S. FULL SERVICE MERCHANT DEVELOPMENT CONCEPT-PAPER' Prepared by First Washington Associates Washington, D.C. December,,: 198 .2.1 TABLE!OF CONTENTS Page 1. Concept. * 1* II. Economic Climate and Private Investment . .4 III. Existing Financial Infrastructure ..... 7 IV. Activities of the New Bank . ... 13 V. Formation, Ownership, and Capitalization ,19 VI. Direction and Management,. .. " .22 VII. Implementation . ' .• ****25 0-H- I. CONCEPT 1. This discussion paper has been prepared at the,, request of the Bureau for Private Enterprise (PRE) and the Jamaican Mission of the U.S. Agency for International Development (AID) and is intended to describe the role which a new Jamaica/U.S. Full-Service Merchant Development Bank can play in helping achieve economic development and growth through expansion and stimulation of the private sector in Jamaica. 2. Under the Government of Prime Minister Seaga, Jamaica has embarked upon a serious, across-the-board program of measures to encourage expansion of private sector productivity and output and lead to substantial new investments in agri culture, manufacturing, and related service industries. The private sector is looked upon as the major driving force for economic rehabilitation, and investments from the United States and local entrepreneurs are being counted upon to bring new vitality and diversification to the Jamaican economy, reverse the outward flow of private capital, transfer new technologies, and help solve the country's balance of payments and unemployment problems. 3. Seriously limiting the achievement of these goals is the lack of an adequate institutional infrastructure to provide equity funding and aggressive medium- and long-term credit facilities to stimulate capital investment. -

BR-69915-210X297mm-Update the UBS Securities China Brochure

UBS Securities First foreign-invested fully-licensed securities firm in China, 51% owned by UBS AG He Di Eugene Qian UBS Securities Co., Limited (UBS Securities) was incorporated on 11 December 2006 following the restructuring of Beijing Securities Co., Limited. In December 2018, UBS AG increased its shareholding in UBS Securities to 51%; the first time that a foreign financial institution had raised its stake to take majority control of a securities joint venture in China. With the support of the UBS Group and the dedication of our employees, UBS Securities remains at the forefront of the industry as the first foreign-invested fully-licensed securities firm in China. Client-centric and committed to the pursuit of excellence and sustainable performance, UBS Securities relies on international experience complemented by local expertise to maintain its market- leading position. Our success would not have been possible without our employees. We would also like to thank our clients, shareholders, business partners, as well as government and regulatory bodies for their support which has been a driving force for the business. Our market position today is a strong foundation for the decades to come. We are determined to build on our core strengths to capture the opportunities arising from ongoing wealth creation, market reforms and globalization in China. We will continue to offer world-class products, services and advice to our clients, and work with all stakeholders towards the further development of China’s financial markets. Very best wishes. He Di Eugene Qian Chairman President UBS Securities UBS Securities 2 Milestones Moving forward December 2018 UBS AG increased its shareholding in UBS Securities to 51%, first international bank to increase stake to take majority control in a China securities joint venture. -

1999-2000 SAR Guide

A Guide to 1999-2000 SARs and ISIRs APPENDIX C NSLDS FINANCIAL AID HISTORY/NSLDS MATCH FLAGS NSLDS Financial Aid History The “Loan Satisfactory Repayment Arrange- 1999-2000 ments” flag reflects the status of loans with a “DX” (Defaulted, satisfactory arrangements Changes to NSLDS data since previous made including six consecutive monthly pay- Prescreening ments). If this flag is set to “Y” a comment will be included on the SAR/ISIR informing the student and the school of that status, but no “C” flag will An indicator will inform schools where NSLDS be set. information provided on a SAR/ISIR has changed since the last CPS transaction. A “#” sign will Aggregate Amounts for FFELP/Direct Loans print in front of the status field for Overpayments, Defaulted Loans, Discharged Loans, Loan Satis- Section factory Repayment Arrangements, or Active Bankruptcy if there has been a change in that The Unsubsidized Loans field has been deleted status since the last CPS transaction. and replaced with a Combined Loans field, which reflects the total amount of subsidized and The “#” sign will also print in front of the Aggre- unsubsidized loans the student has borrowed. gate Amount for FFELP/Direct Loans, Cumula- This change is consistent with guidance provided tive Perkins Loans, or the 1999-2000 Pell Pay- in Dear Colleague Letter, GEN-97-3, which was ment Data sections when information within that published in May 1997. In addition, the Consoli- section has changed since the last CPS transaction. dated Loans field has been renamed FFEL Con- Finally, a “#” sign will print in front of each solidated Loans, and will only include amounts of reported loan in the Loan Detail section when FFEL Consolidated Loans. -

