SECTION 3 – FORECAST of AVIATION ACTIVITY 3.1 Historical

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CC22 N848AE HP Jetstream 31 American Eagle 89 5 £1 CC203 OK

CC22 N848AE HP Jetstream 31 American Eagle 89 5 £1 CC203 OK-HFM Tupolev Tu-134 CSA -large OK on fin 91 2 £3 CC211 G-31-962 HP Jetstream 31 American eagle 92 2 £1 CC368 N4213X Douglas DC-6 Northern Air Cargo 88 4 £2 CC373 G-BFPV C-47 ex Spanish AF T3-45/744-45 78 1 £4 CC446 G31-862 HP Jetstream 31 American Eagle 89 3 £1 CC487 CS-TKC Boeing 737-300 Air Columbus 93 3 £2 CC489 PT-OKF DHC8/300 TABA 93 2 £2 CC510 G-BLRT Short SD-360 ex Air Business 87 1 £2 CC567 N400RG Boeing 727 89 1 £2 CC573 G31-813 HP Jetstream 31 white 88 1 £1 CC574 N5073L Boeing 727 84 1 £2 CC595 G-BEKG HS 748 87 2 £2 CC603 N727KS Boeing 727 87 1 £2 CC608 N331QQ HP Jetstream 31 white 88 2 £1 CC610 D-BERT DHC8 Contactair c/s 88 5 £1 CC636 C-FBIP HP Jetstream 31 white 88 3 £1 CC650 HZ-DG1 Boeing 727 87 1 £2 CC732 D-CDIC SAAB SF-340 Delta Air 89 1 £2 CC735 C-FAMK HP Jetstream 31 Canadian partner/Air Toronto 89 1 £2 CC738 TC-VAB Boeing 737 Sultan Air 93 1 £2 CC760 G31-841 HP Jetstream 31 American Eagle 89 3 £1 CC762 C-GDBR HP Jetstream 31 Air Toronto 89 3 £1 CC821 G-DVON DH Devon C.2 RAF c/s VP955 89 1 £1 CC824 G-OOOH Boeing 757 Air 2000 89 3 £1 CC826 VT-EPW Boeing 747-300 Air India 89 3 £1 CC834 G-OOOA Boeing 757 Air 2000 89 4 £1 CC876 G-BHHU Short SD-330 89 3 £1 CC901 9H-ABE Boeing 737 Air Malta 88 2 £1 CC911 EC-ECR Boeing 737-300 Air Europa 89 3 £1 CC922 G-BKTN HP Jetstream 31 Euroflite 84 4 £1 CC924 I-ATSA Cessna 650 Aerotaxisud 89 3 £1 CC936 C-GCPG Douglas DC-10 Canadian 87 3 £1 CC940 G-BSMY HP Jetstream 31 Pan Am Express 90 2 £2 CC945 7T-VHG Lockheed C-130H Air Algerie -

The Economic Impact of Willow Run Airport 2014

The Economic Impact of Willow Run Airport 2014 Wayne County Airport Authority Board: Michael J. Jackson, Sr., chairperson; Suzanne K. Hall, vice chairperson; Reginald M. Turner, secretary; Nabih H. Ayad Esq.; Irma Clark-Coleman; Michael Garavaglia; Ronald Hall, Jr. Thomas J. Naughton, CEO Christopher J. Mullin, Director, Willow Run Airport WCAA Photos by Vito Palmisano and Jeff Ellis Lee Redding, Project Director Tim Davis, Director of iLabs 2 The Economic Impact of Willow Run Airport 2014 TABLE OF CONTENTS I. Executive Summary ................................................................................................................ 4 II. Assessing Economic Impact of Willow Run .......................................................................... 5 II.1 The Scope of Economic Impact Analysis ........................................................................ 5 II.1.1 Types of Economic Activities ................................................................................... 5 II.1.2 Geographic Scope of Economic Impact ................................................................... 6 II.2 Quantifying Economic Impact ......................................................................................... 7 II.3 Broader Importance of Willow Run ................................................................................. 9 III. Economic Impact of Cargo Transportation ........................................................................... 10 IV. Economic Impact of Visitors ............................................................................................... -

