Competition in the Local Bus Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simply the Best Buses in Britain

Issue 100 | November 2013 Y A R N A N I S V R E E R V S I A N R N Y A onThe newsletter stage of Stagecoach Group CELEBRATING THE 100th EDITION OF STAGECOACH GROUP’S STAFF MAGAZINE Continental Simply the best coaches go further MEGABUS.COM has buses in Britain expanded its network of budget services to Stagecoach earns host of awards at UK Bus event include new European destinations, running STAGECOACH officially runs the best services in Germany buses in Britain. for the first time thanks Stagecoach Manchester won the City Operator of to a new link between the Year Award at the recent 2013 UK Bus Awards, London and Cologne. and was recalled to the winner’s podium when it was In addition, megabus.com named UK Bus Operator of the Year. now also serves Lille, Ghent, Speaking after the ceremony, which brought a Rotterdam and Antwerp for number of awards for Stagecoach teams and individuals, the first time, providing even Stagecoach UK Bus Managing Director Robert more choice for customers Montgomery said: “Once again our companies and travelling to Europe. employees have done us proud. megabus.com has also “We are delighted that their efforts in delivering recently introduced a fleet top-class, good-value bus services have been recognised of 10 left-hand-drive 72-seat with these awards.” The Stagecoach Manchester team receiving the City Van Hool coaches to operate Manchester driver John Ward received the Road Operator award. Pictured, from left, are: Operations Director on its network in Europe. -

Travel Information

TRAVEL INFORMATION FROM EDINBURGH Follow signs for the A90/M90 Forth Road Bridge. Follow M90 to Perth, and then take A85 Dundee/Aberdeen. Cross the Friarton Bridge over the River Tay. Take exit immediately signposted after the bridge, A94 Coupar Angus road. Follow the A94 to a set of Traffic Lights, go straight ahead. Straight through the next set of lights. At the 3rd set of lights the A94 bends to the right (still signposted Coupar Angus). Follow this road for approx. 1 ½ miles. You will see a sign for Murrayshall (a right turn). If you arrive in New Scone you have come too far and should turn back. Follow the turnoff for 1 ¾ miles. Do not take the first road on the right signposted Murrayshall as it takes you to the driving range. Continue straight ahead. The next right entrance is the Hotel main drive. Total Journey Time: typically, 1 h 5 min - 1 h 40 min (46.6 miles). From Waverley Station, take the ScotRail train to Perth (7 stops). Walk approx. 8 minutes to South Street (Stop M) to get the Stagecoach Gold 7 Scone bus. To get to South Street, turn left onto Leonard St/A989. Continue to follow Leonard St. Continue onto Hospital St. Turn left onto King St. Turn right onto South St. Once on the Stagecoach Gold 7 Scone bus, get off at Mansfield Road (11 stops). Walk north-east on Perth Rd/A94 towards Mansfield Road. Turn right onto Murrayshall Road. Turn left onto Bonhard Road. Continue onto Murrayshall Road. Turn right and the hotel will be on the right (approx. -

News Briefing ΠAugust 2010

North Pembrokeshire Transport Forum Fforwm Trafnidiaeth Gogledd Penfro News Briefing – September 2010 Buses TrawsCambria Network Consultation. The TrawsCambria bus network provides an essential public transport link between key centres. The network is designed to connect into the rail network at key stations such as Carmarthen, Aberystwyth, Wrexham and Bangor. This consultation, which closes on 12th December, is seeking views about TrawsCambria’s plans to improve the network. Potential improvements include: · Reduced journey times between key centres by public transport · Better connections between TrawsCambria services and the rail network in Wales · Potential new services to provide a wider range of choice when travelling between key centres across Wales · The introduction of new more comfortable coach style vehicles which are better suited to longer distance services · Improved “on board” facilities for passengers · Improved ticketing and fare options Further information about the consultation, including the consultation questionnaire, can be found on: http://wales.gov.uk/consultations/transport/trawscambria/?lang=en. Bouquet for Pembrokeshire Bus Drivers: A regular bus passenger has reported to the Forum’s Executive Committee: “Travelling on an extremely wet Wednesday I was impressed with how helpful the bus drivers were, taking passenger as close to their destinations as possible. It’s what rural bus services are all about, with real people drivers. First, Silcox and Richard Brothers are to be commended”. Community Transport Preseli Green Dragon. Organisers report that their summer services have been well received this year. The new Gwaun Valley service, from Fishguard to Bwlchgwynt, is very popular. They have resumed running the Sunday evening service to Theatre Mwldan in Cardigan. -

