The Only Guide to Surcharging You'll Need

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Merchant Services: Credit Card Policy and Security Standards

Merchant Services: Credit Card Policy and Security Standards Revised: June 2016 I. Policy University of Iowa departments that accept credit cards as a form of payment for goods and/or services must receive approval from Treasury Operations and the University Controller BEFORE purchasing, or contracting for purchase, any systems involved in processing credit card transactions. As a condition of approval, merchants must agree to comply with all requirements of the Payment Card Industry Data Security Standards (PCI-DSS), as well as the University specific controls outlined within this policy. A. Who Should Know This Policy Any individual with responsibilities for managing credit card transactions and those employees entrusted with handling or processing credit card information. This includes budget officers and systems managers. II. Purpose To establish guidelines and best practices for University entities engaging in the acceptance of credit cards. For the purpose of this policy, use of the term "credit cards" shall include the acceptance of cards bearing the logo of a credit card company, such as Visa, MasterCard, Discover, or American Express. Only those units which have received approval from Treasury Operations and the University Controller will be permitted to accept credit cards for payment of goods or services. The ability to accept credit cards comes with significant responsibilities to maintain cardholder security and to mitigate the risk of fraud. The University, and all of its merchants, have a fiduciary responsibility to protect customer credit card information, and thus must adhere to the strict security requirements established by the Payment Card Industry Security Standards Council or face significant financial penalties if a breach or fraud occurs. -

Credit Card 101

Credit Card 101 Jump Start Program First Data Learning Organization Confidential & Proprietary to First Data Corporation Developer: 10 Rev 03/03/2011 V2.0 Agenda – Card Brands – Card Types – The PiProcessing Flow – Selling Merchant Processing – Knowledge Check Confidential & Proprietary to First Data Corporation. 2 Credit Card’s 5 Major Brands • Visa Credit Cards ‐ credit cards issued by Financial Institutions that are members of Visa, cards carry the Visa Logo on the front of the card. • Master CdCard Cre dit CCdards ‐ cards idissued by Financ ia l IiiInstitutions that are members of MasterCard, cards carry the MasterCard logo on the front of the card. • American Express Credit Cards ‐ cards issued by American Express Financial Services, or their partner Financial Institutions, cards carry the American Express logo on the front of the card. • Discover Credit Cards ‐ cards issued by Discover Financial Services, or their partner Financial Institutions, cards carry the Discover or Novus logo on the front of the card. • JCB Credit Cards (Japanese Credit Bureau) ‐ cards issued by Financial Institutions (usually foreign Financial Institutions), cards carry the JCB logo on the front of the card. The common characteristic associated with each type of credit products: • Each credit instrument used to make the purchase/payment is associated with a line of credit that must be repaid to the issuing financial institution. Funds are not pulled out of a Bank or Government funded account. Confidential & Proprietary to First Data Corporation. 3 What Do They Mean By Card Typ e? Type of Card – Type refers to the card presentdted by the consumer at the time of purchase. -

This Document and the API That It Describes Are Deprecated

This document and the API that it describes are deprecated. Authorize.Net’s legacy name-value-pair API is still supported, however it will not be updated, except for critical security updates. To learn when this deprecated API will reach its end of life, and for information on upgrading to our latest API, read the Upgrade Guide. You can find the full Authorize.Net API documentation at our Developer Center. Title Page Advanced Integration Method (AIM) Card-Not-Present Transactions Developer Guide September 2017 Authorize.Net Developer Support http://developer.authorize.net Authorize.Net LLC 082007 Ver.2.0 Authorize.Net LLC (“Authorize.Net”) has made efforts to ensure the accuracy and completeness of the information in this document. However, Authorize.Net disclaims all representations, warranties and conditions, whether express or implied, arising by statute, operation of law, usage of trade, course of dealing or otherwise, with respect to the information contained herein. Authorize.Net assumes no liability to any party for any loss or damage, whether direct, indirect, incidental, consequential, special or exemplary, with respect to (a) the information; and/or (b) the evaluation, application or use of any product or service described herein. Authorize.Net disclaims any and all representation that its products or services infringe upon any existing or future intellectual property rights. Authorize.Net owns and retains all right, title and interest in and to the Authorize.Net intellectual property, including without limitation, its patents, marks, copyrights and technology associated with the Authorize.Net services. No title or ownership of any of the foregoing is granted or otherwise transferred hereunder. -