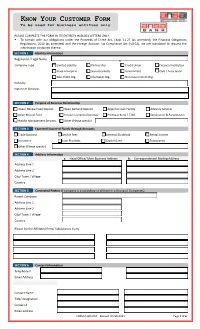

Know Your Customer Form

KNOW Y OUR C USTOMER F ORM To be used for business entities only PLEASE COMPLETE THE FORM IN ITS ENTIRETY IN BLOCK LETTERS ONLY . To comply with our obligations under the Proceeds of Crime Act, Chap. 11.27 (as amended), the Financial Obligations Regulations, 2010 (as amended) and the Foreign Account Tax Compliance Act (FATCA), we are mandated to request the information contained therein. SECTION 1 Identity Information Registered / Legal Name Company Type Limited Liability Partnership Credit Union Financial Institution State Enterprise Statutory Body Government Club / Association Non-Profit Org. Charitable Org. Non-Government Org. Industry Nature of Business SECTION 2 Purpose of Business Relationship Open/ Renew Fixed Deposit Open Demand Deposit Apply for Loan Facility Advisory Services Open Mutual Fund Foreign Currency Exchange Purchase Bond / T-Bill Syndication & Participation Wealth Management Services Other (Please specify) SECTION 3 Expected Source of Funds through Accounts Trade Business Service Fees Interest/ Dividends Rental Income Donations Loan Proceeds Capital Gains Subsidiaries Other (Please specify) SECTION 4 Address Information a. Head Office/ Main Business Address b. Correspondence/ Mailing Address Address Line 1 Address Line 2 City/ Town / Village Country SECTION 5 Connected Parties (if company is a subsidiary or affiliate in a Group of Companies) Parent Company Address Line 1 Address Line 2 City/ Town / Village Country Please list the Affiliated firms/ Subsidiaries if any SECTION 6 Contact -

The Only Guide to Surcharging You'll Need

The Only Guide You'll Need for Surcharging According to The Nilson Report, U.S. Merchants are paying nearly $90 billion annually in fees on card transactions that amount to about $6 trillion. As more transactions shift away from lower cost charge cards and checks, the fees paid by merchants will continue to increase. Consumers and businesses alike are hooked on credit cards with high-value rewards programs. Some 92% of all U.S. credit card purchase volume is charged on rewards cards according to estimates from the Mercator Advisory Group, Inc, a payments research and consulting firm. The most generous credit card reward programs carry the highest fees. Therefore the high fees paid by merchants on these transactions pay for the rich rewards offered by the issuing banks. In other words, your margins are paying for someone else's cashback and travel rewards. The Proof is in the Chart This chart by the Kansas City Federal Reserve Bank clearly shows that the interchange fees for rewards credit cards are significantly higher than traditional or non-rewards credit cards. Merchants Go to Court for Relief Tensions between the card networks and merchants are nothing new. Major retailers and other merchants fed up with the ever-increasing fees and restrictive rules filed a class- action lawsuit against VISA and Mastercard to win relief for their beleaguered margins. After years of fighting, a decision by the U.S. Supreme Court required the card associa- tions (VISA and Mastercard) to change their rules to allow merchants the option to add a fee or surcharge to each credit card transaction. -

Financial Crimes Enforcement Network

Federal Register / Vol. 69, No. 163 / Tuesday, August 24, 2004 / Proposed Rules 51979 (3) Covered financial institution has to document its compliance with the include the agency name and the the same meaning as provided in notice requirement set forth in Regulatory Information Number (RIN) § 103.175(f)(2) and also includes: paragraph (b)(2)(i)(A) of this section. for this proposed rulemaking. All (i) A futures commission merchant or (ii) Nothing in this section shall comments received will be posted an introducing broker registered, or require a covered financial institution to without change to http:// required to register, with the report any information not otherwise www.fincen.gov, including any personal Commodity Futures Trading required to be reported by law or information provided. Comments may Commission under the Commodity regulation. be inspected at FinCEN between 10 a.m. Exchange Act (7 U.S.C. 1 et seq.); and Dated: August 18, 2004. and 4 p.m., in the FinCEN reading room (ii) An investment company (as in Washington, DC. Persons wishing to William J. Fox, defined in section 3 of the Investment inspect the comments submitted must Company Act of 1940 (15 U.S.C. 80a–5)) Director, Financial Crimes Enforcement request an appointment by telephoning Network. that is an open-end company (as defined (202) 354–6400 (not a toll-free number). [FR Doc. 04–19266 Filed 8–23–04; 8:45 am] in section 5 of the Investment Company FOR FURTHER INFORMATION CONTACT: Act (15 U.S.C. 80a–5)) and that is BILLING CODE 4810–02–P Office of Regulatory Programs, FinCEN, registered, or required to register, with at (202) 354–6400 or Office of Chief the Securities and Exchange DEPARTMENT OF THE TREASURY Counsel, FinCEN, at (703) 905–3590 Commission under section 8 of the (not toll-free numbers). -