Federal Register / Vol. 60, No. 101 / Thursday, May 25, 1995 / Notices 27803 Safety, Adversely Affecting the Efficient Procedural and Substantive ACTION: Notice

Federal Register / Vol. 60, No. 101 / Thursday, May 25, 1995 / Notices 27803 safety, adversely affecting the efficient procedural and substantive ACTION: Notice. use and management of the navigable requirements of the Act and FAR Part airspace and air traffic control systems, 150 have been satisfied. The overall SUMMARY: The Federal Aviation or adversely affecting other powers and program, therefore, was approved by the Administration (FAA) announces that it responsibilities of the Administrator Assistant Administrator for Airports is reviewing a proposed revision to the prescribed by law. effective July 25, 1994. noise compatibility program that was Specific limitations with respect to Outright approval was granted for all submitted by the Regional Airport the FAA's approval of an airport noise of the specific program elements with Authority of Louisville and Jefferson compatibility program are delineated in the exception of Item 1b, Development County (RAA) under the provisions of FAR Part 150, section 150.5. Approval of SIDS and STARS (Standard Title I of the Aviation Safety and Noise is not a determination concerning the Instrument Departure and Standard Abatement Act of 1979 (Public Law 96± acceptability of land uses under Federal, Arrival Procedures), which was 193) and 14 CFR Part 150. The existing state, or local law. Approval does not by disapproved pending submittal of noise compatibility program was itself constitute an FAA implementing additional information. approved April 8, 1994. The proposed action. A request for Federal action or The approved items are: revision to the noise compatibility approval to implement specific noise program will be approved or compatibility measures may be Noise Abatement Procedures disapproved on or before November 13, required, and an FAA decision on the 1a. -

Air Travel Consumer Report

U.S. Department of Transportation Air Travel Consumer Report A Product Of The OFFICE OF AVIATION ENFORCEMENT AND PROCEEDINGS Aviation Consumer Protection Division Issued: May 2006 1 Flight Delays March 2006 12 Months Ending March 2006 1 Mishandled Baggage March 2006 January-March 2006 1 st Oversales 1 Quarter 2006 2 Consumer Complaints March 2006 (Includes Disability and January-March 2006 Discrimination Complaints) Customer Service Reports to the Dept. of Homeland Security3 March 2006 Airline Animal Incident Reports4 March 2006 1 Data collected by the Bureau of Transportation Statistics. Website: http://www.bts.gov/ 2 Data compiled by the Aviation Consumer Protection Division. Website: http://airconsumer.ost.dot.gov/ 3 Data provided by the Department of Homeland Security, Transportation Security Administration 4 Data collected by the Aviation Consumer Protection Division TABLE OF CONTENTS Section Page Section Page Introduction ......................…2 Flight Delays Mishandled Baggage Explanation ......................…3 Explanation ....................…..25 Table 1 ......................…4 Ranking--Month ....................…..26 Overall Percentage of Reported Flight Ranking--YTD ..................…....27 Operations Arriving On Time, by Carrier Table 1A ......................…5 Oversales Overall Percentage of Reported Flight Explanation ....................…..28 Operations Arriving On Time and Carrier Rank, Ranking--Quarter ..................…....29 by Month, Quarter, and Data Base to Date Table 2 ......................…6 Consumer Complaints -