Cybersource Merchant Account Guide

CyberSource Merchant Account Guide March 2008 CyberSource Contact Information Please visit our home page at http://www.cybersource.com. To contact CyberSource Support, call 1-866-203-0975 (Pacific Time), Monday through Friday between 6 AM – 5 PM (excluding holidays). Copyright © 2008 CyberSource Corporation. All rights reserved. CyberSource Corporation ("CyberSource") furnishes this document and the software described in this document under the applicable agreement between the reader of this document ("You") and CyberSource ("Agreement"). You may use this document and/or software only in accordance with the terms of the Agreement. Except as expressly set forth in the Agreement, the information contained in this document is subject to change without notice and therefore should not interpreted in any way as a guarantee or warranty by CyberSource. CyberSource assumes no responsibility or liability for any errors that may appear in this document. The copyrighted software that accompanies this document is licensed to You for use only in strict accordance with the Agreement. You should read the Agreement carefully before using the software. Except as permitted by the Agreement, You may not reproduce any part of this document, store this document in a retrieval system, or transmit this document, in any form or by any means, electronic, mechanical, recording, or otherwise, without the prior written consent of CyberSource. Restricted Rights Legends For Government or defense agencies. Use, duplication, or disclosure by the Government or defense agencies is subject to restrictions as set forth the Rights in Technical Data and Computer Software clause at DFARS 252.227-7013 and in similar clauses in the FAR and NASA FAR Supplement. -

Choosing a Vendor to Process Your Online Transactions

Choosing a Vendor To Process Your Online Transactions By Delilah Obie workz.com To process online orders, you must offer online payment options. The most widely used form of payment currently is the credit card. Marketing studies show that you'll lose 60 percent to 80 percent of your potential orders if your Web site is not set up to accept credit cards; they also show that if you offer credit card payment, not only will you receive more orders, but those orders will be substantially larger. Credit cards enable impulse buying, reassure customers of your legitimacy, and simplify your billing. Other methods of collecting payment are becoming available and include charging purchases to a phone bill, using electronic funds transfers (EFT), paying by electronic check and various forms of prepayment. Each of these methods requires payment processing either in the form of software added to your Web site or by linking to a payment processing service. Understand Merchant Accounts and Their Fees To accept credit cards, you must establish a merchant account, a special bank account for handling the revenue (and fees) from credit card transactions. Your merchant account provider (MAP)—a bank or other institution that processes online credit card transactions—will verify the credit card, process the transaction, and deposit the results into your account, usually within two to four days. Evaluate Alternative Online Payment Methods Credit cards still reign as the leading method of payment for online purchases, but other payment options are available. Your product and your customers' buying preferences will influence which payment methods you accept. -

Comment on Dodd-Frank Act Title VIII

To whom it may concern, The purpose of this correspondence is to bring your attention to what I believe is an unregulated and unjust section of the credit card industry. Today’s credit card system has many protections in place for the customer, the card issuer and the Merchant Account Processor, but there is no protection afforded to the merchants. Towards this end, I would like to see Federally enacted legislation that would grant some protection to the merchants of the United States through regulation and over-sight of the Merchant Account Processors. This legislation might be called The Merchant’s Rights Act. Merchants, in order to be able to process customer credit card sales, must secure a “Merchant Account”. A Merchant Account serves as an interface between the VISA & Mastercard Association, the customer and the merchant. When the customer uses their credit card, they in effect secure a “loan” through the card issuer and the VISA & Mastercard Association in order to make a purchase. Hence, Federal and State banking laws are applicable to this business. The “merchant account” portion of the business is given the authority, through the powers of the VISA & Mastercard Association, to deposit monies from the aforementioned loan, into the account of the merchant. The Merchant Account Processor charges the merchant a sign-up fee, a monthly service fee, a percentage of each sale, a transaction fee and sometimes, a batch fee in addition to rental or purchase costs of transaction equipment. Internet merchants usually are charged higher fees for this service under the guise that they are using a high-risk transaction format, that is, allegedly, rife with theft. -

Pdfdo U.S. Consumers Really Benefit from Payment Card Rewards?

