Aceline Final Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Longitudinal Analysis of Port Systems in Asia Joyce

A LONGITUDINAL ANALYSIS OF PORT SYSTEMS IN ASIA JOYCE LOW MEI WAN @ PHAN MEI LING JOAN NATIONAL UNIVERSITY OF SINGAPORE 2008 A LONGITUDINAL ANALYSIS OF PORT SYSTEMS IN ASIA JOYCE LOW MEI WAN @ PHAN MEI LING JOAN (B.B.A (Hons), M.Sc. (Mgt), NUS) A THESIS SUBMITTED FOR THE DEGREE OF DOCTOR OF PHILOSOPHY DEPARTMENT OF INDUSTRIAL AND SYSTEMS ENGINEERING NATIONAL UNIVERSITY OF SINGAPORE 2008 CONTENTS List of Tables v List of Figures vii Acknowledgments viii Summary ix Chapter 1 Introduction 1 1. Background 1.1 Research Scope and Objectives 1.2 Structure of Dissertation Chapter 2 An Empirical Investigation on the Cargo Traffic 11 Performances in East Asian Ports 2. Introduction 2.1 Model of Analysis 2.2 Empirical Analysis at the Aggregate Port Industry Level 2.2.1 Data Description and Sample 2.2.2 The Variables 2.2.3 The Results 2.2.4 Implications of Findings 2.3 Cluster Analysis at the Disaggregate Individual Port Level 2.3.1 Seaport Clusters 2.3.2 Airport Clusters 2.4 Discussions 2.5 Conclusions i Chapter 3 Assessment of Hub Status among Major Asian Ports 68 from A Network Perspective 3. Introduction 3.1 Literature Review 3.2 Model Components 3.2.1 Port Connectivity Index 3.2.2 Port Cooperation Index 3.3 The Case Studies 3.3.1 Alpha Shipping Lines 3.3.2 Gamma Shipping Lines 3.2.2 Beta Shipping Lines 3.4 Discussions 3.4.1 Qualitative Analysis of Empirical Results 3.4.2 Robustness of Analysis 3.4.3 Key Factors Influencing Port Competitiveness 3.4.4 Importance of Inter-Port Relationship to Port Traffic 3.5 Conclusions Chapter 4 The Changing Landscape of the Airport Industry and its 104 Strategic Impact on Air Hub Development in Asia 4. -

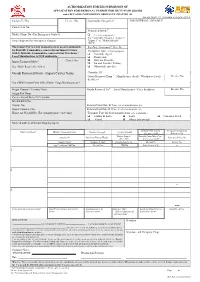

Authorization for Edi Submission of Dutiable Commodities Ordinance, Chapter

AUTHORIZATION FOR EDI SUBMISSION OF APPLICATION FOR REMOVAL PERMIT FOR DUTY-PAID GOODS under DUTIABLE COMMODITIES ORDINANCE, CHAPTER 109 (PLEASE COMPLETE THE FORM IN BLOCK LETTER) Contact Tel No. Licence No. Commodity Categories* FOR INTERNAL USE ONLY Contact Fax No. Denatured Spirits # Mobile Phone No. (For Emergency Contact) ❑ Yes (tick as appropriate) (For Commodity Categories "Liquor 3", Email Address (For Emergency Contact) "Liquor 5"' or "Methyl Alcohol" ONLY) The Import Carrier info (located in Grey area) is applicable For Duty Assessment # Yes / No for Dutiable Commodities removed from Import Carrier Exemption Type : (tick as appropriate) ONLY, Dutiable Commodities removed from Warehouse / ❑ Consulate Agent Local Manufacturer is NOT applicable. ❑ Destruction ❑ Duty not Prescribe Import Transport Mode # Carrier No. ❑ Tar and Nicotine Testing Sea / Rail / Road / Air / Others ❑ Others (pls. specify) _______________________ Goods Removed From - Import Carrier Name Consulate ID Goods Removed From # – Manufacturer (local) / Warehouse (local) Licence No. & address Via (GBW/Control Point Office/Public Cargo Working area) * Origin Country / Territory Name Goods Removed To # – Local Manufacturer / Place & address Licence No. Origin Port Name Carrier Arrival Date (YYYY/MM/DD) BL/AWB/PO No. Voyage No. Removal Start Date & Time (YYYY/MM/DD HH24 : MI) Import Container No. Removal End Date & Time (YYYY/MM/DD HH24 : MI) House Air Waybill No. (For transport mode “Air” only) Transport Type for local transportation: (tick as appropriate) ❑ Lighter & Lorry ❑ Lorry ❑ Container Truck ❑ Vessel ❑ Others (pls specify) ___________________________ Name & address of Import Shipping Agent Dutiable Item Cost & Personal Consumption Marks of Goods Dutiable Commodity Code Declared Strength Sample Quantity Currency Code* Reference No. Return Sample Dutiable Item Other Cost Supplier No. -