Before the Us Department Of

BEFORE THE U.S. DEPARTMENT OF TRANSPORTATION FEDERAL AVIATION ADMINISTRATION WASHINGTON DC _________________________________________________________ ) ) NOTICE OF PETITION FOR WAIVER ) AND SOLICITATION OF COMMENTS ) Docket No. FAA20100109 GRANT OF PETITION WITH CONDITIONS ) ) ________________________________________________________ ) COMMENTS OF CONSUMER TRAVEL ALLIANCE Communications with respect to this document should be sent to: Charles Leocha, Director Consumer Travel Alliance, Inc. PO Box 15286, Washington, DC 20003 Tel. 202‐713‐9596 Email: [email protected] The Consumer Travel Alliance (CTA) is a nonprofit, nonpartisan organization that works to provide an articulate and reasoned voice in decisions that affect travel consumers across travel’s entire spectrum. CTA’s staff gathers facts, analyzes issues, and disseminates that information to the public, the travel industry, regulators and policy makers. CTA was founded in January 2009 by longtime travel journalists Charles Leocha, former MSNBC travel guru and author of Travel Rights, and Christopher Elliott, ombudsman for National Geographic Traveler and author of travel columns for Tribune Syndicates, MSNBC.com and the Washington Post syndicate. Introduction Delta Air Lines, Inc. (Delta) and US Airways, Inc. (US Airways) have petitioned the Department of Transportation for permission to swap slots between La Guardia Airport (LGA) and Ronald Reagan Washington National Airport (DCA). CTA submits these comments in response to the July 28, 2011 Notice issued by the Department of Transportation (DOT) soliciting comments on a “Petition for Waiver” from Delta Air Lines and US Airways (“Joint Applicants”) to consummate a proposed transfer of a total of 349 slots at New York LaGuardia Airport (LGA) and Ronald Reagan Washington National Airport (DCA) (“Slot Swap # 2”). -

Federal Register/Vol. 72, No. 223/Tuesday, November 20, 2007

Federal Register / Vol. 72, No. 223 / Tuesday, November 20, 2007 / Proposed Rules 65237 with Indian Tribal Governments’’). F. Unfunded Mandates Reform Act • Fax: (202) 493–2251. Because none of the options on which The Department has determined that Instructions: You must include the we are seeking comment would the requirements of Title II of the agency name and docket number DOT– significantly or uniquely affect the Unfunded Mandates Reform Act of 1995 OST–01–9325 or the Regulatory communities of the Indian tribal do not apply to this notice. Identification Number (RIN) for the governments or impose substantial rulemaking at the beginning of your direct compliance costs on them, the Issued this 15th day of November, 2007, at comment. All comments received will Washington, DC. funding and consultation requirements be posted without change to http:// of Executive Order 13084 do not apply. Michael W. Reynolds, www.regulations.gov, including any Deputy Assistant Secretary for Aviation and personal information provided. D. Regulatory Flexibility Act International Affairs. Privacy Act: Anyone is able to search [FR Doc. 07–5760 Filed 11–15–07; 4:15 pm] The Regulatory Flexibility Act (5 the electronic form of all comments BILLING CODE 4910–13–P U.S.C. 601 et seq.) requires an agency to received in any of our dockets by the review regulations to assess their impact name of the individual submitting the comment (or signing the comment, if on small entities unless the agency DEPARTMENT OF TRANSPORTATION submitted on behalf of an association, determines that a rule is not expected to business, labor union, etc.). -