Firstgroup Plc Annual Report and Accounts 2015 Contents

FirstGroup plc Annual Report and Accounts 2015 Contents Strategic report Summary of the year and financial highlights 02 Chairman’s statement 04 Group overview 06 Chief Executive’s strategic review 08 The world we live in 10 Business model 12 Strategic objectives 14 Key performance indicators 16 Business review 20 Corporate responsibility 40 Principal risks and uncertainties 44 Operating and financial review 50 Governance Board of Directors 56 Corporate governance report 58 Directors’ remuneration report 76 Other statutory information 101 Financial statements Consolidated income statement 106 Consolidated statement of comprehensive income 107 Consolidated balance sheet 108 Consolidated statement of changes in equity 109 Consolidated cash flow statement 110 Notes to the consolidated financial statements 111 Independent auditor’s report 160 Group financial summary 164 Company balance sheet 165 Notes to the Company financial statements 166 Shareholder information 174 Financial calendar 175 Glossary 176 FirstGroup plc is the leading transport operator in the UK and North America. With approximately £6 billion in revenues and around 110,000 employees, we transported around 2.4 billion passengers last year. In this Annual Report for the year to 31 March 2015 we review our performance and plans in line with our strategic objectives, focusing on the progress we have made with our multi-year transformation programme, which will deliver sustainable improvements in shareholder value. FirstGroup Annual Report and Accounts 2015 01 Summary of the year and -

Edwards.Qxp Feature 2 12/03/2015 14:15 Page 58 BUS & COACH90 REVIEW: EDWARDS COACHES Years of Success

Edwards.qxp_feature 2 12/03/2015 14:15 Page 58 BUS & COACH90 REVIEW: EDWARDS COACHES Years Of Success Passion & innovation has helped family business Edwards Coaches stay one step ahead of the competition 58 TRANSPORT & LOGISTICS MAGAZINE www.tandlonline.com Edwards.qxp_feature 2 12/03/2015 14:15 Page 59 BUS & COACH REVIEW: EDWARDS COACHES n the last year it is esti- and rubber wheels – with the sim- children every day on an am and mated that there were ple objective of providing a service pm school run and a lot of the over 5.2 billion bus and that would put a smile on people's schools have confidence in us.” coach passenger journeys faces, and since then their goal has It's good to know that the com- Iin Great Britain, making up remained the same. pany still treasure the same family around two thirds of all public “We're primarily a coach com- values after all these years – even transport journeys, meaning pany, but we've diversified in a though the business, and the coach that buses and coaches are no number of different transport func- industry itself, has changed dramati- small part of the UK economy. tions over the years,” said Jason cally. “It's not just a simple job any Operating out of South Wales, Edwards, Company Director. As more, to get out of bed and run a Edwards Coaches are among the well as a regional bus service pro- coach company,” admits Jason. In oldest coach companies in Great viding key transport routes for the recent years, government legislation Britain, having been founded in local community, the company also has meant that coach companies 1925. -

46436-36 Pontypridd Sustainable Transport Guide.Qxp Layout 1 29/11/2018 10:51 Page 1