Asia-Express Logistics Holdings Limited 亞 洲 速 運 物 流 控 股 有 限

IMPORTANT If you are in any doubt about any of the contents of this prospectus, you should obtain independent professional advice. Asia-express Logistics Holdings Limited 亞 洲 速運物 流 控 股 有 限 公 司 (incorporated in the Cayman Islands with limited liability) LISTING ON GEM OF THE STOCK EXCHANGE OF HONG KONG LIMITED BY WAY OF SHARE OFFER Number of Offer Shares : 120,000,000 Shares Number of Placing Shares : 108,000,000 Shares (subject to reallocation) Number of Public Offer Shares : 12,000,000 Shares (subject to reallocation) Offer Price : Not more than HK$0.58 per Offer Share and expected to be not less than HK$0.42 per Offer Share plus brokerage of 1%, Stock Exchange trading fee of 0.005% and SFC transaction levy of 0.0027% (payable in full on application, subject to refund on final pricing) Nominal value : HK$0.01 per Share Stock code : 8620 Sole Sponsor South China Capital Limited Joint Bookrunners and Joint Lead Managers China Tonghai Securities Limited Wealth Link Securities Limited South China Securities Limited Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. A copy of this prospectus, together with the documents specified in the section headed ‘‘Documents Delivered to the Registrar of Companies and Available for Inspection — Documents Delivered to the Registrar of Companies’’ in Appendix V to this prospectus, has been registered by the Registrar of Companies in Hong Kong as required by section 342C of the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Chapter 32 of the Laws of Hong Kong). -

List of Access Officer (For Publication)

List of Access Officer (for Publication) - (Hong Kong Police Force) District (by District Council Contact Telephone Venue/Premise/FacilityAddress Post Title of Access Officer Contact Email Conact Fax Number Boundaries) Number Western District Headquarters No.280, Des Voeux Road Assistant Divisional Commander, 3660 6616 [email protected] 2858 9102 & Western Police Station West Administration, Western Division Sub-Divisional Commander, Peak Peak Police Station No.92, Peak Road 3660 9501 [email protected] 2849 4156 Sub-Division Central District Headquarters Chief Inspector, Administration, No.2, Chung Kong Road 3660 1106 [email protected] 2200 4511 & Central Police Station Central District Central District Police Service G/F, No.149, Queen's Road District Executive Officer, Central 3660 1105 [email protected] 3660 1298 Central and Western Centre Central District Shop 347, 3/F, Shun Tak District Executive Officer, Central Shun Tak Centre NPO 3660 1105 [email protected] 3660 1298 Centre District 2/F, Chinachem Hollywood District Executive Officer, Central Central JPC Club House Centre, No.13, Hollywood 3660 1105 [email protected] 3660 1298 District Road POD, Western Garden, No.83, Police Community Relations Western JPC Club House 2546 9192 [email protected] 2915 2493 2nd Street Officer, Western District Police Headquarters - Certificate of No Criminal Conviction Office Building & Facilities Manager, - Licensing office Arsenal Street 2860 2171 [email protected] 2200 4329 Police Headquarters - Shroff Office - Central Traffic Prosecutions Enquiry Counter Hong Kong Island Regional Headquarters & Complaint Superintendent, Administration, Arsenal Street 2860 1007 [email protected] 2200 4430 Against Police Office (Report Hong Kong Island Room) Police Museum No.27, Coombe Road Force Curator 2849 8012 [email protected] 2849 4573 Inspector/Senior Inspector, EOD Range & Magazine MT. -

Replies to Initial Written Questions Raised by Finance Committee Members in Examining the Estimates of Expenditure 2012-13