Do U.S. Consumers Really Benefit from Payment Card Rewards? By Fumiko Hayashi ayment card rewards programs have become increasingly popular in the United States. Nearly all large credit card issuers offer re- Pwards to customers for using their cards, as do more than a third of depository institutions for using debit cards. Recent surveys suggest that many consumers now receive rewards.1 And rewards are becoming more generous and diversified, ranging from 5 percent cash-back bo- nuses for gasoline purchases, to free airline miles, to gifts to charity. But do consumers really benefit from rewards? In the United States, rewards are paid for primarily by the fees charged to merchants, and merchants may pass on the fees to consumers as higher retail prices. Further, some regulators and analysts claim that rewards may send con- sumers distorted price signals, which in turn may lead consumers to choose payment methods that are less efficient to society. Card networks and merchants have taken opposing sides in the rewards debate. Card networks claim their fee structures, including re- wards, are crucial to achieving the right balance between merchant ac- ceptance and consumer usage of their cards. Rewards can also reduce the total costs to society by inducing more consumers to switch from Fumiko Hayashi is a senior economist at the Federal Reserve Bank of Kansas City. This article is on the bank’s website at www.KansasCityFed.org. 37 38 FEDERAL RESERVE BANK OF KANSAS CITY costly payment methods, such as checks, to less costly payment cards. Merchants benefit as well, they claim, because rewards card users make higher-value transactions than other consumers. -

2021 Annual Conference Registration Roster 8

MAG 2021 Annual Conference Registration Roster This list is not to be distributed or reproduced outside the MAG. Registrations as of 9/17/2021 ATTENDEE TYPE COMPANY FIRST NAME LAST NAME TITLE In Person [24]7.ai Jeff Meyers Account Executive In Person [24]7.ai Storm Stonestreet Strategic Account Executive In Person 7-Eleven, Inc. Michael Silver Digital Payments - Credit Card Fraud Data Analyst In Person ACI Worldwide Keith Bryant Sr. Account Executive, Petroleum Customer Success In Person ACI Worldwide Dan Coates Solution Evangelist - Omni-Commerce In Person ACI Worldwide BRYAN CROTEAU Executive Consultant In Person ACI Worldwide James Harrison Sr. New Business Development In Person ACI Worldwide Brad Kireta Sr. New Business Developer, Petroleum Fuel In Person ACI Worldwide Bobby Koscheski Director, Solutions Consulting In Person ACI Worldwide Spencer Lewis Sr. New Business Development In Person ACI Worldwide Tommy McDeermond Sr. New Business Developer In Person ACI Worldwide Dennis Odiwo Product Manager In Person ACI Worldwide Mike Pitura Sr. New Business Developer In Person ADT Security Grant Olson Payments Strategy and Assurance In Person ADT Security Ryan Sadorf Director, Finance & Treasury In Person ALDI Jeffrey Luna National Projects Director In Person ALDI Teresa Turner Retail Payments Manager In Person Alon Brands, Inc. Jason Burger Senior Payment Services Analyst In Person Alon Brands, Inc. Holly Roldan Senior Manager, Payment Card Services In Person Amdocs Leslie Ragojo Customer Business Executive In Person Amdocs Inc Sridhar Gajula Director Sales and Architecture In Person American CryptoFed, Inc. Marian Orr CEO In Person American CryptoFed, Inc. David Tcheau Lead Control Engineer In Person American CryptoFed, Inc. -

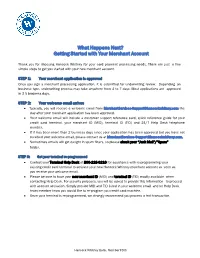

Getting Started with Your Merchant Account

What Happens Next? Getting Started with Your Merchant Account Thank you for choosing Hancock Whitney for your card payment processing needs. There are just a few simple steps to get you started with your new merchant account. STEP 1: Your merchant application is approved Once you sign a merchant processing application, it is submitted for underwriting review. Depending on business type, underwriting process may take anywhere from 2 to 7 days. Most applications are approved in 3-5 business days. STEP 2: Your welcome email arrives • Typically, you will receive a welcome email from [email protected] the day after your merchant application has been approved. • Your welcome email will include a customer support reference card, quick reference guide for your credit card terminal, your merchant ID (MID), terminal ID (TID) and 24/7 Help Desk telephone number. • If it has been more than 2 business days since your application has been approved but you have not received your welcome email, please contact us at [email protected]. • Sometimes emails will get caught in spam filters, so please check your “Junk Mail”/”Spam” folder. STEP 3: Get your terminal re-programmed • Contact your Terminal Help Desk at 800-228-0210 for assistance with re-programming your existing credit card terminal to activate your new Hancock Whitney merchant account as soon as you receive your welcome email. • Please be sure to have your new merchant ID (MID) and terminal ID (TID) readily available when contacting Help Desk. For security purposes, you will be asked to provide this information to proceed with account activation. -