Small Business Banking Issues

Comptroller of the Currency Administrator of National Banks Small Business Banking Issues A National Forum Sponsored by the Office of the Comptroller of the Currency Renaissance Washington Hotel Washington, D.C. February 5, 1998 Acknowledgments The Office of the Comptroller would like to express its appreciation to the speakers at the Small Business Banking Issues Forum, whose presentations are summarized here. Appreciation is also extended to the forum attendees, listed in Appendix A of this publication, for their questions, comments, and experiences shared about small business banking. The project was developed to enable bankers and small busi- ness owners to learn about successful programs, techniques, and strategies relevant to small business banking that could be replicated in their own communities. OCC staff contributing to the planning and conduct of the forum included: Janice A. Booker, director, Community Devel- opment Division (CDD); Yvonne McIntire, senior attorney, Community and Consumer Law; Denise Kirk-Murray, commu- nity reinvestment and development specialist, Community and Consumer Policy Division; Alfred T. Mitchell, community development specialist, CDD; Glenda Cross, director, Minority and Urban Affairs; John Turner, national bank examiner, Credit Risk; and Jacquelyn C. Allen, community development specialist, CDD. Lillian M. Long, program coordinator, CD Investments Program, CDD, served as project leader. Adminis- trative assistance was provided by Tawanda Hudge and Lisa Hemphill, CDD. The Communications Division, particularly Amy A. Millen, senior editor, and Rick Progar, publications liaison officer, helped to bring this publication to fruition. The OCC welcomes your comments or questions about this publication. Please write to the Community Development Division, Office of the Comptroller of the Currency, 250 E Street, SW, Washington, DC 20219, or call (202) 874-4940. -

Merchant Services: Credit Card Policy and Security Standards

Merchant Services: Credit Card Policy and Security Standards Revised: June 2016 I. Policy University of Iowa departments that accept credit cards as a form of payment for goods and/or services must receive approval from Treasury Operations and the University Controller BEFORE purchasing, or contracting for purchase, any systems involved in processing credit card transactions. As a condition of approval, merchants must agree to comply with all requirements of the Payment Card Industry Data Security Standards (PCI-DSS), as well as the University specific controls outlined within this policy. A. Who Should Know This Policy Any individual with responsibilities for managing credit card transactions and those employees entrusted with handling or processing credit card information. This includes budget officers and systems managers. II. Purpose To establish guidelines and best practices for University entities engaging in the acceptance of credit cards. For the purpose of this policy, use of the term "credit cards" shall include the acceptance of cards bearing the logo of a credit card company, such as Visa, MasterCard, Discover, or American Express. Only those units which have received approval from Treasury Operations and the University Controller will be permitted to accept credit cards for payment of goods or services. The ability to accept credit cards comes with significant responsibilities to maintain cardholder security and to mitigate the risk of fraud. The University, and all of its merchants, have a fiduciary responsibility to protect customer credit card information, and thus must adhere to the strict security requirements established by the Payment Card Industry Security Standards Council or face significant financial penalties if a breach or fraud occurs. -

Merchant Bank Proposal

Merchant Bank A Proposal of the World Commission on Forced Displacement Letter from the Chairs December 2018 The circumstance of a large and growing number of forcibly displaced persons in the world – and its destabilizing impacts – should lead us to consider carefully what it would take for the lives affected to be rebuilt – that is for the displaced to be re-integrated in commu- nity living. Damage to societal cohesiveness, lost economic output and the fundamental unfairness of wasted lives should force us to do so. Humanitarian care and maintenance is an essential first and basic need. But that alone is insufficient as a remedy for a population that has become idled and dependent. Whatever else might improve the situation, gainful employment of the working age displaced population is an essential element. This realization has invigorated a paradigm for the leading edge of policy in response to displacement, that of ‘development’. That, in turn, requires investment. And, given the cumulative scale of the need and the very limited public resources available for develop- ment assistance, policy discussion turns to private sector participation. The location in the private sector of over 9 of 10 jobs in the world economy, of business operating capacities and savings – particularly surplus savings – underscores the case. The obvious gap in this picture is the lack of commercial conditions or of investment-ready proposals in most of the locations where jobs are required to address displacement. There is considerable evidence of willing private sector capital staying on the sidelines under current policies and practices, rather than engaging in developing locations. -