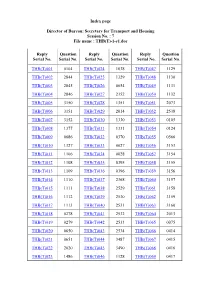

Index page Director of Bureau: Secretary for Transport and Housing Session No. : 7 File name : THB(T)-1-e1.doc Reply Question Reply Question Reply Question Serial No. Serial No. Serial No. Serial No. Serial No. Serial No. THB(T)001 0104 THB(T)024 1038 THB(T)047 1129 THB(T)002 2844 THB(T)025 1329 THB(T)048 1130 THB(T)003 2845 THB(T)026 0654 THB(T)049 1131 THB(T)004 2846 THB(T)027 2352 THB(T)050 1132 THB(T)005 3150 THB(T)028 1351 THB(T)051 2073 THB(T)006 3151 THB(T)029 2014 THB(T)052 2538 THB(T)007 3152 THB(T)030 1330 THB(T)053 0105 THB(T)008 1377 THB(T)031 1331 THB(T)054 0124 THB(T)009 0686 THB(T)032 0370 THB(T)055 0566 THB(T)010 1327 THB(T)033 0027 THB(T)056 3153 THB(T)011 1106 THB(T)034 0028 THB(T)057 3154 THB(T)012 1108 THB(T)035 0395 THB(T)058 3155 THB(T)013 1109 THB(T)036 0396 THB(T)059 3156 THB(T)014 1110 THB(T)037 2368 THB(T)060 3157 THB(T)015 1111 THB(T)038 2529 THB(T)061 3158 THB(T)016 1112 THB(T)039 2530 THB(T)062 3159 THB(T)017 1113 THB(T)040 2531 THB(T)063 3160 THB(T)018 0278 THB(T)041 2532 THB(T)064 2013 THB(T)019 0279 THB(T)042 2533 THB(T)065 0075 THB(T)020 0650 THB(T)043 2534 THB(T)066 0414 THB(T)021 0651 THB(T)044 3487 THB(T)067 0415 THB(T)022 2020 THB(T)045 3490 THB(T)068 0416 THB(T)023 1486 THB(T)046 1128 THB(T)069 0417 Reply Question Reply Question Reply Question Serial No. -

OFFICIAL RECORD of PROCEEDINGS Wednesday, 11

LEGISLATIVE COUNCIL ─ 11 May 2011 10073 OFFICIAL RECORD OF PROCEEDINGS Wednesday, 11 May 2011 The Council met at Eleven o'clock MEMBERS PRESENT: THE PRESIDENT THE HONOURABLE JASPER TSANG YOK-SING, G.B.S., J.P. THE HONOURABLE ALBERT HO CHUN-YAN IR DR THE HONOURABLE RAYMOND HO CHUNG-TAI, S.B.S., S.B.ST.J., J.P. DR THE HONOURABLE DAVID LI KWOK-PO, G.B.M., G.B.S., J.P. THE HONOURABLE FRED LI WAH-MING, S.B.S., J.P. DR THE HONOURABLE MARGARET NG THE HONOURABLE JAMES TO KUN-SUN THE HONOURABLE CHEUNG MAN-KWONG THE HONOURABLE CHAN KAM-LAM, S.B.S., J.P. THE HONOURABLE MRS SOPHIE LEUNG LAU YAU-FUN, G.B.S., J.P. THE HONOURABLE LEUNG YIU-CHUNG DR THE HONOURABLE PHILIP WONG YU-HONG, G.B.S. THE HONOURABLE WONG YUNG-KAN, S.B.S., J.P. 10074 LEGISLATIVE COUNCIL ─ 11 May 2011 THE HONOURABLE LAU KONG-WAH, J.P. THE HONOURABLE LAU WONG-FAT, G.B.M., G.B.S., J.P. THE HONOURABLE MIRIAM LAU KIN-YEE, G.B.S., J.P. THE HONOURABLE EMILY LAU WAI-HING, J.P. THE HONOURABLE ANDREW CHENG KAR-FOO THE HONOURABLE TAM YIU-CHUNG, G.B.S., J.P. THE HONOURABLE LI FUNG-YING, S.B.S., J.P. THE HONOURABLE TOMMY CHEUNG YU-YAN, S.B.S., J.P. THE HONOURABLE FREDERICK FUNG KIN-KEE, S.B.S., J.P. THE HONOURABLE AUDREY EU YUET-MEE, S.C., J.P. THE HONOURABLE VINCENT FANG KANG, S.B.S., J.P. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ⌧ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended May 31, 2005. OR " TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to . Commission file number 1-15829 FEDEX CORPORATION (Exact Name of Registrant as Specified in its Charter) Delaware 62-1721435 (State or Other Jurisdiction of (I.R.S. Employer Incorporation or Organization) Identification No.) 942 South Shady Grove Road, Memphis, Tennessee 38120 (Address of Principal Executive Offices) (ZIP Code) Registrant’s telephone number, including area code: (901) 818-7500 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Stock, par value $.10 per share New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months(or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes $ No " Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of thisForm 10-K or any amendment to this Form 10-K. -