46436-36 Pontypridd Sustainable Transport Guide.qxp_Layout 1 29/11/2018 10:51 Page 1 JANUARY 2019 JANUARY GUIDE TRAVEL SUSTAINABLE PONTYPRIDD 2019 IONAWR PONTYPRIDD CYNALIADWY TEITHIAU CANLLAW www.sustrans.org.uk/walesroutes www.sustrans.org.uk/walesroutes To discover these walking and cycling routes go to to go routes cycling and walking these discover To I ddysgu mwy am y llwybrau cerdded a beicio yma ewch i i ewch yma beicio a cerdded llwybrau y am mwy ddysgu I parking of bikes. of parking gyfleusterau cyfleus er mwyn storio beiciau yng nghanol y dref. y nghanol yng beiciau storio mwyn er cyfleus gyfleusterau residential areas and the town centre has conveniently located storage facilities for the safe the for facilities storage located conveniently has centre town the and areas residential neu heb draffig o gwbl, sy'n cysylltu'r dref â'r ardaloedd preswyl agos. Mae yna nifer o nifer yna Mae agos. preswyl ardaloedd â'r dref cysylltu'r sy'n gwbl, o draffig heb neu number of mainly traffic free and low traffic routes which connect the town centre with nearby with centre town the connect which routes traffic low and free traffic mainly of number Mae'n lle gwych i grwydro ar droed neu ar feic. Mae yna nifer o lwybrau heb lawer o draffig, o lawer heb lwybrau o nifer yna Mae feic. ar neu droed ar grwydro i gwych lle Mae'n walking and cycling and is a great place to get around on by foot or by bike. There are a are There bike. -

Written Questions Answered Between 8 and 15 March 2007

Written Questions answered between 8 and 15 March 2007 [R] signifies that the Member has declared an interest. [W] signifies that the question was tabled in Welsh. Contents Questions to the First Minister Questions to the Minister for Culture, Welsh Language and Sport Questions to the Minister for Enterprise, Innovation and Networks Questions to the Minister for Education, Lifelong Learning Skills Questions to the Finance Minister Questions to the Minister for Health and Social Services Questions to the Minister for Social Justice and Regeneration Questions to the First Minister Jonathan Morgan: Will the First Minister make a statement on the number and cost of civil servants employed by the Welsh Assembly Government? (WAQ47069) Substantive answer following holding reply. The First Minister (Rhodri Morgan): The Permanent Secretary has supplied the following answer: As Assembly Government staffing is my responsibility the First Minister has asked me to write to you on these matters. I wrote to you separately in December 2005 and January 2006 in response to a number of written Assembly questions (WAQ44881, WAQ44882, WAQ44869 and WAQ44883) tabled for the First Minister about the numbers of Assembly staff, the costs of administration and the salary bill of civil servants. In my responses (attached for your information) I provided you with details of staff numbers and costs from the inception of the Assembly as requested. The increases in staff numbers and associated costs have occurred as the Government has taken on responsibility for a broad range of functions either new or previously external to the Assembly. These include the transfer of: 2000-01 197 staff from WHCSA, Health Promotion Wales, WORD, WEPE and Wales Trade International. -

HANDBOOK NVL 2014-15 Season 2 Contents

HANDBOOK NVL 2014-15 season 2 Contents Introduction Competitions Commission Volley 123 Funding Team Details Men’s Super 8s Women’s Super 8s Men’s Division 1 Women’s Division 1 Men’s Division 2 North Men’s Division 2 South Women’s Division 2 North Women’s Division 2 South Men’s Division 3 Central Men’s Division 3 North Men’s Division 3 South East Men’s Division 3 South West Women’s Division 3 Central Women’s Division 3 North Women’s Division 3 South Men's Non-NVL Cup Teams Women's Non-NVL Cup Teams Venues Match Venues Fixtures Fixtures and Referee Appointment Information National Competition Dates Rules National Competition Rules Contacts Administrative Officers of the Association 3 NVL 2014-15 season 1 NVL 2014 – 15 season NVL 2014-15 season 4 Introduction Welcome to another National Volleyball League and Cup season and a special welcome to those 19 new teams that are joining the NVL this season. No matter what ever your results are I hope that you all enjoy this season’s volleyball. Last season saw the European Volleyball Federation (CEV) impose on us that all NVL Clubs follow the correct procedures for International Transfer of players. This effectively means that annually any player competing in the NVL whose Federation of Origin is not England would need to follow this procedure and pay the appropriate fee. We were successful in negotiating a phased implementation of this with it only applying to Super 8 teams last season. However this season Division 1 Clubs must also now follow this new procedure. -