2016-17 Annual Report of the Michigan State Treasurer

ANNUAL REPORT Michiganof State the Treasurer 2016-2017 Rick Snyder, Governor | Nick A. Khouri, Treasurer Table of Contents State Treasurer’s Letter of Transmittal ........................................................................................................1 Cash and Investments Schedule 1 State Treasurer’s Common Cash - Assets and Equities ................................................ 2 Schedule 2 Investment Portfolios of Specific Funds ........................................................................3 Schedule 3 Investment Revenues .....................................................................................................4 Notes to Financial Schedules .................................................................................................................6 Cash and Investments ............................................................................................................................8 Table 1 Investment Revenues for Fiscal Years ...........................................................................8 Table 2 Available Month-End Common Cash ............................................................................9 Table 3 Common Cash History ...................................................................................................9 Table 4 State Treasurer’s Common Cash Fund, Cash Balances, and Transactions by Fund ..................................................................................................10 Table 5 Demand Depositories as of September 30, 2017 -

Credit Card 101

Credit Card 101 Jump Start Program First Data Learning Organization Confidential & Proprietary to First Data Corporation Developer: 10 Rev 03/03/2011 V2.0 Agenda – Card Brands – Card Types – The PiProcessing Flow – Selling Merchant Processing – Knowledge Check Confidential & Proprietary to First Data Corporation. 2 Credit Card’s 5 Major Brands • Visa Credit Cards ‐ credit cards issued by Financial Institutions that are members of Visa, cards carry the Visa Logo on the front of the card. • Master CdCard Cre dit CCdards ‐ cards idissued by Financ ia l IiiInstitutions that are members of MasterCard, cards carry the MasterCard logo on the front of the card. • American Express Credit Cards ‐ cards issued by American Express Financial Services, or their partner Financial Institutions, cards carry the American Express logo on the front of the card. • Discover Credit Cards ‐ cards issued by Discover Financial Services, or their partner Financial Institutions, cards carry the Discover or Novus logo on the front of the card. • JCB Credit Cards (Japanese Credit Bureau) ‐ cards issued by Financial Institutions (usually foreign Financial Institutions), cards carry the JCB logo on the front of the card. The common characteristic associated with each type of credit products: • Each credit instrument used to make the purchase/payment is associated with a line of credit that must be repaid to the issuing financial institution. Funds are not pulled out of a Bank or Government funded account. Confidential & Proprietary to First Data Corporation. 3 What Do They Mean By Card Typ e? Type of Card – Type refers to the card presentdted by the consumer at the time of purchase. -

This Document and the API That It Describes Are Deprecated

This document and the API that it describes are deprecated. Authorize.Net’s legacy name-value-pair API is still supported, however it will not be updated, except for critical security updates. To learn when this deprecated API will reach its end of life, and for information on upgrading to our latest API, read the Upgrade Guide. You can find the full Authorize.Net API documentation at our Developer Center. Title Page Advanced Integration Method (AIM) Card-Not-Present Transactions Developer Guide September 2017 Authorize.Net Developer Support http://developer.authorize.net Authorize.Net LLC 082007 Ver.2.0 Authorize.Net LLC (“Authorize.Net”) has made efforts to ensure the accuracy and completeness of the information in this document. However, Authorize.Net disclaims all representations, warranties and conditions, whether express or implied, arising by statute, operation of law, usage of trade, course of dealing or otherwise, with respect to the information contained herein. Authorize.Net assumes no liability to any party for any loss or damage, whether direct, indirect, incidental, consequential, special or exemplary, with respect to (a) the information; and/or (b) the evaluation, application or use of any product or service described herein. Authorize.Net disclaims any and all representation that its products or services infringe upon any existing or future intellectual property rights. Authorize.Net owns and retains all right, title and interest in and to the Authorize.Net intellectual property, including without limitation, its patents, marks, copyrights and technology associated with the Authorize.Net services. No title or ownership of any of the foregoing is granted or otherwise transferred hereunder.