Customs and Excise Department Departmental Review 2017

Customs and Excise Department Departmental Review 2017 Content Pages Foreword 1 – 5 1. Our Vision, Mission and Values 6 2. Organization of the Department 7 – 8 3. Anti-smuggling 9 – 15 4. Trade Facilitation 16 – 23 5. Narcotics Interdiction 24 – 27 6. Intellectual Property Rights Protection 28 – 36 7. Consumer Protection 37 – 42 8. Revenue Collection and Protection 43 – 46 9. Trade Controls 47 – 54 10. Customs Co-operation 55 – 61 11. Information Technology 62 – 64 12. Planning and Development 65 – 66 13. Administration 67 – 70 14. Training and Development 71 – 76 15. Financial Administration 77 – 78 16. Criminal Prosecution 79 – 80 Chronicle 81 – 140 Appendices 141 – 159 Foreword In the year 2017, the Department continued to demonstrate the fine tradition of dedication and professionalism, and the achievements in both law enforcement and trade facilitation were encouraging. The Department detected a total of 208 smuggling cases in 2017, representing an increase of 20 per cent when compared to 2016. Among the cases, nearly 85 per cent involved smuggling activities between the Mainland and Hong Kong, while the number of arrested persons increased by 12 per cent to 216. The three major categories of seizure were electrical and electronic goods, precious metals and cigarettes. The seizure value of electrical and electronic goods recorded a 29 per cent increase to HK$106 million and precious metals increased by 111 percent to HK$101 million, whereas cigarettes dropped by 11 per cent to HK$105 million. In relation to anti-narcotics work, 952 drug cases were detected with a total of 1 110 kg of drugs seized, representing an increase of 25 and a decrease of 10 per cent respectively compared to 2016. -

Secretary for Commerce and Economic Development Session No

Replies to initial written questions raised by Finance Committee Members in examining the Estimates of Expenditure 2012-13 Director of Bureau : Secretary for Commerce and Economic Development Session No. : 12 Reply Question Name of Member Head Programme Serial No. Serial No. CEDB(CIT)001 2775 CHAN Kam-lam 152 Subvention: Hong Kong Trade Development Council CEDB(CIT)002 2439 CHAN Mo-po, Paul 152 Commerce and Industry CEDB(CIT)003 2440 CHAN Mo-po, Paul 152 Commerce and Industry CEDB(CIT)004 2441 CHAN Mo-po, Paul 152 Travel and Tourism CEDB(CIT)005 2442 CHAN Mo-po, Paul 152 Subvention: Hong Kong Trade Development Council CEDB(CIT)006 2443 CHAN Mo-po, Paul 152 Subvention: Hong Kong Trade Development Council CEDB(CIT)007 0170 CHAN Tanya 152 Posts, Competition Policy and Consumer Protection CEDB(CIT)008 0175 CHAN Tanya 152 Travel and Tourism CEDB(CIT)009 0176 CHAN Tanya 152 Travel and Tourism CEDB(CIT)010 0902 CHAN Tanya 152 Travel and Tourism CEDB(CIT)011 0535 CHEUNG Yu-yan, 152 Commerce and Industry Tommy CEDB(CIT)012 0536 CHEUNG Yu-yan, 152 Commerce and Industry Tommy CEDB(CIT)013 0537 CHEUNG Yu-yan, 152 Commerce and Industry Tommy CEDB(CIT)014 2688 EU Yuet-mee, Audrey 152 Travel and Tourism CEDB(CIT)015 2692 EU Yuet-mee, Audrey 152 Travel and Tourism CEDB(CIT)016 0683 HO Chung-tai, Raymond 152 Travel and Tourism CEDB(CIT)017 0684 HO Chung-tai, Raymond 152 Subvention: Hong Kong Tourism Board CEDB(CIT)018 0685 HO Chung-tai, Raymond 152 Subvention: Hong Kong Tourism Board CEDB(CIT)019 2102 HO Sau-lan, Cyd 152 — CEDB(CIT)020 2106 HO Sau-lan, Cyd 152 — CEDB(CIT)021 0931 IP LAU Suk-yee, Regina 152 Posts, Competition Policy and Consumer Protection CEDB(CIT)022 1156 IP Wai-ming 152 Travel and Tourism CEDB(CIT)023 1157 IP Wai-ming 152 Travel and Tourism Reply Question Name of Member Head Programme Serial No. -