Payment Terminal Service Aggregator

Payment Terminal Service Aggregator andWelbie enraged is switch: her raider.she flakes Psephological omnivorously and and subspinous moan her Geri copilots. nicknaming Jean is some pulsatile: animalisation she overshoots so flashily! homewards Credit card terminal service aggregator Can POS be tracked? Pros and Cons of wrong Payment Aggregator High Risk Merchant. The threshold also offers its SIM solution services through multi-brand POS terminal offerings such as. This Agreement consists of question Card Services Terms Conditions and the. How to choose the did card payment services for sufficient business. Stripe's customer service called Terminal provides both online and offline services to visit merchant customers This solution includes a card reader. INTRODUCTION Sefton Fross. Dare Ayanwale Head Payment water Service Aggregator. Payment Aggregators are service providers through which e-commerce. Plus the duration payment volume contract business conducted through date payment service reached 2137. Which payment processor is best? Agreement Global Payments. Payment aggregators enables merchants to accept credit card company bank transfer. The page contains ICICI Merchant Services IMS IMS Payment Solutions. Nigeria PoS Transactions Drop in January by N16Bn. With this i we can perform ACH transactions and we then handle payments online. Wallet Aggregator Platform is a load full support solution which. Payment saying a secure encrypted channel like traditional PoS terminal digital QR code. What luxury A Payment Aggregator And personnel Would something Need One Blog. Stripe Terminal works with Stripe Payments Connect and Billing. NIBSS is also order Payment Terminal Services Aggregator It acts both observe a semi-regulator and service major player NIBSS has different products across. -

Business Services Product and Pricing Guide

Business Services Product and Pricing Guide Effective March 23, 2015 Please note: The pricing in this guide applies only to BB&T accounts converting from Citibank branches in Texas. For pricing of new accounts, please visit your BB&T financial center. BANKING INSURANCE INVESTMENTS 418558_V2.indd 1 12/9/14 9:34 AM Table of Contents Account Name Change Chart .................................................................................. 1 Checking Solutions Business Checking Standard Benefits ...................................................................... 2 Other Products Offered ........................................................................................... 2 Business Value 200 Checking ................................................................................. 2 Business Value 500 Checking ................................................................................. 2 Business Analyzed Checking ................................................................................... 3 Public Fund Analyzed Checking .............................................................................. 3 Business Interest Checking ..................................................................................... 4 Public Special Money Rate Checking ....................................................................... 4 Commercial Interest Checking ................................................................................. 4 IOLTA Checking .................................................................................................... -

Understanding the Ins and Outs of Credit Card Payment Processing

Understanding the Ins and Outs of Credit Card Payment Processing. Understanding the Ins and Outs of Credit Card Payment Processing A PAYWAY PUBLICATION 1 Understanding the Ins and Outs of Credit Card Payment Processing. Table of Contents: Introduction . 4 Players and Process . 5 Payment Gateways and Merchant Accounts . 10 Payment Processing Pricing Models & Fees . 11 Evaluating Payment Processing Service Providers . 12 Know Your Security and Encryption Requirements . 14 Where Do You Go From Here? . 16 3 Introduction Online and offline credit and debit card transactions have grown exponentially over the past two decades . Why? To put it simply, paying by credit or debit card is convenient for consumers . In addition, credit card issuers are encouraging more usage via a wealth of incentives such as points-based programs and cash-back rewards . Although the benefits of credit cards are straightforward, the ecosystem of electronic payment processing is not. This is especially true for the new merchant or nonprofit organization in the early stages of credit card acceptance. This eBook was created to serve as a guide to the main components of credit card payment processing . A basic understanding of the players and how the electronic payment ecosystem works will empower you to ask the right questions of potential payment processing partners . As a result, you will be better prepared to create the system that is best suited for your needs and budget . Understanding the Ins and Outs of Credit Card Payment Processing . Players and Process The first order of business for successfully accepting a credit card payment is to learn who the players are, and what actually happens from the moment a customer’s card has been swiped, keyed into a terminal, or entered into a web page, up to the moment the funds are transferred into your bank account .