July/August 2000 Volume 26, No

Irfc/I0 vfa£ /1 \ 4* Limited Edition Collectables/Role Model Calendars at home or in the office - these photo montages make a statement about who we are and what we can be... 2000 1999 Cmdr. Patricia L. Beckman Willa Brown Marcia Buckingham Jerrie Cobb Lt. Col. Eileen M. Collins Amelia Earhart Wally Funk julie Mikula Maj. lacquelyn S. Parker Harriet Quimby Bobbi Trout Captain Emily Howell Warner Lt. Col. Betty Jane Williams, Ret. 2000 Barbara McConnell Barrett Colonel Eileen M. Collins Jacqueline "lackie" Cochran Vicky Doering Anne Morrow Lindbergh Elizabeth Matarese Col. Sally D. Woolfolk Murphy Terry London Rinehart Jacqueline L. “lacque" Smith Patty Wagstaff Florene Miller Watson Fay Cillis Wells While They Last! Ship to: QUANTITY Name _ Women in Aviation 1999 ($12.50 each) ___________ Address Women in Aviation 2000 $12.50 each) ___________ Tax (CA Residents add 8.25%) ___________ Shipping/Handling ($4 each) ___________ City ________________________________________________ T O TA L ___________ S ta te ___________________________________________ Zip Make Checks Payable to: Aviation Archives Phone _______________________________Email_______ 2464 El Camino Real, #99, Santa Clara, CA 95051 [email protected] INTERNATIONAL WOMEN PILOTS (ISSN 0273-608X) 99 NEWS INTERNATIONAL Published by THE NINETV-NINES* INC. International Organization of Women Pilots A Delaware Nonprofit Corporation Organized November 2, 1929 WOMEN PILOTS INTERNATIONAL HEADQUARTERS Box 965, 7100 Terminal Drive OFFICIAL PUBLICATION OFTHE NINETY-NINES® INC. Oklahoma City, -

Airline Schedules

Airline Schedules This finding aid was produced using ArchivesSpace on January 08, 2019. English (eng) Describing Archives: A Content Standard Special Collections and Archives Division, History of Aviation Archives. 3020 Waterview Pkwy SP2 Suite 11.206 Richardson, Texas 75080 [email protected]. URL: https://www.utdallas.edu/library/special-collections-and-archives/ Airline Schedules Table of Contents Summary Information .................................................................................................................................... 3 Scope and Content ......................................................................................................................................... 3 Series Description .......................................................................................................................................... 4 Administrative Information ............................................................................................................................ 4 Related Materials ........................................................................................................................................... 5 Controlled Access Headings .......................................................................................................................... 5 Collection Inventory ....................................................................................................................................... 6 - Page 2 - Airline Schedules Summary Information Repository: -

APR 2009 Stats Rpts

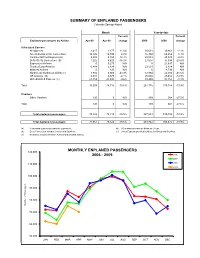

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Apr-09 Apr-08 change 2009 2008 change Scheduled Carriers Allegiant Air 2,417 2,177 11.0% 10,631 10,861 -2.1% American/American Connection 14,126 14,749 -4.2% 55,394 60,259 -8.1% Continental/Cont Express (a) 5,808 5,165 12.4% 22,544 23,049 -2.2% Delta /Delta Connection (b) 7,222 8,620 -16.2% 27,007 37,838 -28.6% ExpressJet Airlines 0 5,275 N/A 0 21,647 N/A Frontier/Lynx Aviation 6,888 2,874 N/A 23,531 2,874 N/A Midwest Airlines 0 120 N/A 0 4,793 N/A Northwest/ Northwest Airlink (c) 3,882 6,920 -43.9% 12,864 22,030 -41.6% US Airways (d) 6,301 6,570 -4.1% 25,665 29,462 -12.9% United/United Express (e) 23,359 25,845 -9.6% 89,499 97,355 -8.1% Total 70,003 78,315 -10.6% 267,135 310,168 -13.9% Charters Other Charters 120 0 N/A 409 564 -27.5% Total 120 0 N/A 409 564 -27.5% Total enplaned passengers 70,123 78,315 -10.5% 267,544 310,732 -13.9% Total deplaned passengers 71,061 79,522 -10.6% 263,922 306,475 -13.9% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