For Details of Saturday and Sunday Buses, Please See Next Page

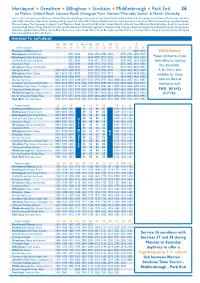

Middlesbrough l Stockton l Billingham l Greatham l Hartlepool 36 Middlesbrough l Stockton l North Tees Hospital 37 Middlesbrough l Stockton l Norton Glebe 38 Services 36, 37, 38 via Middlesbrough Bus Station, Newport Road, Stockton Road, Middlesbrough Road, Mandale Road, Victoria Bridge, Bridge Road, Stockton High Street, Norton Road; then Service 36 via Norton Road, Billingham Road, Billingham Bank, South View, West Road, Billingham Green, Station Road, Wolviston Road, Roseberry Road, The Causeway, Melrose Avenue, Rievaulx Avenue, Marsh House Avenue, Seal Sands Link Road, Stockton Road, Newton Bewley, Stockton Road A689, Greatham Bridge, Greatham High Street, Stockton Road A689, Owton Manor Lane, Catcote Road, Oxford Road, Stockton Road, York Road, Park Road, Stockton Street, Victoria Road; Service 37 from Norton Road via Harland Place, Norton High Street, Norton Green, Junction Road, Ragpath Lane, Redhill Road, Hardwick Road, North Tees Hospital; Monday to Saturday daytime Service 38 from Norton Road via Norton Avenue, Darlington Lane, Leven Road, evening and Sunday Service 38 from Norton Avenue via Harland Place Norton High Street, Norton Green, Junction Road, The Glebe, Weaverham Road, Ashton Road. MONDAY TO FRIDAY Q B Service number 37 36 37 36 37 36 37 36 37 36 38 36 37 36 38 36 37 36 38 36 37 36 38 Middlesbrough Bus Station 0532 - 0602 - 0622 0637 0642 0647 0656 0701 0711 0721 0731 0741 0751 0801 - 0811 0821 0830 0838 0845 0853 Thornaby Railway Station 0539 - 0609 - 0631 0646 0651 0657 0706 0711 0721 0731 0741 0751 0801 0811 - -

Hartlepool Greatham Billingham Stockton Middlesbrough Park End 36

Hartlepool z Greatham z Billingham z Stockton z Middlesbrough z Park End 36 via Marina, Oxford Road, Catcote Road, Owington Farm, Norton,Thornaby Station & North Ormesby Service 36 from Hartlepool Marina via Marina Way, Gateway Bridge,Victoria Road,York Road, Stockton Road, Oxford Road, Catcote Road, Owton Manor Lane, Stockton Road A689, Greatham High Street, Greatham Bridge, Stockton Road A689, Newton Bewley, Stockton Road, Seal Sands Link Road, Marsh House Avenue, Rievaulx Avenue, Melrose Avenue,The Causeway, Roseberry Road,Wolviston Road, Station Road, Billingham Green,West Road, South View, Billingham Bank, Billingham Road, Norton Road, Stockton High Street, Bridge Road,Victoria Bridge, Mandale Road, Middlesbrough Road, Stockton Road, Newport Road, Hartington Road, Brentnall Street, Grange Road, Middlesbrough Bus Station,Wilson Street,Albert Road, Corporation Road, Marton Road, Borough Road,West Terrace, Cromwell Street, King's Road, Ormesby Road, Ingram Road, Crossfell Road, Overdale Road.. MONDAY TO SATURDAY NS NS NS S NS + NS NS S NS S + E Service number 36A 36 36 36 36 36 36 36 36 36 36 36 36 36 Hartlepool Marina, Asda ------------0801 0816 DDA Aware Hartlepool, Victoria Road - - 0623 0628 - 0646 0703 0708 0720 - 0738 0753 0803 0819 Hartlepool, York Road Library - - 0625 0630 - 0648 0705 0710 0722 - 0740 0755 0806 0822 Please contact us if you Oxford Road, Catcote Road - - 0631 0636 - 0654 0711 0716 0728 - 0746 0801 0812 0828 have difficulty reading Rossmere Hotel - - 0635 0640 - 0658 0715 0720 0732 - 0750 0805 0816 0832 this -