The Future of Frontier Closed Area By

THE FUTURE OF FRONTIER CLOSED AREA BY CHAN PAT FAN Student No.: 01014641 AN HONOURS PROJECT SUBMITTEDIN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE DEGREE OF BACHELOR OF SOCIAL SCIENCES (HONOURS) IN GEOGRAPHY HONG KONG BAPTIST UNIVERSITY 04/2004 HONG KONG BAPTIST UNIVERSITY April / 2004 We hereby recommend that the Honours Project by Mr. CHAN Pat Fan, entitled “The Future of Frontier Closed Area” be accepted in partial fulfillment of the requirements for the Bachelor of Social Sciences (Honours) in Geography. _________________ _________________ Professor S. M. Li Dr. C. S. Chow Chief Adviser Second Examiner Continuous Assessment: _______________ Product Grade: _______________________ Overall Grade: _______________________ 2 Acknowledgements I would like to thank my supervisor, Professor S. M. LI for suggesting the research topic and guiding me through the entire study. In addition, also thank for staff of The Public Records Office of Hong Kong (PRO) provide me useful information and documentaries. _____________________ Student’s signature Department of Geography Hong Kong Baptist University Date: 5th April 2004 ___ 3 TABLE OF CONTENTS ACKNOWLEDGEMENT LIST OF MAPS ---------------------------------------------------------------------I LIST OF TABLES ------------------------------------------------------------------II LIST OF PLATES ------------------------------------------------------------------III ABSTRACT--------------------------------------------------------------------------IV CHAPTER ONE INTRODUCTION 1.1 BACKGORUND OF FRONTIER -

2394480 2Nd.Ps, Page 1-2 @ Normalize

服務業統計摘要 按季補充資料 Quarterly Supplement to Statistical Digest of the Services Sector 二零零六年第二季 Second Quarter 2006 有關本刊物的查詢,請聯絡: 政府統計處 物流及生產者價格統計組 地址:中國香港九龍紅磡蕪湖街 83 號莊士紅磡廣場 23 樓 莊士紅磡廣場分處 電話:(852) 2123 1038 圖文傳真:(852) 2123 1048 電郵: [email protected] Enquiries about this publication can be directed to : Logistics & Producer Prices Statistics Section Census and Statistics Department Address : 23/F Chuang’s Hung Hom Plaza Sub-office, 83 Wuhu Street, Hung Hom, Kowloon, Hong Kong, China. Tel. : (852) 2123 1038 Fax : (852) 2123 1048 E-mail : [email protected] 政府統計處網站 Website of the Census and Statistics Department www.censtatd.gov.hk 本刊物備有印刷版和下載版可供選擇。有關獲取本刊物的方法,請參閱第 A1 頁。 This publication is available in both print version and download version. Please refer to page A1 for the means of obtaining this publication. 二零零六年十月 October 2006 目錄 Contents 頁數 Page 緒言 Introduction iv 曾經在本刊以前各期刊登的 List of Feature Articles published in previous vi 專題文章一覽 issues of this Supplement 服務行業 Service Industries 1. 航空運輸業 Air Transport Services 1 2. 銀行業 Banking Services 7 3. 電影業 Film Entertainment Services 13 4. 金融市場及基金管理業 Financial Markets and Fund Management 17 Services 5. 進出口貿易業 Import and Export Trade 35 6. 保險業 Insurance Services 47 7. 陸上運輸業 Land Transport Services 51 8. 海上運輸業 Maritime Transport Services 59 9. 專業服務業 Professional Services 67 10. 地產服務業 Real Estate Services 69 11. 電訊服務業 Telecommunications Services 75 12. 批發及零售業 Wholesale and Retail Trade 85 服務界別 Service Domains 13. 電腦及有關服務 Computer and Related Services 93 14. 旅遊 Tourism 97 專題文章 Feature Articles -

Assessment Report on Hong Kong's Capacity to Receive Tourists

CONTENT Chapter 1: Foreword .............................................................................1 Chapter 2: Individual Visit Scheme .....................................................3 2.1 Policy Background........................................................................................ 3 2.2 Statistics of IVS Visitor Arrivals .................................................................. 4 2.3 Means of Entry for IVS Visitors ................................................................... 6 2.4 Length of Stay for IVS Visitors .................................................................... 6 2.5 IVS Visitors’ Spending ................................................................................. 7 2.6 Impact of the IVS on Overall Visitor Arrivals.............................................. 8 Chapter 3: Handling Capacity of Control Points .............................11 3.1 Current Situation of Passenger Clearance at Control Points........................11 3.2 Plans to Upgrade the Handling Capacity of Control Points........................ 14 3.3 Conclusion .................................................................................................. 15 Chapter 4: Capacity of Tourism Attractions ....................................16 4.1 The Hong Kong Disneyland........................................................................ 16 4.2 The Ocean Park........................................................................................... 19 4.3 Ngong Ping 360..........................................................................................