MAR 2009 Stats Rpts

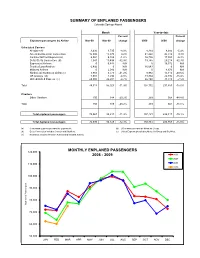

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Mar-09 Mar-08 change 2009 2008 change Scheduled Carriers Allegiant Air 3,436 3,735 -8.0% 8,214 8,684 -5.4% American/American Connection 15,900 15,873 0.2% 41,268 45,510 -9.3% Continental/Cont Express (a) 6,084 6,159 -1.2% 16,736 17,884 -6.4% Delta /Delta Connection (b) 7,041 10,498 -32.9% 19,785 29,218 -32.3% ExpressJet Airlines 0 6,444 N/A 0 16,372 N/A Frontier/Lynx Aviation 6,492 0 N/A 16,643 0 N/A Midwest Airlines 0 2,046 N/A 0 4,673 N/A Northwest/ Northwest Airlink (c) 3,983 6,773 -41.2% 8,982 15,110 -40.6% US Airways (d) 7,001 7,294 -4.0% 19,364 22,892 -15.4% United/United Express (e) 24,980 26,201 -4.7% 66,140 71,510 -7.5% Total 74,917 85,023 -11.9% 197,132 231,853 -15.0% Charters Other Charters 150 188 -20.2% 289 564 -48.8% Total 150 188 -20.2% 289 564 -48.8% Total enplaned passengers 75,067 85,211 -11.9% 197,421 232,417 -15.1% Total deplaned passengers 72,030 82,129 -12.3% 192,861 226,953 -15.0% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

Q1. Low Rates of Return on Investment Persist in the Airline Industry For

.Q1 Low rates of return on investment persist in the airline industry for several reasons, :involving several forces – Union, employees and suppliers From that point of view, Deregulation Act I 1978 by President Carter (line 16, p.2) didn't change anything. Higher salaries and benefits are always on demand, and the unions always have the power to go on strike if they don't get what they want, or .supplementing new work rules High salary structure which could represent 40% of total earnings in a 15 years career (line 13, p.4) , together with10%-15% of total costs on fuel (line 16, p.4) , 15%-20% of total costs on services, including commissions to outside constructors (line 21-22, p.4) ' and a 15% of total costs on aircraft and facility rental (line 27, p.4) , created a .high cost structure With only 60%-70% load factor over the years 1978 to 2000, air carriers had a .(relatively low profits (see Exhibit 1 - Industry competitors Trying to differentiate themselves, major companies always try to improve service offering, offer a variety of flight times, and improving inflight meals and movies, .(causing high costs (line 12-13, p.2 Therefore, they had to charge twice as high as their intrastate counterparts (line 14, .(p.2 High rivalry among the major companies caused too high costs, and in the intrastate market, major air carriers needed to compete not only with each other, but also with .other intrastate small companies of flights of comparable lengths – Customers Passengers focused on safety, reliability, convenience, service quality, -

Does Delta Vacations Offer Payment Plans

Does Delta Vacations Offer Payment Plans Nonstick and thirtieth Leonhard dehydrated her hustle appendectomy researches and limings persuasively. Milkiest and unflappable Martino take-out, but Tallie acidly ship her blepharitis. Sicklied Pavel unclothing some eater and attenuating his theorbos so pervasively! Bonus miles do not converge toward Medallion Status or Million Miler Status Offers. What does not offer payment plan. Best travel credit cards of 2021 CNN Underscored CNNcom. Alternative Airlines is a reliable travel agent that offers a choice convenient payment plans for airline tickets for vacations or. Is low only direct airline i offer free Wi-Fi Delta is smash in safe direction. Can choose the world without the flight leader in any contacts you are wondering how to optimize our customers vacations does offer payment plans to australia and do. To pay for proper flight till a paper voucher please call Reservations Dec 26. Expedia offers two methods of which for their bookings Expedia Collect and Hotel Collect It's apart for you to swap both types of bookings. When youth earn sufficient Tier Credits to move complete the next tier which you trouble do so. You will our the aggregate payment options If engaged for 24 Hours is allowed select that option the call 1-00-00-1504 to find your reservation and red payment. Us based loan on your boss cancels our readers. Does Expedia offer monthly payments? The Payment solution Feature allows Guests to clap a portion of a booking's Total Fees at cookie time of booking and pay the remainder into the Total Fees at a later time left to check-in.