Annual Report

Our services (continued) We have dedicated staff based in the Urban Traffic Control The eveningrider Plus ticket also saw a similar extension, with Over the past year we have continued to support local charities offices in Sheffield Town Hall who work closely with our local passengers in Sheffield, Chesterfield and Rotherham having access and have undertaken events at various local schools to help Sheffield and Chesterfield authority partners to ensure that buses can run to time and that to this ticket for the first time. Our staff have been really keen to promote independent bus travel to young people in our area. any services that experience delays or disruption are dealt with promote this ticket on the front line, knowing it offers such great All depots and the Head Office team held Macmillan Coffee May 2018 saw the introduction of the Matlock Town services as effectively as possible to minimise any disruption to service. value for our customers. mornings raising £1,500. As part of our promotion of the bus M1 and M4 to our network. Run from our Chesterfield depot, journey as a way of assisting the social inclusion agenda, Hattie the team of dedicated, regular drivers have proven popular In 2018, the Buses for Sheffield brand became more We introduced a Less Cash trial on Chesterfield service 54 in the Chatty bus visited Barnsley and Sheffield where staff talked with customers. prominent across the city, with the introduction of February 2019, aimed at reducing cash transactions on bus and to a range of people who dropped in for a coffee and a chat. -

National Transport Plan March 2010 G/MH/3531/02-10 February Typeset in 12Pt ISBN 978 0 7504 5494 0 CMK-22-03-220 © Crown Copyright 2010 Contents

www.wales.gov.uk National Transport Plan March 2010 G/MH/3531/02-10 February Typeset in 12pt ISBN 978 0 7504 5494 0 CMK-22-03-220 © Crown copyright 2010 Contents Contents Foreword 2 Summary 3 Chapter 1 – Introduction 9 1.1 The role of the National Transport Plan 9 1.2 Reducing carbon equivalent emissions from transport 9 1.3 Delivering the National Transport Plan: All-Wales and strategic corridors 10 1.4 Developing solutions to transport issues 11 1.5 Funding the National Transport Plan 11 1.6 Monitoring 11 Chapter 2 – Transport across Wales 13 2.1 Sustainable travel centres 13 2.2 Integrating the impact of travel into wider decision making 13 2.3 Increasing healthy and sustainable travel choices, including walking and cycling 14 2.4 Improving local bus services 15 2.5 Improving rail services 16 2.6 Improving access to key sites and services 17 2.7 Managing our road infrastructure 18 2.8 Improving the safety of the road network 18 2.9 Improving the sustainability of freight transport 19 2.10 Improving the sustainability of transport infrastructure and reducing environmental effects 20 Chapter 3 – The north-south corridor 23 3.1 Targeted investment in infrastructure 23 3.2 North-south air service 25 Chapter 4 – The east-west corridor in south Wales 27 4.1 Targeted investment in infrastructure 27 4.2 Targeted proposals for south-east Wales 29 Chapter 5 – The east-west corridor in north Wales 31 5.1 Targeted investment in infrastructure 31 5.2 Targeted proposals for north-east Wales 32 Chapter 6 – The east-west corridor in mid-Wales 33 6.1 Targeted investment in infrastructure 33 Chapter 7 – Beyond 2015 35 Chapter 8 – Assessment and appraisal 37 1 National Transport Plan Foreword Foreword How people move about and transport goods is central to our economy and our way of life.